Nina Shatirishvili/iStock via Getty Images

When I woke up this morning, I thought to myself “self, what do you think would brighten the readers’ collective day today?” No sooner had I posed the question to myself that an answer came back from some dark deep spot in my mind: “they would be absolutely thrilled to find out how your Wynn Resorts, Limited (NASDAQ:WYNN) short puts have worked out!” Because I’m absolutely obsessed with trying to give you people what you want, prepare to be absolutely thrilled by the story of my Wynn resorts short put trade. In my previous piece on Wynn Resorts, I bragged about how well my “avoid” recommendation had worked out. In case you’ve forgotten, the shares had underperformed the S&P 500 by about 41% after I told people to avoid them. I would have been content to spend the entire article bragging about that performance, but you selfish readers demand more, so I had to add more. I reviewed the financial performance, focusing on the debt and repayment schedule, and I looked at the valuation. I’ll do the same again today, while trying to work out whether or not it makes sense to buy the shares at current prices. Finally, the fact is that the above-mentioned puts are about to expire, and that reminds me to look at the options market yet again. I’ll write about that, and then probably sermonize about the risk reducing, yield enhancing potential of deep out of the money put options.

I put a “thesis statement” paragraph at the beginning of each of my articles as a service to my readers. Because I’m absolutely obsessed with making your lives as pleasant as possible, I want to try to save you time by giving you the highlights of my thinking up front. This will give you more time to do what you like, while helping you avoid some of my bragging, which some people find tedious for some reason. You’re welcome. Anyway, I’m of the view that investors would be wise to continue to avoid Wynn Resorts at current prices. The company has done marginally better so far in FY 2022 than the same period in 2021, but that’s hardly a barn burner performance given how bad 2021 was. Additionally, the debt rollover schedule is punishing at a very inopportune time. Worst of all, the stock is trading at valuations last seen in the 2015-2019 period when this was a much more profitable business. Finally, I write about my short put trade below. I think the $4.65 I earned from selling deep out of the money puts is a superior risk adjusted return to the $21 earned by stockholders, especially since the latter return will likely be taken away in the near term in my view. So, if you’re not yet actively using deep out of the money puts as a way to enhance returns and reduce risk, I would recommend you consider doing so. While I normally like to repeat success, the premia on offer for puts is too thin at the moment. I’ll review again when the shares inevitably drop in price from here. There it is. That’s my thesis statement. If you read on from here, that’s on you.

A Break In Financial History

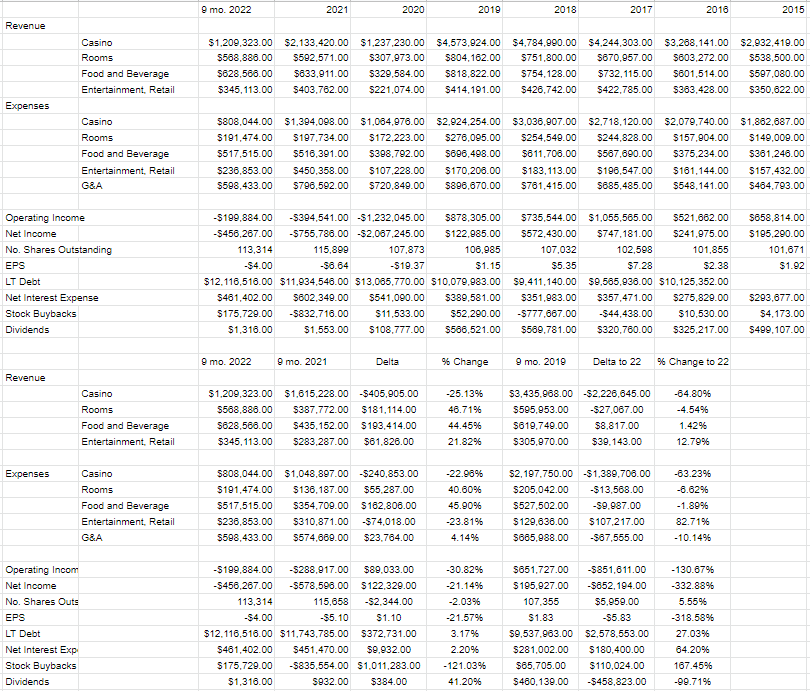

In my view, the most recent financial performance could be characterised as “mixed to bad.” Revenue during the first nine months of 2022 was up by about 1.1% relative to the same period in 2021, driven by huge increases in the three smaller lines of “Rooms” and “Food & Beverage”, and “Entertainment.” In spite of only a small improvement in sales, the company managed to reduce net losses by about 21% when compared to the same period in 2021. I’d suggest that their cost cutting efforts in “Casino” and “Entertainment & Retail” paid off well. So, an optimistic sort might suggest that the company is turning a corner. I’m not that sort. I’m the sort to point out that 2021 was hardly a banner year, so any comparisons to it should be taken with a large grain of salt. For instance, sales in 2021 were between 15% and 44% lower than any year between 2015 and 2019. Thus, beating 2021 is hardly worthy of praise in my view.

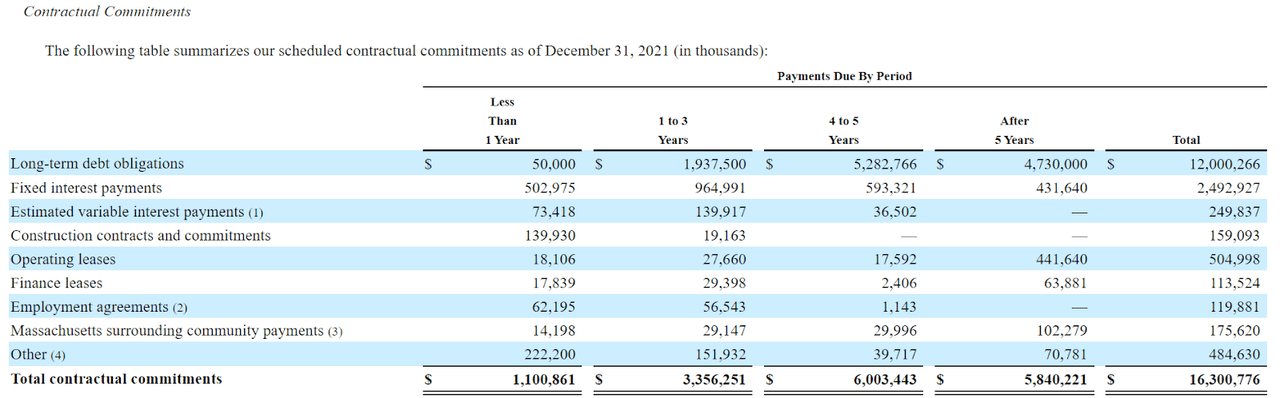

Turning to the capital structure, in my previous missive on the name, I liked the fact that the capital structure had improved from the last time I had reviewed the name. That’s a distant memory, given that debt exploded higher during the first nine months of the year. Additionally, as I pointed out in my previous missive, the debt repayment schedule is punishing over the next few years. We will have more detail on the schedule when it’s published in the next 10–K, but until then, I’ll republish the latest schedule once again for your enjoyment and edification.

Wynn Resorts Upcoming Debt Repayments (Wynn Resorts latest 10-K pp 52)

We see from the above that the company will be “on the hook” for an average of $1.678 billion in debt repayment this year and next. I don’t know if you’ve been following the financial news, but interest rates are a tad higher this year, so the timing of this debt rollover isn’t awesome. Thus the risk of leverage.

In conclusion, I think we should come to the view that this is no longer the same business as it was in 2019. While “Entertainment & Retail” are about 12.8% higher now than they were in 2019, overall, revenue has declined by 44.5% from the pre-pandemic era. The biggest loser is, of course, “Casino”, which is down 64.8% from the same period in 2019. I think the shares have value, but I think it would be foolish to apply the same multiples as the market did in 2019, for example. The Wynn of 2022 is certainly not the same animal as the Wynn of 2019, so I’d be willing to buy, but only at the right price.

Wynn Resorts Financials (Wynn Resorts investor relations)

The Stock

My regulars know that I’ve talked myself out of some profitable trades with the words “at the right price.” So, if you’re heading to the comments section to write about how my fastidiousness in this regard is self-harming, save yourself the effort because I’m way ahead of you. In response to this criticism, I’d point out that I’m of the view that it’s better to miss out on some gains than lose capital. My regulars also know that I consider the “business” and the “stock” to be quite different things. Every business buys a number of inputs and turns them into a final product or service. For instance, they may sell patrons a delicious meal before Bryan Adams sings at them. The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd’s rapidly changing views about the future health of the business, future demand for gaming services, future margins, and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about “the market” in general. A reasonable sounding, if counterfactual, argument can be made to suggest that shares of Wynn Resorts would have done even better since I wrote about them if the S&P 500 itself hadn’t dropped by about 13% since. It’s impossible to prove this point definitively, but it’s worth considering. In any case, the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it’s a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. In my experience, this is the only way to generate profits trading stocks: by determining the crowd’s expectations about a given company’s performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I’ve also found it’s the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by.

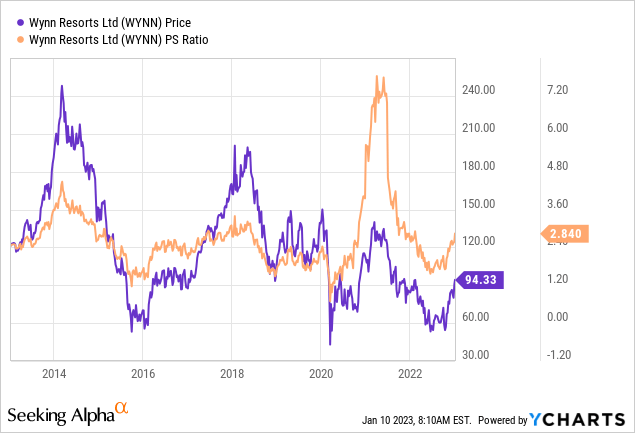

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. Now in the case of Wynn, things like “earnings” and “free cash flow” are non-existent at the moment, so I’m going to review the price to sales ratio. I want to see it trading at a fairly massive discount to both the S&P 500 and most definitely to its own past. Unhappily, that’s not what I see. I see the market is paying approximately the same for $1 of sales as it did during the much better years 2015-2019 per the following:

Source: YCharts

As my regulars also know, in order to validate (or refute) the idea that the shares aren’t objectively cheap, I want to try to understand what the crowd is currently “assuming” about the future of a given company. If the crowd is assuming great things from the company, that’s a sign that the shares are generally expensive. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit dense, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Anyway, applying this approach to Wynn Resorts at the moment suggests the market is assuming that this company will now grow profits at a rate of about 6.5% from here. Given the financial struggles we see here, I consider this to be a wildly optimistic forecast, and I must therefore recommend continuing to avoid the shares.

Options Update

In my previous missive on this name, I recommended selling the January 2023 puts with a strike of $55 because I was of the view that that represented a great entry price for this troubled firm. I earned $4.65 on each of these puts that were about 25% out of the money at the time of writing. The premia on these spiked as the shares rapidly lost value, they went “into the money” in the summer time a few times, but they have lost virtually all of their value, and are about to expire worthless. I think the trade worked out well. I also think it would have worked out well had I been exercised at $55 per share last summer. This “great outcomes either way” is why I refer to the strategy of selling deep out of the money put options to be a “win-win” trade. Specifically, I’ll only ever sell puts on companies I want to buy at prices I want to pay.

While I normally like to try to repeat success, I can’t in this instance. That’s because the premia on offer for reasonable strike prices is non-existent at the moment. For example, the June 2023 puts with a strike of $55 are only bid at $0.95 at the moment, which I consider to be too little given the risks present. For that reason, I’ll simply wait for what I consider to be an inevitable price decline, and will review the opportunity once again then.

That written, I want to remind investors that under the right circumstances, short puts are an excellent risk reducing, yield enhancing investment. The investor who purchased these shares at $73.50 last April saw their investment collapse by about 25% into the summer, while my short puts spiked a little bit. While the stock holder has earned more money, they certainly paid for that result in more grey hair and stress. Thus, I’m of the view that my $4.65 put premia is a superior risk adjusted return to the $21 stockholder return. I’m particularly firm in this view given that my returns can’t be taken away by a capricious market, whereas I think returns from the stock at current levels are tenuous at best at current prices.

Be the first to comment