ipopba/iStock via Getty Images

Quick Take On Wuxin Technology Holdings

Wuxin Technology Holdings (WXT) has filed to raise an undisclosed amount in an IPO of its Class A ordinary shares, according to an F-1 registration statement.

The firm provides a range of Internet of Things chips and related electronic smart products.

WXT has grown revenue, profits and operating cash flow and operated in a large and growing industry.

I’ll provide a final opinion when we learn more IPO details.

Company & Technology

Shenzhen, China-based Wuxin was founded to develop technical solutions to network computing products for Internet of Things applications.

Management is headed by Chairman and CEO Mr. Lianqi Liu, who was previously involved in the design and construction of a number of wide area and customer premise networks in China.

The company’s primary offerings include:

-

Chips

-

Modules

-

Antennas

-

Controllers

-

Smart hardware

-

Smart household devices

-

Other smart products

-

Licensed IP

Wuxin has booked a fair market value investment of $11.8 million as of June 30, 2021 from investors including a variety of senior management and investment companies.

Wuxin – Customer Acquisition

The company sells its products to a wide variety of customers and also provides related product design services to other manufacturers.

Wuxin also licenses its IP to companies seeking to incorporate the technology into their product or service plans.

Selling & Marketing expenses as a percentage of total revenue have risen slightly as revenues have increased, as the figures below indicate:

|

Selling & Marketing |

Expenses vs. Revenue |

|

Period |

Percentage |

|

FYE June 30, 2021 |

3.2% |

|

FYE June 30, 2020 |

3.0% |

(Source)

The Selling & Marketing efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Selling & Marketing spend, was 10.2x in the most recent reporting period. (Source)

Wuxin’s Market & Competition

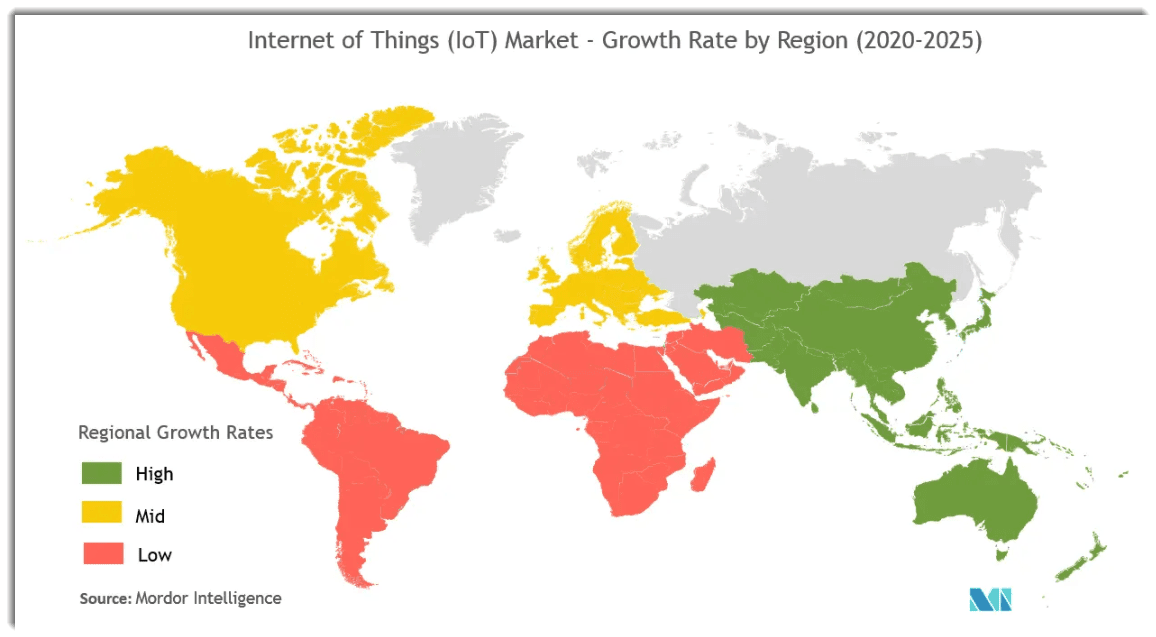

According to a 2020 market research report by Mordor Intelligence, the global market for IoT was valued at an estimated $761 billion in 2020 and is expected to reach $1.39 trillion in value by 2026.

This represents a forecast CAGR of 10.53% from 2021 to 2026.

The main drivers for this expected growth are an increasing adoption of IoT technologies across a wide range of industry verticals, including automotive, manufacturing and healthcare.

Also, a shift to manufacturing ‘Industry 4.0’ is placing an emphasis on complementing and augmenting human labor with robotics to reduce accidents and increase efficiencies.

Regional growth rates are estimated in the chart below:

Global Internet of Things Market (Mordor Intelligence)

Major competitive or other industry participants include:

-

Tuya Smart

-

Sunway Communication

-

Huizhou Shuobede Wireless Technology Co.

-

ShenZhen B&T Technology Co.

-

Harxon Corporation

-

Wunder Mobility

Wuxin Technology Holdings’ Financial Performance

The company’s recent financial results can be summarized as follows:

-

Growing topline revenue

-

Increasing gross profit and gross margin

-

Higher operating profit and margin

-

Growing cash flow from operations

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

FYE June 30, 2021 |

$ 46,977,350 |

47.6% |

|

FYE June 30, 2020 |

$ 31,833,721 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

FYE June 30, 2021 |

$ 15,025,075 |

52.3% |

|

FYE June 30, 2020 |

$ 9,863,152 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

FYE June 30, 2021 |

31.98% |

|

|

FYE June 30, 2020 |

30.98% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

FYE June 30, 2021 |

$ 6,241,267 |

13.3% |

|

FYE June 30, 2020 |

$ 3,345,881 |

10.5% |

|

Comprehensive Income (Loss) |

||

|

Period |

Comprehensive Income (Loss) |

Net Margin |

|

FYE June 30, 2021 |

$ 7,705,333 |

16.4% |

|

FYE June 30, 2020 |

$ 3,816,426 |

8.1% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

FYE June 30, 2021 |

$ 4,083,189 |

|

|

FYE June 30, 2020 |

$ 3,201,611 |

|

(Source)

As of June 30, 2021, Wuxin had $5.8 million in cash and $15.4 million in total liabilities.

Free cash flow during the twelve months ended June 30, 2021 was $2.8 million.

Wuxin’s IPO Details

Wuxin intends to raise an undisclosed amount in gross proceeds from an IPO of its Class A ordinary shares.

Class A ordinary shareholders will be entitled to one vote per share and Class B shareholders will have 10 votes per share.

The S&P 500 Index no longer admits firms with multiple classes of stock into its index.

No existing shareholders have indicated an interest to purchase shares at the IPO price.

Management says it will use the net proceeds from the IPO as follows:

20% for research and development;

50% for investment in technology infrastructure, marketing and branding, and other capital expenditure; and

30% for other general corporate purposes.

(Source)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management says the firm is not currently involved in any legal proceedings that would have a material adverse effect on its financial condition or operations.

The sole listed bookrunner of the IPO is Prime Number Capital.

Commentary About Wuxin’s IPO

WXT is seeking U.S. capital market investment to fund its general corporate expansion plans.

The company’s financials have produced increasing topline revenue, growing gross profit and gross margin, increasing operating profit and margin and higher cash flow from operations.

Free cash flow for the twelve months ended June 30, 2021 was $2.8 million.

Selling & Marketing expenses as a percentage of total revenue have risen a little as revenue has increased; its Selling & Marketing efficiency multiple was 10.2x in the most recent reporting period.

The firm currently plans to pay no dividends on its shares and anticipates that it will use its future earnings to reinvest back into its growth initiatives.

The market opportunity for Internet of Things products and services is extremely large and expected to grow at a significant rate of growth over the coming years, so the firm has strong industry dynamics in its favor.

Like other firms with Chinese operations seeking to tap U.S. markets, the firm operates within a WFOE structure or Wholly Foreign Owned Entity. U.S. investors would only have an interest in an offshore firm with interests in operating subsidiaries, most of which are located in the PRC. Additionally, restrictions on the transfer of funds between subsidiaries within China may exist.

The recent Chinese government crackdown on IPO company candidates combined with added reporting and disclosure requirements from the U.S. has put a serious damper on Chinese or related IPOs resulting in generally poor post-IPO performance.

Prospective investors would be well advised to consider the potential implications of specific laws regarding earnings repatriation and changing or unpredictable Chinese regulatory rulings that may affect such companies and U.S. stock listings.

Prime Number Capital is the lead underwriter and the only IPO led by the firm over the last 12-month period has generated a return of negative (9.0%) since its IPO. This is a lower-tier performance for all major underwriters during the period.

The primary risk to the company’s outlook is the continuing uncertain nature of the Chinese regulatory environment, especially with regard to listing in overseas markets.

When we learn more about the IPO, I’ll provide a final opinion.

Expected IPO Pricing Date: To be announced.

Be the first to comment