Delmaine Donson/E+ via Getty Images

Wix.com Ltd. (NASDAQ:WIX) has been a well-known web builder for a long time. As I covered in my last article, its sticky business model and cash-rich balance sheet should offer investors good returns. However, the overall market has dropped so much recently that lots of other SaaS (software as a service) bargains have emerged. I don’t know if WIX is still an attractive investment that can outperform its peers and deliver long-term growth given the product challenges and complexities of the new dynamics in the web builder market.

Editor X has come a long way to get here

WIX has been promoting its partner business using its premium web-building tool Editor X for a while. The management expects it as the main growth engine of the future, with a 31% YOY revenue increase last quarter. However, it’s been a long way for WIX to get here. From Code, and Corvid to now Editor X, WIX has rebranded this tool multiple times. When WIX first launched Editor X in the early times, they were not fully ready yet. I personally think WIX made a branding and reputation mistake as Steve Jobs has said, “good brands never ship junk.” Designers and developers found its limitations and led to a damaging reputation of being not responsive and esthetic. Some people claim that they would never want to work with it.

Although WIX has improved its Editor X product offerings and designs (maybe equal to Squarespace (SQSP)) recently, I don’t see the explosive and game-changing impact on the industry that it was supposed to be.

Closed garden vs. Open source

To be a true platform tool, development support is crucial. And this is what WIX Velo is doing, which offers so-called a full-stack, low code, and rapid development environment. However, WordPress still goes neck to neck with WIX regarding popularity and the number of websites built. As an open-source platform, WordPress is loved by a huge body of developers who build flexible and high-value websites. It definitely has more functionalities than WIX. When market opportunities emerge, WordPress always offers new plugins faster than WIX. This could be a concern for WIX (as a closed garden) who may have a difficult time keeping up with the various demands of future websites.

The good news is that WIX wins by better integrations and faster speed. It is also easier to maintain a website through WIX than through WordPress. Especially for an SMB who has no technical skills, Wix offers better tools.

WIX’s culture and edge on people are weakening

In the last ten years, WIX has grown from 300 employees to now 4700+. It is not a start-up anymore. CEO Avishai is awesome, but he cannot directly manage all of the vertical units, marketing, design, BI, and operations. It is inevitable that the company will be divided into teams like eCommerce, restaurants, development, content, etc. Each team will have to appoint a manager or head person in charge. Once you have more and more administrative layers, no decisions will be made fast. It is also gonna be harder to push initiatives which is a natural thing for bigger companies.

Historically, WIX has invested around 15% of revenue in Stock-Based Compensation while Shopify (SHOP) only had 7%. WIX’s employee amount doubled during 2020 and 2021 when the stock traded at around 300+. As the stock prices dropped from 340 to 60, people were losing money, which led to huge pressures on talent retention and company culture.

The other issue is the different landscape of Israel’s tech industry. WIX may still attract top-notch talent. However, it is not considered the sole big name for tech jobs anymore. You have global companies like Apple (AAPL), Google (GOOG, GOOGL), etc., and new emerging startups such as Elementor, Aspire, or Similarweb (SMWB), etc. It will be much tougher for WIX since Israel has a very start-up-friendly environment where a strong developer has lots of options to grow and get paid better.

The Agency business may not be as meaningful as expected

WIX’s agency business has a very promising start as agencies can have faster and more secure tools to manage their own clients and create sites. Especially for freelancing and SMBs who try to increase the volume of WIX websites, WIX would be a perfect fit. However, the real market space for WIX is still unclear. Bigger agencies that have development capabilities may not super interested in working with WIX. These agencies are different from DIY users; they are smarter and more sophisticated. Unless WIX’s products are ten times better than alternatives, WIX won’t have any pricing power.

More Competitive markets

The other concern is the competitive landscape. WIX is not just facing threats from Squarespace; Elementor, GoDaddy (GDDY), Webflow, Weebly and many others all have capabilities to catch up with WIX. I especially believe Elementor can make a change as a drag-and-drop page builder for WordPress. It has exponential growth and could be a great combination of both WIX and WordPress.

Moreover, WIX completed missed the eCommerce opportunity. Now, WIX has to compete with Shopify, BigCommerce (BIGC), WooCommerce, Magento, etc. It is an extremely tough space for it to win customers and market shares. As the chart below, WIX is having similar growth to SQSP but significantly behind BIGC and SHOP.

WIX and peers’ revenue growth (Seeking Alpha)

Bottom line

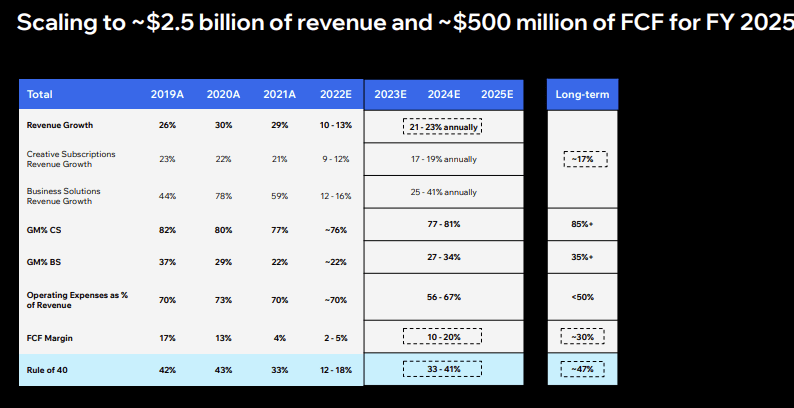

WIX has shared its three-year financial plan for 2025 (as the image below). It targets 2.5B revenue and 500M free cash flow. The long-term annual revenue growth target sets at 17%. The free cash flow margin sets at 30%. These numbers look amazing if WIX can achieve them.

WIX 2025 target (WIX presentation)

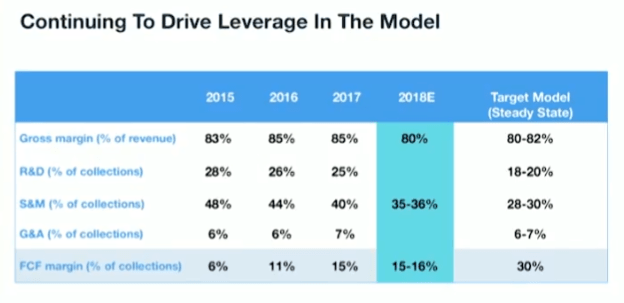

However, I don’t think WIX can control its destiny in this market. Looking back to its 2018 financial target, including 80% gross margin, 20% R&D, 30% S&M, and 7% G&A, these profitability numbers have never been achieved.

WIX financial target from 2018 (WIX presentation)

Overall, WIX is a cheap stock at this level, given a 3.4B market cap with 1.2B cash on its balance sheet. But I don’t see the strong growth capability and durability as before especially compared to other SaaS companies. Time is not WIX’s friend, and I see the business turning weaker in the next 10 years.

Be the first to comment