Fundamental Forecast for the US Dollar: Neutral

- Fed rate hike expectations have ratcheted higher in recent weeks. If the FOMC disappoints, the US Dollar may be in trouble.

- What makes the US Dollar so vulnerable to a FOMC disappointment? Positioning in the futures market – which remains near its longest level since October 2019.

- According to the IG Client Sentiment Index, the US Dollar has a mixed bias heading into mid-January.

US Dollar Week in Review

The US Dollar snapped back last week, with the DXY Index closing up by +0.49%, nearly eradicating its losses month-to-date (although remains -0.04% lower in January). With the drums of European war beating louder, EUR/USD rates notched a -0.62% loss, while GBP/USD rates fell by -0.86%. Weakness in risk assets duly stoked demand for safe havens, with USD/CHF rates dropping by -0.22% and USD/JPY rates slipping by -0.43%.

US Economic Calendar in Focus

The upcoming week’s economic calendar will prove consequential. The first Federal Reserve policy meeting of the year has already stoked a great deal of speculation in financial markets, with high expectations for hints of an accelerated rate of monetary tightening. Wednesday’s FOMC meeting could represent a significant turning point for a number, not just for the US Dollar, but for all currencies and asset classes.

- On Monday, January 24, the December US Chicago Fed national activity index will be released in the morning ahead of the January US Markit manufacturing PMI report.

- On Tuesday, January 25, the November US house price index is due 30-minutes ahead of the US cash equity open, while the January US consumer confidence gauge will be released 30-minutes after US stocks start trading.

- On Wednesday, January 26, weekly US mortgage applications data are due, as is the December US goods trade balance, ahead of the US cash equity open. December US new home sales figures will be released later in the morning. The January Federal Reserve rate decision and Fed Chair Jerome Powell’s press conference will arrive at 14 EST/19 GMT.

- On Thursday, January 27, the December US durable goods orders report, the initial 4Q’21 US GDP report, and weekly US jobless claims figures are due in the morning. December US pending home sales will also be released.

- On Friday, January 28, the December US PCE price index is due, as are December US personal income and personal spending figures. The January US Michigan consumer sentiment report is due later in the morning.

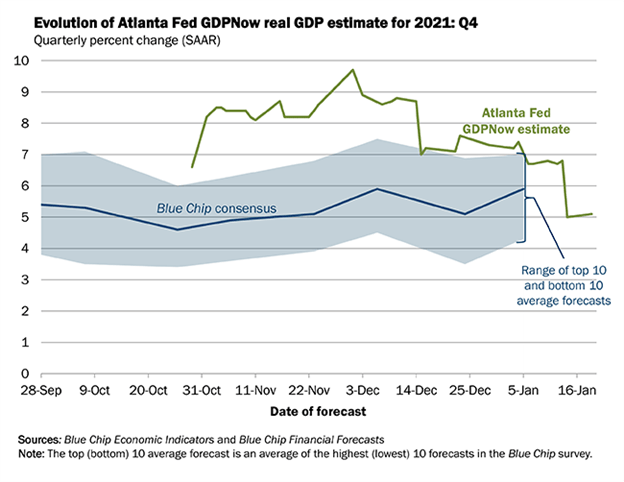

Atlanta Fed GDPNow 4Q’21 Growth Estimate (January 19, 2021) (Chart 1)

Based on the data received thus far about 4Q’21, the Atlanta Fed GDPNow growth forecast is now at +5.1% annualized, up from +5% on January 14. The upgrade was a result of “the nowcast of fourth-quarter real gross private domestic investment growth increased from +18.1% to +18.6%.”

The final update to the 4Q’21 Atlanta Fed GDPNow growth forecast is due on Wednesday, January 26 after the December US goods trade balance and December US new home sales figures are released.

For full US economic data forecasts, view the DailyFX economic calendar.

Market Pricing Points to Aggressive Fed

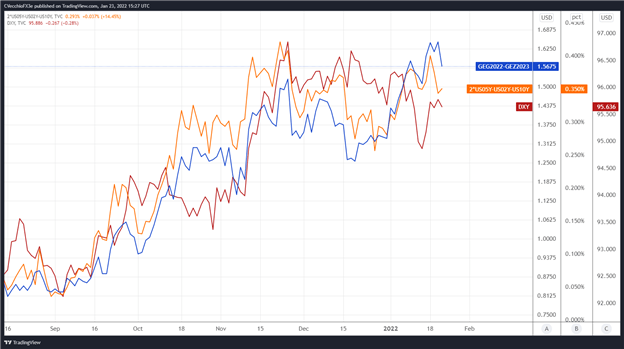

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 2 below showcases the difference in borrowing costs – the spread – for the February 2022 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (February 2022-DECEMBER 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Chart (August 2021 to January 2022) (Chart2)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are 156.75-bps of rate hikes discounted through the end of 2023 while the 2s5s10s butterfly is just off of its widest spread since the Fed taper talk began in June. Ahead of the January Fed meeting, rates markets are effectively pricing in a 100% chance of six 25-bps rate hikes and a 27% chance of seven 25-bps rate hikes through the end of next year. Furthermore, expectations for a 50-bps rate hike to start the hike cycle have edged higher in recent weeks.

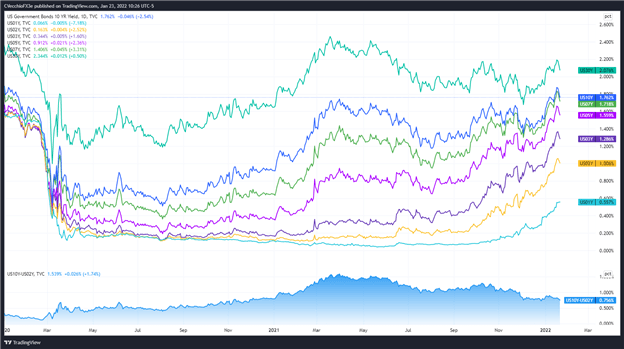

US Treasury Yield Curve (1-year to 30-years) (January 2020 to January 2022) (Chart 3)

The retracement in Fed hike odds coupled with declining US Treasury yields poses a problem for the US Dollar, however. If the FOMC makes clear that it will not hike rates by 50-bps in March, or suggests that inflation pressures are due to subside further – implicitly suggesting that aggressive tightening isn’t warranted – then the US Dollar remains vulnerable to another swing lower.

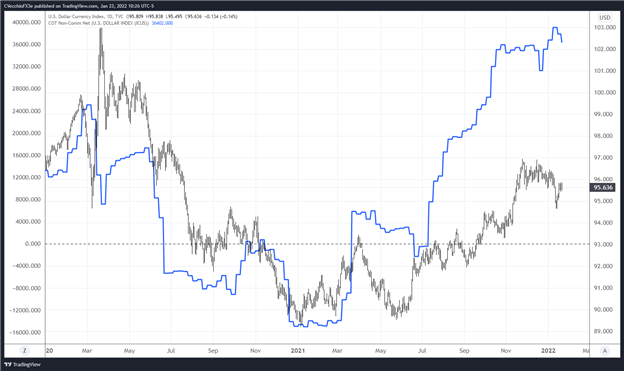

CFTC COT US Dollar Futures Positioning (January 2020 to January 2022) (Chart 4)

Finally, looking at positioning, according to the CFTC’s COT for the week ended January 18, speculators decreased their net-long US Dollar positions to 36,402 contracts from 37,860 contracts. Despite having fallen for two weeks, net-long US Dollar positioning remains near its highest level since October 2019, when the DXY Index was trading above 98.00. The oversaturated net-long position in the futures market remains a headwind for significant US Dollar upside in the near-term.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment