FactoryTh/iStock via Getty Images

In the months following Freeport-McMoRan Inc. (NYSE:FCX) posting Q3 results in Oct. 2022, shares gained nearly 60%. The copper producer outperformed the 9.05% return from the S&P 500 Index (SP500). At the time, some readers shared negative commentary on the miner’s prospects. The idea was that a combination of higher copper capacity and a recession would hurt prices.

The macroeconomic backdrop, however, changed sharply in the last quarter. The Chinese people protested China’s dynamic zero-Covid policy. In a partial response, the Chinese Communist Party reopened its borders. FCX stock benefited from the speculation that copper is among the commodities that will benefit from renewed Chinese demand.

What should investors make of Freeport-McMoRan’s fourth-quarter results? Analysts expected profit and revenue to fall. Instead, the firm beat expectations on both earnings per share and revenue.

Solid Execution By Freeport-McMoRan

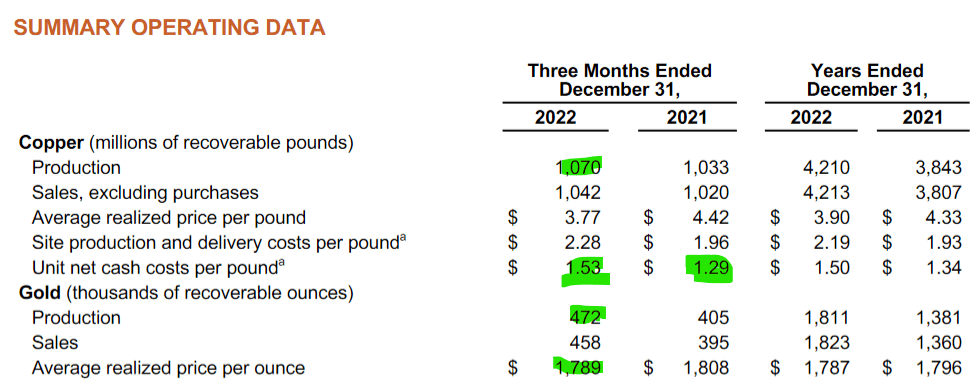

Freeport posted strong execution in the period. It posted an increase in gold and copper production. Although output rose, prices fell, as shown in the operating data below.

Freeport-McMoRan

Revenue fell from $6.16 billion last year to $5.76 billion in the quarter. Operating cash flow totaled $1.1 billion for the quarter and $5.1 billion for the year. The company expects operating cash flow to top $7.2 billion in 2023. The lower capital expenditure in 2023 gives Freeport many options to increase shareholder returns.

Freeport-McMoRan Inc. could pay down its debt this year. It ended 2022 with $10.6 billion in consolidated debt. With $8.1 billion in consolidated cash and cash equivalents, Freeport had $2.5 billion in net debt.

The company could continue its buyback program. It still has $3.2 billion left under its $5.0 billion share repurchase program. Freeport bought back $1.3 billion worth of shares or 35.1 million shares. This translates to an average price of $37.04. FCX stock traded at close to $46 at the time of writing and is not in value territory. Management may want to pause its stock buyback. Otherwise, it risks overpaying for the stock, should it correct on falling copper prices.

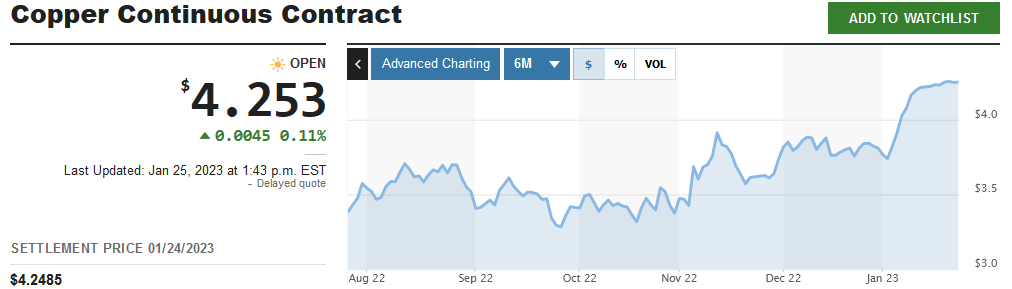

MarketWatch

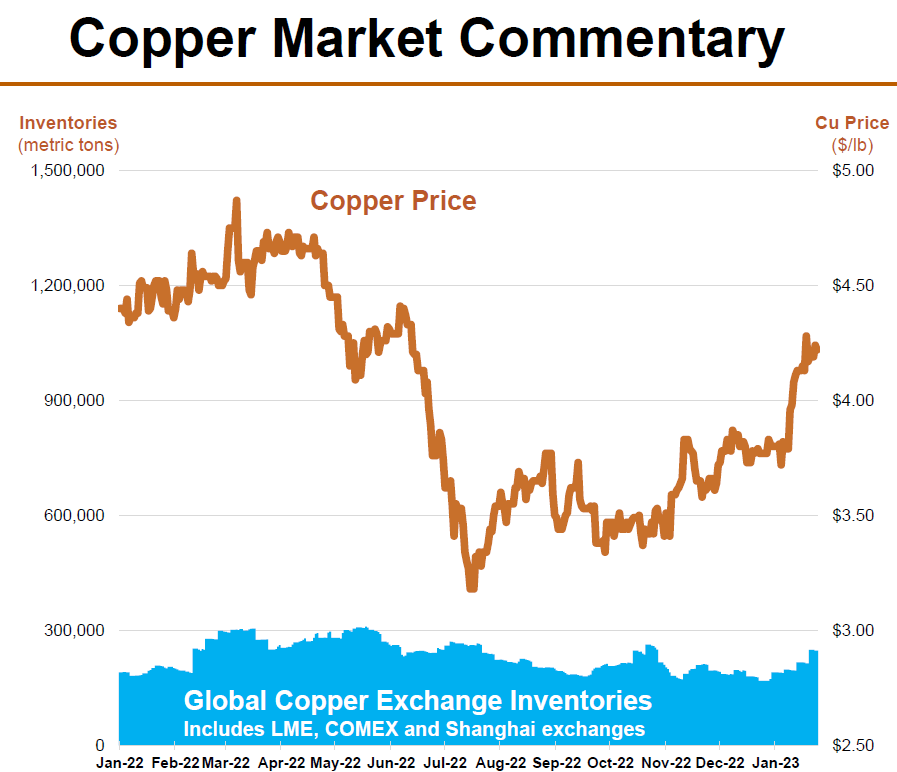

Above: copper continuous contract prices broke out in Nov. 2022, after China re-opened. Below, from the presentation: copper prices in the last year:

Freeport-McMoRan Q4 Presentation (Freeport-McMoRan Q4 Presentation)

China’s upcoming reopening is the basis for questioning the strong copper prices. The country is currently celebrating Chinese New Year. After the festivities end, the rise in Covid infections may disrupt the workforce.

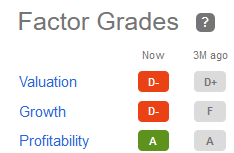

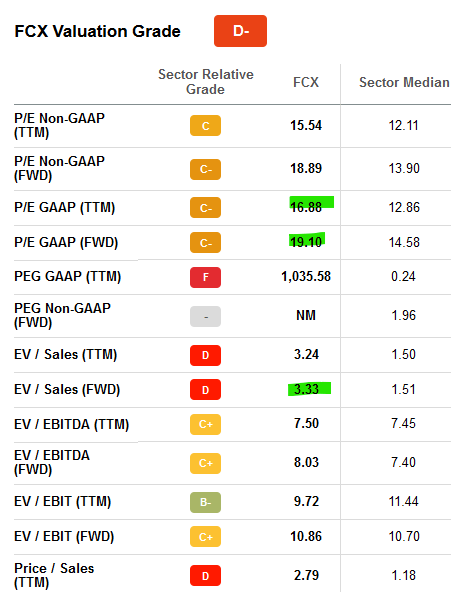

The stock grades below are warning shareholders that the growth and valuations are poor. Conversely, the company scores an A on profitability.

Seeking Alpha Premium

Digging deeper into the value scores, FCX stock has a P/E, forward P/E, and EV/Sales that are above the sector median:

FCX Valuation Grades (Seeking Alpha Premium)

Just as investors once paid a premium for the hyper-growth in technology in 2020-21, commodity investors are bidding FCX stock above the median.

Commodity Supercycle

Investors need to differentiate between the commodity supercycle and the breakdown in the U.S. Dollar Index (DXY).

FCX Chart (Seeking Alpha)

Copper prices rallied alongside the decline in DXY. In the coming weeks, the market will learn what is driving commodity prices higher. In the U.S., markets will digest the Federal Reserve’s interest rate policy discussion and its rate hike in the next month.

The Fed’s actions will have an impact on the economy. The next rate hike will slow activity in the quarters ahead. In addition, previous aggressive rate hikes will start to slow businesses from now through the next few months.

Opportunity

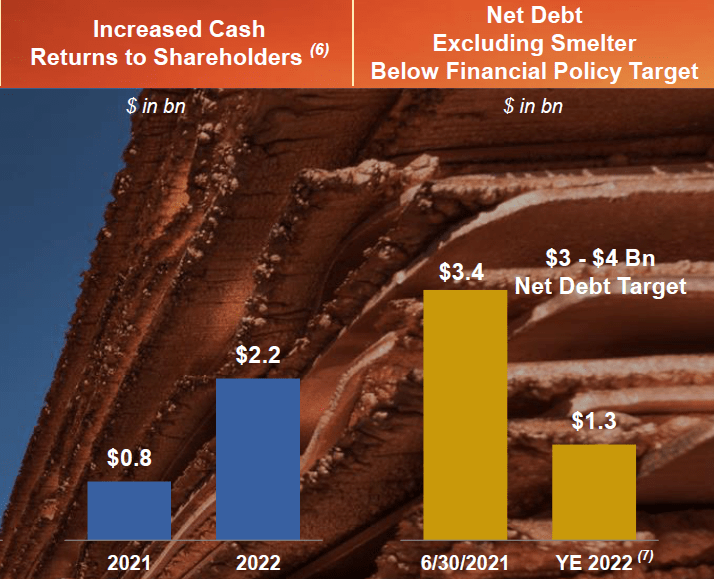

As mentioned above, Freeport increased its cash flow. It also has an aggressive net debt target. The sooner it de-leverages its balance sheet, the lower the risks in investing in this firm.

In the left chart below, management increased its cash returns to shareholders. It paid a $0.3 billion dividend and bought back $0.5 billion of shares in 2021. In 2022, it paid $0.4 billion in base dividends plus $0.4 billion in variable, performance-based dividends.

Freeport-McMoRan Q4/22 Presentation (Freeport-McMoRan Q4/22 Presentation)

This year, a rise in copper prices will lift Freeport’s cash flow. It might pay a bigger variable dividend.

Economic growth should increase demand for Freeport’s molybdenum business. It produced 85mm in 2022. Its mines produce high-purity, chemical-grade molybdenum concentrates.

The strong, long-term fundamentals are tailwinds. Physical demand remains strong amid low inventories. Clean energy technologies are secular growth drivers for metals. Government efforts to support decarbonization are a small but positive catalyst for Freeport.

Related Investments in Decarbonization

Investors seeking speculation may consider Babcock & Wilcox (BW), which won a carbon capture contract. To broaden exposure in the lithium metal and sulfur composite cathode, consider Solid Power (SLDP). It won a contract for battery cell development from the Department of Energy.

Investors may also click on the Peers tab to compare FCX stock to that of Southern Copper (SCCO) and Taseko Mines (TGB).

Risks

Global decarbonization is driving the use of copper. Should electric vehicle (“EV”) demand fall, copper demand in this segment may fall. Already, firms like Tesla (TSLA) have cut prices to spur demand. This might price other EV makers out of business. Their operating costs will rise as revenue per unit sold falls.

Your Takeaway

Freeport-McMoRan Inc. retains a buy rating. Copper prices show no signs of breaking down. The Chinese economy is about to rebound in 2023. This should increase demand for metals, lifting Freeport-McMoRan Inc.’s business.

Be the first to comment