kokkai/iStock Unreleased via Getty Images

Why Has Sea Limited Dropped In 2022?

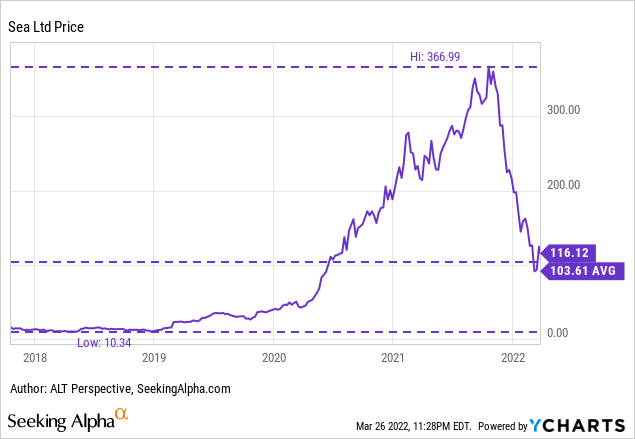

I wrote in mid-December on Sea Limited (NYSE:SE) warning readers against investing based on the “illusions of growth.” Some commented that I was late as its share price had already lost 42% from a recent peak. However, SE stock was shaved by more than half thereafter. Year-to-date alone, it has declined 48%.

Nonetheless, at the closing price of $116.12 on March 27, 2022, Sea Limited remains a profitable investment for early shareholders, including those who bought as late as mid-2020. After its IPO in 2017, SE stock had traded in the double-digit price range up until May 2020. Whether an investor has used dollar-cost-averaging [DCA] or simple averaging, he will be in a positive position as the share price of SE is currently above its all-time average of $103.61. SE stock is up six-fold since its IPO.

YCharts

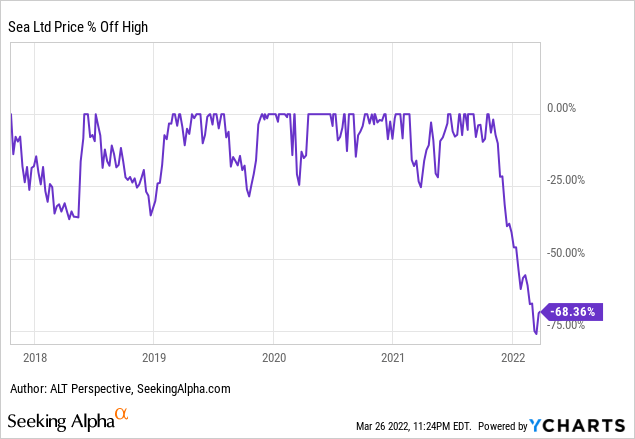

Traders who had adopted the buy-the-dip strategy before the fourth quarter of 2021 did well too, as SE stock rebounded each time even from dips of more than 25%. However, those who had expected to repeat the same strategy when SE lost more than 25% in December 2021 learned the hard way that “this time is different.”

YCharts

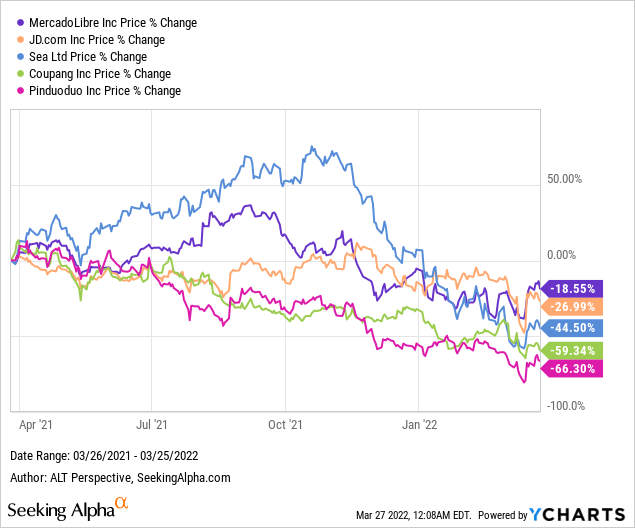

The current trying period for SE shareholders can be mainly attributed to the aversion towards non-profitable and weak profitability growth stocks, especially those deemed to have enjoyed pull-forward growth thanks to the pandemic. The peer group of Sea Ltd. suffered in the past months.

MercadoLibre, Inc. (MELI), the e-commerce giant of Latin America, declined 18.6% over the past year. Coupang (CPNG), dubbed the Amazon.com, Inc. (AMZN) of South Korea, plunged a whopping 59.3%. JD.com Inc. (JD) and Pinduoduo Inc. (PDD) were dragged down further by China-related woes, losing 27.0% and 66.3% respectively.

YCharts

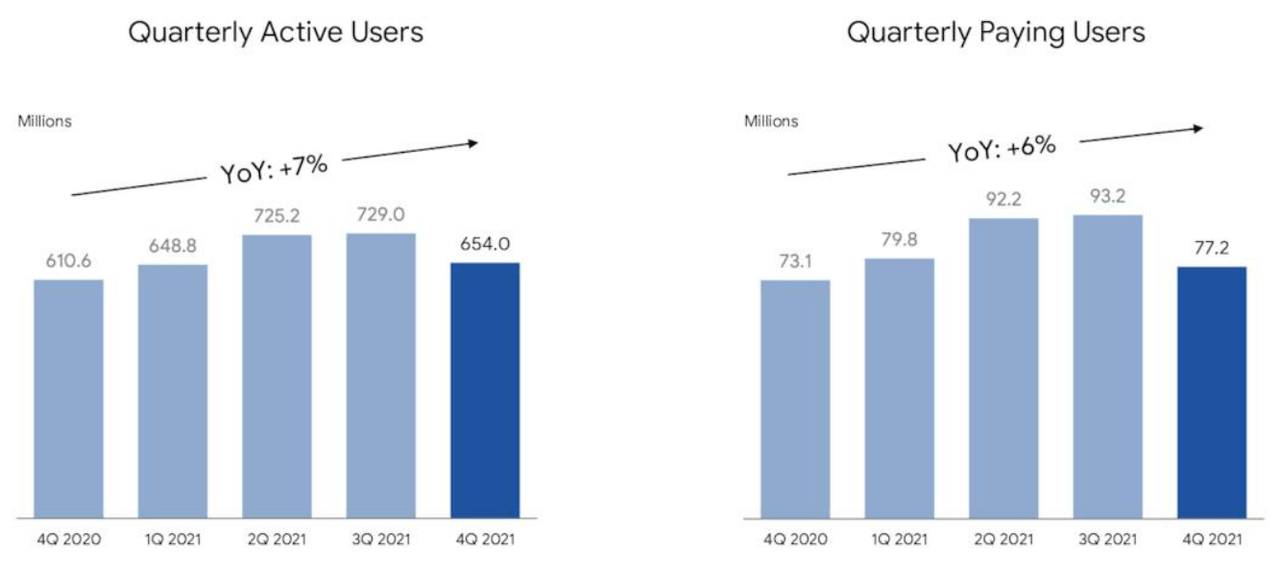

Company-specific weaknesses also played a major role in the downturn in SE stock. The Digital Entertainment division of Sea Limited has long been the sole profitable business enabling the company to invest in new growth but loss-making areas. Unfortunately, the cash cow gaming unit has experienced a significant quarterly decline in both the number of active users and paying users, spooking analysts and investors alike.

There were 654 million quarterly active users at the end of 2021, a mere 5.2 million more than the first quarter of the same year. The number of quarterly paying users at the end of 2021 was lower than the end of the first quarter of the same year.

Sea Limited

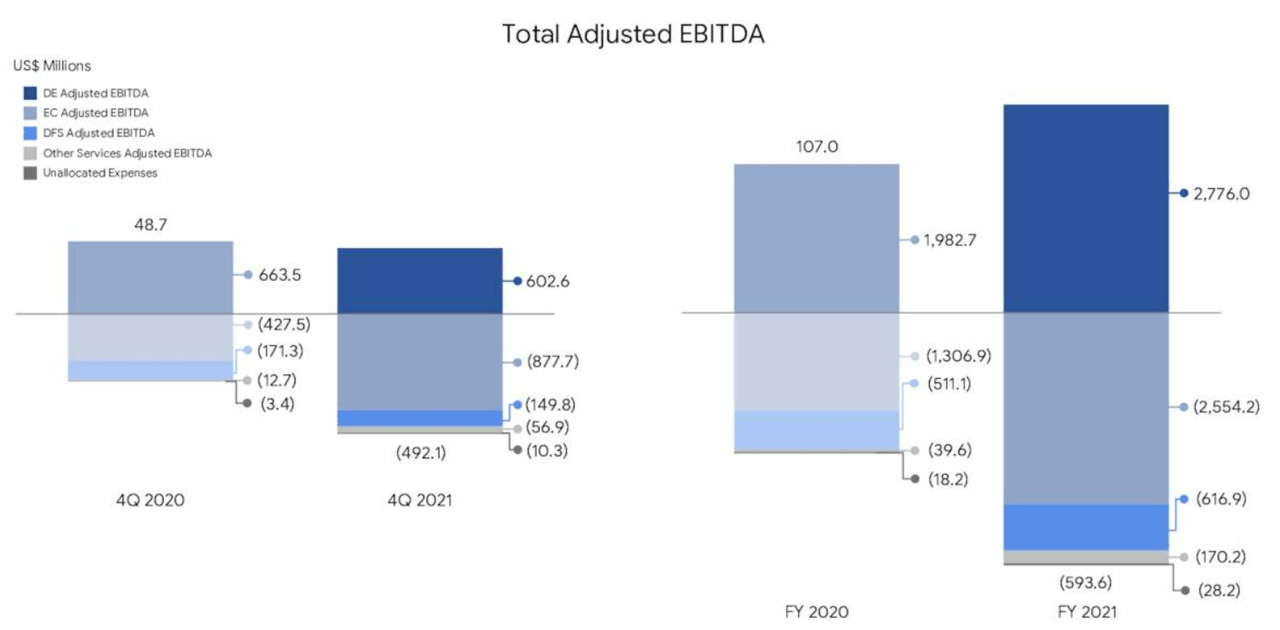

Even as losses on an adjusted EBITDA basis at the e-commerce unit mounted ($877.7 million in Q4 2021 versus $683.8 million in Q3 2021), the profitability at the gaming side shrunk to $602.6 million in Q4 2021 from $715.1 million in the previous quarter. Consequently, the net adjusted EBITDA loss ballooned to $492.1 million in Q4 2021 from $165.5 million in Q3 2021. This brought the full year 2021 adjusted EBITDA loss to a record loss of $593.6 million.

Sea Limited

The ongoing progress in the post-pandemic reopening globally will continue to negatively impact the availability of gamers as they have many more options to spend their time. This makes it hard to anticipate a rebound in the number of active users and paying users in the near term.

Sea Limited’s India ambition thwarted by Free Fire ban

Furthermore, Garena Free Fire, the flagship game of Sea Limited, has also been hit by a ban by the Indian government in mid-February for being “of Chinese origin.” Shareholders comforted themselves believing that the impact would be limited due to the small revenue contribution from India for Free Fire and that the newer Free Fire Max remained accessible. Market players and analysts had other thoughts, with SE stock tumbling 16% on the day of the news and J.P. Morgan cut its target on Sea to $250 from $420.

When I detailed in December last year how Sea Limited was regarded as Chinese, several readers vehemently protested. This came despite my acknowledgment that Sea Limited is Singapore-based and registered, and that the China-born co-founders became naturalized Singaporeans.

I cited in the article an exposé by a local media outlet describing Shopee Singapore as a “Chinese majority company,” where the managers reportedly insisted on Chinese (Mandarin) as the language of communication. The phenomenon was similarly covered by other publications subsequently. This is where the distinction with Zoom Video (ZM) is obvious. While Zoom Video’s founder, Eric Yuan, is also born in China, his management team was never filled with Chinese and the default language was not Mandarin.

Although the media attention was about the dominance of Chinese in terms of operations at Sea Limited’s Shopee, I highlighted that the Confederation of All India Traders (CAIT), an Indian trade body, was more concerned that the “complex structuring of entities is nothing but an attempt to hoodwink the Indian government and infuse Chinese funds into India.”

Apparently, the complaint by CAIT on Shopee has led the Indian government to believe Sea Limited’s gaming unit Garena to be similarly structured. The significant SE stake held by Chinese social media and gaming giant Tencent Holdings (OTCPK:TCEHY)(OTCPK:TCTZF) could have played a part in the misconception.

The paring of SE stake by Tencent and the relinquishing of special voting rights in January could have the opposite effect of reminding India of Sea Limited’s Chinese heritage. Tencent’s intention to hold onto the majority of its remaining stake may have assuaged shareholders but that kept the Indian government unnerved.

Furthermore, the Indian government may not appreciate the supposed changes in the “Chinese-ness” of Sea Limited with the increase in the total voting power held by Chairman/CEO and founder Forrest Li to 57% while Tencent’s voting power was reduced to less than 10%. Indian officials may be unconvinced that the China-born co-founders would not be beholden to Beijing, especially with their parents and relatives (possibly including their spouses) remaining Chinese nationals.

The media attention surrounding Eileen Gu, the American-born freestyle skier who competed for China in the recently concluded Beijing Winter Olympics, may have reinforced the thinking among Indian officials. Even though Gu was born, grew up, and still lives in California. Yet, she chose to represent China at the Olympics. Her story was widely reported in Asia, making it hard to miss.

Where Will Sea Limited Stock Be In 5 Years?

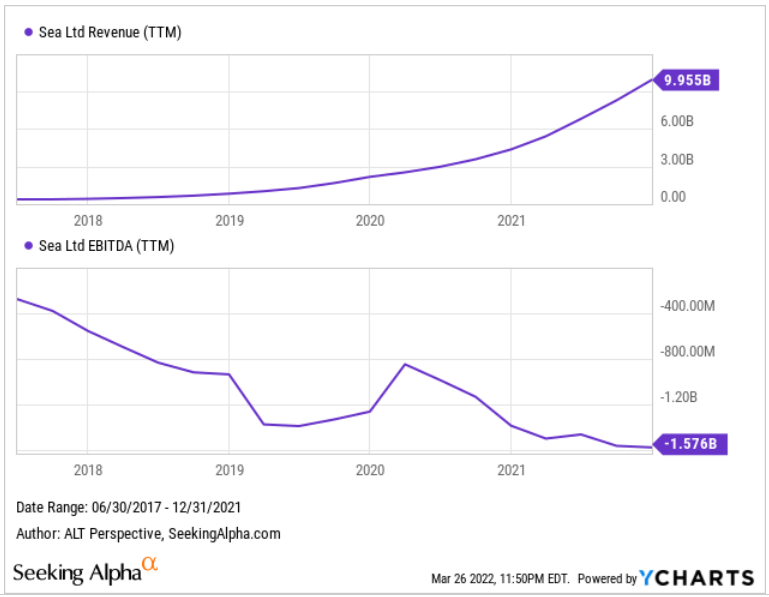

Sea Limited continues to invest in its businesses even as its profitable gaming unit slows down. Its EBITDA reached a new low of $1.58 billion on a twelve-month-trailing basis. Nonetheless, Sea Ltd has proven to be capable of growing its revenue exponentially, increasing to nearly $10 billion in 2021.

YCharts

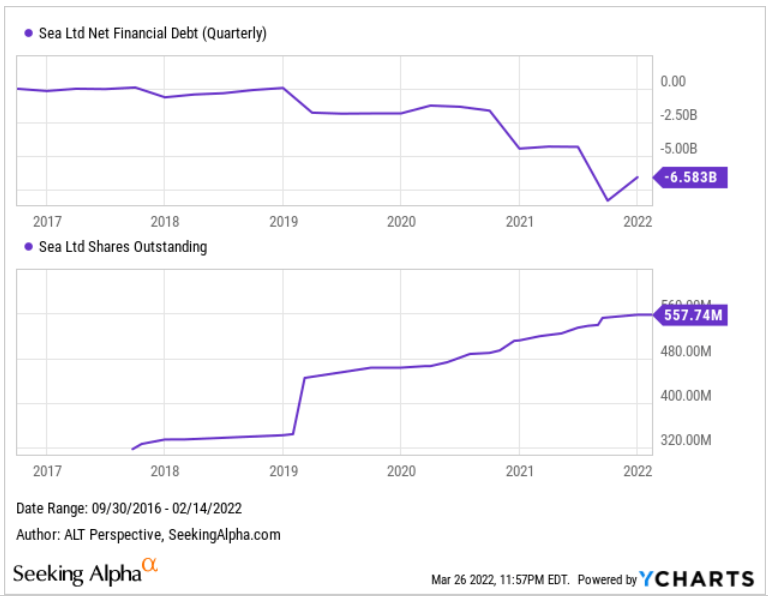

At the same time, the management of Sea Ltd shrewdly raised capital by selling shares at opportune times, helping to boost its net cash (reflected as negative net financial debt in the following chart). In the last exercise in September 2021, the company placed 11 million American Depositary Shares, each representing one Class A ordinary share, at $318/ADS, raising $3.5 billion.

Underwriters’ over-allotment was an additional 1.65 million ADSs. Sea Ltd also issued $2.5 billion of its 0.25% convertible senior unsecured notes due September 15, 2026, with over-allotment for an additional $375 million of notes. This provides the company with plenty of ammunition to last through more quarters of continued hemorrhaging amid a funding winter.

YCharts

SE stock is challenged in the short-term, as its quant rating suggests, amid the rise of regional super-apps

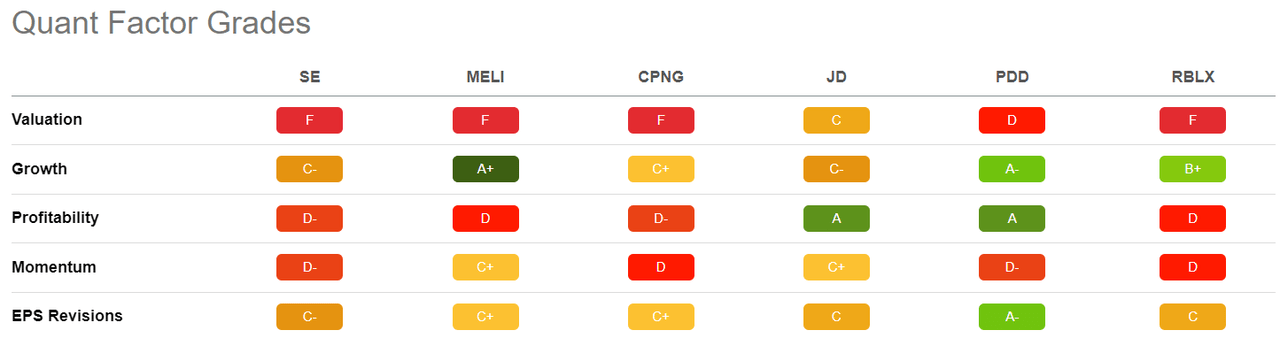

In the short term, the prospects for SE stock are dim. Its quant rating is Strong Sell, the same as its metaverse-wannabe Roblox (RBLX). However, that is the worst among the international e-commerce players, namely MELI, CPNG, JD, and PDD.

Seeking Alpha Premium

Looking into the factor grades, SE is deemed overvalued even as its stock has plunged nearly 70% from the peak. Its growth leaves much to be desired with a score of C-. Its profitability and momentum are understandably poor and deserving of D-.

Seeking Alpha Premium

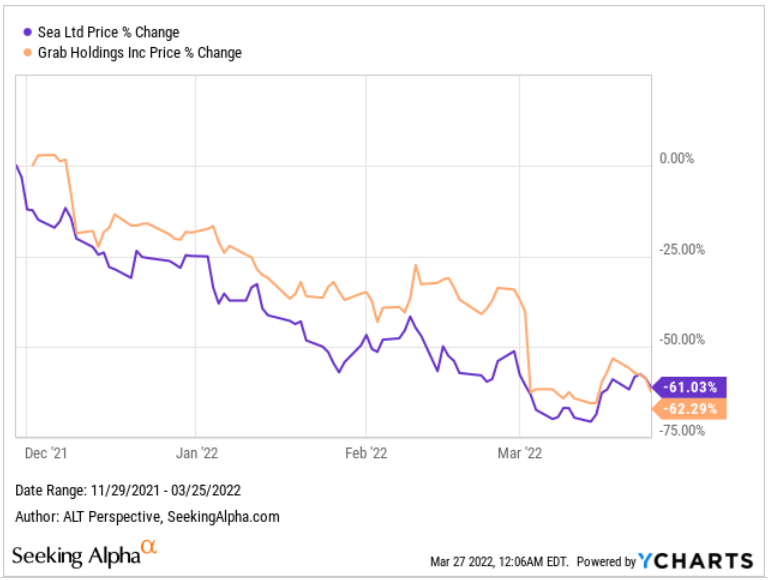

Meanwhile, regional super-apps are on the rise and becoming more powerful. Indonesia-based super-app GoTo Group (GOTO-INDONESIA), the regional e-commerce, ride-hailing, lifestyle services platform, and digital finance giant, has raised about $1.1 billion in a recent IPO. The public listing is expected to elevate its profile and attract more users while enabling the company to invest in its business to better compete with rivals such as Sea Limited.

GoTo’s IPO has also come hot on the heels of the December 2021 de-SPAC-ing of Grab Holdings Limited (GRAB). In less than four months, GRAB stock has declined by 62%, nearly mirroring the 61% fall of SE stock on the way down in the same period. GoTo’s stiff competition with Grab in the ride-hailing space is the most pronounced among their overlapping businesses.

YCharts

Unfortunately, the duo has to grapple with the soaring energy prices made worse by the Russia-Ukraine war. If Grab chooses to avoid a damaging fight with GoTo in ride-hailing, it may choose to redirect its resources to its e-commerce and digital finance arms, resulting in more competition for Sea Limited.

On the horizon, South Korea’s mobile financial platform Toss is also eyeing an expansion in Southeast Asia and India, according to Financial Times, as it evolves into a super app, challenging Grab, GoTo, and Sea Limited. South Korean e-commerce titan Coupang reportedly began operations in Singapore in July last year, beginning a series of steps to branch out into the Southeast Asian market.

Longer-term though, as we look five years out, Sea Limited may be in a much stronger position. During the Q4 2021 earnings conference call, Yanjun Wang, Group Chief Corporate Officer of Sea Ltd, said management was “looking at more and more markets turning profitable as we shared in terms of adjusted EBITDA before HQ cost allocation,” echoing Forrest Li’s belief that the company would “reach profitability across more markets and segments in 2022 and beyond.”

Wang also said that new games might be launched this year. Hence, shareholders can be assured that Sea Limited is not resting on its laurels, depending solely on Free Fire to propel the company forward. In the next five years, more games are expected to be launched. Even acknowledging that there will be hits and misses, the time frame should add to the successful franchises, while Sea Limited’s investments in game developers could also bear fruits.

Apart from India, SE stock is unaffected by the strong anti-China sentiment in the West. It doesn’t suffer from any threat of delisting or risk of investment ban. This means that the management has less to worry about, and will be able to focus on longer-term growth. Unlike pure SaaS companies, SE is often said to be profitable anytime they decided to cut down on aggressive expansion.

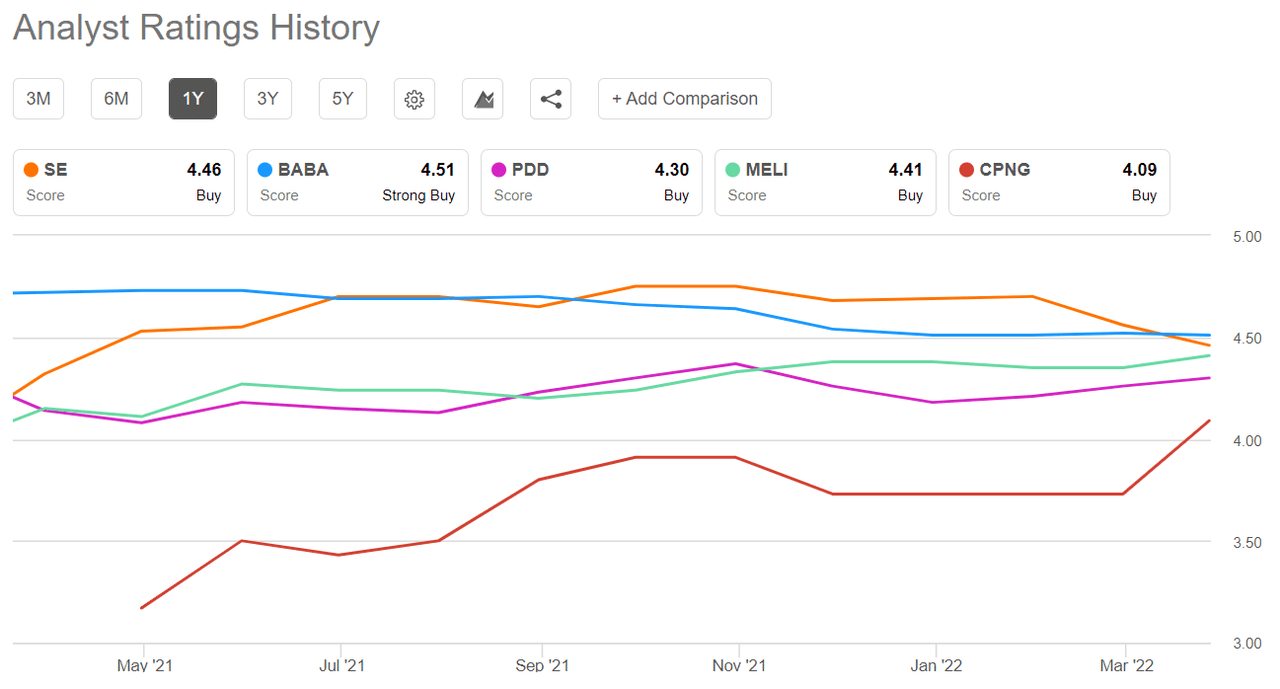

Wall Street analysts are confident about the stock’s prospects. SE has an analyst rating of 4.46 [Buy], surprisingly lower than the beleaguered Alibaba Group (BABA), but higher than the other international e-commerce players.

Seeking Alpha Premium

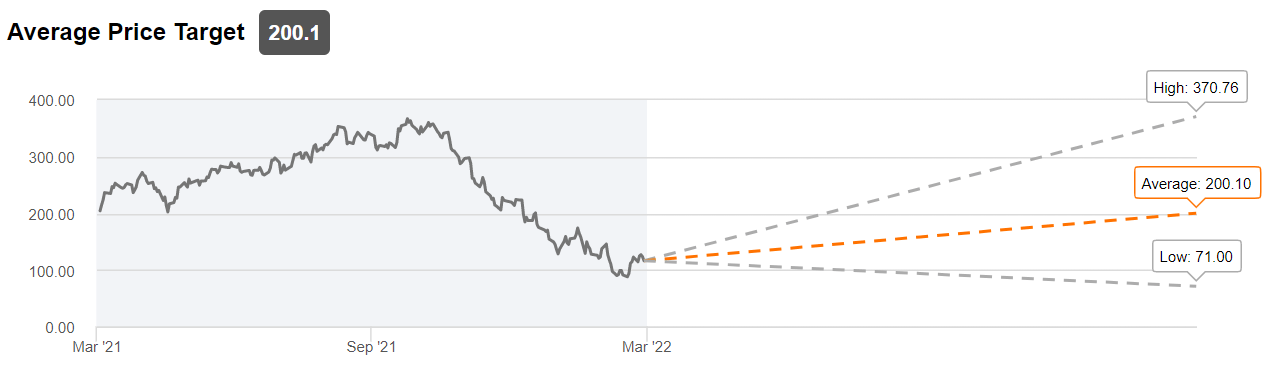

The average price target at $200.10 offers plenty of upside for SE which closed at $116.12 on March 27, 2022. The most bearish analyst has SE at $71 while the most bullish is expecting SE to reach $370.76.

Seeking Alpha Premium

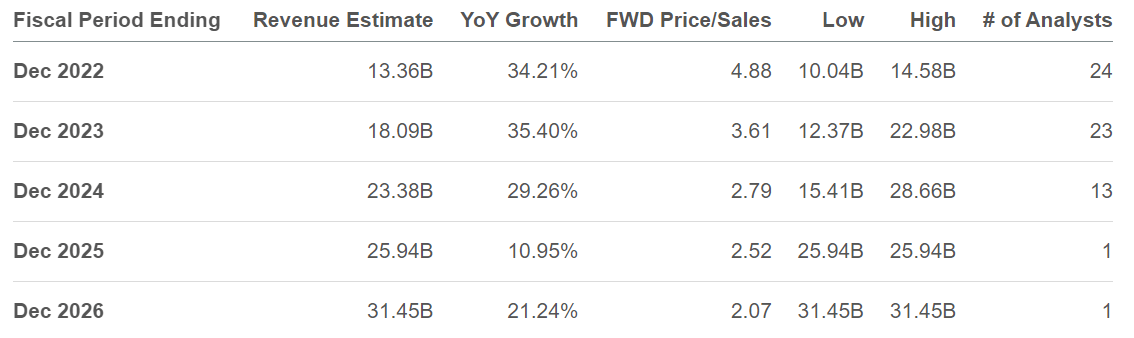

Analysts are projecting Sea Limited to more than double its revenue in the next five years on a consensus basis, from an estimated $13.4 billion in end-2022 to $31.5 billion in end-2026. If that materializes, it means SE stock is trading at a 5-year forward price-to-sales ratio of only 2.1 times.

Seeking Alpha Premium

While we only have a consensus EPS estimate to end-2024, we can see that analysts are already anticipating a clear improvement in Sea Limited’s earnings, with narrowing losses in the next couple of years and potentially EPS-positive by 2025.

Seeking Alpha Premium

Is SE Stock A Buy, Sell, or Hold?

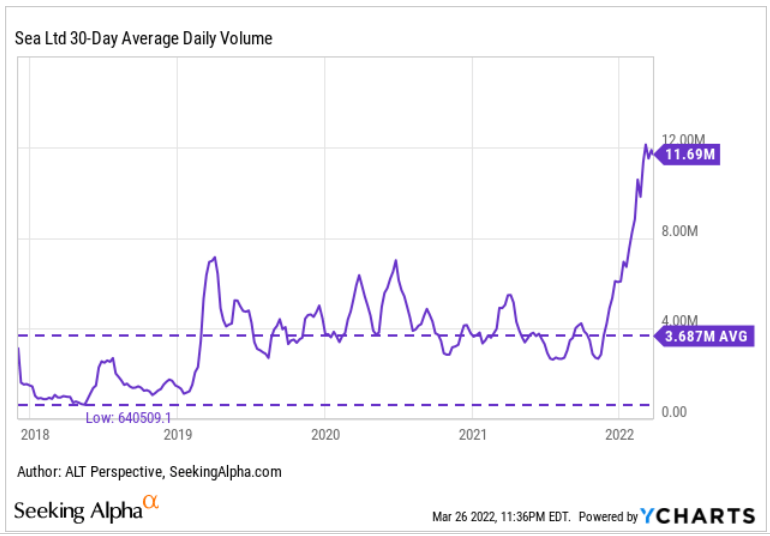

The 30-day average daily volume [ADV] of SE stock has soared from below three million in November 2021 to around 12 million currently. Since going public, SE stock saw only an average of 3.7 million 30-day ADV. Thus, this suggests that Sea Limited is getting more investor attention.

YCharts

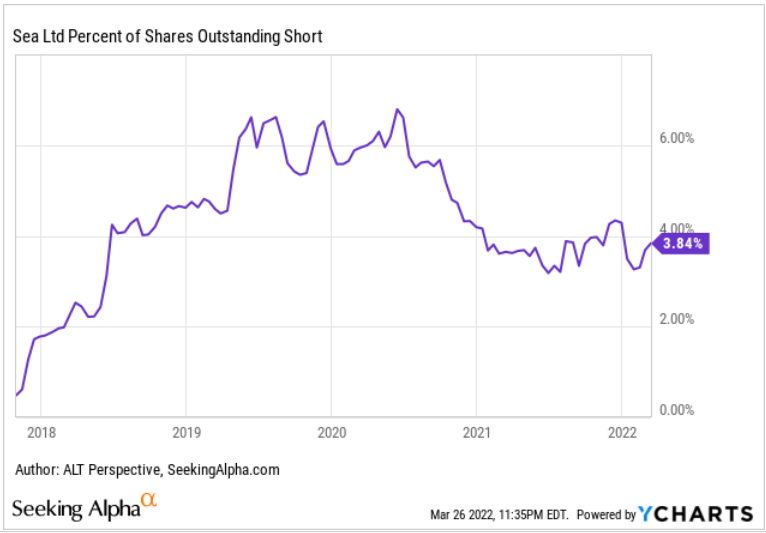

At the same time, SE stock is only getting 3.8% of its shares outstanding short. This is around the average level throughout 2021. Thus, short-sellers don’t seem to be pouncing on Sea Ltd. The heightened trading volume is probably a result of early investors taking profit, late investors taking advantage of tax-loss selling, and bargain hunters.

YCharts

If the large trading volume indicates a shakeout in the shareholder mix, such that there are more institutional investors, it is a positive for SE stock as they are deemed to be longer-term players than retail investors. The changing of hands is also a positive since new shareholders typically have more patience to wait out the volatility.

Although I listed several challenges facing Sea Limited in the previous section, I believe SE stock has a good potential to be rewarding to investors in five years. Sea CEO Forrest Li reassured employees in mid-March that the plunge in SE stock “is short-term pain that we have to endure to truly maximize our long-term potential.”

Time heals all wounds, the adage goes. The scrutiny on the growth-at-any-cost approach adopted by the SaaS and platform companies would make the executives across the industry sit up and re-evaluate their strategies. This could make the participants like Sea Limited more sustainable and attractive over the next few years.

Barring further deterioration in the geopolitical climate and fresh global black swans, the valuation of SE stock seems to have bottomed. Although I remain short-term bearish, the five-year horizon this article is looking at makes it more reasonable to call SE stock a ‘buy’ than a ‘hold’. The proven track record of Sea Limited’s management slate bodes well for SE’s stock, which could be a multi-bagger for those who are patient.

Be the first to comment