Wheels Up is a strong player in the private aviation space. gremlin

Flying can be akin to roulette these days. Flight cancellations due to coronavirus restrictions, pilot shortages, and weather delays are widespread. Thousands of flights have been delayed or canceled this summer. In fact, more flights in 2022 have been canceled through mid-year 2022 than all of 2021.

In addition, some airports have capped the number of departing passengers. Schiphol Airport in Amsterdam has capped passengers to 67,500 per day, while Heathrow Airport in London has capped the number of departing travelers to 100,000 per day.

Flight cancelations in the United States continue to be significant as well. La Guardia Airport tops the list with 8% of flights canceled. Newark Liberty International, St. Louis Lambert International, and Raleigh-Durham International had 6% of their flights canceled.

Still, corporate executives and wealthy individuals want and need to travel. We believe that the private aviation industry is absorbing that demand. In our opinion, many of these CEOs and wealthy individuals may find that once they experience private aviation, they don’t want to return to traditional airports. Wheels Up Experience Inc. (NYSE:UP) has strong brand recognition and is set to continue to be a lead player.

Robust, experienced leadership and attractive valuation make Wheels Up a buy for us at these levels.

Disclosure: Risks of Investing in Microcap Stocks

With a share price of less than $3 and a market capitalization of just $500 million, Wheels Up is considered a microcap stock. There are many risks in investing in microcap stocks, including increased volatility and potential lack of liquidity. While we recommend Wheels Up as a medium-term investment, we urge investors to approach Wheels Up cautiously and as part of a larger, balanced investment strategy. We would not recommend this stock to risk-averse or conservative investors.

Wheels Up Experience Inc. Overview

Wheels Up Experience is one of the largest private aviation companies, providing a comprehensive portfolio of services to non-owner fliers as well as jet owners. The company has over 200 aircraft in their owned and leased fleet, and offers access to over 1,200 third-party aircraft, including multiple aircraft types and categories. This includes aircraft in the jet light, mid-size jet, super mid-sized jet, and large cabin jet categories. The company also maintains a strategic partnership with Delta Air Lines (DAL).

Their app enables travelers to search and book flights quickly from their smartphones. Their membership program offers clients enhancements like empty-leg hot flights, flight sharing, shuttle flights, company events, and other member benefits from luxury brands.

In addition to simplifying the experience, acquisitions have been a part of their growth. In May 2019, Wheels Up acquired Travel Management Company, which is a light jet operator in Indiana. In September 2019, the company acquired Avianis, a flight management system provider. In 2020, the company acquired Delta Private Jets, which is Delta’s private aviation branch. This gave Delta a 27% equity stake in Wheels Up. In March 2020, Wheels Up acquired Gama Aviation Signature, and in 2021, it purchased Mountain Aviation, which provides maintenance and operation services for Cessna Citation Xs.

Wheels Up reported $1.2 billion in revenue for 2021. This is up significantly from $695 million in 2020 and $385 million in 2019.

Wheels Up Experience Financial Overview

On May 21, Wheels Up reported its first quarter financial results for the period ended March 31, 2022:

- Revenue grew to $325.6 million for an increase of 24%

- Active members reached 12,424 for an increase of 25%

- Live flight legs were 17,625 for an increase of 26%

- Net loss was $56.8 million versus a net loss of $89 million in the same quarter last year

- Adjusted EBITDA was $40.8 million versus $49.4 million in the same quarter last year

Stock Performance

Wheels Up Experience went public on July 14, 2021. On July 16, it closed at $10.25. It declined to $7.01 on October 29, 2021, yet saw a brief rise to $7.80 on November 5. Since that time, UP has declined steadily and now trades in the $2.25 to $2.50 range.

The decline could be incorporating some of the pessimism that has swirled around stocks that were taken public by SPACs. Many stocks in that category deserve skepticism about whether or not they are even viable businesses. But Wheels Up should be considered as separate from that crowd.

Valuation Summary

Even if one doesn’t buy into the description that bills Wheels Up as an Uber or Airbnb sort of business, and even if one is skeptical about the TAM expansion aspects of their story, at these levels the stock could still be appealing. Especially given that the company is led by an executive who previously built and sold a successful private aviation business.

The stock could top out at approximately $4B in revenue ten years from now (giving the company credit for achieving only a fraction of their expanded TAM estimates) while settling for operating margins that rise gradually and level off near those of non-private airlines, and that could still imply a valuation of about $4.75/share.

One could even apply a hefty probability of failure and still end up with a price target higher than current levels, and that likely would not be appropriate given their lack of debt.

Going Forward

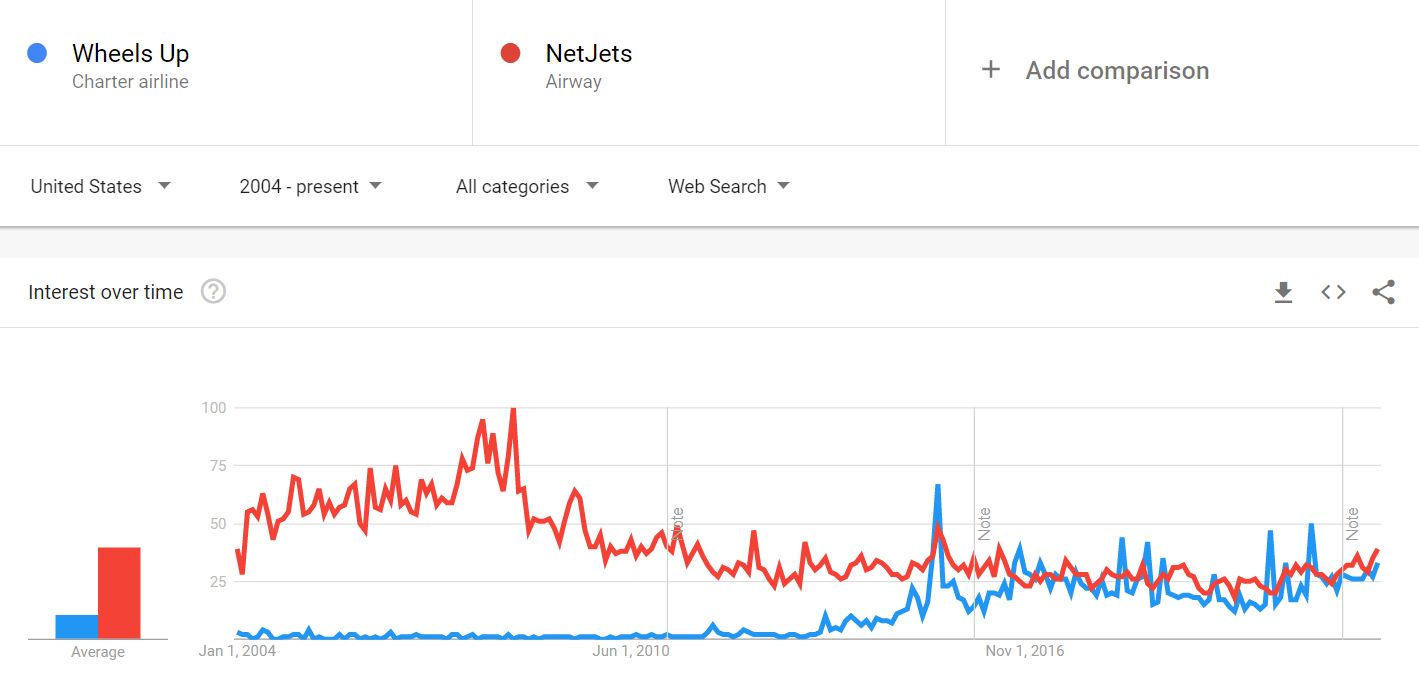

The company has a strong brand name (the below chart from Google Trends has them on par with NetJets, a major player in private aviation), and once people fly private, in my opinion, it is difficult to reverse the habit, which are two tailwinds that should help them pass along cost increases eventually.

Google

Although one shouldn’t expect the company to turn profitable overnight, at some point in upcoming quarters, it would be a positive sign to see evidence that steps have paid off to better offset surging expenses like fuel and labor.

Earnings will be reported on August 11th, after the closing bell.

Be the first to comment