Vertigo3d

In April 2022, four rural banks in the Chinese province of Henan announced the freezing of what turned out to be roughly 40 billion renminbi (or about $6 billion) of retail deposits. Within three months, a group of homebuyers around China threatened to stop making mortgage payments on apartments connected to building projects that were still under construction.

The two events are technically not related, but they are connected in many people’s minds. In part, this is because the mortgage boycott began so soon after the rural banking crisis, because the mortgage crisis may have even been set off in part by concerns about the frozen deposits, and because both events were disproportionately centered on Henan. This large, agriculturally important, and landlocked province in central China’s Yellow River Valley has a population of just under 100 million and a GDP of nearly $1 trillion.

There has been a great deal of misinformation and confusion about these events, and many of the details are likely to change over the next few days and weeks. While local officials have been at pains to portray both events primarily as problems driven by local circumstances (see, for example, this Global Times article on the topic), both events actually are symptoms of a deeper weakness in the Chinese financial system and can help illustrate the systemic pressures the country’s financial system has struggled to adjust to amid many years of soaring debt, nonproductive investment, and rising property prices.

This insight has two important implications. First, as Chinese regulators are increasingly recognizing, over a decade or more the Chinese financial system has evolved toward quite risky, self-reinforcing borrowing structures. These vulnerabilities will be blamed on causes specific to each case (such as lax regulation, fraud, and greed), but in fact, as economists like Hyman Minsky, Irving Fisher, and Charles Kindleberger have long understood, they are the natural and almost automatic outcome of many years of monetary expansion, rapid growth, and rising asset prices.

Second, many analysts have proposed various ways of resolving the problems facing China’s rural banks and the owners of unfinished apartment buildings or the Chinese real estate market, more generally. Yet most of these supposed resolutions do not resolve anything. These proposals consist mainly of ways of postponing a painful or chaotic resolution by restructuring and extending implicit and explicit liabilities. Most of these extensions involve directly or indirectly placing repayment obligations on local governments or larger, solvent banks.

This is just a version of treating a solvency problem as if it were a liquidity problem. In China, however, many years of rapid debt expansion have been backed by nonproductive investment in infrastructure and property and by a systematic overvaluation of real estate property. The rise in debt, in other words, has not been matched by a rise in the economy’s overall debt-servicing capacity. That being the case, the only way to service the debt is through implicit or explicit transfers to the lenders from one or another sector of the economy or another.

As I explained in a February 2022 blog post, these transfers can come in the form of taxes, defaults, financial repression, inflation, wage suppression, or currency appreciation, but what differentiates them is mainly the way the costs are allocated. Ultimately, some sector of the economy must absorb the costs, whether that party is the household sector, businesses, local governments, Beijing, the agricultural sector, the tradable goods sector, or someone else. Which sector is ultimately forced to absorb the costs is almost always a political decision, but it has enormous economic implications.

The Henan Bank Runs

The Henan banking crisis emerged in April 2022 when four rural banks – Yuzhou Xinminsheng Village Bank, Zhecheng Huanghuai Community Bank, Shangcai Huimin County Bank, and New Oriental Country Bank of Kaifeng – announced the freezing of roughly 40 billion renminbi ($6 billion) in what were initially described as retail deposits.

These banks are among the approximately 1,650 rural banks in China, and they collectively account for roughly 12 percent of the country’s banking assets. These banks focus mainly on local economic activity (primarily agriculture) in the areas they serve.

Because of the geographical and sectoral concentration of their banking activity (and their well-known vulnerability to pressure from local governments), the rural banks are generally assumed to be among the riskier parts of the Chinese banking system.

Despite this geographical concentration, or perhaps because of it, rural banks in recent years had relied increasingly on various online deposit schemes to diversify their funding away from their rural bases. As a Caixin article explains:

Small regional banks, especially rural lenders, often find it difficult to increase deposits from local customers partly because the population in general is less affluent and partly because the rise of the internet has made it easier for them to shop around for savings. Over the past few years, small banks have tried to attract money from savers all over the country through tie-ups with online financial services platforms and through agents, who offer financial incentives to customers to open savings accounts, even though the practice is illegal.

Because of rising concerns that these online deposit schemes were hard to regulate and easy to abuse, many of them were made illegal in early 2021. Nonetheless, it seems that their use persisted well into 2022. In a typical version of such a scheme, an online platform (like Du Xiaoman Financial) might offer products tied to a specific bank with interest rates around 4 percent, often for one-year maturities that could be rolled over for up to five years.

By offering high interest rates and in some cases a very valuable optionality, the four rural banks were able to draw funding from around the province and even neighboring provinces. This is why, when the banks announced the freezing of deposits, it immediately mattered to more than just local rural communities.

The initial stated reason for the deposit freeze in April, according to the relevant banks, was an upgrading of their online systems. But as the freeze dragged on for many days, and as depositors who visited their local branches also found they were unable to withdraw cash, depositors around Henan and those in neighboring provinces became increasingly concerned, especially when it was discovered in late April that a major shareholder of the four banks had been arrested under murky circumstances for “serious financial crimes.” In the past few years, many Chinese observers have become familiar with the spectacle of takedowns of a major figure just prior to a financial breakdown involving the institution with which that figure was associated.

The rising concern precipitated a series of bank runs and small, mostly local demonstrations, until May 21, when a large demonstration was held outside the office of the China Banking and Insurance Regulatory Commission (CBIRC) in Zhengzhou, the provincial capital of Henan. The police soon halted the rally, but it helped ensure national exposure for the plight of the depositors.

This widespread exposure became a national embarrassment when, as depositors continued agitating, many of them discovered in June that the pandemic-era public health codes on their mobile phones had turned red when they scanned city-specific QR codes at railway and bus stations, hotels, shopping malls, and other venues that required such codes.

The red health codes are supposed to mean that they had not passed the required COVID-19 tests, even though most, if not all, were certain that they had. A red code effectively prevents its holder from entering most public spaces and, most importantly, made it impossible for the affected depositors to travel by public transportation if they were planning to go to Zhengzhou to protest the deposit freezes.

The possibility that municipal authorities were manipulating the COVID-19 public health codes for reasons that had nothing to do with the pandemic created outrage throughout China, forcing Beijing to intervene. Local authorities then explained that the mislabeling of the health codes was in fact an accident caused by a computer glitch, but few were satisfied with this explanation, and five Zhengzhou officials were later punished, including a deputy director in the Political and Legal Committee of the Zhengzhou Municipal Party Committee.

The gaffes continued when a much larger protest on July 10 in front of the People’s Bank of China office in Zhengzhou turned violent. As protesters demonstrated (peacefully, by all accounts) in front of the bank’s office, a large group of white-shirted thugs attacked the protestors, physically assaulting them and causing many to be hospitalized. There were police officers at the protest, but they watched the assault and did nothing to intervene. By Monday, videos showing the violence had gone viral, and the behavior of local officials was widely criticized on social media.

The Authorities Respond To The Rural Bank Crisis

The next day, the police in Henan announced a breakthrough in the criminal proceedings related to the four banks. By then, they had discovered that the problems extended also to Guzhen New River Huai Village and Township Bank in the neighboring province of Anhui.

A Caixin article describes the breakthrough in the criminal proceedings, a development that involved a holding company that controlled all of the relevant banks:

According to a Sunday statement from the Xuchang city police department, an unspecified number of members of a “criminal gang” led by Lü Yi are suspected of “various serious crimes” related to illegal loan issuance and transfer of funds. The gang is thought to have gained control of several village banks by illicit means, sold financial products through their own platform, and set up shell companies to conceal data, the statement said.

Two days later, amid further protests on July 12, financial regulators in Henan and Anhui, including the local bureau of the CBIRC, ordered partial payments to depositors. Individuals with deposits of up to 50,000 renminbi were repaid starting on Friday, July 15. A week later, after they had presumably completed the first batch of payments, regulators announced the repayment of a second batch of depositors, this time with up to 100,000 renminbi in deposits.

On July 29, they announced a third batch of repayments for depositors who had up to 150,000 renminbi of frozen deposits in the affected banks, following it with an announcement on August 5 that individuals with accounts of up to 250,000 renminbi were to be repaid.

Were The Deposits Insured?

This is where things get a little complicated. Nearly eight years ago, in late October 2014, the State Council adopted a Deposit Insurance Regulation for Chinese banks that was intended to come into force on May 1, 2015. The first two articles of the resolution describe the purpose of the regulation:

Article 1: This Regulation is developed to establish and regulate the deposit insurance system, protect the lawful rights and interests of depositors according to the law, timely prevent and eliminate financial risks, and maintain financial stability.

Article 2: Commercial banks, rural cooperative banks, rural credit cooperatives, and other deposit-taking banking financial institutions formed within the territory of the People’s Republic of China shall buy deposit insurance under this Regulation.

Article 5 states that “Deposit insurance has a coverage limit, and the maximum amount of coverage is 500,000 yuan.” This seems pretty clear. Depositors in the rural banks should be protected for deposits up to that amount.

The Deposit Insurance Fund Management Company wasn’t set up immediately thereafter, but on May 24, 2019, the People’s Bank of China established the company with 100 billion renminbi in assets on the very same day that it intervened in the now-notorious Baoshang Bank collapse. By the end of last year, the deposit insurance fund had a balance of 96 billion renminbi after repaying 23.2 billion renminbi in finance stability loans.

Many analysts at first assumed that the four Henan banks’ depositors would have been covered for up to 500,000 renminbi. Some depositors claimed to have deposited far more than that, but it was widely believed that their fates would be determined politically, mainly on the basis of how much noise they were able to make and how destabilizing it might be for the financial system if wealthy investors with deposits that exceeded the 500,000-renminbi limit were suddenly to become alarmed about the possibility of losses.

This is a bigger problem than one might at first assume. One much-discussed issue in the Chinese banking system in the past decade has been the ability of wealthy lenders involved in risky projects to get the government or, more likely, a larger bank to backstop their risks.

One result of this implicit backing is that Chinese banks, and the country’s financial system more generally, is heavily underpinned by an assumption of almost infinite moral hazard. Any serious breach of the assumption could, consequently, cause a chaotic restructuring of liabilities as investors in risky banks, wealth management products, and loans hastily withdrew their financing.

Who Will Cover The Losses?

It quickly became apparent, however, that the Deposit Insurance Fund Management Company had no intention of covering the depositors’ losses. That’s because the money deposited through the online platforms turned out not to be bank deposits because they had apparently been whisked off and poured into other assets (or pockets).

It is unclear, at least to me, whether the investors originally believed that they were investing in ordinary bank deposits, or whether they in fact knew they weren’t and were relying on an assumption of moral hazard to allay their concerns. It is worth noting that these supposed deposits were earning much higher interest rates than normal bank deposits.

If they are not bank deposits, then clearly neither the Deposit Insurance Fund Management Company, the CBIRC, the People’s Bank of China, or the Henan authorities have any legal obligation to pay off the depositors. It would seem to me that the depositors, if that is the case, have only two recourses, one explicit and one implicit. The explicit recourse is to argue that their losses were caused by the poor regulation of the online platforms and the failure of the authorities to prevent an obvious fraud.

Such a case was undoubtedly helped by reports that bank officials had been arrested for participating in the mislabeling of the deposits. It was presumably strengthened on July 24 when, perhaps in response to mounting criticism of the CBIRC, Li Huanting, a senior inspector at the Henan branch of the CBIRC, was placed under investigation.

The CBIRC did not explain the reason for the disciplinary probe and made no reference at all to problems at the four rural banks, but most analysts assume the two are connected. This was followed four days later (on July 29) with an announcement that three more officials in Henan were being put under investigation.

The other (implicit) recourse available to the depositors is to agitate vocally and hold public demonstrations so as to embarrass the authorities and stoke uncertainty among depositors throughout the country. If such a disturbance were to create enough concern to cause a disruptive restructuring of liabilities among worried depositors and retail investors, it could force local authorities to provide at least a partial reckoning of the losses so as to calm things down and save face.

But this raises a further problem. Local governments throughout China, including that of Henan, have been whipsawed by a simultaneous collapse in revenues and surge in expenses, including pandemic-related expenses, even as they are tasked with funding enough economic activity to help China achieve its GDP growth targets. Most of them are too strapped for funding to take on additional expenses.

The provinces have nonetheless been under pressure to clean up and recapitalize the banks. According to a Reuters report, for example, in the first half of 2022, the provinces of Liaoning, Gansu, and Henan and the city of Dalian already were granted “a combined quota of 103 billion renminbi in special local government bond issuances.”

This is about an estimated 1 percent of their collective annual GDP (author’s calculation). According to the same Reuters report, “In the near future, other local special bond issuance plans will be approved, and it is expected that the overall amount of 320 billion yuan will be distributed by the end of August.”

From the very beginning, it seemed clear that the problems with the Henan rural banks were likely to have implications that extended well beyond the directly affected banks. In that light, a comment by an anonymous banker quoted in a recent South China Morning Post article is suggestive:

Other local governments, such as in the northeastern province of Liaoning, have also stepped up supervision of the small-bank sector. The provincial government has issued three rounds of special-purpose bonds totalling 33.1 billion yuan since last year to recapitalise local banks. “If the risks cannot be contained, what happened in Henan will also likely happen in Liaoning,” said a Liaoning-based auditor on condition of anonymity.

And this is not just a problem for bank regulators in Liaoning. There is likely to be pressure in several other provinces, too. In fact, in every province in which the property bubble is starting to deflate, we will likely discover that expectations of ever-rising real-estate prices have been underpinning an enormous amount of very risky borrowing.

The Mortgage Boycott

As if the rural bank problems in Henan and Anhui weren’t enough, conditions were suddenly made much worse by a threatened mortgage boycott that seemed to spread very soon after the rural bank problems in Henan went viral. In China, it is pretty standard for property developers to sell apartments in developments long before the projects have been completed. According to Ting Lu of Nomura, Chinese developers have delivered “only around 60 percent of homes they [sold in advance] between 2013 and 2020.”

In early- to mid-July, perhaps taking inspiration from the activity surrounding the rural banks, an online crowdsourcing group (“WeNeedHomes”) began complaining about the failure of property developers to deliver apartments on schedule, even though many of the homebuyers had taken out mortgages to make the payment deposits on these yet-to-be-constructed apartments and were required to maintain their mortgage payments.

The group soon organized and began to threaten to stop making payments on the mortgages unless something was done to guarantee the completion of the apartments. By the end of July, more than 320 projects in a multitude of cities were affected by the mortgage boycott.

Caixin, in a very useful July 29 article, explains the peculiarities of the pre-sales process in China in some detail:

Although developers in many countries are allowed to sell homes before they finish building them, the practice in China is special in two ways. First, homebuyers have to pay in full when they decide to buy. Usually, they produce a downpayment for a mortgage and the bank covers the rest. But in other countries like the UK, buyers of presale homes only need to come up with a deposit to reserve a property. They don’t need to pay off a mortgage until their homes are delivered. This full-payment requirement has helped developers raise cash quickly, which they have burned to fund land purchases or expand their business, analysts said.

Second, until recently, Chinese developers had been allowed to use the bulk of their presale revenue for whatever they wanted. Although China has laws and regulations requiring developers to set aside enough money to finish construction on their housing projects, local governments and banks had allowed them to sidestep some of the rules, including the requirement that presale funds must be deposited into government-supervised escrow accounts. Instead, a vast amount of presale funds ended up in developers’ own accounts.

Pre-selling apartments had become a major source of financing for developers, and perhaps it was the combination of credit overextension and the cheap financing available from pre-selling that created incentives for property developers to increasingly exploit this as a source of financing. One way of doing so is for property developers to start projects, and announce pre-sales, more aggressively than they can complete them.

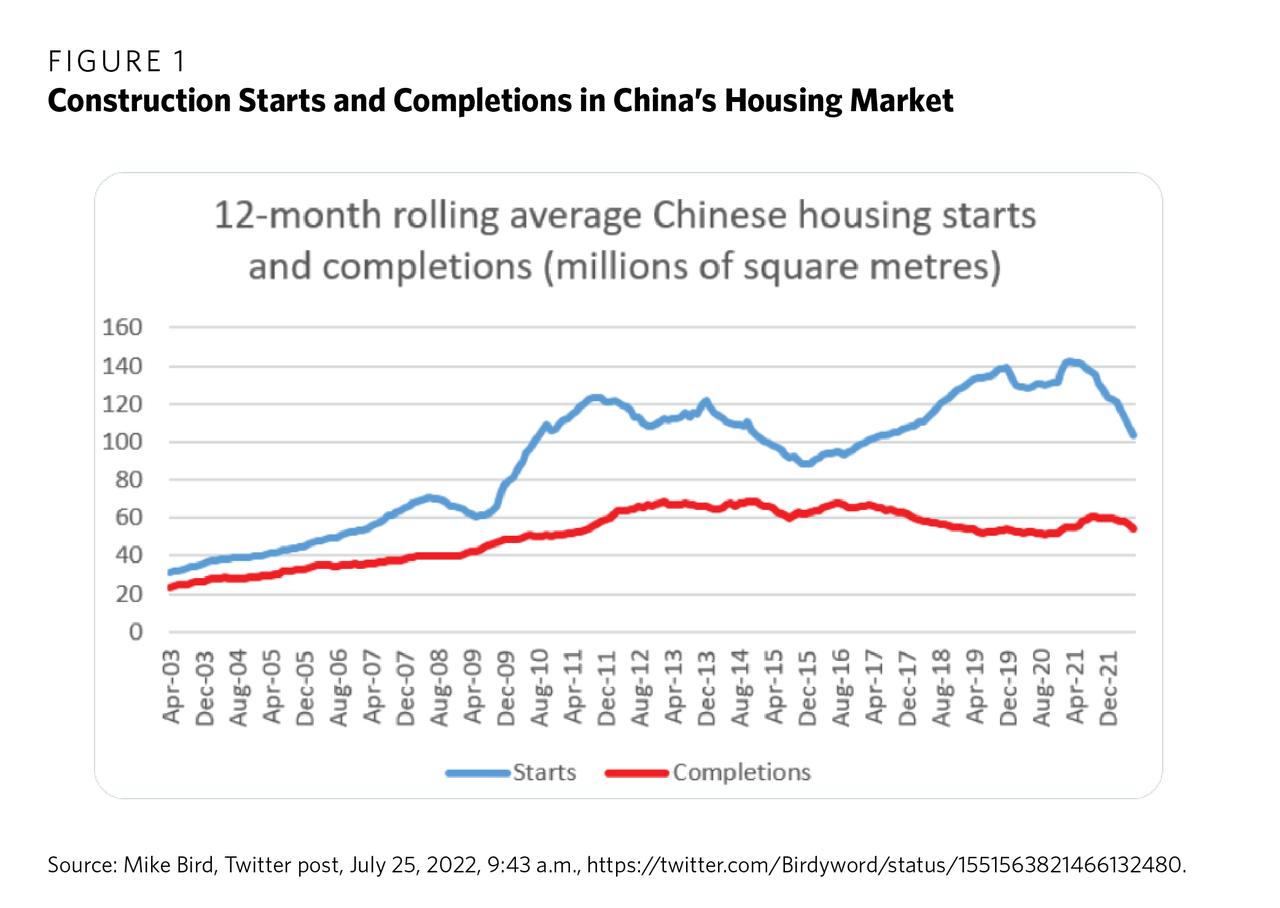

This happened extensively in China, and the result was a growing gap between property starts and property completions. The Economist’s Mike Bird, using data from the National Bureau of Statistics, prepared the following graph (figure 1), which he has allowed me to use.

This rather ugly set of numbers illustrates the extent of the problem. Whenever financing conditions got tighter for property developers in China, they were quick to start new projects so they could pre-sell apartments and raise financing, but they were much slower at completing them. Pre-sales, in other words, had increasingly become a scheme to obtain cheap financing and was used in an especially aggressive way when liquidity conditions tightened.

This is an illustration of one of the many forms of balance-sheet inversion, a concept I will discuss later in this post, that has emerged in China in recent years: such self-reinforcing behavior was systematically encouraged in a manner that led automatically to rising systemic risk within the financial sector

As a result of what was effectively a financing scheme, homebuyers found themselves waiting longer and longer for the apartments they had purchased to be completed. As long as property prices could only surge, this often didn’t matter. Pre-purchases became part of the speculative apparatus used by both investors and property developers, and they were often seen by homebuyers as a successful investment alternative to bank deposits. Borrowing from banks to pre-purchase apartments seemed like a way to, in effect, arbitrage the spread between mortgage costs and rising property prices.

The problem is that this process, one of many issues that has developed over the years, automatically results in behavior that can be intensely self-reinforcing both on the way up and on the way down. When the property market was booming, pre-sales became a low-cost financing mechanism that allowed property developers to ratchet up their activity rapidly and this, in turn, boosted the property market further.

The problem is that once conditions reversed, the financing mechanism was likely to dry up very quickly, and this would put enormous liquidity pressure on the property developers that could not help but drive the market down further.

Mortgage Boycotts Roil The Property Markets

But pre-purchasing apartments as an investment scheme only works, of course, when prices trend inexorably up. Once prices began to decline, such purchases became much less interesting, and the fact that homebuyers couldn’t even take ownership of the apartments for which they had partially pre-paid became a growing problem. This was made worse by the fact that, by most accounts, the majority of those who had initiated the mortgage boycotts were not wealthy speculators looking to back out of a bad deal.

Most of the “WeNeedHomes” group, it seems, were working-class or lower-middle-class residents of secondary and tertiary cities, and the apartments they had purchased were low-quality apartments on the edges of cities into which they had planned to move as soon as they could. In that context, it is not at all surprising that eventually angry homebuyers took action, including through the mortgage boycott.

This could not have come at a worse time. Since the beginning of the property crisis in September and October 2021, property prices have declined in more than two-thirds of China’s seventy largest cities (and probably all of the smaller ones), while, more importantly, sales of new apartments this year have collapsed. The mortgage boycott made things worse:

Analysts predict that the wave of mortgage boycotts will further disrupt the already fragile property market. During the two weeks through July 17, new home sales in thirty major cities dropped 41 percent and 12 percent in terms of floor space from the previous week, CRIC data showed. “Prospective homebuyers have grown reluctant to purchase new homes in cities with multiple boycotted projects,” CRIC analysts said in a note.

This has locked the property sector in a classic vicious cycle (see my earlier Carnegie blog post on the Evergrande meltdown). Property developers had historically depended on rising home prices and surging sales to justify massive leverage and overbuilding, but once the bubble began to deflate last year, these overleveraged property developers ran into serious liquidity and credit constraints that made it impossible for them to complete their construction projects.

This reduced homebuyers’ confidence even more, and not only did purchases drop sharply, but pre-construction purchases dropped even more quickly. This deadly combination only increased the liquidity pressure on the property developers, exacerbating the whole cycle. With pre-sales accounting for more than half of the financing developers had been able to obtain, the collapse in pre-sales hit especially hard. This is why so many of the projects have fallen so far behind schedule, and this is what has aroused the frustration of homebuyers who had pre-paid their purchases.

All of this was made worse by the threatened mortgage boycott. According to Bert Hofman, the director of the East Asian Institute at Singapore’s Lee Kuan Yew School of Public Policy,

Mortgages outstanding as of the end of June totalled [41 trillion renminbi ($6 trillion], around 40% of GDP. Total household debt is about 60% of GDP, or 114% of household disposable income. While this is moderate compared to many Organisation for Economic Co-operation and Development countries, it has risen steeply since the 2008 financial crisis.

The Authorities Respond To The Mortgage Boycott

The threatened boycott set off an initial wave of panic and confusion, as well as a certain amount of bluster (with some officials warning that a failure to meet mortgage payments could result in serious long-term consequences for the person defaulting). There were concerns that if homebuyers were successful in boycotting mortgage payments on unfinished homes, these boycotts might spread to other mortgages, especially in cases where property prices had been falling.

The authorities responded in two ways. First, they allowed homebuyers temporarily to halt mortgage payments on undelivered property projects without incurring penalties. Officials in Beijing seemed to suggest that homeowner eligibility and the length of the grace periods would be decided by local governments and banks.

Second, they took steps to expedite the completion of the apartment construction projects. In mid-July, a newspaper published by the CBIRC said that the commission was urging banks “to support mergers and acquisitions by developers to help stabilize the real estate market. Banks were also asked to improve communications with homebuyers and to protect their legal rights.”

In addition, local governments were asked to take direct steps to push the uncompleted projects forward, with the province of Henan taking the lead. According to a July 28 South China Morning Post article:

Henan’s local authorities assigned a bad-loans manager and a state-owned real estate developer to clean up the province’s property mess, taking drastic action to contain a crisis ahead of China’s twice-a-decade leadership conclave. A working team set up by Henan Asset Management Company and Zhengzhou Real Estate Group will help cash-starved developers to work out their funding woes, according to a report posted on the asset management firm’s website. The team will also aim to revive stalled projects, sell assets, and restructure businesses to ensure the completion and smooth delivery of homes to contracted buyers, the report added.

A related Caixin article added to the various proposals:

Authorities have promised to help developers resume construction on unfinished projects as soon as possible. China’s banking regulator has also urged banks to increase lending to make that happen. The government could eventually bail out unfinished projects, market insiders said, by directing local state-owned enterprises (SOEs) to partner with banks to acquire them and complete construction. Local government financing vehicles, which are SOEs intended to fund infrastructure and public-welfare projects, will also likely inject cash into some projects, they said.

In Zhengzhou, Henan province, the city with the most mortgage boycotts, two state-owned enterprises will jointly set up a fund for the local real estate industry. “One feasible way to deal with the problem is for local governments to buy unfinished projects and turn them into rental housing, with future rental income used to repay the government bailout fund,” said Hong Hao, former head of research at Bocom International Holdings Co. Ltd. Another possible approach is local authorities paying mortgages for homebuyers and leaving banks to write off the bad loans, he told Caixin.

China Construction Bank Corp., one of the largest state-owned banks, is exploring establishing a fund worth tens of billions of yuan with the local government in Hubei Province to transform unfinished projects into rental housing for public-sector employees, sources with knowledge of the issue told Caixin.

However, many local governments are struggling with their own tight budgets. In one northeastern province, local governments have been in talks with banks since late 2021 to fund SOE takeovers of unfinished projects, a source at a bank’s local branch told Caixin. Such cooperation requires localities to put up at least 30 percent of funding, but many local governments cannot afford it.

The mortgage boycott is still in its early stages, and I expect additional measures in the next days and weeks. It is clear that the potential associated risks to the financial system and the economy could be damaging, and with the all-important Party Congress just a few months away, Beijing will not want to see any disruption of the triumphant story the Chinese Communist Party plans to tell the country.

Next week, I will publish the second part of this blog post, discussing what I think are the most important implications of the recent events and the lessons learned.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment