Gabe Ginsberg

Hormel Foods Corporation (NYSE:HRL) develops, processes, and distributes various meat, nuts, and food products to retail, foodservice, deli, and commercial customers in the United States and internationally.

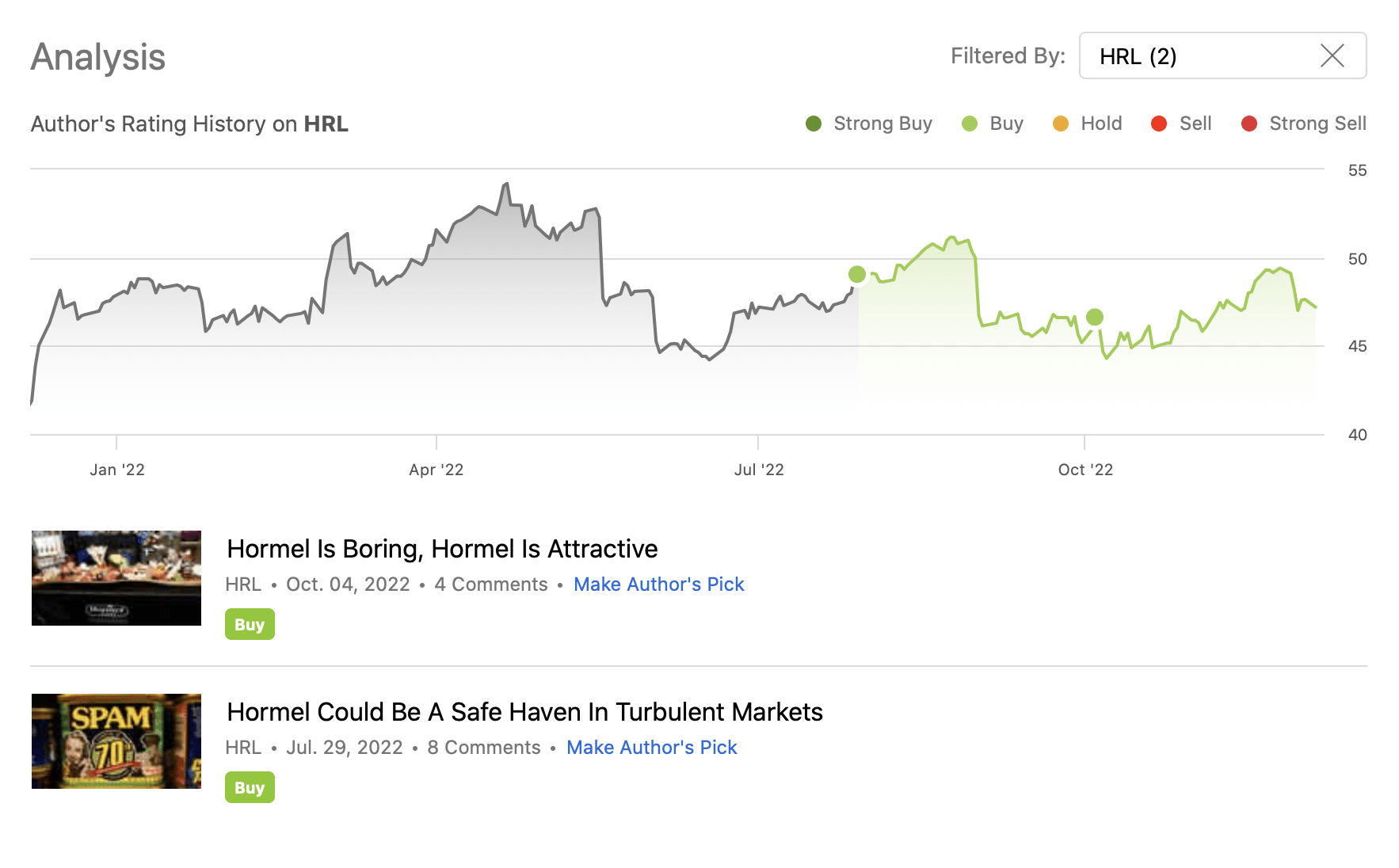

This year, we have already published two articles on Hormel, rating the firm’s stock as “buy” both times.

These articles were:

Analysis history (Author)

The primary reasons for rating the stock as “buy” were:

- The stock has performed well during times of low consumer confidence in the last 20 years.

- The demand for the products has remained high in 2022.

- Commitment of returning value to shareholders in the form of quarterly dividends.

Today, we are taking a look at the firm’s latest quarterly report and evaluate whether our previously established rating is still valid.

Hormel Q4 earnings

Hormel released their fiscal Q4 earnings results on the 30th of November 2022.

After the earnings release, Hormel’s stock price fell sharply due to the worse-than-expected outlook. However, since then, the stock price has largely recovered.

Overall Financial metrics

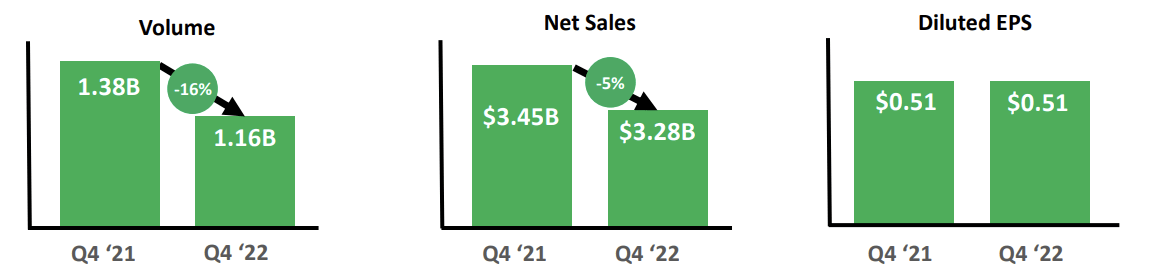

In the fourth quarter, volume declined by as much as 16%. While this is not a particularly positive piece of news, this decline was anticipated. It was primarily driven by the company’s earlier decision to rationalize lower-margin commodity pork volume and lower turkey supplies. On the other hand, organic volume increased for the “Grocery Products and International & Other” segments.

The main reasons for the decreasing sales were: reduced commodity sales and the impact from an additional week of sales last year. Organic sales have, on the other hand, increased, driven by the center-store grocery portfolio as well as by the strong performance of the foodservice businesses.

Diluted EPS is in line with last year’s figures, despite the additional week of sales in 2021. The Jennie-O Turkey Store has been a key contributor to the growth.

Selected metrics (HRL)

Important to pay attention to the margin expansion year-over-year, which has enabled the diluted EPS to stay flat year-over-year.

Margins (HRL)

In our opinion, the expansion of the margins in the current market environment is a positive sign that HRL’s strategic pricing actions are working and that they are able to leverage the Jennie-O Turkey Store business.

Let us now take a closer look at the different segments to understand how their performance has contributed to the overall Q4 results.

Results by segments

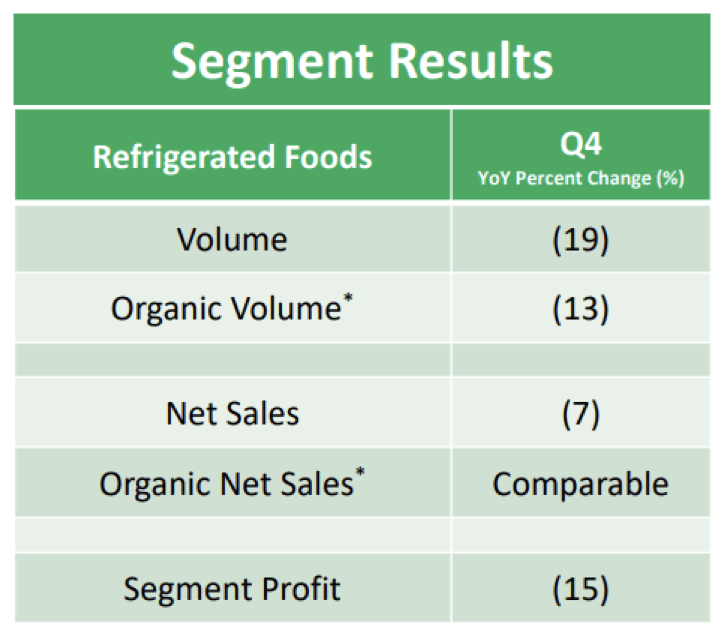

Refrigerated Foods

Volume declined substantially by as much as 19% in the refrigerated foods segment. The key reason for the decline was the lower commodity sales resulting from the company’s new pork supply agreement. At the same time, net sales and segment profit have also declined by 7% and 15%, respectively. The sales decline has been largely driven by the impact from an additional week in the fourth quarter of last year and lower commodity sales, while the profit has been negatively impacted by the lower commodity profitability and higher operational, logistics and raw material costs.

Refrigerated goods (HRL)

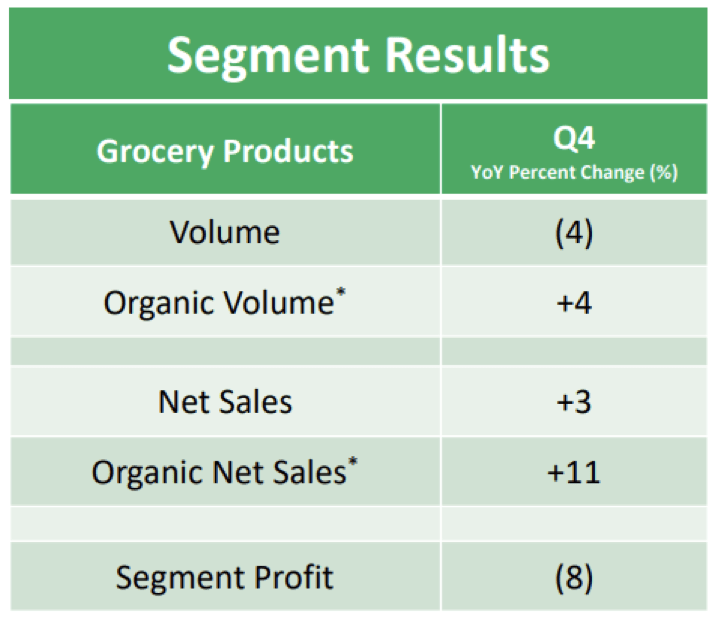

Grocery products

HRL achieved higher net sales in this segment than in the year-ago quarter. The increase has been led by the strong demand for SKIPPY® peanut butter and the impact of pricing actions across the Mexican and simple-meals portfolios. Unfortunately, the increase in sales did not translate into profit. The firm’s pricing actions have not been enough to offset the impact from the continued inflationary pressures.

Grocery products (HRL)

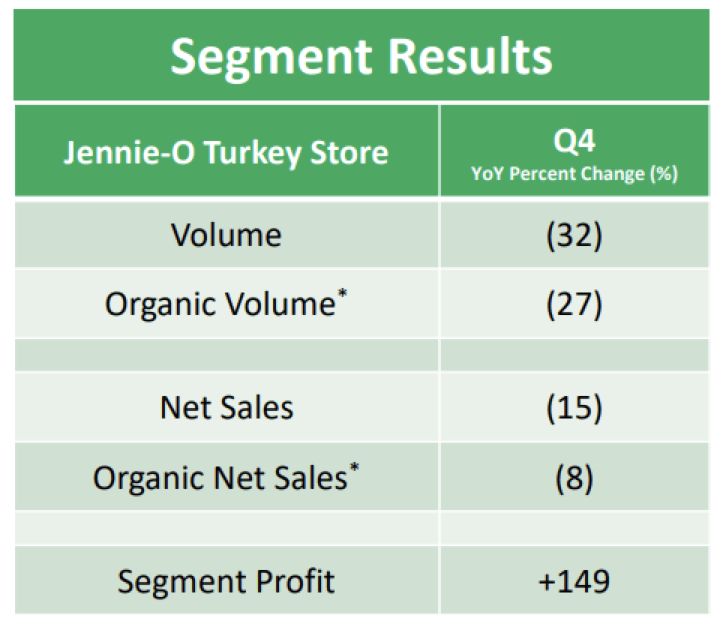

Jennie-O Turkey Store

Both volume and net sales fell substantially in this segment. The highly pathogenic avian influenza (HPAI) has been responsible for this decline. On the other hand, this segment delivered the highest profit growth year-over-year and contributed significantly to the margin expansions, higher commodity prices, and improved value-added mix.

Jennie-O Turkey Store (HRL)

International & Other

While volume remained flat year-over-year, the lower fresh pork and refrigerated export sales offset the positive impacts of the growth from the SPAM® and SKIPPY® brands, resulting in a net sales decline. As already mentioned above, the fresh pork sales decline has been a result of the company’s new pork supply agreement. Elevated logistics expenses also negatively impacted the results.

International & Other (HRL)

To sum up

We believe that the demand for HRL’s products remains strong. Although volumes have been decreasing across most segments, the decline has been primarily related to the supply chain related issues and the HPAI, and not to demand.

While Hormel is being negatively impacted by continued inflationary pressures, they have still managed to expand their margins year-over-year. Going forward, the macroeconomic landscape is likely to remain challenging in the first half of 2023. However, in the longer term, we expect HRL’s margins to further expand, leading to a positive impact on the EPS.

In our opinion, not only the improving macroeconomic environment can have a positive impact on the margins, but also the implementation of the firm’s new strategy. This includes:

- Adopting new organizational design and management structures

- Continuing to fully integrate Jennie-O Turkey Store into the company’s One Supply Chain and new operating segments

- Standing up the Brand Fuel Center of Excellence

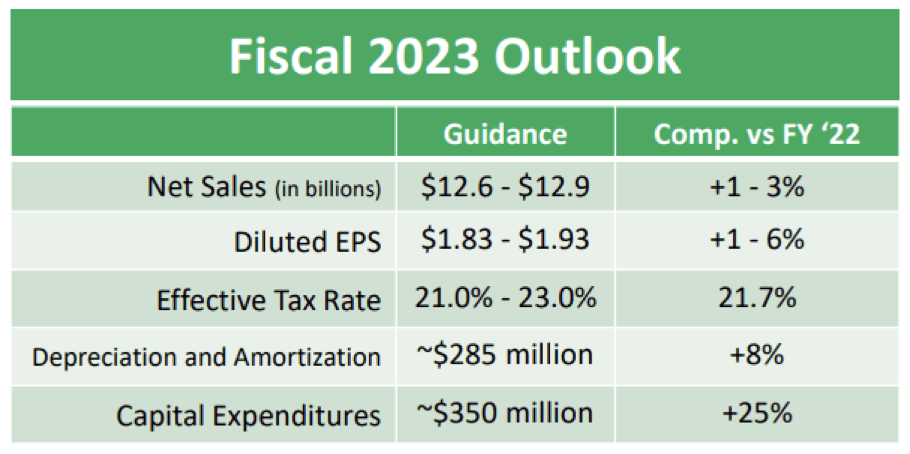

Outlook

Despite the expected macroeconomic headwinds, the firm anticipates top and bottom line growth for the coming fiscal year. The primary drivers of growth are expected to be the Foodservice and International segments, and improvements across the supply chain.

Outlook (HRL)

In our opinion, the targets set out by the firm are realistic and achievable, as HRL has managed historically to perform well, even in periods of poor consumer sentiment.

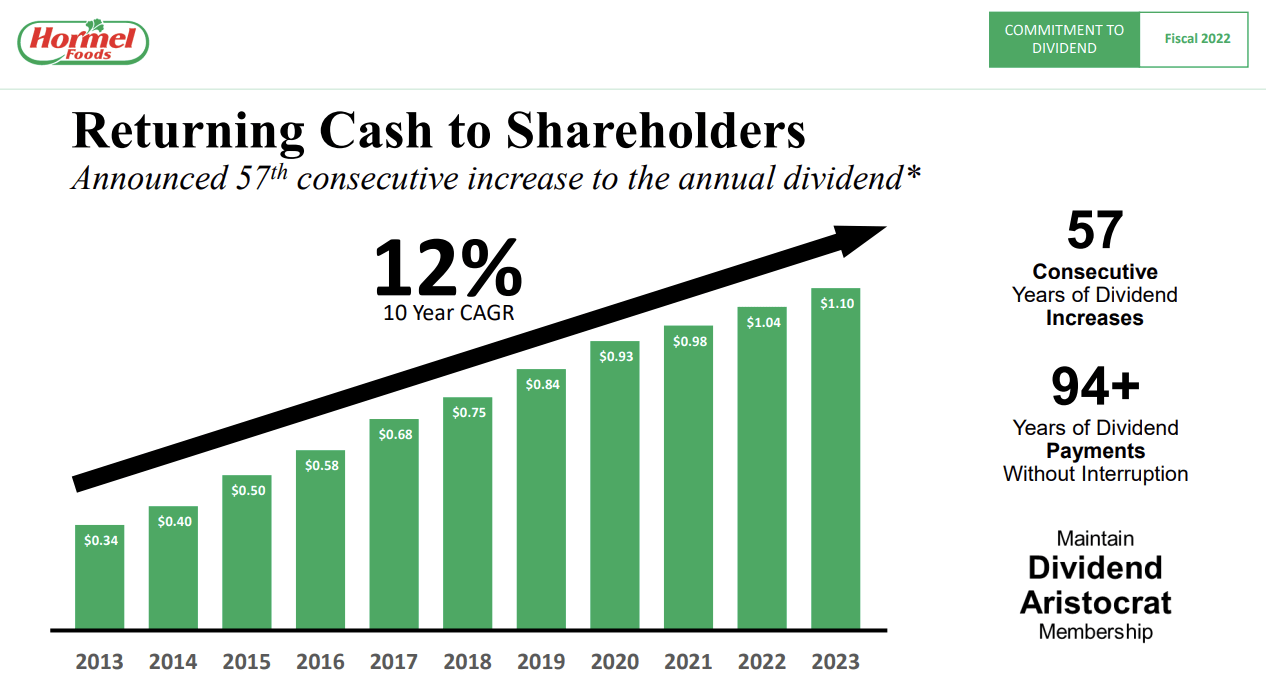

Dividends

One of the reasons why we have been in favor of HRL’s stock is the company’s commitment to return value to its shareholders.

Hormel recently announced its 57th consecutive increase to the annual dividend.

Dividends (HRL)

In our opinion, despite the short-term fluctuations of sales and net income, the Hormel dividend is safe and sustainable, as the dividend coverage ratio is about 1.7. As earnings are forecasted to grow further next year, we do not see an imminent threat of cutting or pausing the dividend. For this reason, we believe that Hormel Foods Corporation stock remains attractive for dividend and dividend growth investors.

Be the first to comment