AzmanJaka

The time has come again for me to take a look at what may be my favorite dividend growth stock I’ve never owned, Waste Management (NYSE:WM). Now, more than ever, as I delve deeper into the company’s trajectory, I can’t help but wonder whether I’m blinded by the valuation when all signs point to this being perhaps the best dividend growth stock in the market.

I don’t say that lightly. There are faster growers, sure. There are companies that have been paying their shareholders for longer. But there are not many that I’d throw the stock certificates into a coffee can and not look at the business for 3 decades. WM is one of those.

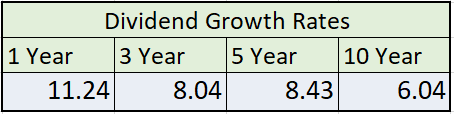

I have little doubt that 20 years from now, WM will be bigger than it is today, and it will more than likely have raised its dividend every year for 39 years. I’ll set a reminder on my phone to see how that prediction pans out.

Seeking Alpha

I wrote on the company for the first time at the beginning of 2020, mere weeks before Covid locked us all down and forced us to participate in more Zoom calls than anyone ever wanted. Covid was a blip for WM. The company faced minor challenges over the past 2 years with commodity pricing on its ancillary recycling commodity resale business, but there were no long-term concerns for the business. 75% of the company’s revenues are recurring, so it should probably start reporting its ARR and net revenue retention numbers, right? All WM needs now for a rerating is to advertise itself as a cloud TaaS (trash as a service) company powered by AI with its routes improved by machine learning. I’d be willing to bet the company’s churn numbers would be the envy of the tech sector. The gross margins may not get their foot in the door, though.

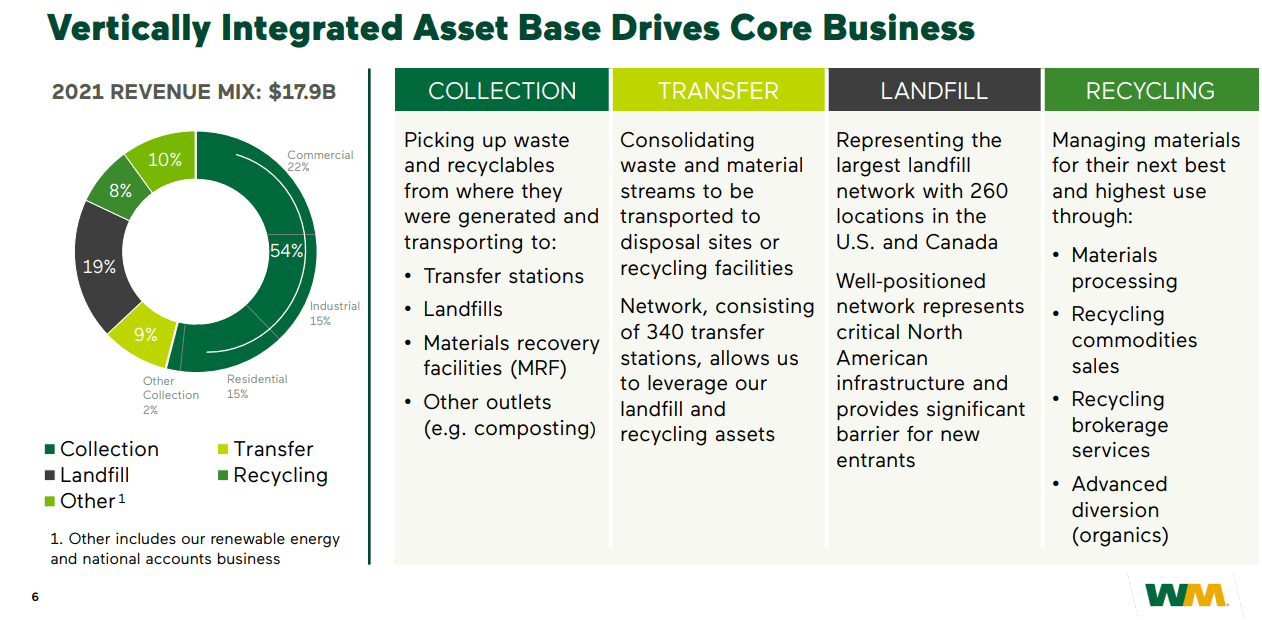

Company presentation

The secret sauce for WM is the nearly insurmountable moat it has in landfills. Even if a company beats the company out on price to collect the waste, odds are good they are paying tipping fees to WM to dispose of it at their landfill. Why don’t the company’s competitors build more landfills? They can’t. The country’s landfills have decreased from around 10000 in the 1980’s to 1500 today. Do you want a new landfill behind your neighborhood? Nobody else does, either, and the existing ones are able to fill the need so the regulatory barriers to entry protect WM’s position.

With that, the moves WM has made over the past 2 decades were amazingly simple in theory, but difficult to execute as well as the company has done. They buy other waste operators, roll their business in, drive cost synergies, hike up prices (sorry, customers), and then profit. They’ve done it over and over, and most recently rolled in one of their largest acquisitions ever with Advanced Disposal costing $4.6B in 2020. That acquisition came with a few dozen landfills as part of the bargain.

My last article covered Coca-Cola (NYSE:KO), and in it I discussed my concerns with the company’s debt load and the need for acquisitions over time to continue to maintain the company’s leadership position in the beverage landscape. The main difference here is WM gets stronger with every acquisition. Its economies of scale grow, efficiencies are found, and the company is effectively able to tack on profits to the bottom line.

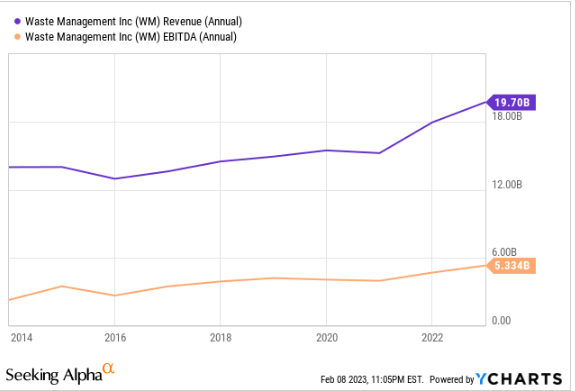

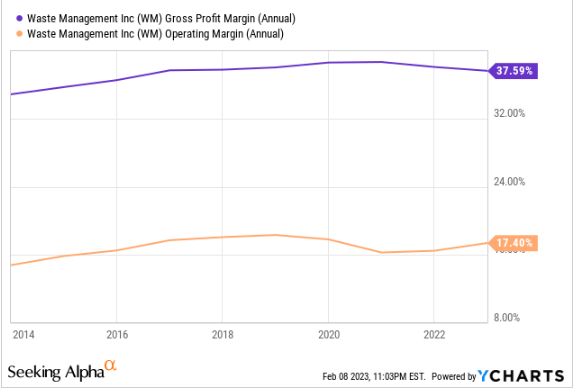

YCharts

For an old stodgy trash company, revenue growth has been great, and so has growth in earnings. In the most recent quarter, the company drove 9.5% growth in EBITDA on the back of organic revenue growth across all segments and a 40 bp improvement in margin while combatting a $59M drop in commodity revenue YOY.

Looking to 2023, management was confident to project 4.5-5% revenue growth, 40-80 bp’s of additional operating leverage, and 7% growth in earnings. Additionally, the board just hiked the dividend again by 7.7%. Looking to 2024 and 2025, it’s likely the company is driving earnings growth back into the low double digits based on its investments in the pipeline and the projected EBITDA effects.

Company Presentation

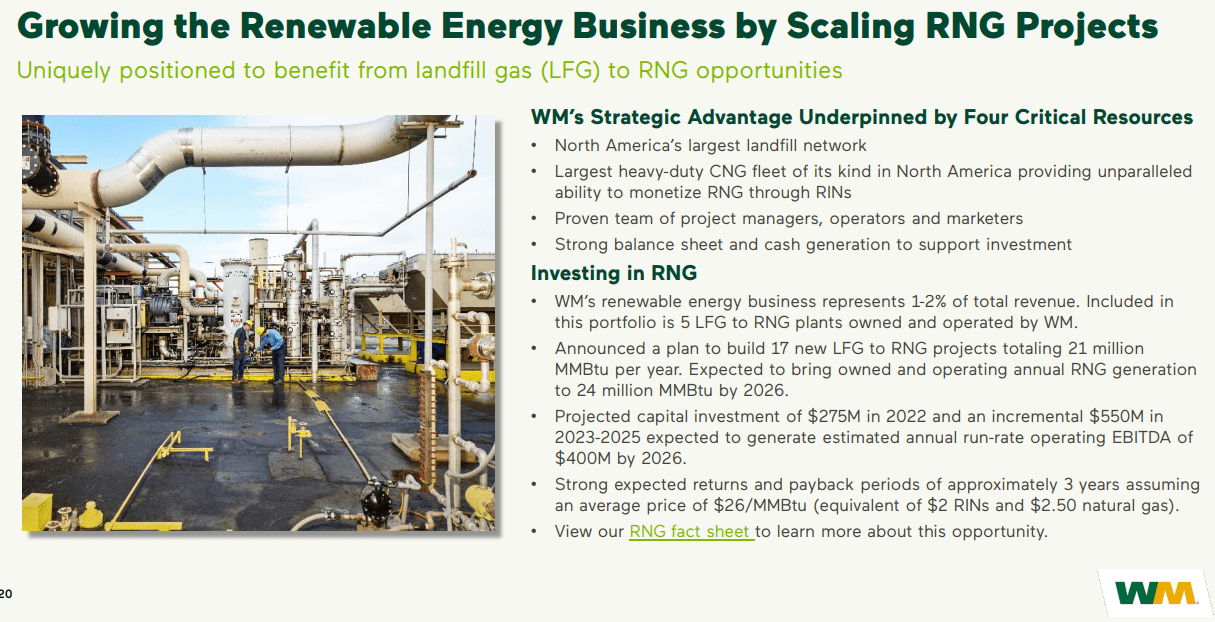

Eventually, the company will run out of smaller operators to gobble up and that will cause growth to slow. However, the company has no shortage of places to invest its cash. RNG produced naturally by the company’s landfills has been used to power 74% of the company’s truck fleet and is sold to the grid. Government regulation is moving in the direction of requiring some amount of RNG use by utilities, and with the company’s classification of RNG as a renewable energy source, future legislation benefitting all the renewables will likely favor WM. In this case, I don’t want to model for specific values, but the tides are moving in the right direction. These investments are projected to have a 3 year payback timetable.

YCharts

Margins have been relatively stable, and the company’s automation efforts have recently driven a 35% reduction in labor costs at the company’s MRF’s, and corporate cost-cutting saw an additional 600 positions eliminated in back-office efficiency gains. SG&A comes in at 9.6% of revenues, and the company most recently spent about $2.26B to maintain the business. It’s capital intensive, after all. 2023 projects for similar values, with $2-2.1B for business operations.

Company Presentation

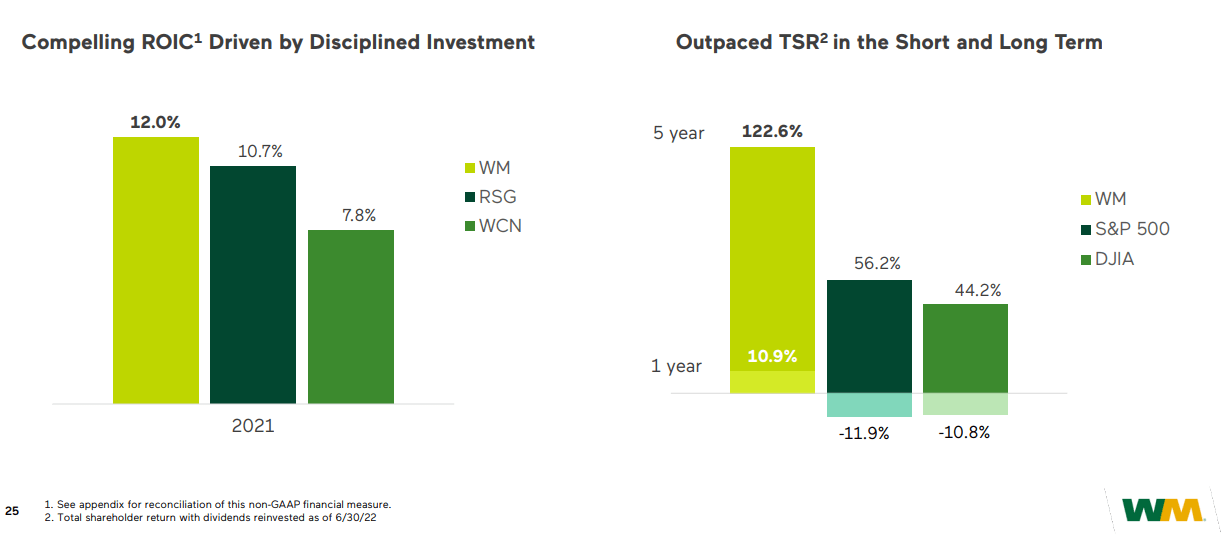

With all the company’s acquisitions, the 12% ROIC number isn’t eye popping. However, I included this slide from the investor presentation to show its best-in-class for the industry. So long as the company maintains their ROIC-WACC spread while they deploy capital, shareholders benefit.

Company Presentation

Here’s where I have some quibbles. WM is not a cheap stock. It hasn’t been a cheap stock for a very long time. However, management is throwing wads of cash at share repurchases which I am not a fan of. Although the recession resistant nature of the business has tended to keep the company’s share price relatively steady across the business cycle, I’d like to see smarter cash deployment. Most recently, the company spent $1.5B on repurchases and is planning another $1.5B this year.

Company presentation

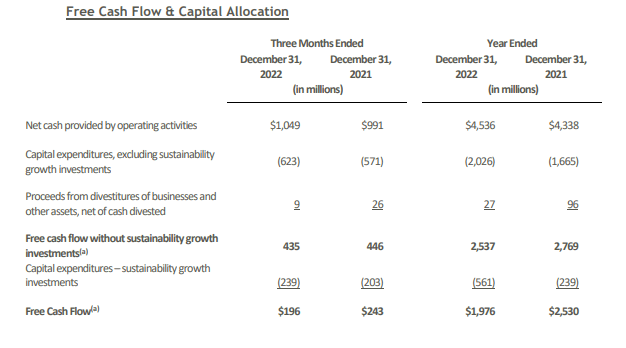

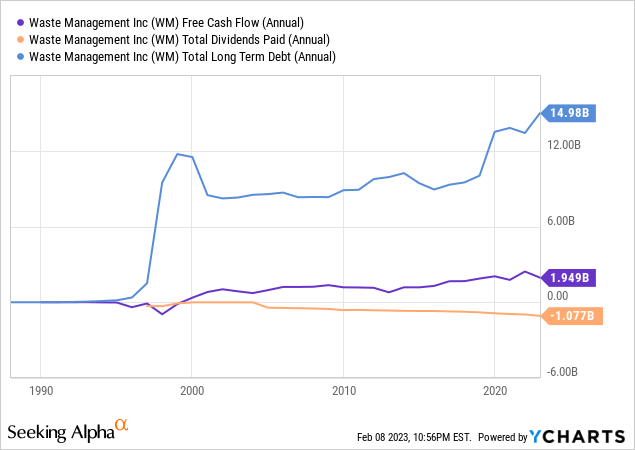

The dividend stands at $1.1B as a cash outlay against $1.5-1.6B in free cash flow, so it is well covered. The company’s growth initiatives account for pretty substantial capex, with another $1.1B going out for recycling and renewables projects this next year. The payout ratio stands at a comfortable 47%.

Dividend Radar

The total debt load here is not surprising based on the company’s cash outlays I discussed above. It’s not ideal, but based on the recurring nature of the business and its recession resistance, there is a slightly larger appetite for the company to hold some debt on the balance sheet. Long-term debt to equity stands at 1.97X, and management has discussed they are well within their comfort level against their target leverage. Free cash flow and earnings growth are adequate for me to believe the company can handle its debt and continue to grow the dividend.

FAST Graphs

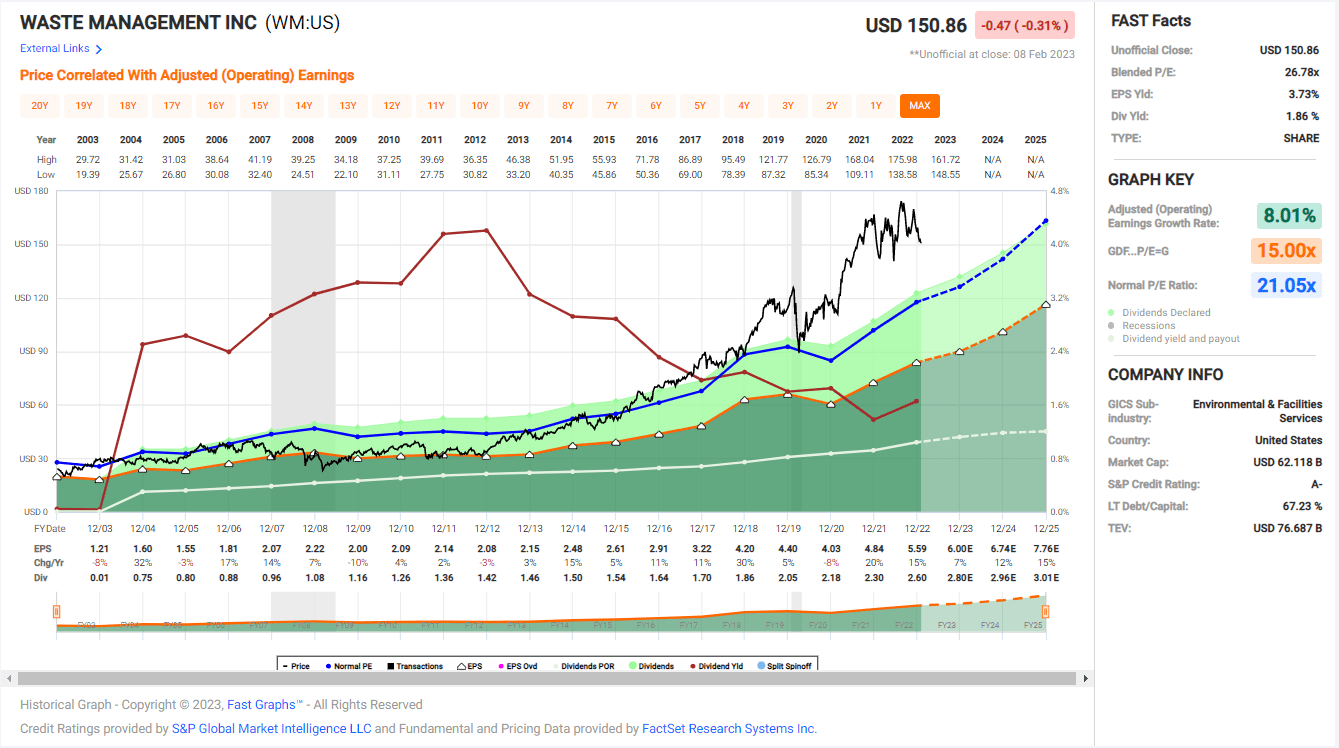

Now we come to the company’s valuation. I’m all for a company commanding a premium when it’s growing very strongly or is very consistent. In this case, the company’s consistency has driven the price up to what I would consider inflated levels. The Covid low only just brought the company down to its long-term average multiple. However, the long-term average multiple may not be the perfect guide here. The company’s efficiencies of scale have driven excess returns over time, and the string of positive earnings growth over the company’s recent history is likely to blame for the valuation expansion since 2014.

FAST Graphs

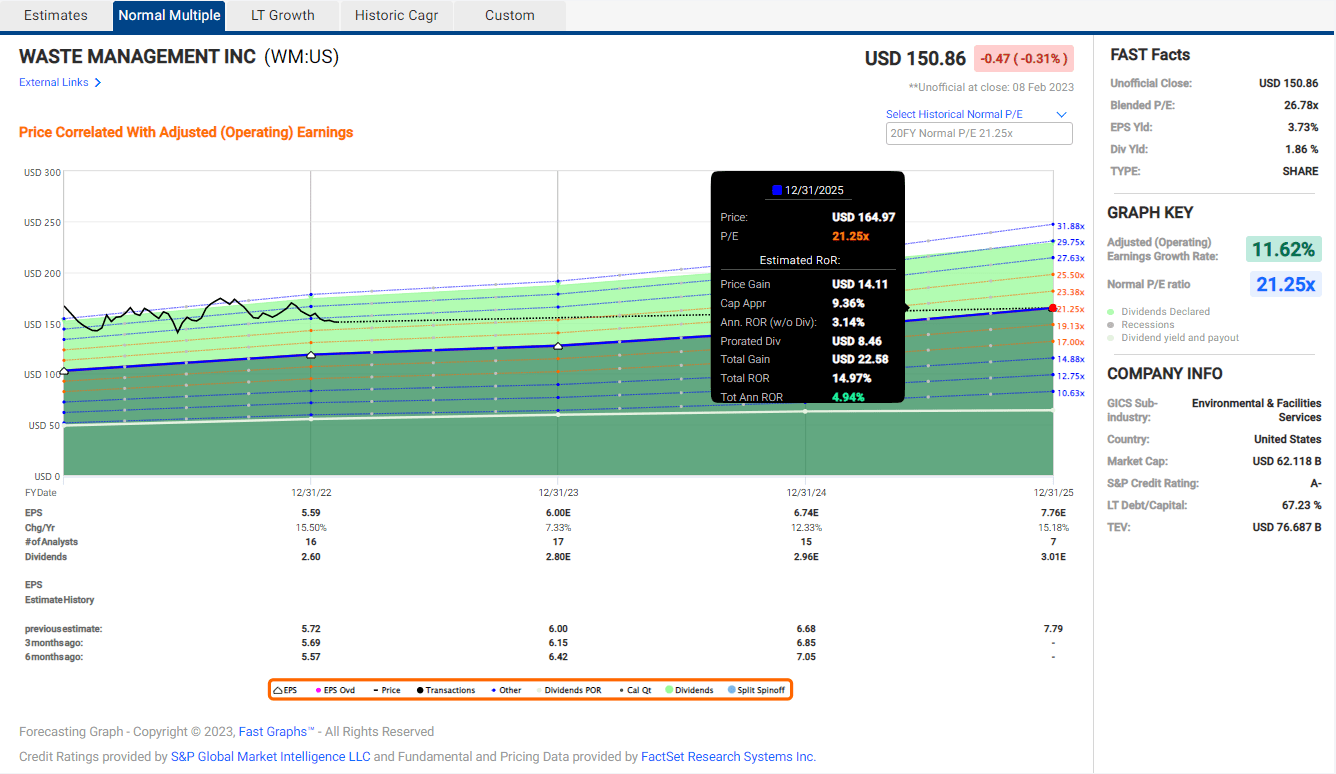

Based on analyst estimates for earnings growth, which include double digit increases in 2024 and 2025 based on current projects the company is investing in, an investment today would yield around 5% if the company returns to its long-term average multiple. If it doesn’t, you’re looking at closer to 14-15% annualized returns.

I’m torn on this company more than I am most of the time when I get to the end of my analysis. The company has definitely taken on some debt, but all signs point to strong earnings and cash flow growth from those acquisitions to counter it. If it weren’t for the share buybacks, I think I’d be looking past the valuation and buying here. However, I don’t understand the strategy there. Management has spoken to plenty of opportunities for deploying capital, with 2023 being what they’ve called a peak year for investment. If extra cash is laying around, I’d prefer they deploy it to pay down debt or raising the dividend further. I am maintaining my rating on WM as a hold, for now. I still consider it one of the best dividend growth stocks on the market.

Be the first to comment