US Dollar, Singapore Dollar, Thai Baht, Indonesian Rupiah, Philippine Peso, Indian Rupee, ASEAN, Fundamental Analysis – Talking Points

- US Dollar sinks against ASEAN currencies as jobs report miss bolsters sentiment

- Fed speak eyed, dovish talks could undermine an unexpectedly strong CPI print

- Philippine Central Bank, Indian and Chinese inflation data are also in focus

US Dollar ASEAN Weekly Recap

The haven-oriented US Dollar largely underperformed its ASEAN counterparts this past week. The Singapore Dollar, Indonesian Rupiah and Philippine Peso strengthened. Gains were also observed in the Indian Rupee amid a glut of Greenback in the banking system amid a tax dispute. Market sentiment notably improved, with the MSCI Emerging Markets Index rising by 1.32%.

Currencies from developing markets can be quite sensitive to risk appetite and capital flows. That is likely why a notable standout was the Thai Baht, which was little changed. According to Bloomberg, global investors sold a net $335.7 million of local equities on May 5th. That was the most since August 2019. On that day, the Bank of Thailand left benchmark lending rates unchanged and painted a soft outlook for growth ahead.

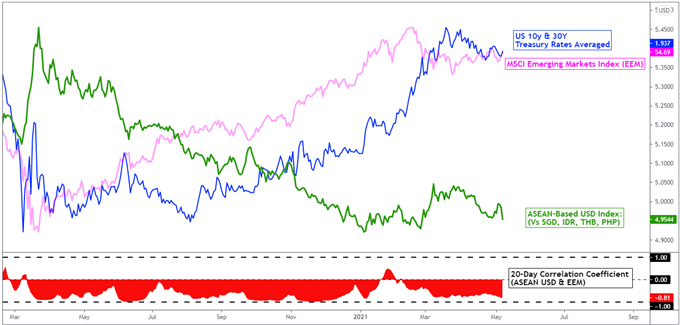

US Dollar, MSCI Emerging Markets Index– Last Week’s Performance

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

External Event Risk – Fed Speak, US CPI and Retail Sales Data

Last week’s disappointing US non-farm payrolls report missed expectations by a record margin. While the nation added almost 270k positions, economists were looking for a 1 million increase. This further pushed back 2022 Fed rate hike bets, offering global stock markets noticeable upside momentum right into the weekend. This also reflected poorly in the US Dollar, which swiftly depreciated.

With that in mind, there is going to be a plethora of Fed speak in the coming week. Speeches from branch presidents across the nation are due. Vice Chair Richard Clarida and Board of Governor member Lael Brainard will also present. Policymakers could use the soft jobs report to underscore the central bank’s still-dovish stance and downplay rising near-term inflation expectations as transitory.

This may continue cooling rate hike bets, which may bode well for Emerging Market sentiment. That would likely continue pressuring USD/SGD, USD/THB, USD/PHP, USD/IDR and USD/INR lower. US retail sales and CPI data are also on tap. Having said that, dovish commentary from the Fed could undermine the impact of a higher-than-anticipated inflation print.

ASEAN, South Asia Event Risk – Philippine Central Bank and GDP, Indian and Chinese CPI

Focus on the ASEAN economic docket, USD/PHP will be awaiting the Philippine Central Bank interest rate decision on Thursday. Bangko Sentral ng Pilipinas is expected to leave the overnight borrowing rate unchanged at 2.00% and likely maintain its dovish stance. This is despite recent CPI data continuing to clock in above the 2 – 4% target. The Philippine Central Bank may look past recent supply-driven gains in CPI.

First-quarter Philippine GDP is due on Tuesday. Growth is expected to rise 0.8% q/q versus 5.6% prior. The year-over-year outcome is expected at -3.2%, better than the previous -8.3% result. Still, these figures remain far off from where the nation was prior to the coronavirus, bolstering the case for a still-dovish central bank. Indian CPI and industrial production are due on Wednesday.

USD/INR could be open to a turn higher given recent dovish action from the RBI amid the surge in local coronavirus cases. A softer-than-expected inflation print could also keep the central bank open to further easing. Chinese CPI data will also be on tap this week. The nation is a key trading partner for ASEAN countries. Given episodes of liquidity drain from the PBOC, a higher inflation print code risk damaging Emerging Market sentiment.

Check out the DailyFX Economic Calendar for ASEAN and global data updates!

On May 7th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets index changed to -0.81 from -0.70 one week ago. Values closer to –1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-Based USD Index Versus EEM and Treasury Yields – Daily Chart

Chart Created Using TradingView

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

— Written by Daniel Dubrovsky, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter

Be the first to comment