SolStock

Upstart (NASDAQ:UPST) has been one of my worst holdings as a plunge in the stock price coincided with deteriorating fundamentals. With profits disappearing on account of negative revenue growth rates, this is an unfortunate situation in which it is very difficult to add to the stock in spite of the lower valuations. While the long-term outlook remains promising, management has a lot to prove to win back investor trust as the company appeared ill-prepared for the rise in interest rates. At this point, UPST represents a high risk / high reward investment proposition on lower interest rates.

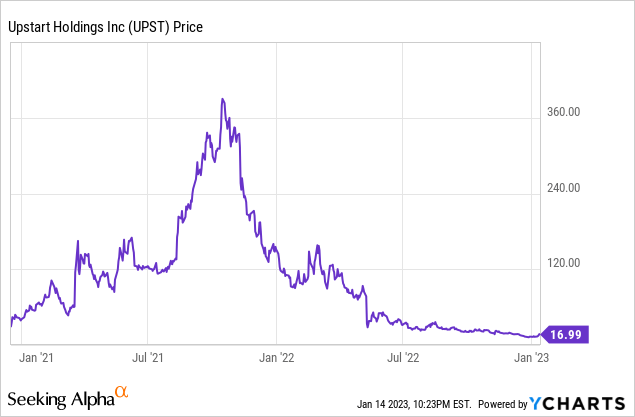

UPST Stock Price

UPST was a huge winner in 2021 as investors (including yours truly) were fooled by the rapid growth rates.

I last covered UPST in September where I explained why the risk profile soared alongside the plunging stock price due to poor management execution. The stock has since fallen 27%, but valuation is still not the problem here.

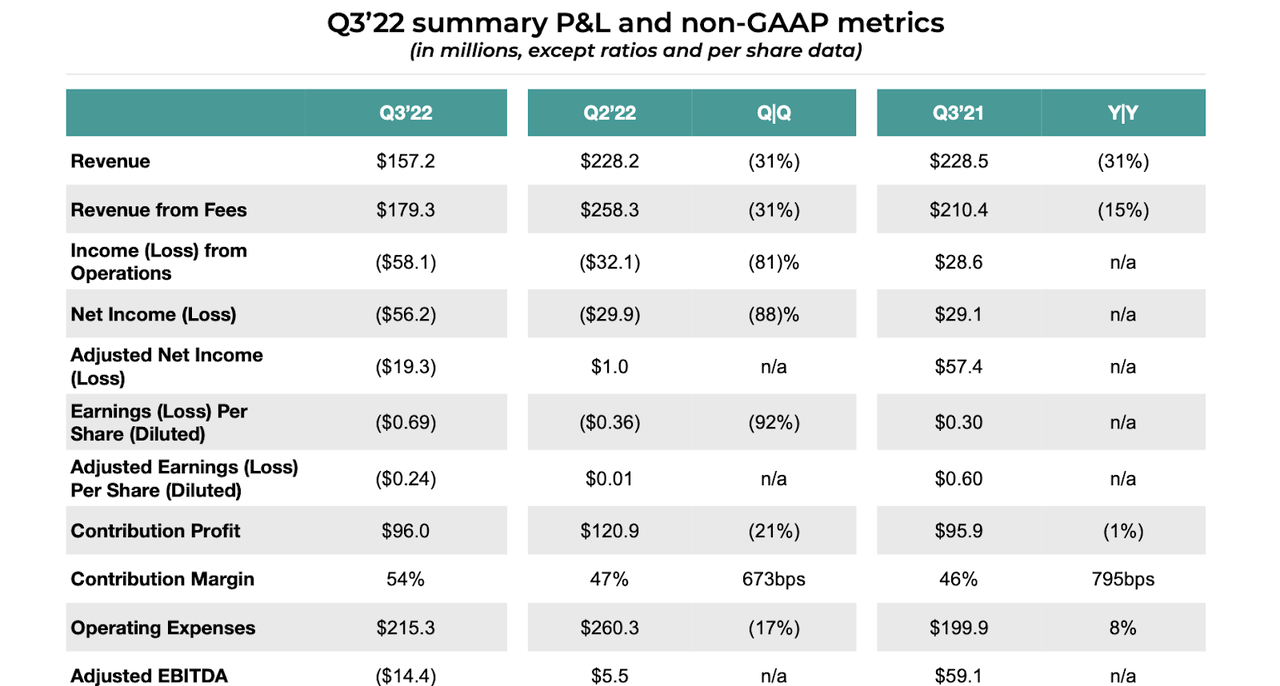

UPST Stock Key Metrics

The latest quarter saw revenues decline 31% YOY to $157.2 million and adjusted net income turn negative. One rare bright spot was the 795 bps rise in contribution margin to 54%, as the company has typically increased take-rates in response to lower loan demand.

2022 Q3 Presentation

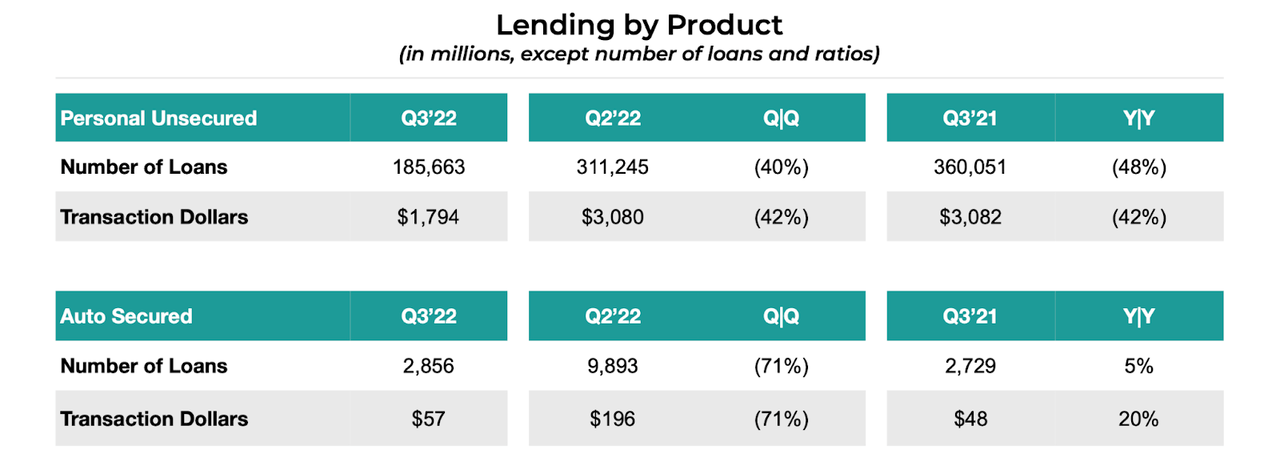

UPST saw the greatest weakness in its core personal unsecured lending platform, seeing 42% YOY declines. UPST did see auto lending grow by 20% but decline 71% sequentially, and this is a very new program so the deceleration in growth is quite disappointing.

2022 Q3 Presentation

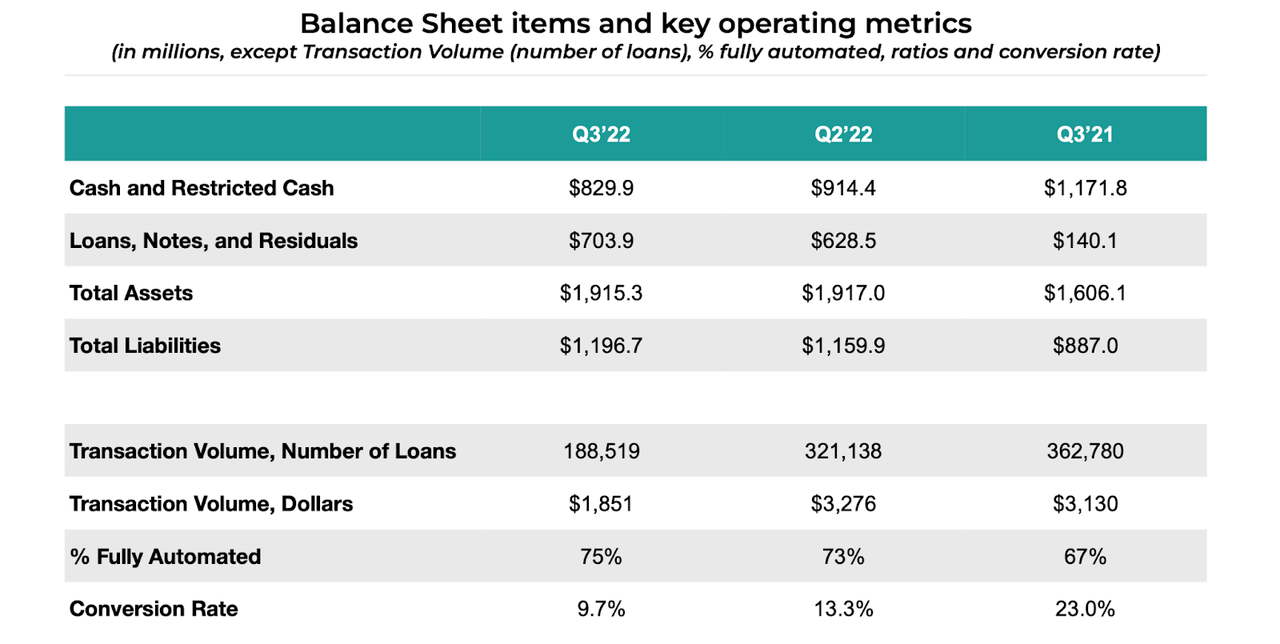

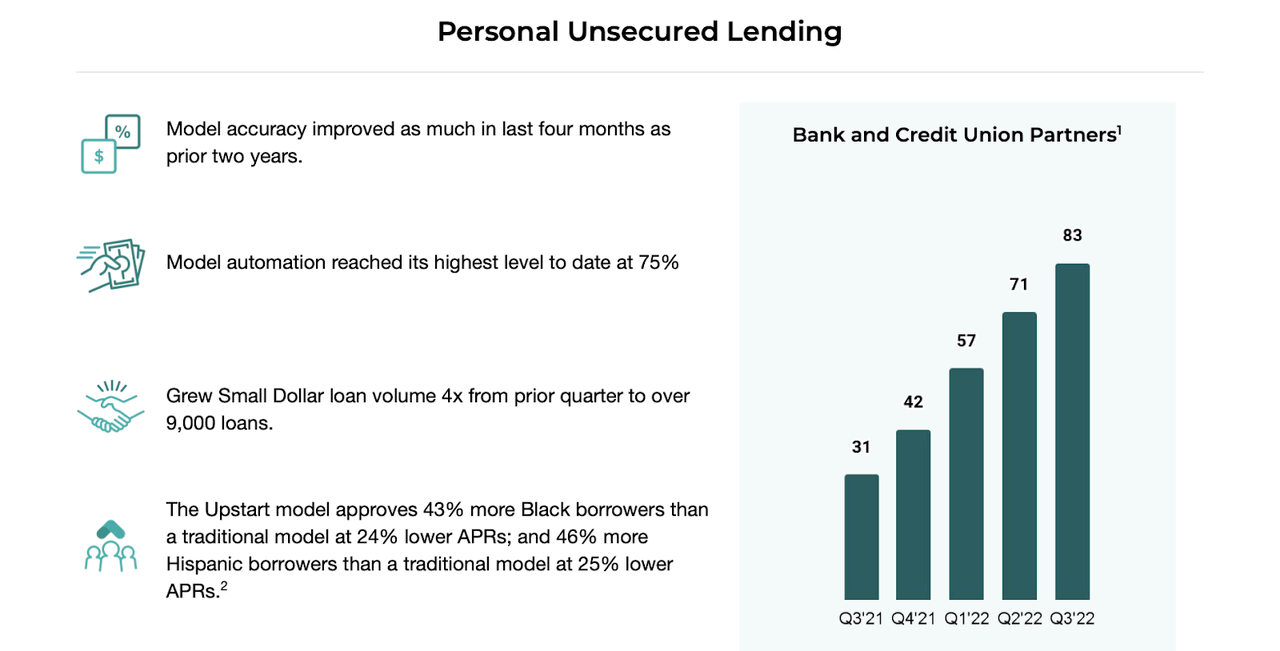

UPST ended the quarter with $829.9 million of cash representing over 50% of the market cap. UPST did see the percentage of fully automated loans jump to 75%, but the conversion rate of 9.7% reflected deteriorating demand for loan products. It does make sense – prospective borrowers found the higher offered interest rates less attractive than before.

2022 Q3 Presentation

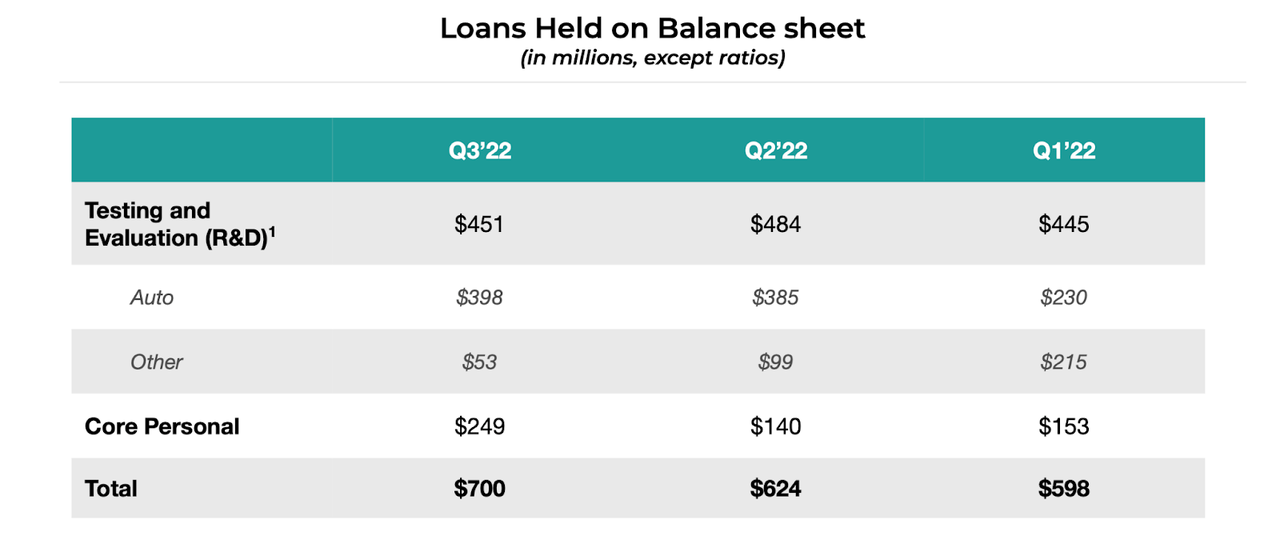

A common criticism of the company in prior quarters has been the use of its balance sheet to hold loans. Loans held on the balance sheet once again grew sequentially to $700 million, though the majority is considered to be held for “R&D” purposes.

2022 Q3 Presentation

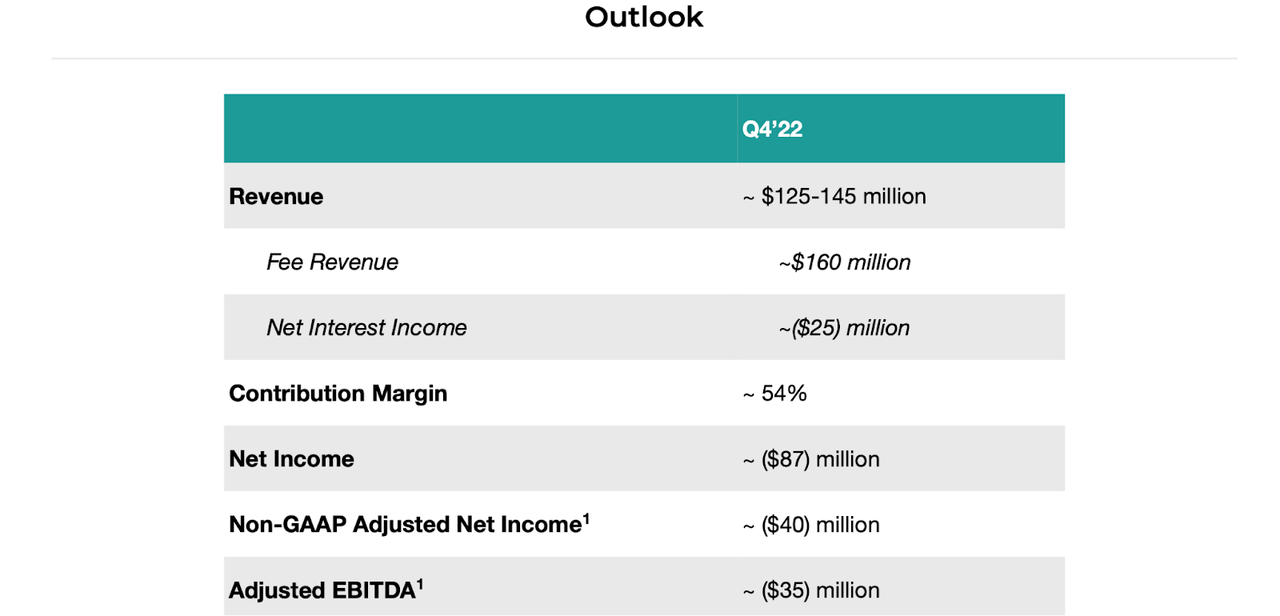

Looking ahead, UPST expects further pain, with fourth quarter revenues expected to be around $145 million – that represents a 50% YOY decline. The adjusted net loss is expected to widen to $40 million.

2022 Q3 Presentation

On the conference call, management noted that they are approving 40% fewer applicants than a year ago, with those approved applications seeing offers 800 bps higher. The lower loan demand has come at the same time as a drain in funding supply, with many of their lending partners reducing their originations and raising their required rates of return.

UPST has responded to the slowdown by laying off 7% of the workforce, but as seen above, this was still not enough to keep the company profitable even on a non-GAAP basis.

Nonetheless, management remains bullish on the long-term prospects of the business, noting that their AI models continue to improve relative to the traditional FICO-based model, with the rate of improvement over the past 4 months being as much as seen in the last 2 years. As investors, we can only hope that these improvements eventually lead to tangible financial benefit at some point.

UPST previously noted that the rapid rise in interest rates was something that their platform was not prepared for. Management noted that they have since developed the “Upstart Macro Index” to help the company more quickly adapt and predict future levels of default. The company may need some time for this product to win back the trust of funding partners.

Does the company need to raise cash? On the call, management stated that they did not see any need to do so considering that the pace of cash burn was still modest relative to the large cash balance.

Is UPST Stock A Buy, Sell, or Hold?

UPST remains an interesting story on using artificial intelligence to increase access to lending products. UPST continues to rapidly add bank and credit union partners and investors can hope that these partners eventually increase their participation in the platform.

2022 Q3 Presentation

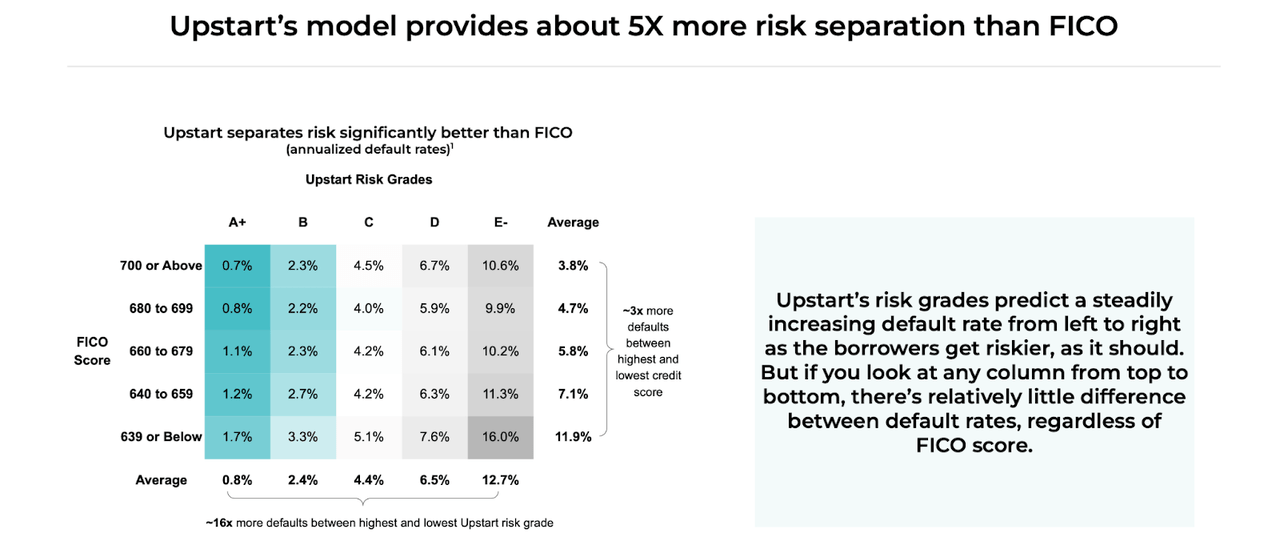

UPST estimates that its AI-based models provide 5x more risk separation than FICO – meaning that UPST is able to better identify safer borrowers and risky borrowers.

2022 Q3 Presentation

How much progress has UPST made in bringing on long term funding partners which can provide consistent funding to help reduce volatility in growth rates? And does UPST think that it needs to become a bank to address volatility in funding sources? Management stated the following:

I will say this, we believe fundamentally in a marketplace structure in the sense that a lot of lenders making independent decisions over the long haul is going to get to the right answer. I mean marketplace — market-based economies are historically far more efficient than centrally planned economies. That’s a very — I would just say a very basic truism.

But having said that — so that means we don’t want to become a centrally planned economy. We don’t believe us being a bank makes a lot of sense for what we hope to pursue for lots of reasons. But having said that, we can certainly do a better job of securing supply of funding on our platform. And that can really be through some of the things we talked about getting longer-term funding agreements in place; being in more products — a more diverse set of products, such as secured products like auto loans, mortgages, et cetera.

Based on that commentary, it appears that investors will have to be patient for a while.

The stock is cheap here. UPST is trading at 1.8x sales and that is not including the net cash making up 50% of the market cap. Due to the company generating operating losses, it may be prudent to ignore that net cash because it is unlikely for the company to engage in aggressive share repurchases even at current levels. Assuming a return to 20% growth, 30% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see UPST trading at 9x sales, representing a $100 stock price. The projected upside could be even higher if growth rates recover even stronger, but there is great risk here. It is unclear when growth rates will recover, if ever. Will loan demand recover over time or will it only recover if interest rates fall? Is the UPST business model only possible under low interest rate conditions? Even as a bull who purchased the stock at much higher levels, it is difficult to give positive answers to these questions.

The way management handled the difficulties of the past year has shaken investor trust, as management has been wishy-washy about whether to hold loans on the balance sheet and whether its models can handle a changing interest rate environment. Maybe the company is making progress towards fixing those errors – but I need to see real results of those efforts before adding more to the name.

The most obvious catalyst at this point is a Fed pivot, but that makes for a rather lottery-ticket kind of investment thesis. As discussed with Best of Breed Growth Stocks subscribers, a portfolio of quality undervalued tech stocks is my chosen strategy to take advantage of the tech stock crash. The stock is priced right and I continue to find the stock buyable here but note that there are many compelling alternatives in the tech sector offering which offer less binary risk.

Be the first to comment