andresr

Upstart Holdings, Inc. (NASDAQ:UPST) has been one of the more harrowing experiences for those that bought into the “this time is different” theme. The stock is down 95% from its peak and those high triple digit price targets are beginning to look impossible. We examine three things investors should keep an eye on in 2023 as this settles down into a normal valuation.

Loan Demand & Market Share

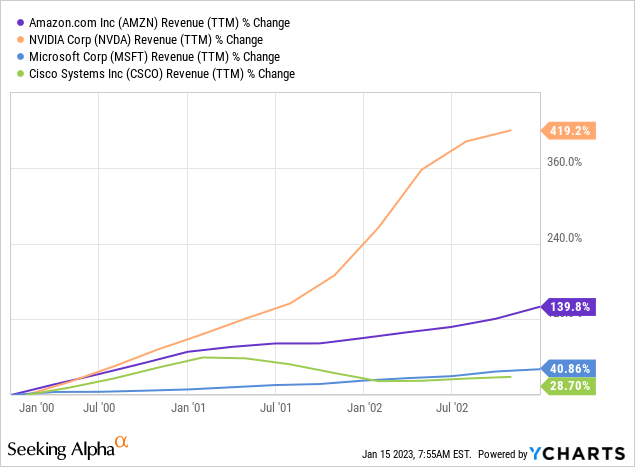

Upstart had guided for just $135 million in revenues for Q4-2022. Let’s put this growth company in its proper place here. Revenues for the same quarter last year (Q4-2021), came in at $305 million. In other words we are talking about close to a 60% revenue decline. This is important for people to understand. All those stocks which created the growth story and made it through the NASDAQ 2000 bubble, were ones that delivered very strong revenue numbers all the way into the 2001 recession. Below we have shown Amazon. Com, Inc. (AMZN), NVIDIA Corp. (NVDA), Microsoft Corp. (MSFT) and Cisco Systems, Inc. (CSCO).

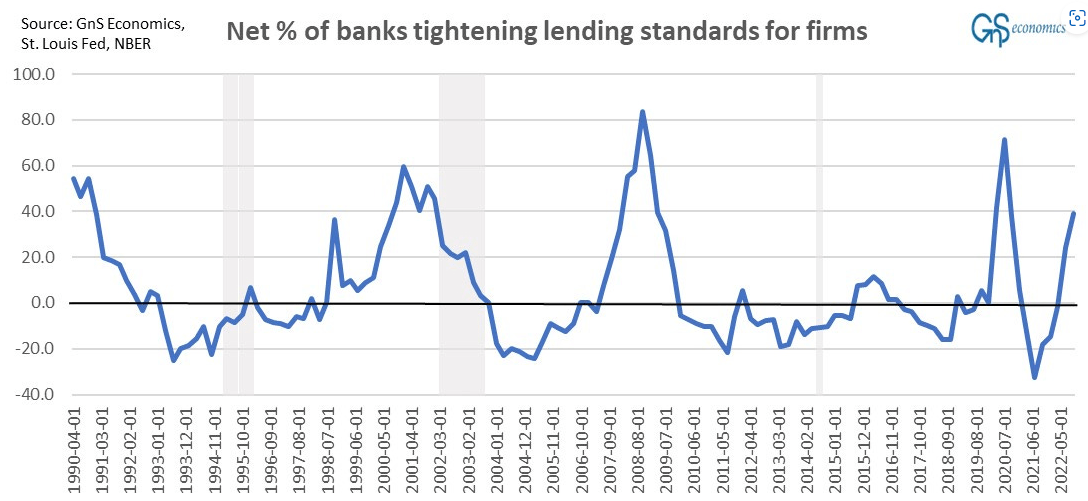

While their stocks suffered in the implosion of the tech bubble in 2000, the growth story continued to give hope that you could make it all back some day. 60% drop from Upstart is so extreme that we have to wonder exactly how much the model was dependent on extremely low interest rates. In fact, this was the perfect spot to actually prove that the model works. After all, who would not want superior loans going into a recession? Yet, we are getting the exact opposite. Nobody wants Upstart loans. This is happening just as there is a vacuum for credit. Banks are tightening loan standards and credit is harder to come by.

GS Economics

In theory, this should be the best possible time for a firm like Upstart if it is indeed as disruptive as it claims. But instead we are saddled with a 60% revenue decline. That number also suggests that Upstart is losing market share even before the recession has started.

Analyst Estimates

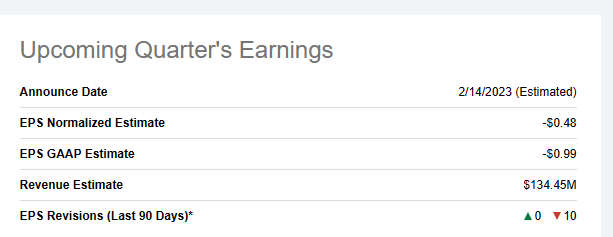

You can get a bounce from time to time in stocks that are fundamentally destined to go a lot lower. Nothing moves in a straight line. But if you want a sustainable large move up, you need analysts to have an upgrade cycle in place. In other words, they need to have underestimated the firm’s potential. Let’s see Upstart with that lens. For the upcoming quarter, analysts have zeroed in on the company’s guidance using little imagination as to what will actually happen on Valentine’s Day.

Seeking Alpha-UPST Estimates

This is despite some massive misses by the company and lowering of guidance in the last 9 months. For the year ahead, analysts have been trimming estimates with a fury. 10 out of 10 analysts think that they were too optimistic about the company’s prospects.

Seeking Alpha-UPST Estimates

Ok, so that is the past. The problem though is that no one has a shred of realism yet. We have seen this when massive bubbles implode. Analysts tend to take a long, long time to get on board with what is happening. It is in essence an admission of failure and it shows up with realism missing in their estimates. In the case of Upstart, every single quarter, the prediction has been that it will be the trough. Don’t take our word for it, just look at the revenue estimates for the upcoming one.

Seeking Alpha-UPST Estimates

At present there is zero evidence that Upstart can turn things on a dime. What there is evidence for is that 2023 has a high probability of a recession. We would be very careful extrapolating 50% annual growth rates into a recession for this company. Until these estimates normalize, we cannot see a sustainable bottom here.

Cash Burn

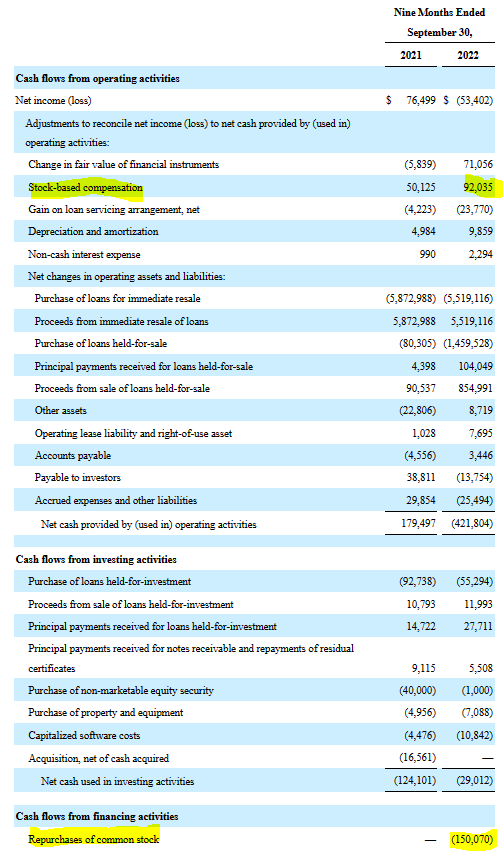

One final piece of the puzzle is where the cash goes. Obviously, we have had a pessimistic view of this company for some time, and we think that losses will likely be huge as revenues fail to materialize. For the current quarter, GAAP loss will be about $1.00 and that works out to $4.00 of losses for the coming year. Some of these will be cash losses and some of it will be stock based compensation related losses. Unfortunately, Upstart has been using its balance sheet cash to buy back shares. In this manner it is converting its non-cash losses into cash losses.

UPST 10-Q

We also think that cash losses will also accelerate as reverse economies of scale kick in.

Verdict

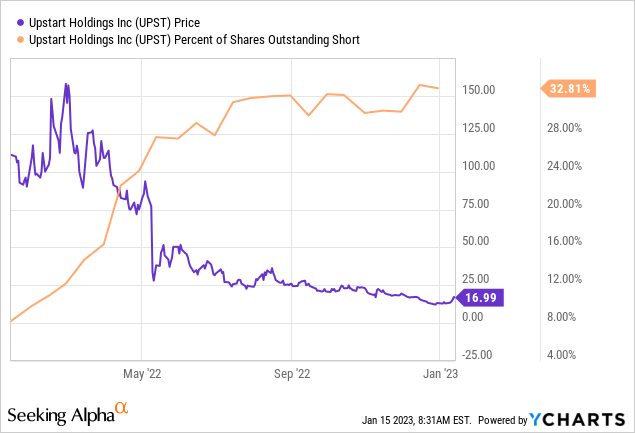

It is always tough to convey the long term challenges of Upstart while making sure everyone gets that the stock could move 10% higher in a single day. Certainly, with the high levels of short interest, squeezes are always possible.

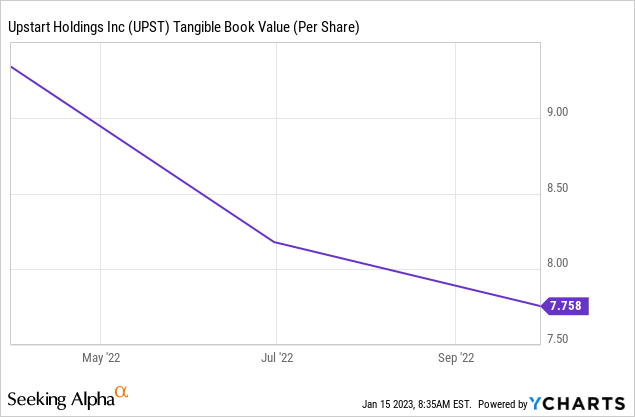

What we do have for you though, are the facts. The fact is that the company’s losses will be at a $4.00 annualized run-rate in the coming quarter. The fact is that you can pull up the tangible book value per share on any finance website.

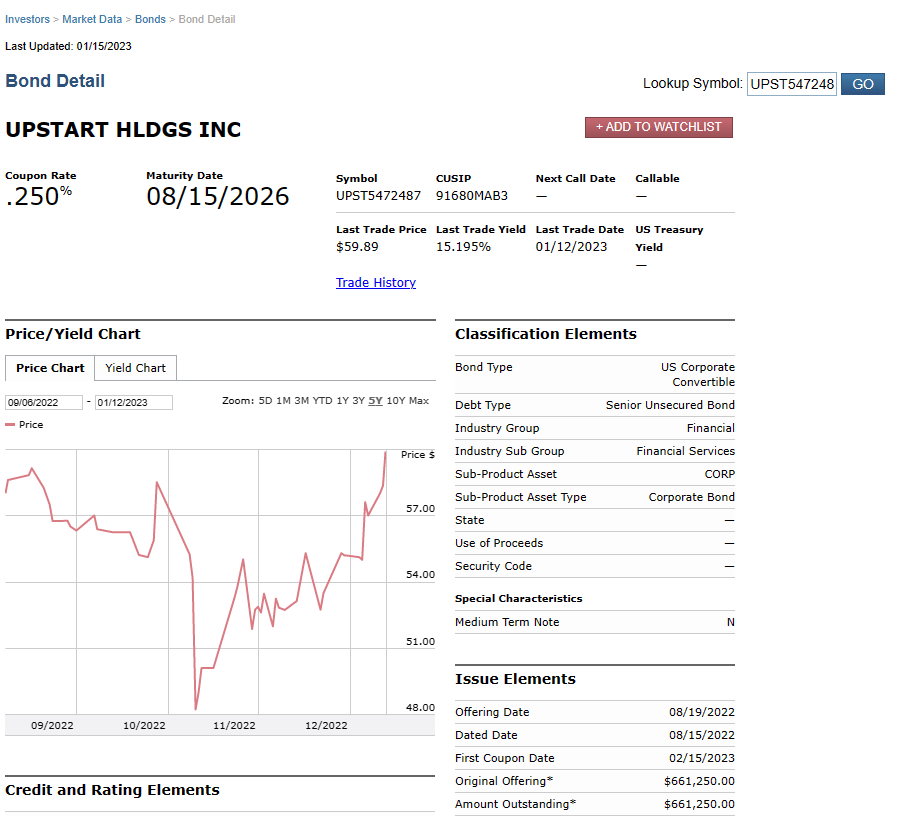

So if these levels of losses persist, you can extrapolate where that goes in 2 years. There is a reason that this bond that matures in under 4 years has a 15% yield to maturity.

FINRA

Upstart is now on the clock and has to turn things around within 1-2 quarters. At a minimum this requires a stabilizing revenues and ideally it will require a return to GAAP profits. If the company does land up as a benefactor of a short squeeze, it should strongly consider a massive stock issuance to buy itself more time to deliver on its promises. This may seem counterintuitive, especially considering that the company bought back stock at far higher prices, but we have to move past that sunk cost. At present we rate the stock as a hold/neutral and don’t think risk reward favors either the bulls or the bears at this juncture.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment