simarts/iStock Editorial via Getty Images

A lot has happened since my last article on the 20th of April. The bank published excellent earnings results, which made the shares rebound somewhat. However, after that, the financial markets were quite stressed out due to the Fed’s hawkish rhetoric and the ECB’s decision to raise the interest rates. This made the financial markets shatter. Although higher interest rates usually mean higher profits for the financial sector, banking stocks are more sensitive than the overall market. In other words, banks are highly cyclical and do not do well during recessions. At the same time, UBS (NYSE:UBS) is an undervalued profitable bank and its stock should eventually recover. Let me explain this in some more detail.

The bank’s financial results

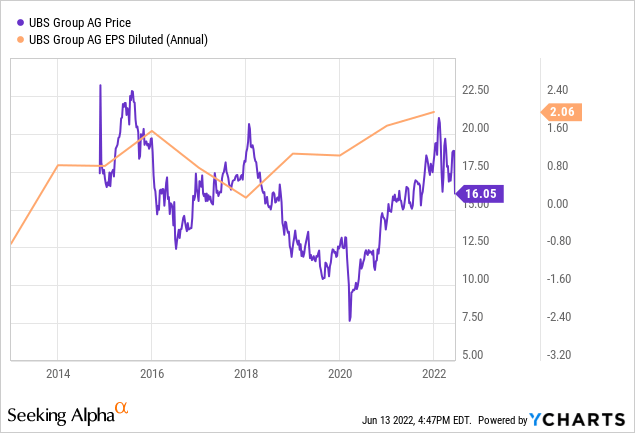

Between 2012 and 2018 the bank’s quarterly results did not show stable growth. However, between 2018 and 2022 the bank showed sound earnings per share (EPS) growth but the stock price did not follow. As can be seen from the graph below, the beginning of 2020 was a great time to buy the stock.

The same can be said about the last earnings results, published at the end of April.

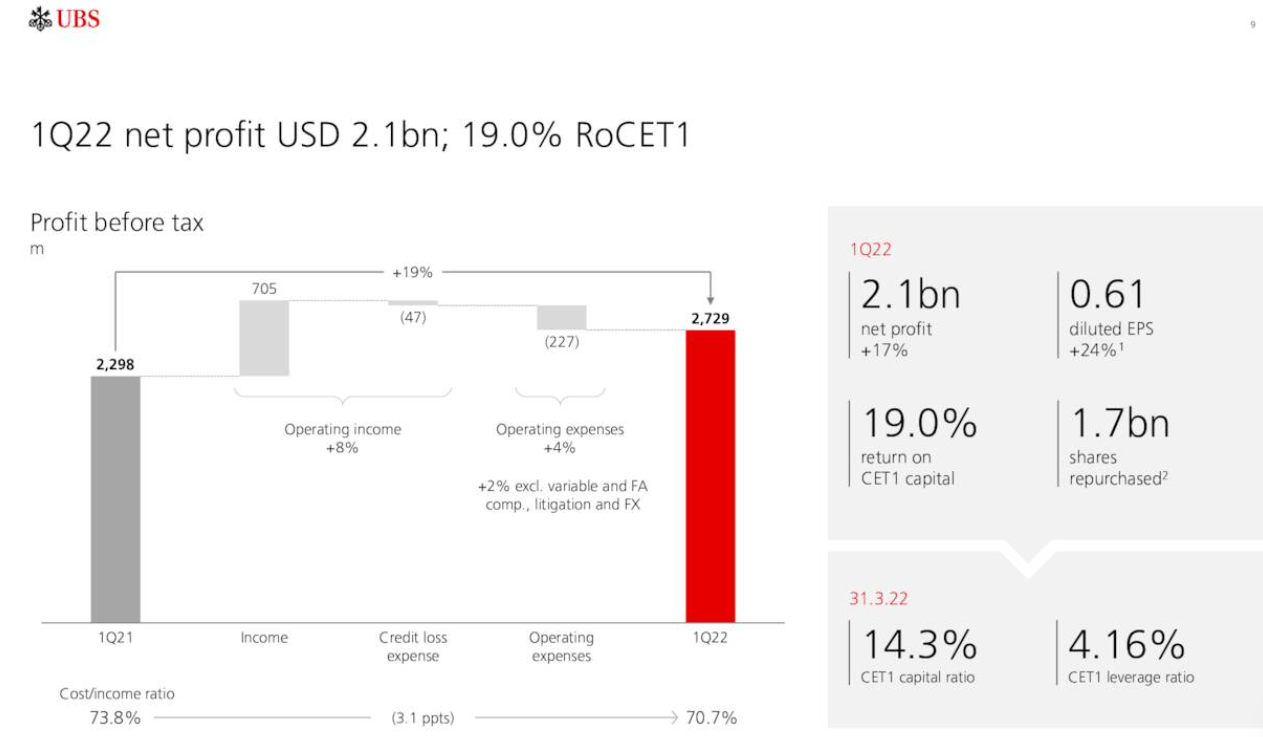

Lots of financial indicators reported for the first quarter of 2022 were really good. For example, the CET 1 capital ratio for 1Q2022 was 14.3%, whereas the requirement is 10%. The return on CET1 capital was 19%, which is quite sound given the bank’s high CET1.

The bank’s earnings presentation, slide 10

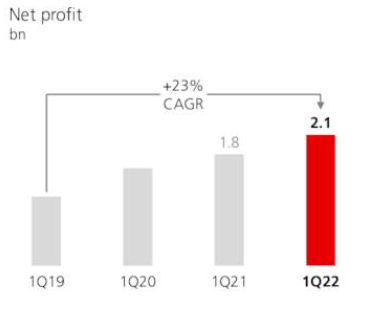

But the most important development for 1Q2022 was the net profit figure of $2.1 billion. On its own it may not mean as much but if we look at the net profit history for the last four years, we will see there was substantial growth. The net profit rose from $1.8 billion in 1Q2021 to $2.1 billion in 2Q2022, an almost 17% rise. That is quite impressive, given the bank’s conservative profile.

UBS earnings presentation

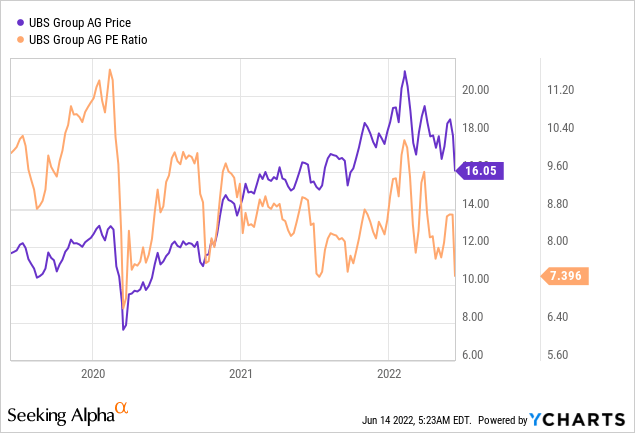

Let us assume the bank reports exactly the same profit for each of the following three quarters. So, $2.1 billion times 4 gives us $8.4 billion. The current market capitalisation is around $60 billion. If we divide the current market capitalisation by $8.4 billion, we will get a price-to-earnings (P/E) ratio of 7.14, which is not high at all.

In fact, if we have a look at the graph above, the bank’s P/E ratio is now hovering near its 3-year lows. The current indicator is only slightly higher than the spring 2020 low of about 6.5. The latter was logical at the time since the global pandemic made many countries’ economies halt. So, the stock markets crashed. Right now there is also a reason for the stock price decrease, namely due to the central banks’ monetary policies.

The central banks’ monetary policies

The Fed, the ECB and even the Swiss National Bank are sounding the alarm – the inflation indicators are near their multi-year highs. The ECB and the Fed have already started raising the interest rates. The Swiss National Bank also decided to raise the interest rates. This has not happened for years since in Switzerland the inflation rate is traditionally very low or even negative.

Monetary tightening is, generally speaking, bearish for the global economy since it usually provokes recessions. The banking sector is also highly cyclical and is affected by the macroeconomic conditions. However, we can also safely say that, provided there is no recession, rising interest rates should raise the financial sector’s interest income – profit from borrowing and lending. So, it really depends on where the economy is heading next. Nevertheless, UBS is not a very standard bank, in that sense.

UBS as a bank

As a bank UBS would not lose much even if there is a serious recession. Here, I do not even hint at the fact the Swiss government came to the rescue of UBS when there was the 2008-2009 crisis, also affecting Switzerland. After the crisis the UBS changed their risk profile and became more conservative than they used to be. That is logical since UBS is a bank for the rich. In other words, it does not rely too much on lending money to highly indebted individuals and businesses.

That is a great positive for UBS – in other words, it would not suffer from its clients’ bankruptcies to the extent its peers would, since it does not have risky clients.

Although I do not know exactly when this correction would end and if there is a recession any time soon, in my view, buying UBS at a discount would make perfect sense since it is “recession-resistant”.

Technical analysis

By all means, technical analysis is only secondary to the fundamental one. However, I decided to conduct some analysis using Bollinger bands.

In other words, the bank’s stock price moves within certain bands or lines. It is in a certain trend. Right now the 5-year trend seems to be upward. There is some volatility and information noise over the way but overall the trend remains intact.

TradingView

On the graph above since 2020 there is an upward move of the bank’s stock price. Provided there is no recession in the next several month or any other significant financial distress, UBS stock price would keep rising and investors would do well if they buy when there is “blood on the streets”.

In my view, it is not a good idea to invest when the stock market indices are at their all-time highs and financial mass media advocate active investing. Just the opposite is true – it is the best to buy sound companies’ shares after their correction when everything else is crashing. UBS has not faced any significant scandals in the last several years, has reported excellent profits but its stock corrected somewhat during the market sell off.

Conclusion

UBS is a highly profitable bank for the rich operating in a cyclical sector. Its stock got cheaper mainly due to the information noise. Provided there is no recession in the next several months, the stock has great upward potential in the near future. Technical analysis suggests a strong upward trend. It is the best to invest in profitable banks when everything is selling at a discount.

Be the first to comment