Kevork Djansezian

Ubisoft (OTCPK:UBSFY) is a French-based video game company that is known for a range of iconic games from Assassin’s Creed to Splinter Cell. The company benefited from a surge in gaming demand during the lockdown of 2020, but is now going through a cyclical downturn, along with the rest of the gaming industry. A positive is the gaming market is forecast to grow at a 8.94% compounded annual growth rate and reach a value of $339 billion by 2027. In addition, Ubisoft has a series of new games ready to launch and given the industry consolidation in the gaming industry, it could even be acquired. In this post I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model

Ubisoft develops and publishes games, across a plethora of platforms from PC to consoles and smartphones. The company has developed a range of iconic games which include Assassin’s Creed, Tom Clancy’s Splinter Cell, Ghost Recon, Far Cry, Prince of Persia, and even the classic Rayman game.

Ubisoft Games (Q3,22 report)

The business makes its revenue from the sale of its games, as well as in-game “microtransactions”. In addition, the company sells merchandise and has many partnerships and licenses.

In 2019, the company launched its “Uplay” subscription service, which then became Ubisoft connect. This is a “global ecosystem” which marries together the social and individual parts of game playing. Basically, this allows users to play games with each other no matter what platform is used (console, PC, etc.). In addition, the platform offers a loyalty program and allows players to track achievements. I believe this is a great platform overall and helps to build that sense of community and further “gamify” gaming. This will likely result in increased brand strength and a competitive advantage.

Acquisition Potential and Tencent

We are currently going through a period of consolidation in the video game industry. In January 2022, Microsoft announced the monster acquisition of Activision Blizzard for a staggering $68.7 billion. This acquisition has been scrutinized by many. For example, the FTC has reportedly filed a legal case to block the takeover. However, it has been approved in Chile. Either way, this is a sign of consolidation in the industry. We also saw gaming giant Take-Two (TTWO) acquire Zynga mobile gaming for $12.7 billion in 2022. Ubisoft could be the next acquisition target. In early 2022, Ubisoft’s management commented on a potential acquisition by stating they would “review any offers”. In addition, other reports indicated leading Private Equity firms such as Blackstone and KKR were reviewing the company. Then in September 2022, it was reported that Chinese gaming titan Tencent (OTCPK:TCEHY) has invested $297 million into the company, increasing their minority stake from 4.99% to 9.99%. I believe this investment is a testament to the quality of Ubisoft’s IP and the value of the gaming industry as a whole. I believe the forecasted growth in the “Metaverse” is also a key factor in increasing the value of gaming companies. The Metaverse is basically a 3D virtual world, in which you interact with avatars, this sounds a lot like an online social game to me. I am actually surprised Meta Platforms (META), formerly known as Facebook hasn’t tried to acquire a gaming publisher, to help bolster the graphics of its Metaverse named “Horizons”. Perhaps if Meta wasn’t going through a tough financial period they would, so we could call this a prediction for the future. The Metaverse industry is forecasted to grow at a rapid 39.8% compounded annual growth rate, and be worth just under $1 trillion by 2030.

Mixed Financials

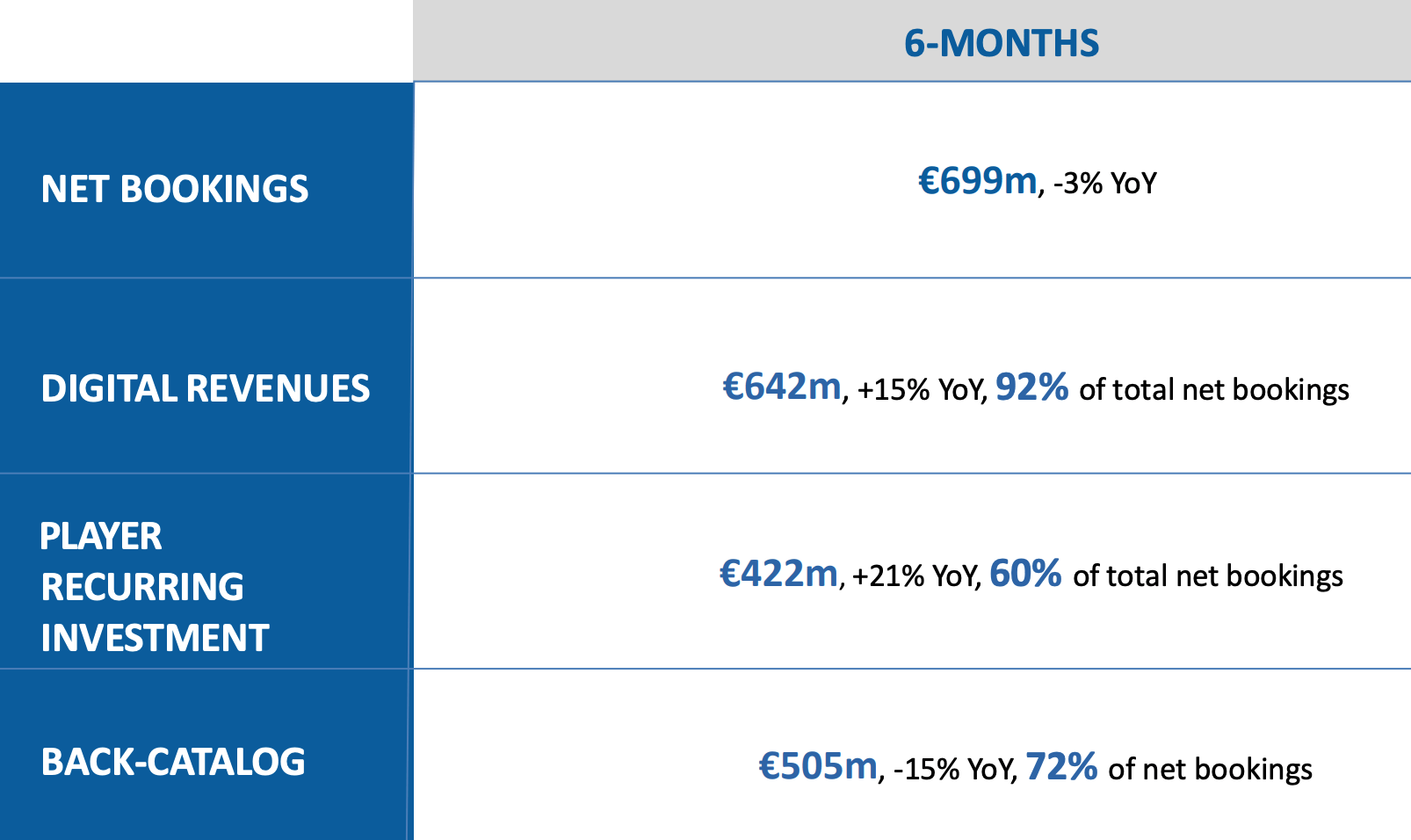

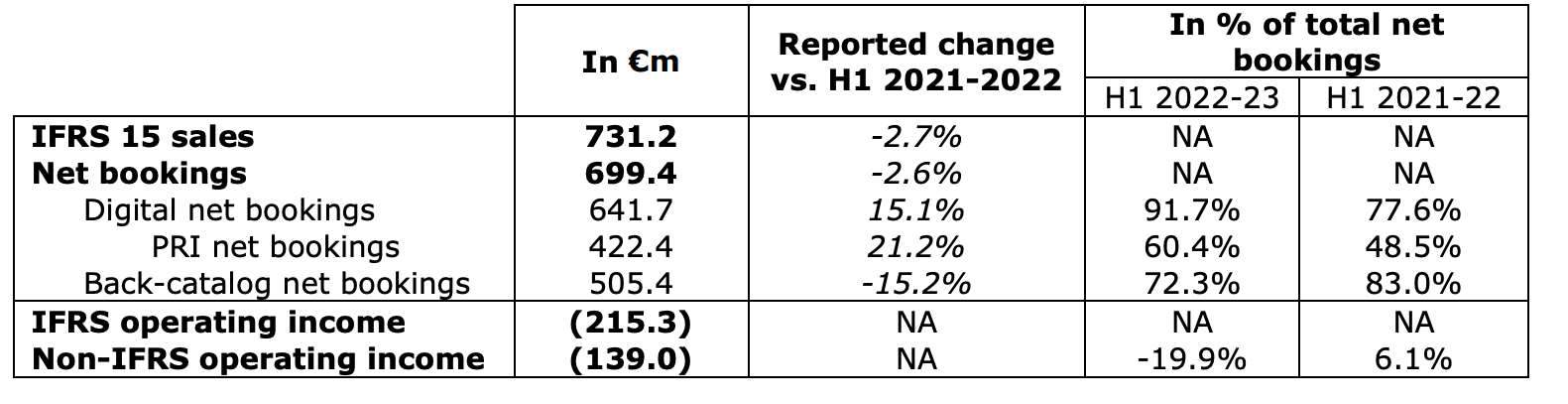

Ubisoft reported mixed financial results for the second quarter of fiscal year 2023. Its Net Bookings were €406.1m ($435.6 million), which increased by just 3.6% year over year but massively surpassed management’s forecast of €270 million. On a 6-month basis, Net Bookings were €699 million ($750 million), which declined by 3%, but again this was higher than management forecasts, given we are going through a cyclical decline in the gaming market. Digital Revenues increased by a solid 15% year over year to €642 million. Player recurring investment increased by a rapid 21% year over year to €422 million. Back-catalog revenue reported a 15% year-over-year decline to €505 million, although again management was happy with this result.

Ubisoft (Q2, FY23)

Ubisoft reported solid “outperformance” in its games such as Tom Clancy’s Rainbow Six Siege, which increased its unique players by 18% year over year to a staggering 85 million players. In addition, the Assassin’s Creed series reported strong performance across its games such as Origins, Odyssey, and Valhalla. Its Valhalla game was a key growth driver with over 20 million unique players reported. Ubisoft has also been teasing gamers with its roadmap and the market is excited about new games Assassin’s Creed Mirage and Codename Red, expected to be released in 2023 and 2024 respectively.

Assassin’s Creed Mirage (Ubisoft)

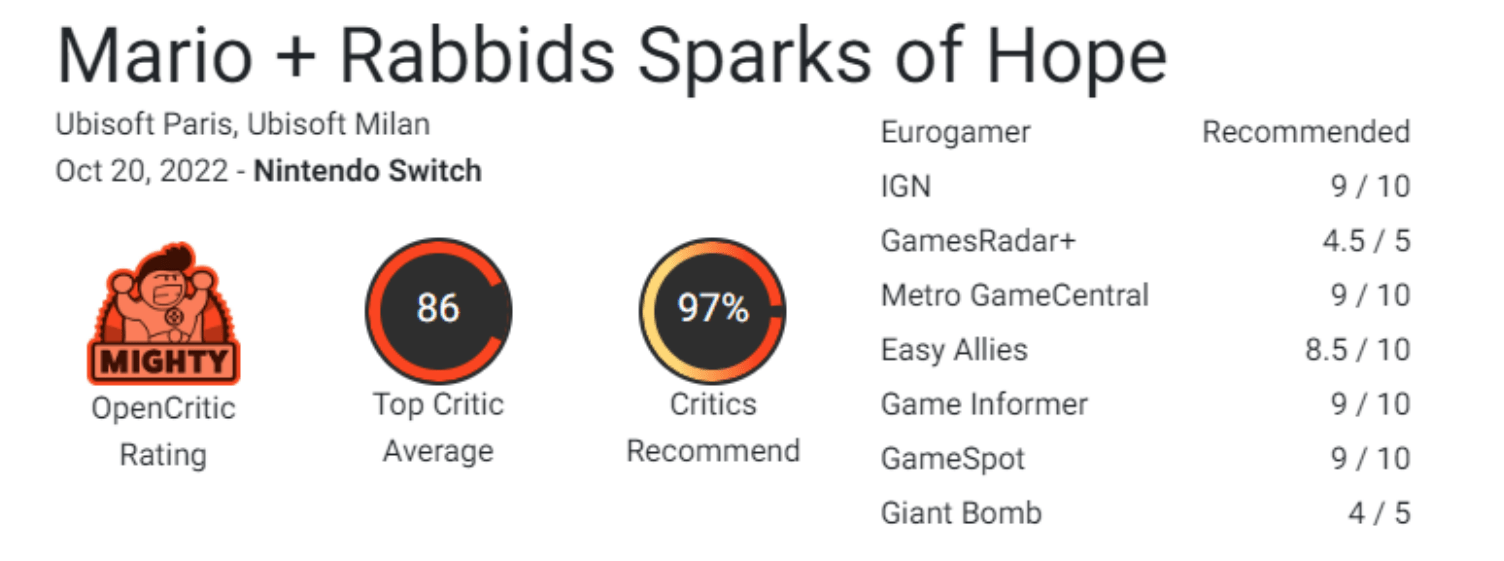

In October 2022, Ubisoft launched its Mario + Rabbids Sparks of Hope game, which was critically acclaimed. IGN gave the game 9 out of 10 stars and other review sites were also favorable.

Mario Rabbids (Gameplay screenshot)

Given the Mario game was launched after the second quarter results were released, its financials will show up in the next quarter’s results. This is expected by management to be strong (€830 million) in net bookings, for Q3, FY23. The holiday season and marketing support from Nintendo is also expected to play a part in the strong result. Nintendo has announced a Super Mario movie, which is expected to be released in April 2023. I forecast this movie to drive strong results for games such as Mario + Rabbids.

Mario + Rabbids (reviews)

Onto profitability, the company reported a Non-IFRS operating income of negative €139 million in H1, 2022-2023. This made up a negative 19.9% of total net bookings, which was worse than the 6.1% reported in the prior year.

Operating Income (Q2, FY23 result)

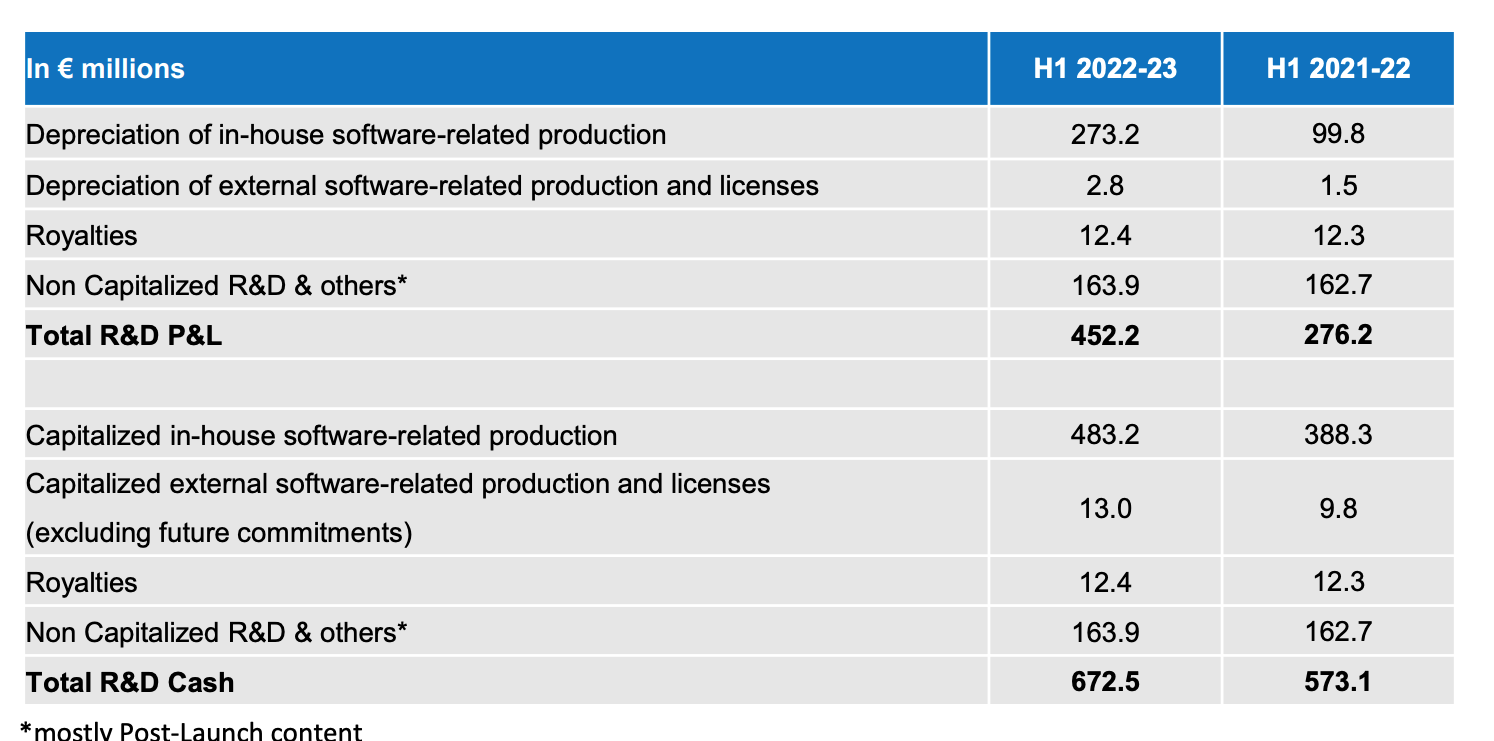

A positive is these results look to have been driven by large Research & Development [R&D] investments, which increased by ~63% year over year. Full breakdown is shown below, this is quite complex, but you get the idea. Operating income is forecast to rebound strongly in the second half of the year and ~€400 million ($429 million), is expected for the full fiscal year 2023.

R&D expenses (H1, FY23)

Ubisoft has a solid balance sheet with €1.39 billion ($1.499 billion) in cash and short-term investments. The company does have a high total debt of $2.159 billion but a large portion of this $1.163 billion is long-term debt and thus manageable, assuming Ubisoft hits its growth forecasts.

Advanced Valuation

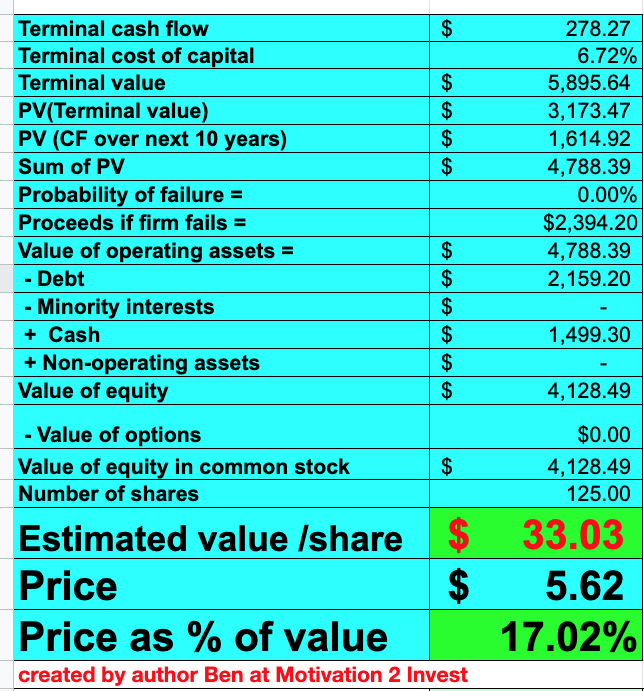

I have plugged the latest financials into my discounted cash flow valuation model. I have forecast 5% revenue growth for “next year”, which in my model includes the next couple of quarters. This growth is based upon a slight improvement in Net Bookings, driven by games such as Super Mario and new game releases in the Assassin’s Creed franchise. In years 2 to 5, I have forecasted an even faster growth rate of 7% per year, driven by a cyclical improvement in the gaming market. Ubisoft has historically generated very cyclical revenue. For example, in Q1,21 the company reported a staggering 73.89% growth in its revenue. However, since the start of 2021, its revenue has been declining by varying degrees. A similar pattern occurred in its history (pre-2020) and thus I don’t deem this to be a major worry.

Ubisoft stock valuation 1 (created by author Ben at Motivation 2 invest)

To increase the accuracy of the model, I have capitalized R&D expenses which has lifted net income. In addition, I’ve forecasted its operating margin to increase to 15% over the next 8 years, driven by management forecasts.

Ubisoft stock valuation 2 (created by author Ben at Motivation 2 Invest)

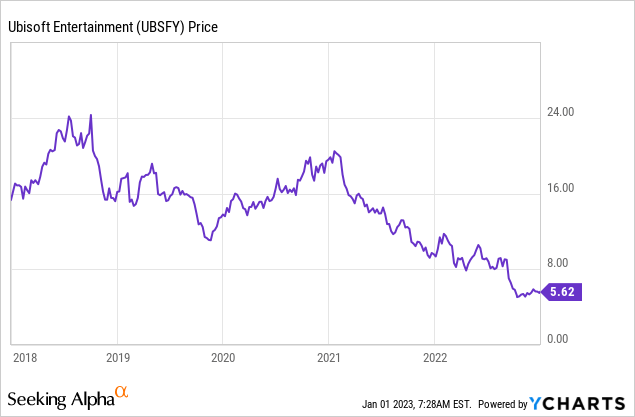

Given these factors I get a fair value of $33 per share, the stock is trading at ~$5.62 per share and thus is significantly undervalued. I have calculated its value in US dollars, which complies with the ticker UBSFY.

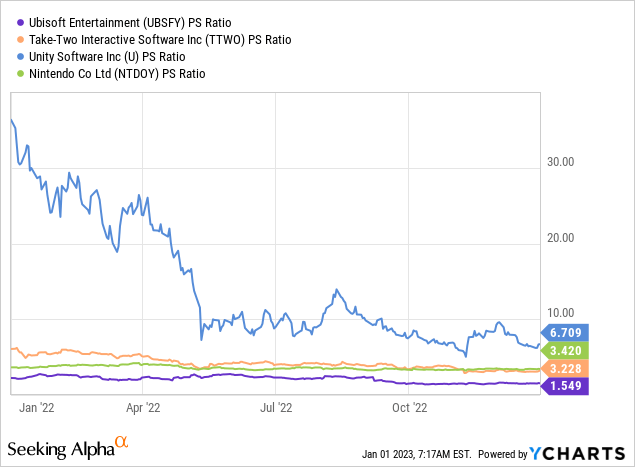

As an extra datapoint, Ubisoft trades at a price to sales ratio = 1.4, which is 56% cheaper than its 5 year average. Relative to other gaming stocks in the industry, Ubisoft looks to be trading at the cheapest level, see chart below.

Risks

Cyclical Gaming Market

The gaming market is currently going through a downturn, as I’ve highlighted in prior posts such as those on Microsoft with its Xbox. The positive is the market has been cyclical historically and the industry is forecasted to grow, stats mentioned in the introduction.

Final Thoughts

Ubisoft is a leading gaming company with a strong IP of popular gaming franchises. Given the industry consolidation and growth in the Metaverse, gaming companies are becoming increasingly valuable. Ubisoft is deeply undervalued at the time of writing, whilst it is poised to benefit from new game releases. Tencent’s investment has helped to make the company more financially secure and I wouldn’t be surprised if it got acquired.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment