SHansche

Shipping stocks enjoyed favorable fundamental conditions in the first half of 2022. Interestingly, one small-cap global player in the space did not stretch its legs until the back half of last year.

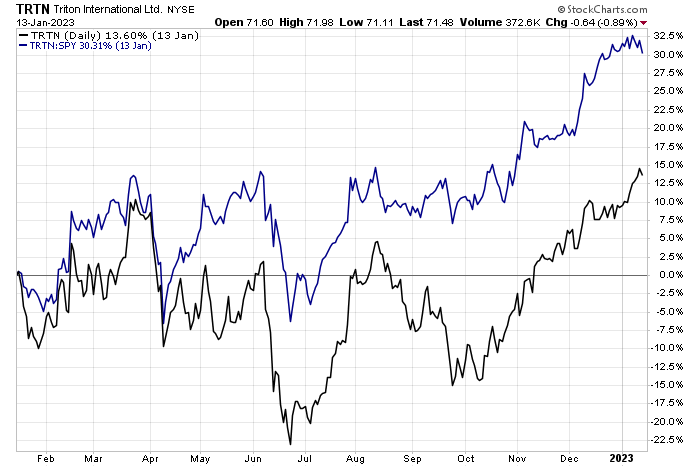

With monster relative strength in the last 6 months, are there more gains on the horizon for Triton? Let’s climb aboard and see what’s in the hull of this Industrials stock.

Triton: High Relative Strength Last 6 Months

Stockcharts.com

According to Bank of America Global Research, Triton International (NYSE:TRTN) is an intermodal container leasing company with the world’s largest container fleet with 7.04 million twenty-foot equivalent (TEU) containers. Its customers include the world’s largest shipping liner companies. TRTN has a significant global presence, including 20 offices in 16 countries and a network of 299 third-party container depot facilities in 75 countries.

The Bermuda-based $4.2 billion market cap Trading Companies & Distributors industry company within the Industrials sector trades at a low 6.4 trailing 12-month GAAP price-to-earnings ratio and pays a high 3.9% dividend yield, according to The Wall Street Journal.

Triton has a few positive headlines for the bulls to work with. The firm beat on both its top and bottom-line estimates back in October (though there was a sequential EPS forecast for its Q4). Moreover, the management team authorized an expanded $400 million share repurchase program in December. Finally, TRTN hiked its dividend by 8% in November. While growth likely slows in the coming quarters, favorable shareholder accretive activities are upsides.

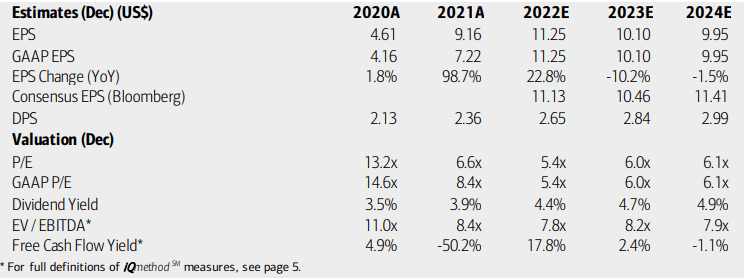

On valuation, analysts at BofA see earnings having grown sharply in 2022 after a near double in EPS in 2021. A weaker global container shipping market this year compared with high prices in the last 12 months should result in lower per-share profits over the coming quarters.

EPS is seen as steadying near $10, so that could be a good earnings number to use on valuation analysis. At a normalized 7x P/E, the stock still looks ok versus its historical 5-year average 8.4 trailing 12-month operating P/E. Moreover, its PEG ratio is quite appealing at 0.67.

Triton: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

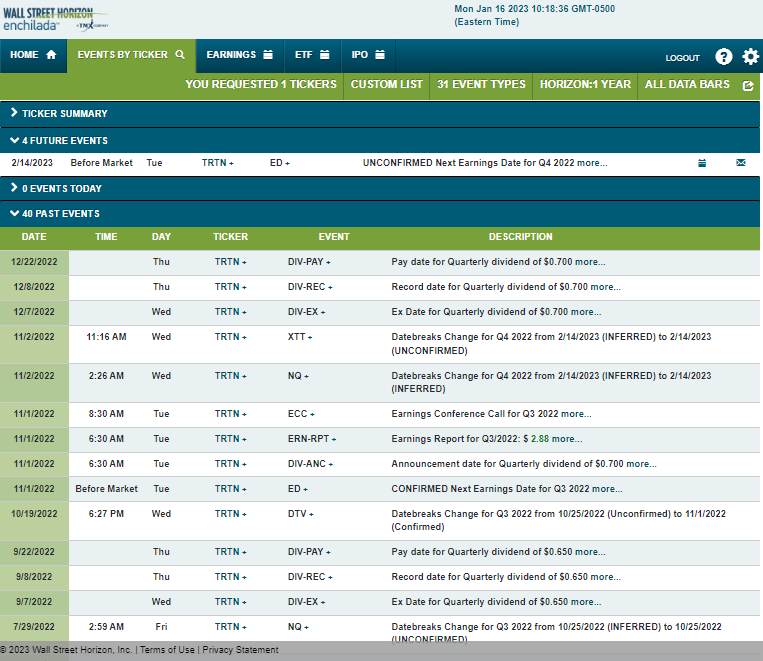

Looking ahead, corporate event data from Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Tuesday, February 14 BMO. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

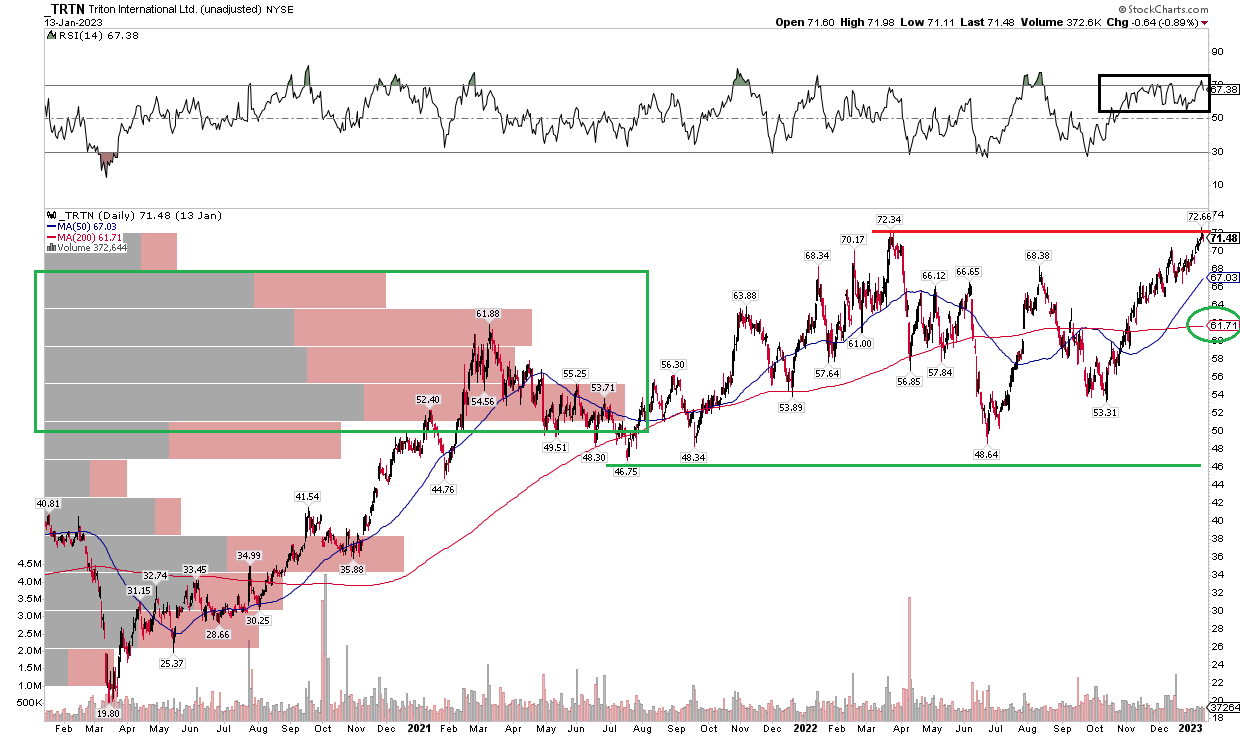

TRTN has enjoyed quite a rally in the last few months. With shares up about 25% from late October, the stock now tests its all-time high just shy of $73. I think this is a natural point of possible profit-taking, so buying a dip on the stock makes sense. But, should it break out, then a bullish price objective to near $96 would be in play based on the measured move price target using the range from the last two years.

Also notice in the chart below that there’s a high amount of volume-by-price in the $50 to $65 zone, so that range should be supportive on pullbacks. With a flat 200-day moving average, long-term momentum is actually not that great with TRTN, but short-term momentum is strong as evidenced by consistently high RSI at the top of the chart.

Overall, it’s a wait-and-see approach as the stock tests its high – we could see some back and fill. But I would be a buyer on a move into the mid-$60s or on a clean breakout above $73.

TRTN: Shares Gain Steam, Test All-Time Highs

Stockcharts.com

The Bottom Line

TRTN remains attractive on valuation despite some growth risks in the industry in the next few years. With a high yield and stock buybacks, there is a lot for shareholders to like. The chart, meanwhile, could be modestly extended in the short run.

Be the first to comment