Fotografo Mineiro/iStock via Getty Images

“In the business world, the rearview mirror is always clearer than the windshield.” – Warren Buffett

Investors have weathered the first real correction in the indices in over a year. The damage under the surface preceded this corrective phase. That selling was so severe that many analysts have labeled the recent action as a BEAR market. I’m not here to argue semantics, but I will note that if an investor hasn’t participated in the momentum trades (Energy/Commodities) they have suffered big losses.

Losing money, even if it is on paper, is very disturbing. However, before we act, we should think. Investors have watched the value of their portfolio shrink in the last two months. It’s all about what have you done for me lately, a mindset that can get any investor into big trouble.

When I mention that it’s time to think, let me clarify. The thinking has to be void of any preconceived notions on politics, headline issues, emotions, etc. That’s hard to do BUT it will only get in the way. When an investor is faced with difficult times, it is far better to evolve into a cold, calculating individual.

The first step, go back and review where the longer-term trend stands. Watching the day-to-day action will only add more fear to the equation. Reinforce that long-term view (good or bad) in your mind, because until that shows a decided change, making major portfolio changes could be premature. Of course, my reference is to those that are investors, or at the very least looking out a year or more. Traders have their own set of worries to contend with.

However, this market backdrop seems to be ever-changing for that active investor who likes to navigate the market currents while maintaining their CORE holdings in what by definition is still a BULL market. There are always many pieces to see the picture to form a strategy. Many get wrapped up with ONE piece of the puzzle that they become blind to everything else. Some investors can be like Pitbulls. Once they latch on to something they just never let go. That’s fine, but they better be right. Wading through the investment world with a closed mind will spell serious trouble for an individual’s financial future.

No doubt the recent volatility has made for a confusing market situation. When confused, it may be best to do nothing. We are witnessing stocks start at point “A”, go through a period of volatility, and wind up back at Point “A”. Sitting and watching that price action too closely will lead to overreactions and mistakes. Step back, look around and take in the market’s message. At the moment a few yellow canaries are flying around trying to tell us something.

P.S. Don’t ignore the “Canaries”

The Week On Wall Street

With the up and down gyrations of the markets recently it doesn’t feel like it but the S&P and NASDAQ started trading on Monday riding a 3-week winning streak. After Monday’s opening day rally it was all downhill for every Major index. So the notion that the S&P 500 was about to head back to the old highs was quickly abandoned.

On an intraday basis, the S&P traded down 2.8% before reversing in late Thursday trading. Despite the topsy-turvy price action the S&P 500 narrowed its loss for the week to only 55 points. However, it was under the surface where plenty of damage could be found. With only a few bright spots, this equity market continues to be frustrating and directionless.

The Fed

I rarely pay attention to “Fedspeak”, as I labor under the assumption if it’s not coming out of Fed Chair Powell’s mouth it isn’t policy. This week Lael Brainard had her 10 minutes of air time and in her prepared statement revealed her views on the inflation problem.

“Accordingly, the committee will continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting.”

In the three weeks, since they last met, many Fed officials have indicated they could support raising rates by a half percentage point instead of the traditional quarter-point at their coming meeting on May 3-4. Interestingly Ms. Brainard didn’t elaborate on that debate in her prepared remarks Tuesday. However, according to analysts/economists, the probability of back-to-back 50-point rate increases is now elevated.

At the same time, Ms. Brainard said she expected several factors to bring supply and demand into better balance this year, which could bring inflation down. She cited factors including a slowdown in foreign growth, a decrease in U.S. federal spending, an increase in the supply of workers, and a drop in demand due to higher borrowing costs.

On the federal spending comment, investors can only hope someone starts paying attention. On the drop in demand due to higher borrowing costs, I believe we will have to see just how much impact these increases have on a 7% inflation rate.

When it comes to spending, I do know one person that isn’t listening to Ms. Brainard. There is a proposal from Gavin Newsom, the Governor of California that says he’s going to send money to drivers to help them deal with the high inflation/gas problem. What? You’re going to increase government spending to reduce inflation that was largely caused by government spending?

More proposals for programs like this one and the inflation fire burns hotter and longer.

Ms. Brainard’s comments set the stage for the unveiling of the minutes from the last Federal Reserve meeting:

“Many participants noted that – with inflation well above the Committee’s objective, inflationary risks to the upside, and the federal funds rate well below participants’ estimates of its longer-run level -they would have preferred a 50 basis point increase in the target range for the federal funds rate at this meeting.”

So that should “officially” set the stage for a 50 basis point increase at the next Fed meeting. In my view, this was ALL telegraphed at the last meeting. The handwriting was already on the wall and this isn’t such a huge surprise. Analysts and economists will now extrapolate that to 50 basis point increases in multiple monthly meetings. Perhaps that will indeed be the case, but only if inflation stays elevated. My “guess” is that it will, and the stock market is now in the process of digesting what that could mean for the economy.

The Economy

The seasonally adjusted final S&P Global US Services PMI Business Activity Index registered 58.0 in March, up from 56.5 in February. The increase in business activity was steep and the quickest in 2022 so far, accelerating further from January’s Omicron-induced slowdown. Many companies stated that the easing of COVID-19 restrictions boosted client demand.

This report falls in line with my consumer-led “services” spending thesis.

The Global Scene

Meanwhile, the conflict is taking its toll. Since Russia’s invasion, eurozone sentiment and German Ifo expectations have plunged to early pandemic lows. Sentiment toward stock markets around the world broadly deteriorated in April as reported by Sentix this morning. The single major exception was Eastern Europe, where 6 months ahead sentiment improved sequentially from a record low. Below we show current and forward sentiment across a scope of global economies covered by the Sentix survey.

Markit Global PMIs for a range of countries (Services and Composite) were updated this week with minor changes.

Eurozone – Slight decline from 55.5 to 54.9

Japan – Rose sharply from 44.2 to 49.4

India – fell slightly from 54.9 to 54

Earnings

Earnings season is set to begin on Wednesday, April 13th with several Financial companies reporting. The preannouncements and reports recently have been more muted than we have become accustomed to in aggregate. The level of earnings beats has been moderating in recent quarters though still above the 15-year average of 5.3%.

“Early Q1 reporters” have only been surprising by 1.1% thus far. Additionally, only 69% of these “early reporters” have beaten the bottom line. While this is in line with the 15-year average, it would be the lowest since Q1’20. There has been a decent correlation between ISM New Orders and the % of Positive Earnings Surprises over the past 15-years, and ISM New Orders have remained elevated lately. It will be interesting to hear companies update their results and outlooks regarding input costs, consumer demand, and margins.

FOOD FOR THOUGHT

No surprise, inflation continues to run HOT. In the inflation story, energy costs show up everywhere. Yet, the present policies will keep those costs at high levels.

The current regulatory environment has cut off lending to the Oil and Gas industry from large money center banks, and now private equity is abandoning the sector as well.

The administration recently announced another tapping from the Strategic Petroleum Reserve which amounts to 1 million barrels a day for the next 6 months leading up to the mid-term elections. The entire draw amounts to 9 days’ worth of U.S. consumption.

Whether it has weakened and made the U.S. vulnerable is a debate for another day, suffice to say ALL should agree the SPR doesn’t exist to try and curb short-term gasoline prices before an election.

What has been accomplished is to ensure longer-term demand stays high as by design this emergency deposit has to be replenished and in certain instances with interest. In the case of oil, that means more barrels will have to be added to the resupply.

Any investor hoping for, or anticipating a change that would lower the price of energy will have to wait for another time. High Energy costs mean inflation stays around for a lot longer than many are anticipating. A Fed Funds rate AFTER the 7-8 rate increases that are expected, will not put a dent in a 7% inflation rate.

In addition to the Canaries, I see Lemmings plummeting into the sea.

The EU didn’t shoot themselves in the foot with their “green agenda” they shot themselves in the head. They’re on life support and waiting for the neurosurgeon to take the bullet out. The U.S. is following the same path. The fact remains that the global economy is bringing millions of people out of poverty every year. These consumers want to live first-world living standards. And first-world living standards involve the consumption of gross amounts of petroleum-based products. PERIOD, end of the statement. To believe otherwise is a fantasy.

The Russian/Ukraine war has put a spotlight on REALITY from the tragedy of death and suffering to what is needed to run the global economies of the world TODAY. Despite the attempts to RUSH into renewables, this war has made it abundantly clear the global economy is VERY dependent on oil. Those that thrust the globe into an energy crisis have shown they can’t deal with reality, and that was abundantly clear from the outset. Now that plan has produced terrible consequences for society in general. Hundreds of millions are impacted now all in the name of “climate policy”.

It’s certainly a priority to promote renewable energy, but ignoring the fact that first-world living standards are still hugely dependent on oil is going to cause continued severe economic repercussions the likes of which have not been seen in decades. Until the mindset on energy policy changes to REALITY, the global economy is at great risk of a long-drawn-out recessionary period.

It’s not just an energy policy. Mistakes continue to pile up. Inflation is at a 40-year high. The 6th extension of the student loan repayment “pause” was announced this week. With 10+ million jobs available, there are plenty of opportunities not to mention the unemployment rate for a college-educated individual is 2%. In addition, the money used to repay that debt never enters the overheated economy which is what the Fed is attempting to do by raising interest rates. In essence, this amounts to stimulus to an economy that is saddled with red hot inflation.

One issue we never hear about is the “cost”. The Department of Education recently reported that the pause in student loan repayment has cost the government $98.4 billion so far – a number that will continue to rise. The current student loan forbearance period costs the federal government about $4.3 billion per month, according to the Congressional Budget Office (CBO).

Finally, the students who paid off their debt are tossed to the curb as this policy labels them fools for doing the right thing.

There is always a chance “changes” come along to offset the policy mistakes which are mounting up. It’s why I don’t jump to a conclusion today, BUT time is of the essence, and so far investors are watching policy announcements by people who are playing their fiddles.

The Daily chart of the S&P 500 (SPY)

Another volatile topsy-turvy week. Initial support has held leaving the index in the middle of what can be called a very wide trading range between 4100 and 4800.

S&P 500 4-8 (www.FreeStockCharts.com)

Within that range, almost anything can occur and with a 700 point range to deal with the investment backdrop is about as firm as a bowl of jello. Hats off to anyone that can come up with a short-term forecast from these levels.

INVESTMENT BACKDROP

I started this week looking at headlines from Morgan Stanley and others telling investors:

“The BEAR Market Rally is Over.”

Rather than attempt to either rationalize or argue their views, it’s better to take that for what it’s worth. It just might be a great “contrarian” signal, but it does define the present investment backdrop.

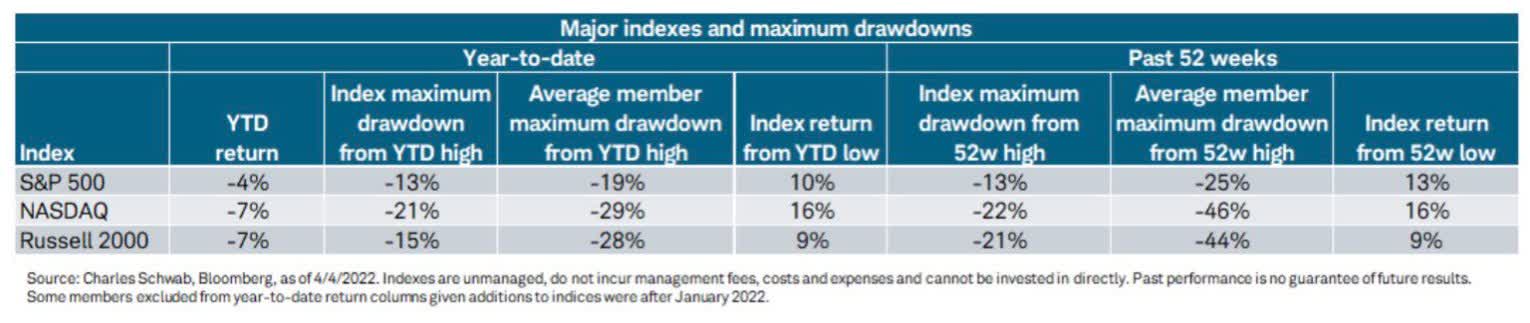

While we use the indices as our guideposts, this table highlights just how tough it has been to navigate the equity market this year.

Major Indices – Drawdown (www.schwab.com/)

The “average ” stock has suffered mightily, and if your portfolio has suffered more than the indices you aren’t alone.

The playbook for this year is ever-changing and it’s about to change again. Every correction doesn’t have to turn into a crash. However, that’s a tough sell to investors watching the violent swings we have seen in the equity markets lately. You could easily make the case that we are in a different market environment now where the bears have control.

As if investors need more concerns, at the moment all this chatter about an inverted yield curve and a looming recession has added more uncertainty to the mix. We’ve seen how there are days when the positives are accentuated, followed by days when it is all about the negatives. I think we see this market behavior continue.

I’m staying with what is working, trimming what I believe won’t be working in Q2, and waiting to see how Q1’s earnings look before I make any more decisions on strategy. This is the time to be that cold calculating investor I talked about earlier.

If you think it’s been a bad year for stocks so far, check out Treasuries as the long end of the curve (TLT) is down over 14% YTD.

The 2022 Playbook Is Open For Business

Thank you for reading this analysis. If you enjoyed this article so far, this next section provides a quick taste of what members of my marketplace service receive in DAILY updates. If you find these weekly articles useful, you may want to join a community of SAVVY Investors that have discovered “how the market works”.

BIFURCATED MARKET

It’s been a rough week for the broader market. Coming into the last day of trading for the week, the S&P 500 declined more than 2.5% over five trading days. In looking at the performance of individual sectors over that span, performance has been about what you would expect in a tape with a more defensive tone.

While cyclical sectors like Industrials, Consumer Discretionary, Technology, and Financials have been crushed with declines of more than 4%. Defensive sectors have bucked the trend. Utilities have risen more than 3%, Real Estate is up over 2%, Consumer Staples have risen 1.8%, and Health Care is in the green. This behavior contrasts sharply with the market environment in 2020 and 2021 and has some investors dazed and confused.

One day technology is back in favor, the next it’s dumped like toxic waste. Our first “Canary”, the Dow Transports sold off and in 8 trading days lost 13%. “Canary” number two fell over as the Semiconductor ETF (SOXX) dropped 14% in the same period. These two sectors can be used as barometers of the economy, and the message this week is “wake up and listen”. Unless we start to see stabilization and a very quick turnaround from these levels, the market is forecasting weak results for the economy that might come quicker than some are anticipating.

SMALL CAPS

The Russell 20000 small caps (Canary #3) are also a good way of gauging what comes next for the U.S. economy. This back and forth action continue to give conflicting signals, BUT once again the index has failed to break up and out of its trading range and with a 3.8% loss this week is now moving back to the bottom of said range.

SECTORS

ENERGY

WTI seems as if it may settle into the $95 -100 range I was forecasting after concluding the spike to $130 was unsustainable. The Energy ETF (XLE) remains in a solid uptrend, just below overhead resistance. My focus has been adding select Energy stocks that are offering Base + Variable dividends that can bring a total yield north of 7%. To that end, I added another E&P player to my holdings this week. While it’s clear this trend may slow, I do not believe it reverses anytime soon. In the meantime, the dividend yields offer excellent rewards.

CLEAN ENERGY

“Solar” and “Lithium” are two themes I have been playing since early March when they also suffered pullbacks during the general market weakness. The back and forth volatility will continue, but the clean energy theme will continue to be highlighted and these trends should remain in favor for a while.

From November of last year until the beginning of March both of these clean energy themes were trashed because they fell into the HIGH PE category. Babies were tossed out with the bathwater as some very profitable solar companies were sold off hard.

For the most part, Lithium stocks are still trading on the “dream” and the notion that there will be two EVs in every garage. I still consider it a momentum play and a “trade” that over time will morph into a very necessary industry where it will have its ups and downs like all others involved in the auto industry. To that end, I added to my lithium holdings this week on the recent dip.

FINANCIALS

The overall growth slowdown theme is also being exhibited (Canary #4) by the price action in the Financial ETF (XLF). The ETF has headed back to potentially test the March lows. A stalwart like a “JPMorgan” is now by my definition in a BEAR market trend. If that’s not a sign to sit up and take notice, I’m not so sure what is. I’m positioned with a lean to the Main street(regional) banks as opposed to the Wall Street banks. However, that group is also being tossed away as well.

COMMODITIES

This group continues to shine and one of the best places to be has been a metal I mentioned earlier – Uranium. An 8+% rally this week added to the 8+% rally in March makes this sector an outperformer this year.

This week I extended my reach to other precious metals, by adding an established mining company with a proven track record, offering a hedge against inflation. A South African mining company selling at a very inexpensive valuation that tracks the price trends of platinum and palladium closely.

GOLD

After pulling back from resistance on March 8th, the Gold ETF (GLD) continues to meander in a narrow trading range. The Gold Miners ETF (GDX) is also just under near-term resistance but in my view has a slightly better chart pattern working now

HEALTHCARE

This group continues to perform in a tough market. Large-cap Pharma caught a bid this week with one of my favorites – Pfizer (PFE) finding buyers that moved the stock 5.8% higher.

During selling events, I look for stocks that are showing a potential “reversal” in trend. In this case, the selection is also part of a resilient healthcare sector. CVS Health (CVS) – In the prior 2 weeks the stock fell from 110 to 100. From that low point where I picked up shares midweek, the stock finished the week at $106 up 6+%. The LT trend is in place and CVS pays a 2.2% yield. I advised clients to add as a quick trade or added as a Long Term holding.

There is plenty of opportunity in this market.

REITs

The 2-week rally for this group (XLRE) has now reached ~5%. Select companies in this sector offer dividend income and a chance for some growth as well. Digital Realty Trust (DLR) is one that I continue to recommend. It recently rallied 5.7% off of its intermediate-term support level and yields 3.2%. Despite the angst about the tech sector, properties of this data center REIT will continue to be in demand.

TECHNOLOGY

You don’t need me to tell you that 2021 has been a volatile year for the stock market, but in one way it has been even more volatile than you think. Nowhere in the equity market has the uncertainty and day-to-day moves been higher than in the Nasdaq.

Bespoke Investment group:

Over the last 50 trading days, the Nasdaq’s average daily move has been a gain or loss of 1.76% and on a YTD basis, the average remains at a still unsettling level of 1.66%.

To put this in perspective, in all of 2021, there were only 37 days that even experienced a gain or loss of 1.66% or more. However, this pales in comparison to the Financial Crisis when the average daily move approached 4% per day. That was even greater than the highs from the bursting of the dot-com bubbles when 3% daily moves for the Nasdaq were routine.”

The Tech sector is represented by the SPDR Select Technology ETF (XLK) and like the NASDAQ it experienced quite a bit of selling pressure. However, the ETF did rally 15% off the March lows and has now given 6% of that move back.

UTILITIES

It’s been a HOT sector, up 4.7% in ’22 and +19+% in the last 12 months. Investors are “hiding out on this group fearing the worst is about to come. Admittedly I have missed this “trade” with Utilities being an underweight position in my portfolio. Now that they have run to these levels, I do advise some caution. No matter what metric one wants to use to “value” this group, momentum has carried the stocks in the sector to their highest valuation levels in years. With a PE of ~29, it sells at levels that are higher than some of the best growth names in the universe while growing 1-2%.

Sentiment drives stock prices a lot more than the average investor believes.

CRYPTOCURRENCY

After rallying 25% since March 13th, Bitcoin stalled right at its 200-day moving average earlier this week. A stall is to be expected in the near term after such a massive move higher as demand just runs out of steam. That the stall occurred right at resistance at the 200-day moving average isn’t surprising either given that technicals appear to be widely used in the crypto trading community.

Bitcoin (www.bespokepremium.com)

Bitcoin stopped going down right at new support that has briefly formed from its prior high points seen in early February and again in late February. That didn’t last long. On Thursday Bitcoin traded down to the 43K range leaving investors scratching their heads and wondering if support will form at the 50-day moving average.

Ultimately either upper resistance or lower support will break in the coming days/weeks, which leaves the door open for a sharp move either higher (if resistance at the 200-DMA breaks) or lower (if support at the 50-DMA breaks).

FINAL THOUGHT

There are times when an investor searches for a “Canary in the Coal Mine”. A “tell” that there could be trouble ahead. Most of the time they “conjure up” an issue. Market participants can go back and forth on the policy issues, and debate the data about interest rates and inflation that guide many investment decisions. Price action is “black and white”. As I look over the landscape, multiple canaries are telling investors to wake up. The Dow Transports, Semiconductors, Financials, and the Small-cap US-based Russell 2000 are a “tell”.

While the canaries are dropping, others species are flying, and that’s where an active investor has to be these days. My strategy doesn’t call for quick knee-jerk reactions, as it allows ALL “issues” to play out. However, as I wrote earlier unless these market signals change course and reverse quickly, 2022 will continue to be a very challenging year.

Either way, it continues to be a backdrop that is nearly impossible to come up with any short-term forecast. That simply means I stay nimble and open to any possibilities.

“Our prayers and thoughts should be focused on the plight of the Ukrainian people who are under unimaginable stress.”

POSTSCRIPT

Please allow me to take a moment and remind all of the readers of an important issue. I provide investment advice to clients and members of my marketplace service. Each week I strive to provide an investment backdrop that helps investors make their own decisions. In these types of forums, readers bring a host of situations and variables to the table when visiting these articles. Therefore it is impossible to pinpoint what may be right for each situation.

In different circumstances, I can determine each client’s situation/requirements and discuss issues with them when needed. That is impossible with readers of these articles. Therefore I will attempt to help form an opinion without crossing the line into specific advice. Please keep that in mind when forming your investment strategy.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

Be the first to comment