D-Keine/E+ via Getty Images

Summary

Market fears are back at their highest levels since March 2020 as higher interest rates, persistent inflation, and the likelihood of an economic slowdown have contributed to continued uncertainties for equity markets. With the S&P 500 Index (SPX) down over 22% YTD along with most sectors in the red (ex-energy), short-term investors may be seeking to earn returns through other asset classes. Many turn to volatility markets, which have spiked considerably during the second quarter of 2022.

One popular VIX ETF product investors can use is the ProShares Ultra VIX Short-Term Futures ETF (BATS:UVXY). This investment vehicle, as described by the well-known ETF issuer ProShares, “seeks daily investment results, before fees and expenses, that correspond to one and one-half times (1.5x) the daily performance of the S&P 500 VIX Short-Term Futures Index”. This essentially means in theory the fund is designed to generate 1.5x times the returns of the VIX. However, since the VIX futures curve is typically in contango, ProShares needs to constantly roll its short-term futures contracts to the next month at a higher price than where the VIX currently trades. This is why typically UVXY trades negatively in the long run despite the VIX index being higher over the last few years. However, since the VIX futures curve has been in backwardation recently, I believe UVXY has become overpriced. When the VIX returns back to its normal futures curve, UVXY will likely decline considerably as it will become more expensive to roll its short-term futures contracts.

Why UVXY Has Generated Positive Returns Recently

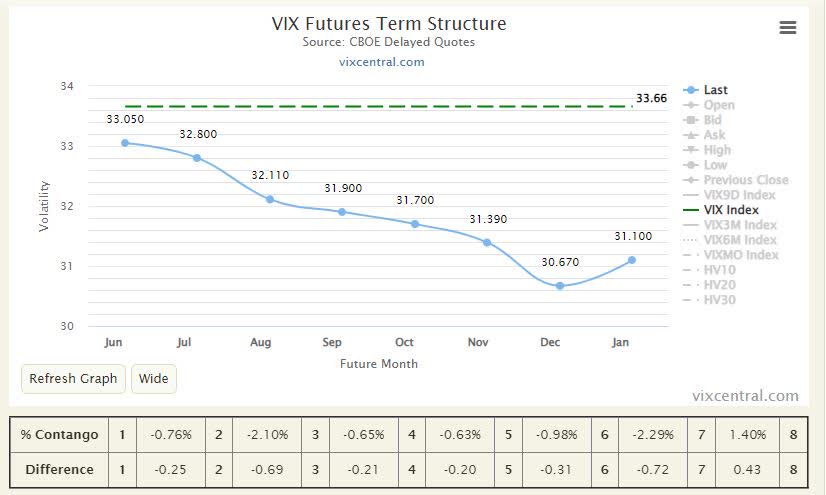

Volatility has remained elevated since the beginning of the pandemic. Prior to 2020, the VIX was hovering around $12-15 whereas over the past two years it has consistently traded over $20. Even during the bull market throughout 2021, the VIX was still very elevated compared to 2018-19 levels. As many of you already know, equity markets across the world have struggled significantly during the first half of 2022, leading to a higher VIX, up over 70% YTD to just under $30. During these short-term spikes, futures markets can become a bit erratic, which is exactly what happened to the VIX. Figure 1 below shows the VIX futures curve from earlier this month and how futures prices have been below spot levels.

Figure 1: VIX Futures Term Structure (June 15th)

VIX Term Structure (vixcentral.com)

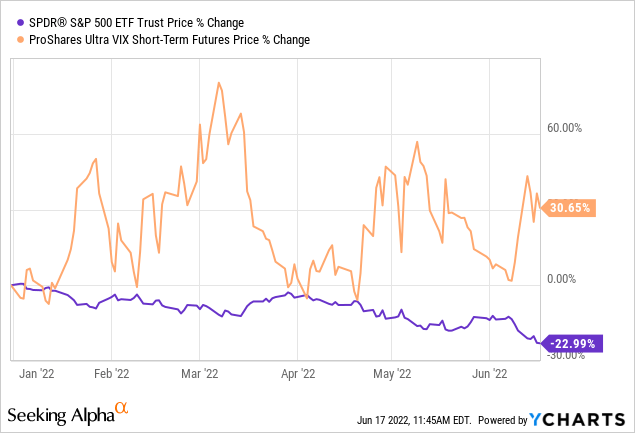

Unsurprisingly, funds such as UVXY have benefited in the near term from a combination of lower short-term futures prices and heightened market fears. As of mid-June, UVXY was up more than 30% YTD while the S&P 500 was down nearly 23%.

Figure 2: SPY vs. UVXY

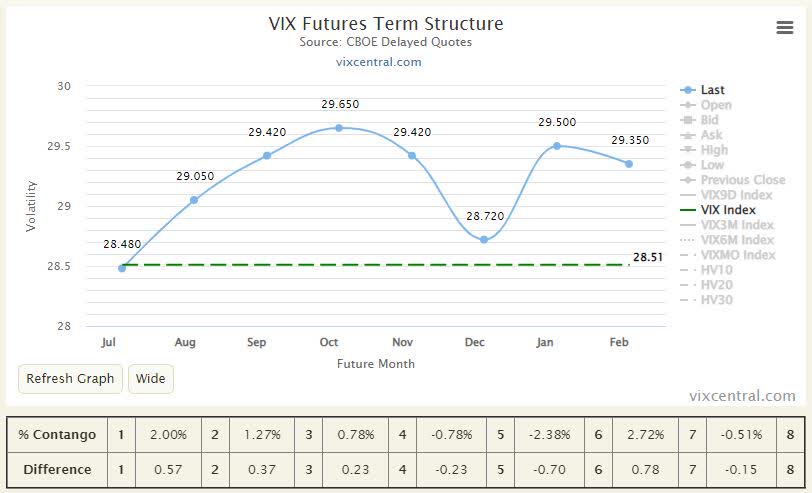

However, as the VIX futures curve returns to its normal contango structure, it’s going to become more costly for ProShares to roll its futures contracts. As you can see in the image below from late June, futures are becoming more expensive compared to earlier in the month (figure 1)

Figure 3: Vix Futures Term Structure (June 30th)

VIX Term Structure (vixcentral.com)

While UVXY has declined about 17% since mid-June, I believe there is a lot more room to fall (as it has historically). In my opinion, investors should continue to use caution when deciding if they should take a long position or purchase call options in UVXY, even if it is just a short-term trade. It may be tempting in this challenging market where every sector and stock seems to be down while volatility surges. Once the tide turns and the VIX curve returns to contango as it has in the past, UVXY should continue falling. However, that doesn’t mean betting against UVXY is a sure thing as I’ll explain next.

Challenges Of Betting Against UVXY

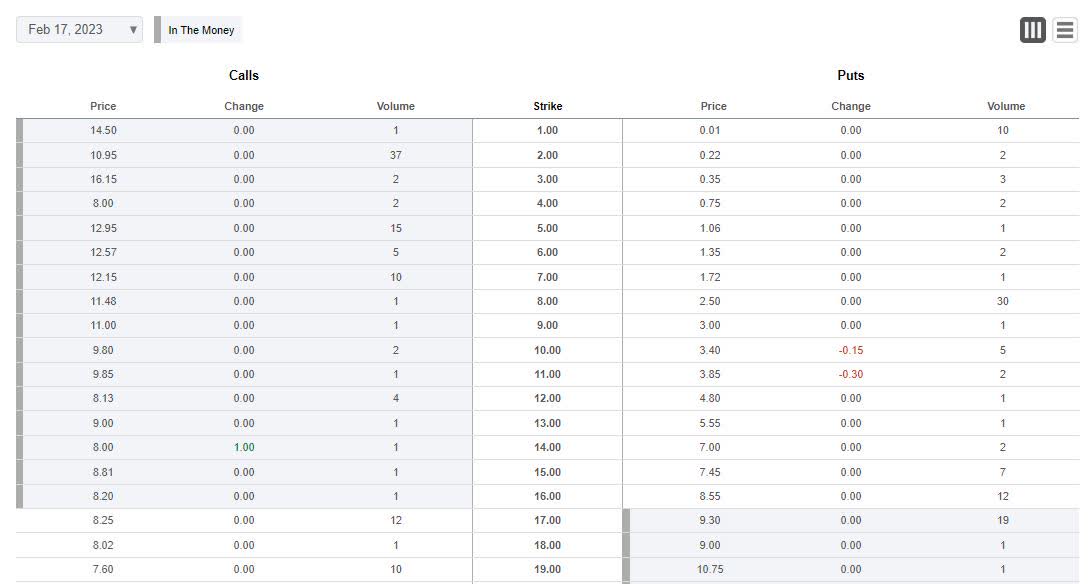

Since markets are aware that the VIX term structure will likely return to its normal contango pattern eventually, it prices that into options markets. While it may seem straightforward to just purchase put options and wait it out for a year, markets already price that in. For example, to purchase a $10 strike put option for the February 17th, 2023, expiry, it will cost $3.40 (as of June 15th). With a breakeven price of $6.60, UVXY would need to fall by more than 57% before expiration to make a profit.

Figure 4: UVXY Option Chain

Seeking Alpha

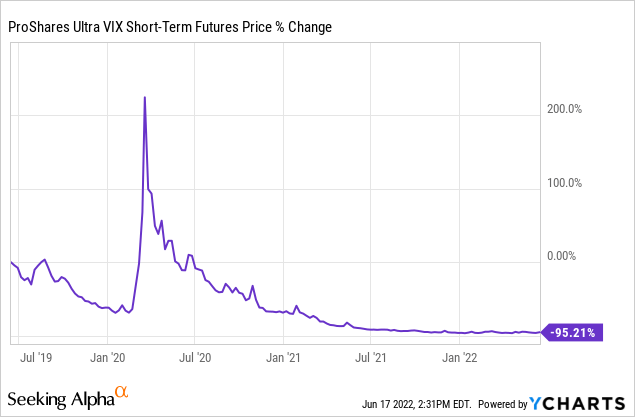

Historically speaking, purchasing long-dated put options of UVXY, while expensive, can offer a favorable return for patient investors if equities return to a bull market. Timing can always be a problem though. No one can predict the future, and if there is a black swan at or around expiration, an investor could see their option become worthless. It’s a risky investment strategy. The three-year chart shows how a put option can become worthless if an investor purchased one with an expiration around March 2020.

Figure 5: UVXY 3-Year Performance

However, as you can see in Figure 5, UVXY has underperformed tremendously in the long run, and that’s due to the design of the fund. Even in the prospectus, ProShares states that this vehicle should not be used as a long-term investment. Rather, it should primarily be used by institutional investors as a hedging vehicle.

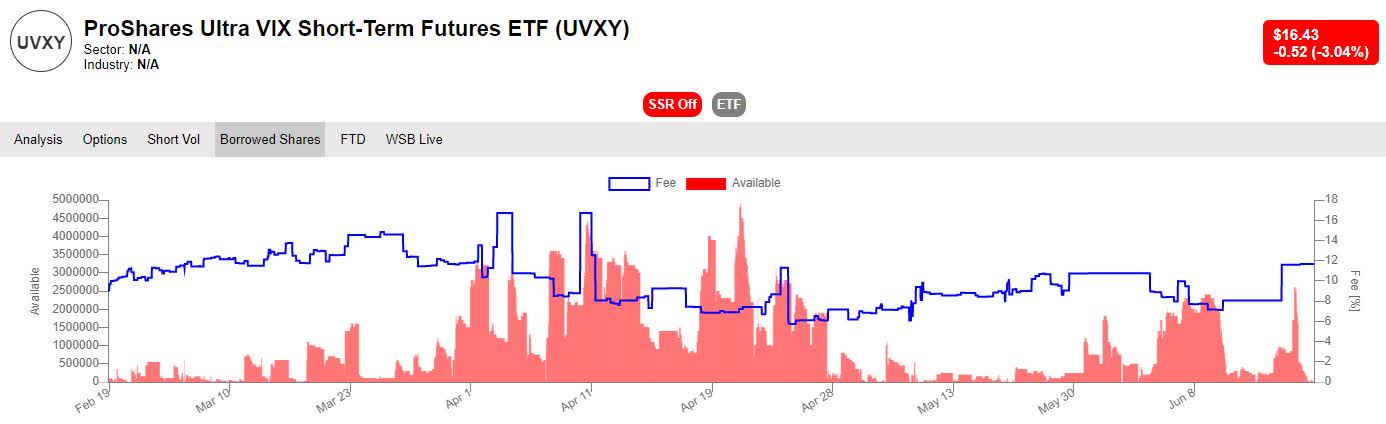

If an investor would rather initiate a short position, it can do so at a relatively cheap rate. However, there is a significant risk that if the VIX spikes due to another unforeseen event, a short position would require additional collateral or it would be closed out.

Figure 6: UVXY Borrowing Fees

Stocksera

Borrowing costs to initiate a short position typically range anywhere between 2% and 12% on an annualized basis depending on the supply and demand for UVXY. While this is much cheaper than buying put options, there is a risk that an investor would need to post additional collateral if UVXY surges due to the VIX increasing. This has happened before, and investors should not think it won’t happen again.

Conclusion

For a speculative investor, going short or purchasing a long-dated put option could be an interesting play (in theory). However, the costs associated with betting against UVXY are significantly high, and investors who go short UVXY should understand the risks, whether it be a high upfront cost for a put option or the risk of getting margin called on a short position. In my opinion, I think UVXY has become overvalued in the near term primarily due to the VIX futures curve being in backwardation, and I expect over the next 6 months to 1 year it will return back to its normal structure. Once that occurs, UVXY could plummet to new all-time lows as it has in the past.

Be the first to comment