In this article, we’ll do two things. First, we are going to discuss what the global transition towards “net-zero” technologies means for material demand. Especially copper demand will accelerate for decades to come, causing a massive supply/demand imbalance, given slow supply growth. Second, I will give you a stock that I believe will be one of the biggest winners of the move toward a low-carbon future. That company isn’t an electric car company, nor is it a high-tech company. As the title already gave away, it is Caterpillar (NYSE:CAT), the heavy machinery producer from Deerfield, Illinois. I thought about it for weeks, and I’m very serious about this investment as I believe that this “good old” machinery giant and dividend aristocrat is one of the best ways to protect investors against what could be an ugly side effect of the global search for low-emission technologies.

So, let’s dive into the details.

Net-Zero & Material Demand

One thing I’m increasingly incorporating here on Seeking Alpha is the combination of macro research and a fitting actionable idea. My background has obviously something to do with it, but I believe that a clear macro vision is the single most important thing before investing in anything.

Hence, in this article, we will discuss one of the most important trends in global macro. A secular trend that will impact our economies for decades to come: looming material shortages.

As most know, the Paris Agreement aims to get most countries to become climate neutral by 2050. Personally, I think a lot of this discussion is nonsense and not feasible for reasons we’re experiencing right now. Energy is seeing a huge supply/demand imbalance, and the European energy crisis is made worse by governments’ inability (or unwillingness) to boost domestic fossil fuel production.

Anyway, my opinion doesn’t matter as we need to acknowledge the facts that the push for net zero is happening. According to the IEA (International Energy Agency), we will likely see close to 55 million electric cars on the roads in 2030. That’s 18x higher compared to 2020. This will come with close to 1,000 GW of solar and wind capacity additions, up four-fold compared to 2020. Meanwhile, the energy intensity of GDP is expected to decline by 4% per year.

Think about that for a second. Not only is it increasingly hard to achieve economic growth, but now “we” need to come up with further increasing efficiencies to avoid missing 2050 targets. That’s a tough nut to crack, to put it mildly.

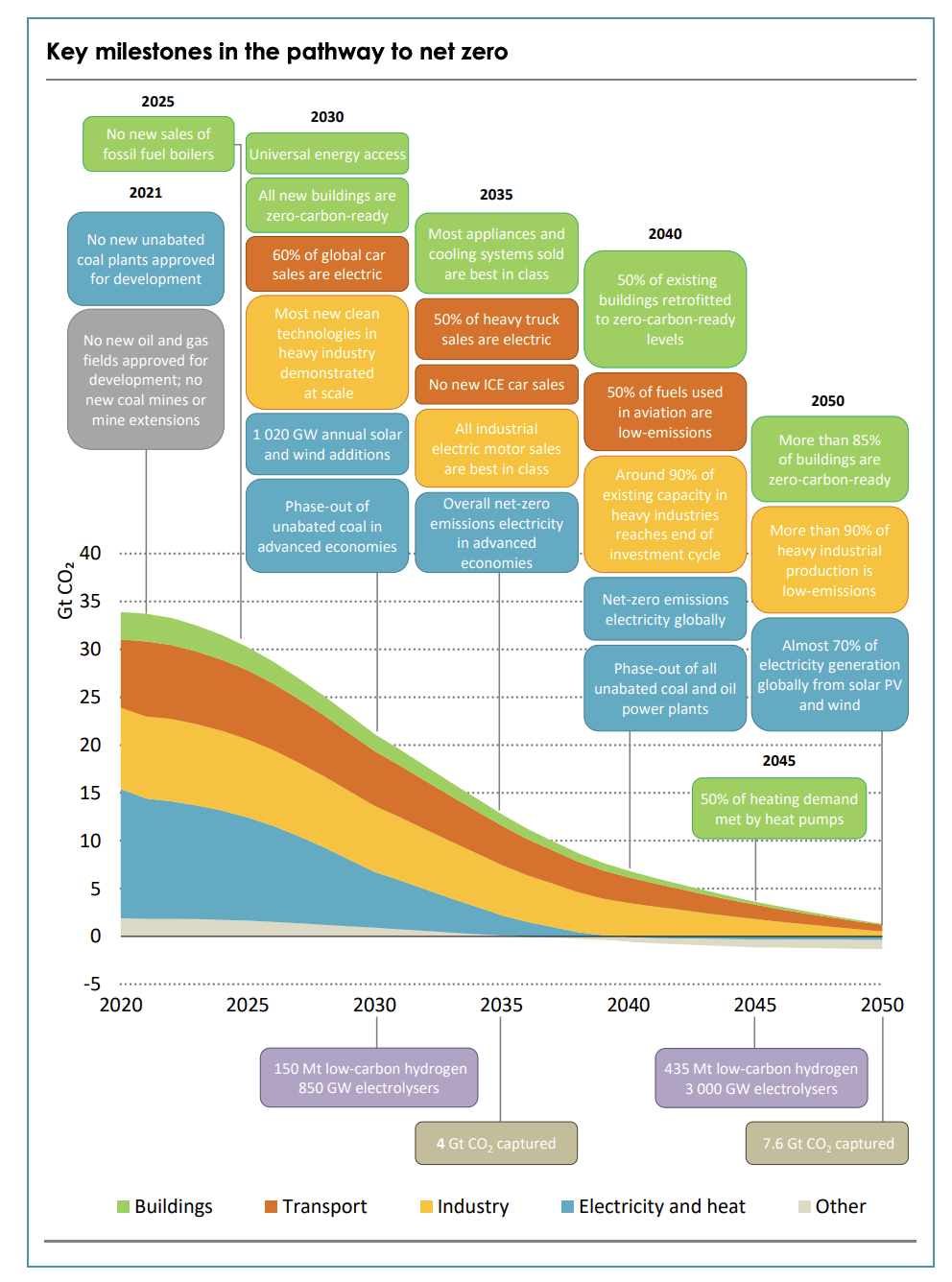

Thanks to the IEA, we have a handy overview of how this is expected to be achieved. Essentially, what we’re looking at is a massive push for EV mobility. This includes passenger cars, heavy trucks, and pretty much everything on wheels. Moreover, electricity production is expected to be net-zero early in the process, which means demand for solar, wind, and related will explode as we already briefly discussed.

IEA

By 2050, for example, close to 50% of global electricity is expected to be generated by wind and solar. Unless we have built a network of reliable storage, I don’t think we will get a number even remotely close to that.

Anyway, as my opinion is secondary, a trend towards net zero will mean one thing for sure: accelerating demand for materials. Batteries, solar panels, wind turbines, vehicles, and efficient buildings, all require more materials. Hence, by 2050, we’re looking at a situation where we need more than $400 billion worth of critical metals in order to replace coal.

IEA

It is important to mention that we’re replacing a very affordable and abundant energy source like coal with applications that require expensive amounts of miners that come with new geopolitical risks (China dominates the processing of almost all of these materials) and expenses as these metals are everything but abundant.

As I said, I’m not against clean energy. I just hope that politicians and NGOs know what it means to replace coal within 30 years.

As the graph above shows, copper will be the most dominant critical mineral. Hence, I will focus on that and use it a bit as a proxy for the other materials as well.

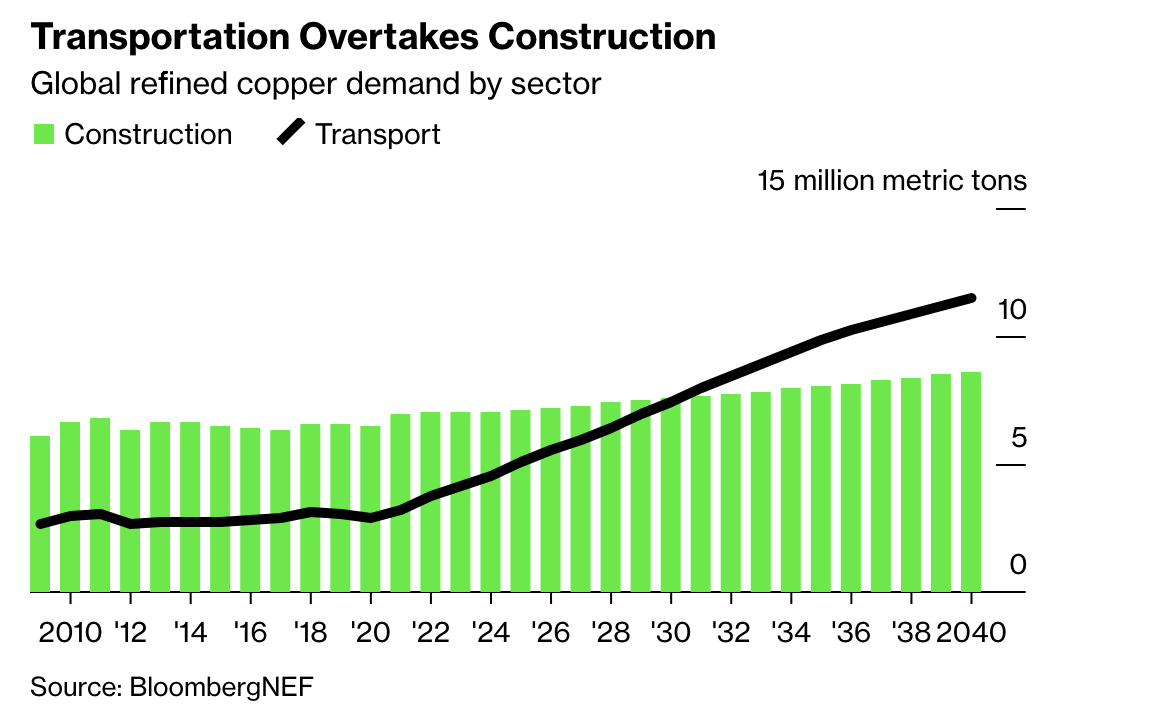

With that in mind, let me show you a few statistics. Between 2021 and 2040, annual copper demand is expected to expand by 53% to almost 40 million metric tons. This is driven by the electrification of transport and infrastructure – that’s the backbone of net zero.

Bloomberg

So far, copper was mainly known for its use in construction (wiring and related). However, in 2020, a new trend emerged. Transportation will require a lot of copper. By 2030, transportation could use more copper than global construction.

Bloomberg

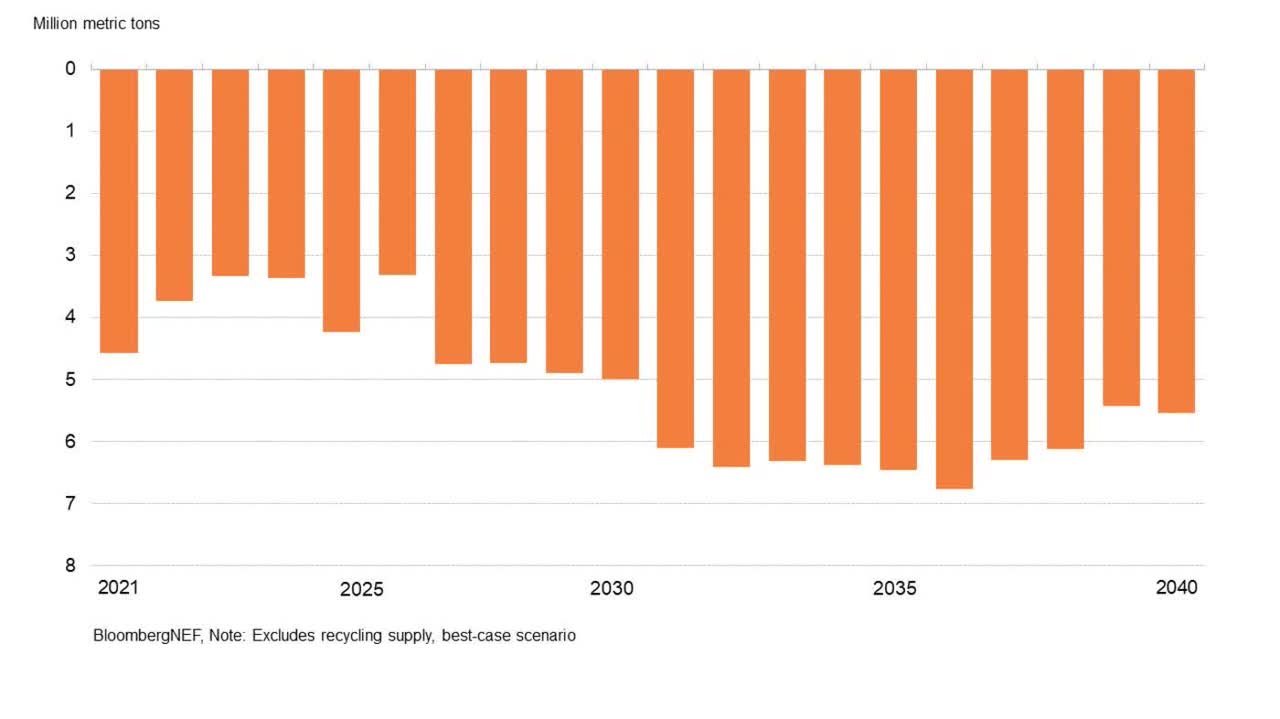

So far so good. The problem is that supply is expected to rise by 16% during the same period. This is expected to cause a shortfall of more than 5 million tons – in a best-case scenario.

Bloomberg

We need to be aware that this will almost certainly lead to higher prices. Eventually, that could improve supply as it becomes more attractive to open up new mines. However, the dominant trend of increasing deficits seems to be very hard to stop.

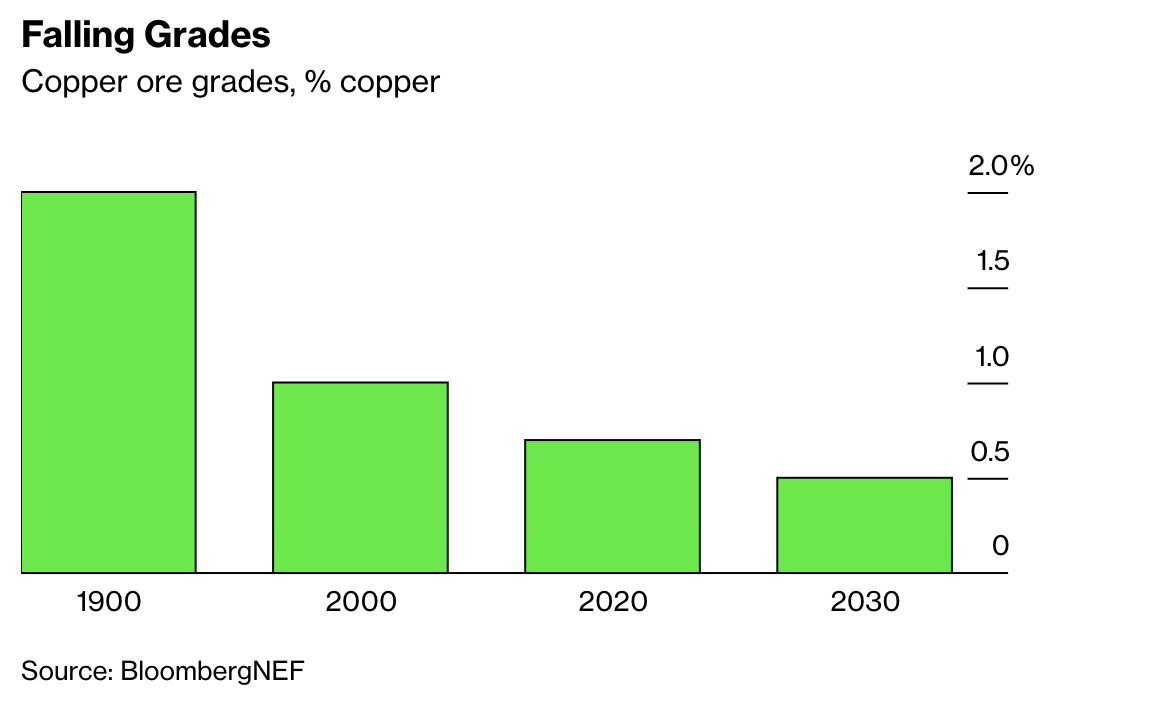

For example, there are no new copper discoveries to be expected over the next three years. It also doesn’t help that the quality of copper ore is falling. Miners expect to end up with 0.5% copper ores in 2030. That’s down from roughly 2.0% in the 1900s when the industrial revolution started to gain momentum.

Bloomberg

So far, everything discussed in this article is bullish for copper – very bullish. However, it does not mean that copper is going “to the moon”. While it will structurally support the price of copper, there will be a point where demand weakens due to high prices. That’s why I do not believe in global net-zero targets. On paper, it seems like a good idea. However, reality won’t be kind to these plans.

It also needs to be seen if, and how, governments will support new mining development. The same goes for recycling as we need to use existing copper given the deterioration of copper quality.

One “great” example of this is the electric Ford F-150. Ford (F) just hiked the price again for the second time in about two months. The cheapest version now costs about $52 thousand, which is up 30% from the original starting price of $40 thousand.

Given what we have discussed so far, it may not come as a surprise that the reason is higher material costs:

But Ford executives have said profits have evaporated on EVs as battery and other material costs have risen.

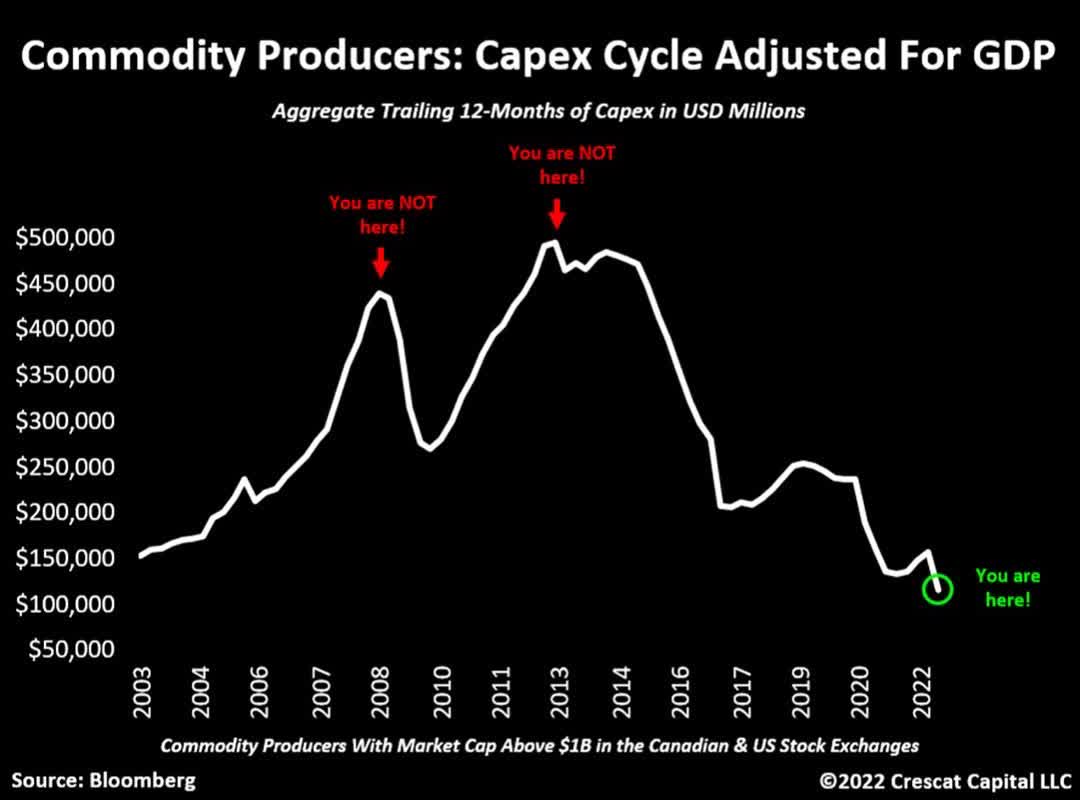

And to go back to the bigger picture, we’re dealing with sky-high underinvestment in commodities, in general. Comparing capital expenditures of commodity producers to GDP, we’re dealing with under investments not seen since the early 2000s as Crescat Capital tweeted the other day:

Crescat Capital, Bloomberg

Based on this context, here’s why I like Caterpillar so much.

CAT Stock Is The Ultimate Net-Zero Investment

I bought Caterpillar in the summer of 2020 when I decided to invest my money in long-term dividend (growth) stocks. The decision to buy CAT shares was based on its juicy yield after the pandemic sell-off, its characteristics as a dividend growth stock, and the basic fact that the company gave me exposure to global mining. As this means that CAT is well-protected against inflation, I wanted to own the company.

2020 was also the year “everyone” bought growth stocks. The money went into everything that looked like it could be part of new technology trends or the move toward net zero.

This includes electric car producers (even the small ones that may not survive), small battery startups, software developers, and companies that simply installed solar panels – among many other niches.

After thinking about this a lot, I have decided to use Caterpillar to benefit from global net zero.

This machinery giant from Deerfield, Illinois, with a market cap of $94.2 billion isn’t on people’s “environmental” radar. After all, building trucks that use up to 13 gallons of fuel per hour isn’t what makes people think of a carbon-neutral future.

However, that’s why I wrote the first half of this article. The energy transition will be all about materials and technologies. Hence, I looked for companies that benefit from this. We can buy mining companies as well. However, when it comes to long-term investing, I prefer the producers of equipment as this takes away a lot of mining risks. Most mining companies come with geopolitical risks and significant operating risks.

Caterpillar benefits from growth on a bigger scale without being exposed to these “smaller” risks. Caterpillar’s main risk is failing to deliver the required technologies, which comes with competition risk.

With that said, Caterpillar dominates global industries related to the EV transition. In 2021, the company did $51 billion in sales. $22 billion came from construction industries, which is expected to benefit from 100% growth in residential construction spending between now and 2040, 100% growth in “traditional” infrastructure, and more than 200% growth in energy transition infrastructure – again, a big winner of new infrastructure requirements.

Resource industries and energy & transportation accounted for $30 billion in sales. In these segments (especially in resource industries), the company is prepared to deal with close to 15,000 kilotons of mineral demand by 2040. Up from 7,000 kilotons in 2020.

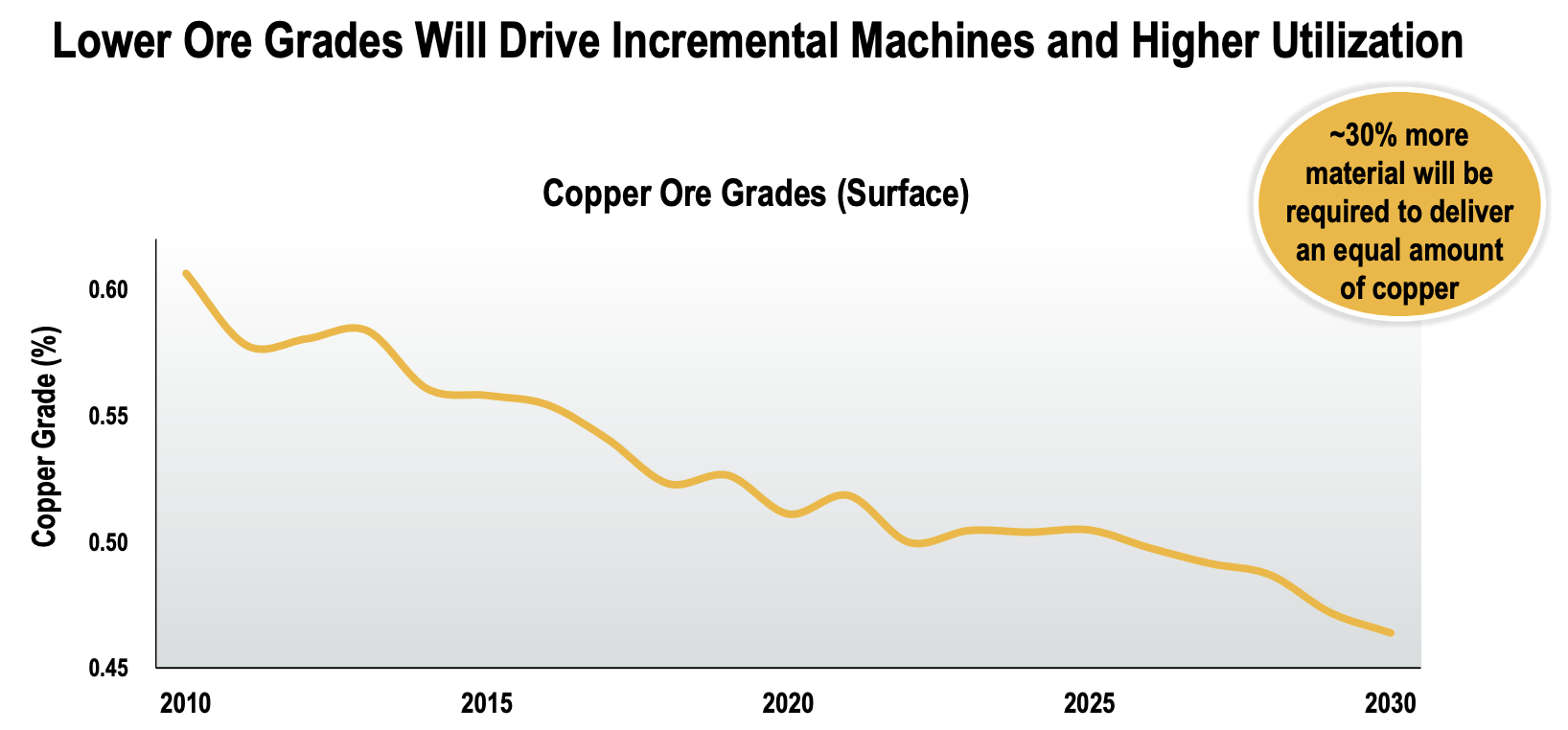

Moreover, in light of falling ore qualities, the company put a number on what this means for the required machinery. With copper ore quality falling to less than 0.50% by 2030, 30% more material will be needed to maintain a steady copper supply. Imagine what this means for equipment and maintenance.

Caterpillar

If we assume that mining CapEx is going to accelerate, we could see a move similar to the early 2000s.

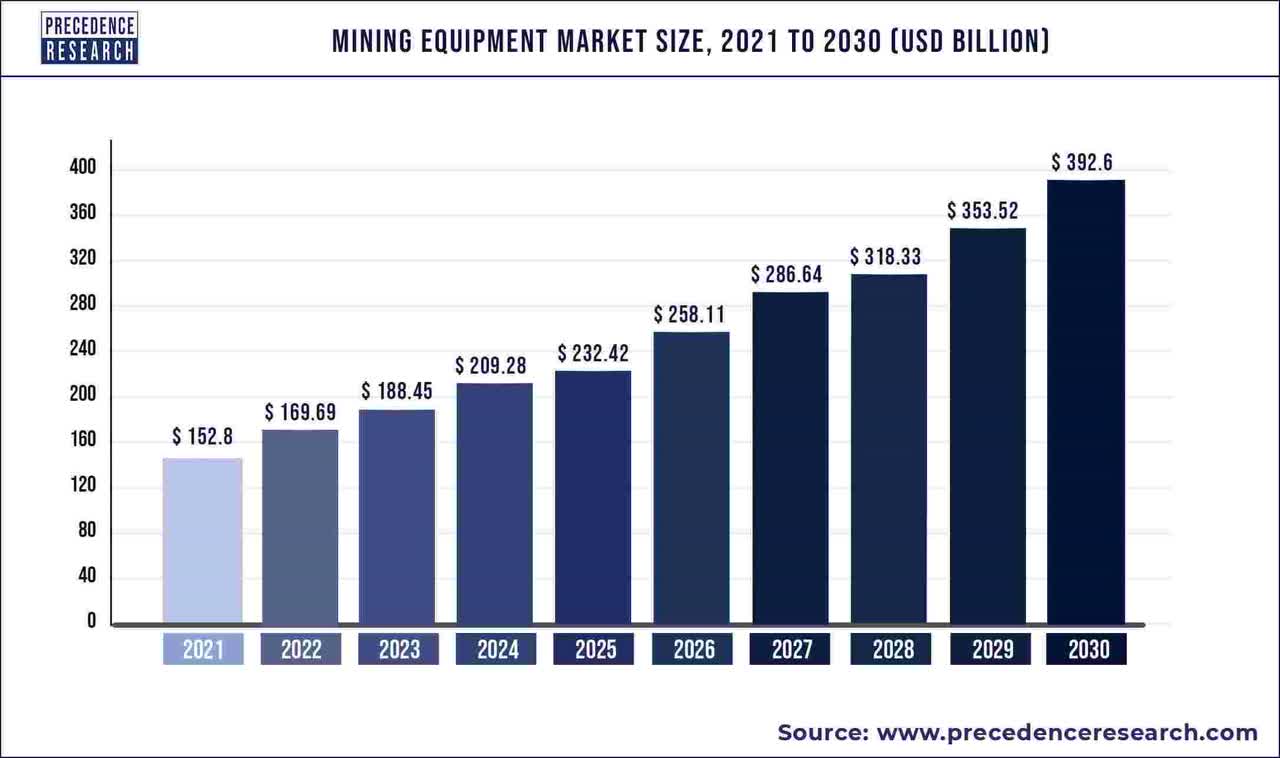

According to research conducted in 2021, the global mining equipment market share could reach $393 billion in 2030. That’s up from $153 billion in 2021. That’s 9.9% annual compounding growth.

Precedence Research

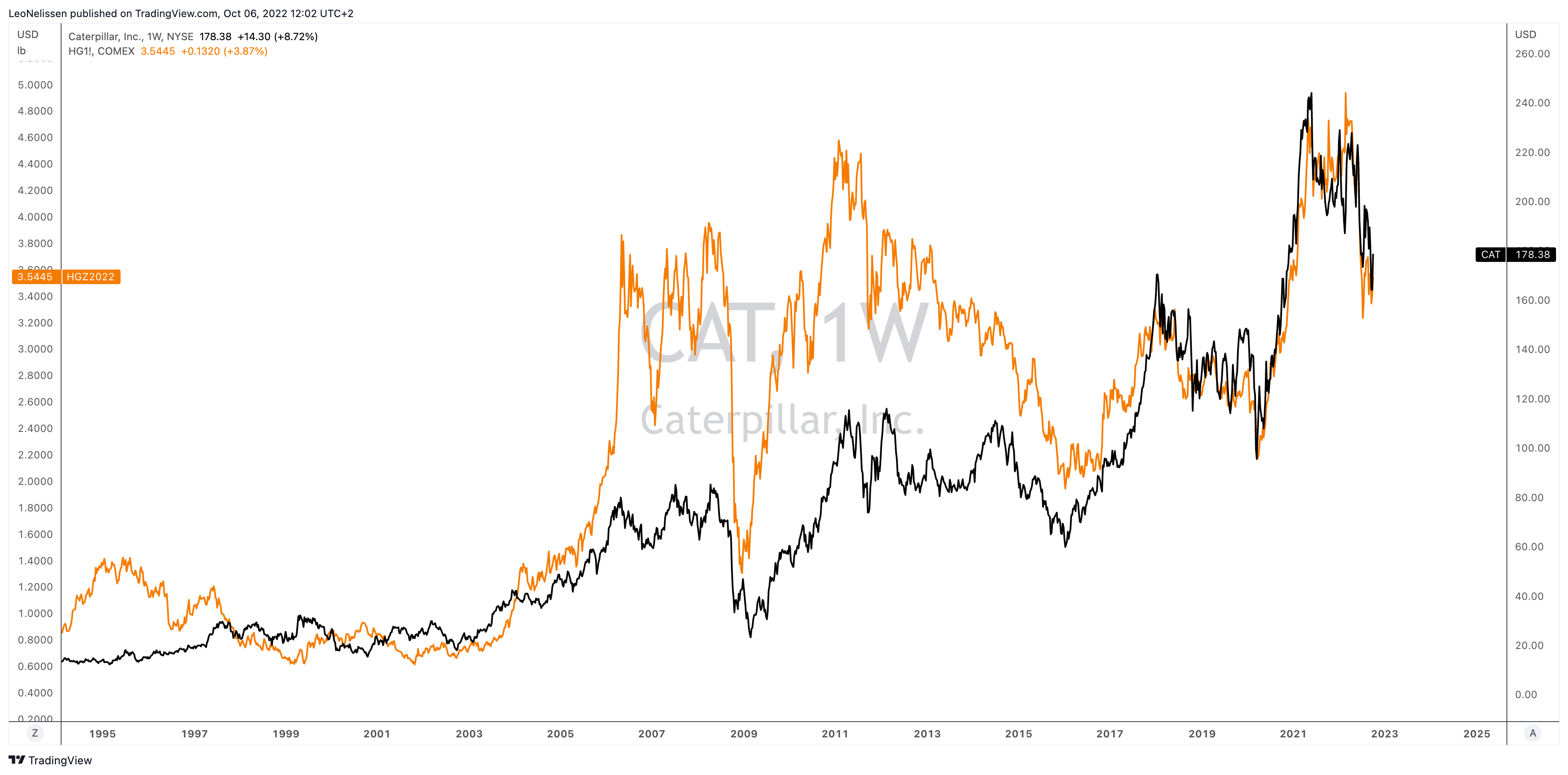

The TradingView chart below (the one below the Seeking Alpha dividend scorecard) displays at least two things. First of all, it shows that Caterpillar is essentially a proxy for the price of copper. However, it’s a value-adding proxy as Caterpillar buys back shares and improves its business with the profits it generates. Hence, while it is dependent on the direction of the copper price, it does outperform on a long-term basis.

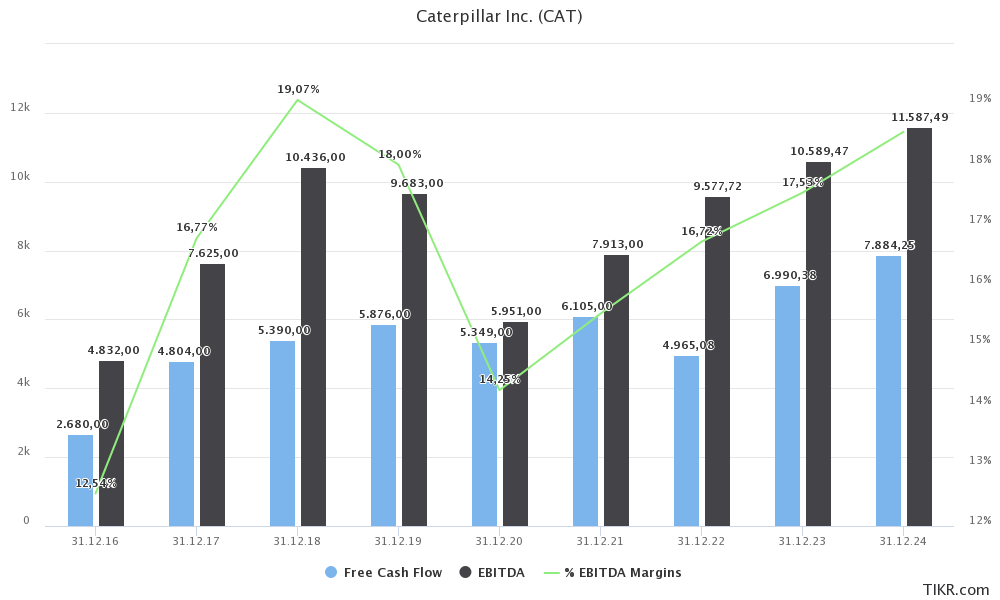

In 2016, for example, the company recovered from the 2014/2015 commodity crash, which pressured EBITDA and margins. However, even back then, the company did close to $2.7 billion in free cash flow. That number is now expected to rise to almost $8.0 billion in 2024, with EBITDA margins rising towards 19%. This implies a free cash flow yield of more than 8.0%.

TIKR.com

This will provide more room to continue high dividend growth and outperformance as I discussed in this article. The quote below summarizes it a bit:

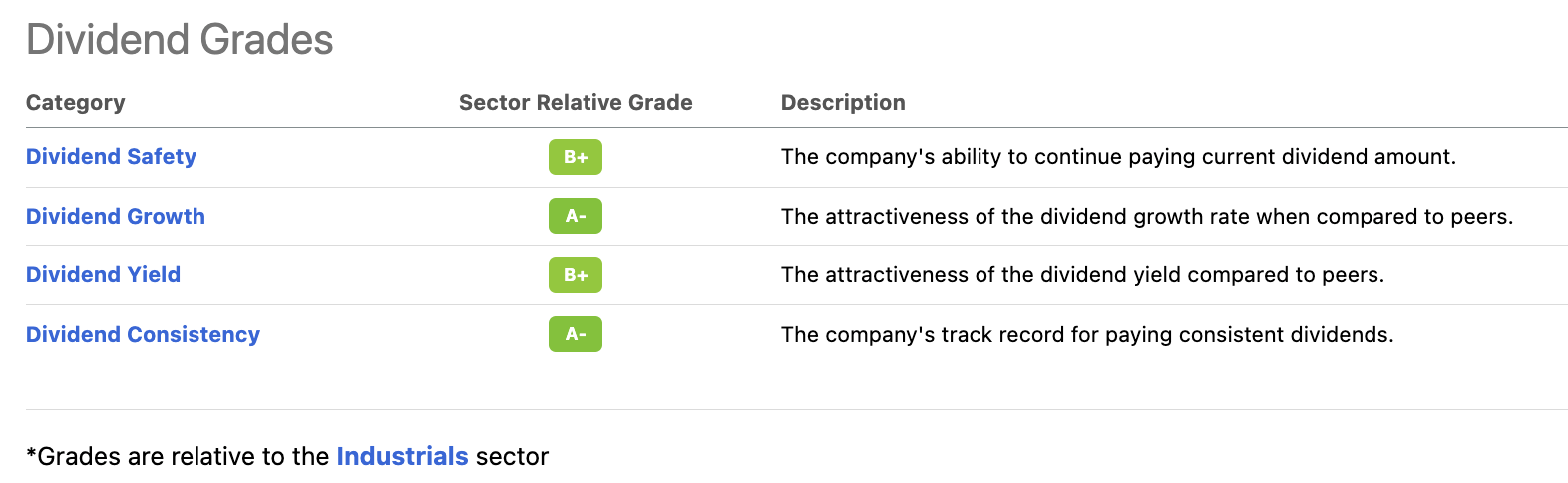

When it comes to dividends, Caterpillar has one of the best Seeking Alpha scorecards I’ve seen in a long time. It scores high on everything, especially dividend growth, and consistency.

Seeking Alpha

On June 8, Caterpillar hiked its dividend by 8.1% to $1.20 per share. This implies a 2.8% dividend yield. The 10-year average annual dividend growth rate is 9.2%, which is more than decent for a stock that is as mature and cyclical as Caterpillar. Also, 9% per year on a current yield of 2.8% is a big deal that quickly turns 2.8% into a yield on cost that even high-yield-seeking investors will appreciate.

The second thing is that Caterpillar returned more than 400% between early 2000 and 2006. This move was supported by rapid growth in China, a weaker dollar, and tailwinds in pretty much all of its end markets.

TradingView (Black = CAT, Orange = COMEX Copper)

Right now, China isn’t the growth engine it was 20 years ago. However, now we have net zero as a growth engine.

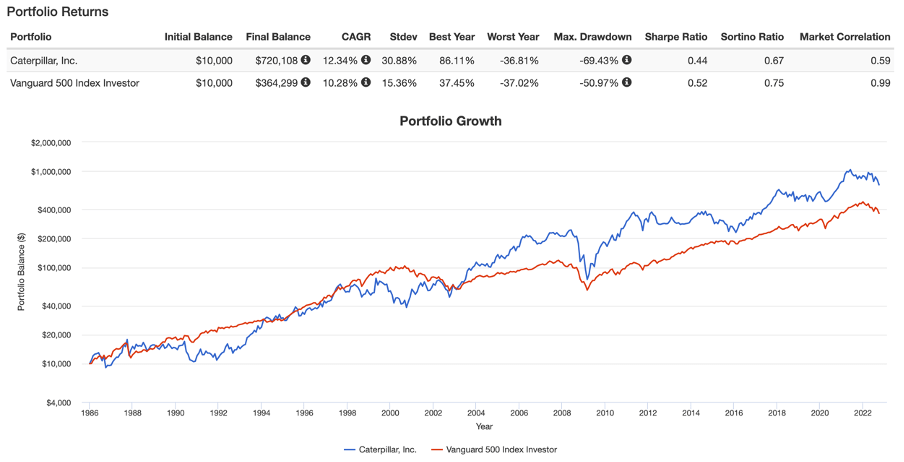

Moreover, despite its cyclical behavior, Caterpillar gains more during bull markets than it loses during bear markets – a lot more. Since 1985, Caterpillar has returned 12.7% per year, turning $10,000 into more than $720,000. This beats the S&P 500 by more than 200 basis points per year. The issue is that this comes with a 30.9% standard deviation, which is double the standard deviation of the S&P 500.

Portfolio Visualizer

So, what about the valuation?

Valuation

Caterpillar is down 13.7% year to date. The company has lost a quarter of its value from its 2021 all-time high.

While the company is outperforming the S&P 500 this year, there is no denying that the stock is suffering from an ugly mix of slow economic growth, high inflation, and the Fed’s dedication to fighting inflation despite the aforementioned economic slowing trend.

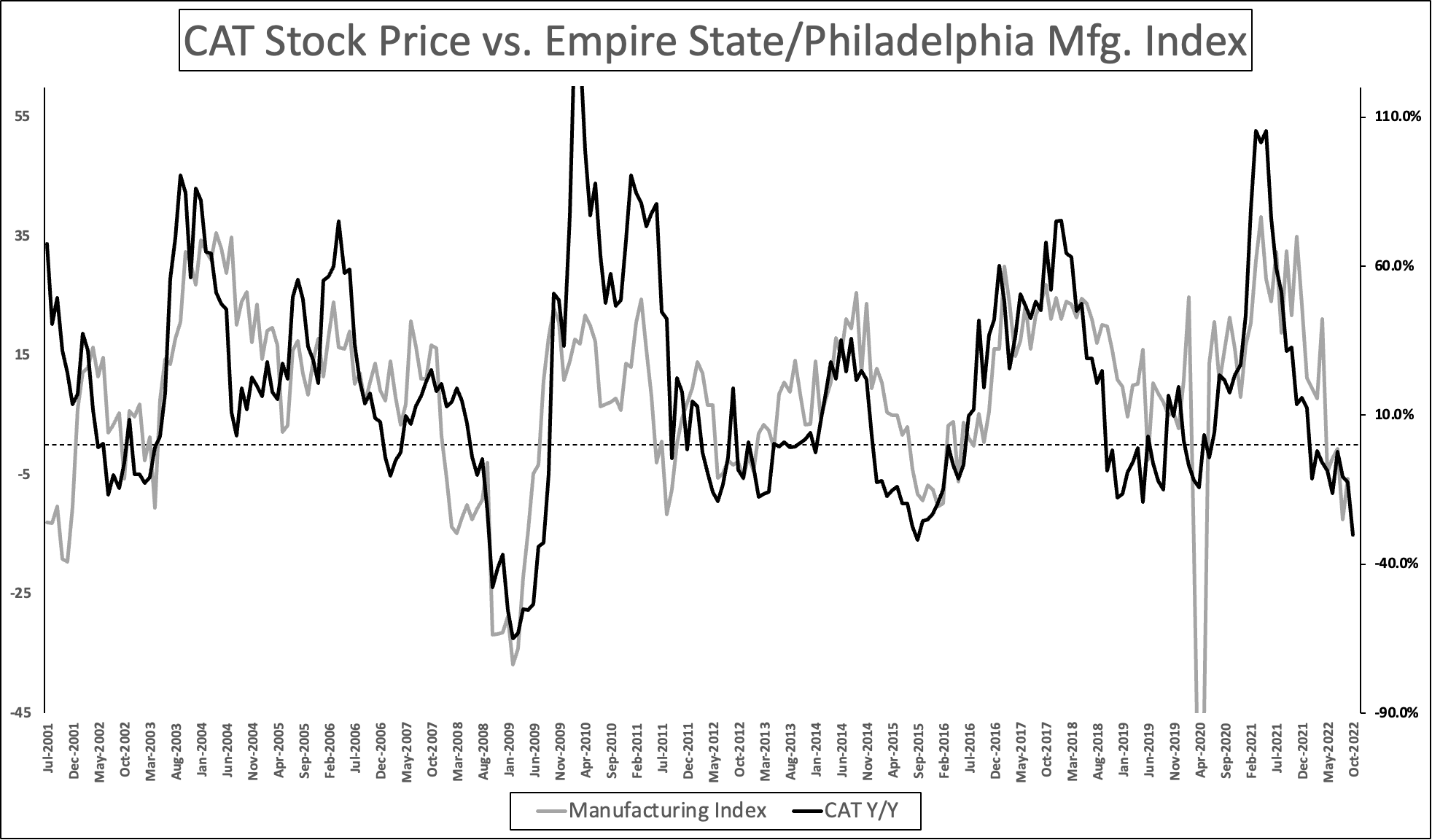

I discussed this in a detailed article at the end of last month. The graph below shows that economic growth is indeed weakening. Manufacturing surveys pointing at high contraction risks, comparable (yet different) to the period in 2015. The good news is that the Caterpillar stock price has priced in a lot of weakness. This helps the valuation a lot.

Author

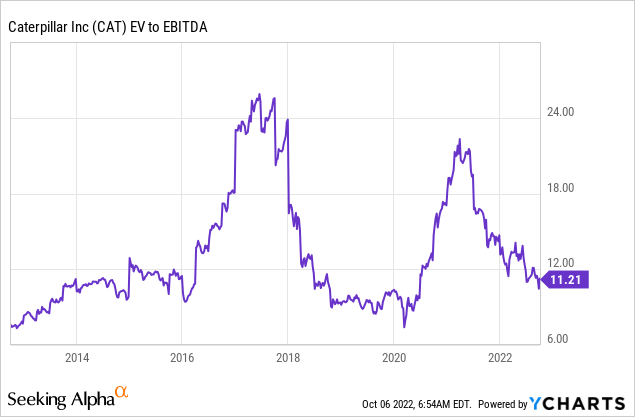

The company is currently trading at 11.9x 2023E EBITDA of $10.6 billion. That’s based on its $126.4 billion enterprise value, consisting of its $94.2 billion market cap, $27.0 billion in net debt, and $5.2 billion in pension-related liabilities.

This valuation is very fair, especially given the implied free cash flow yield of almost 8%. It means investors are not overpaying to get access to free cash flow.

Caterpillar has become one of my favorite investments. While the current sell-off isn’t so much fun, we are being offered new opportunities to buy cyclical companies at attractive prices.

In this case, Caterpillar is becoming more than just a company that does well when economic expectations rise. I believe that this machinery company is turning into one of the best ways to play the long-term trend toward net zero.

Caterpillar delivers top-tier infrastructure and resource supplies, which are needed to produce the materials required for new energy technologies.

Very ambitious environmental goals are about to meet rapidly rising material shortages, which are set to cause commodity prices to explode in the decades ahead. This requires higher spending on mining operations and energy infrastructure. Investments have hit multi-decade lows at a time when demand is accelerating. It’s a worst-case scenario for supporters of the energy transition as it is set to maintain high material inflation.

I expect mining CapEx and infrastructure spending to accelerate for decades to come, providing a similar bull case for CAT compared to the early 2000s.

My plan is to use the current stock price weakness to add more aggressively to CAT in the months ahead.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment