Andres Victorero/iStock via Getty Images

There isn’t a weekday that goes by where I don’t see an article boldly suggesting REITs (VNQ) are the best way for retirees to invest their hard earned nest eggs. Many, but certainly not all, articles go onto suggest that REITs are SWAN like (sleep well at night) instruments that are well suited for retirees. The subtext of the articles suggest that somehow a select few High Priests of finance, have found this magic elixir, in the form of well curated REITs, and they are willing to share these secrets, with retirees, on how they can consistently generate superior risk adjusted and low volatility returns.

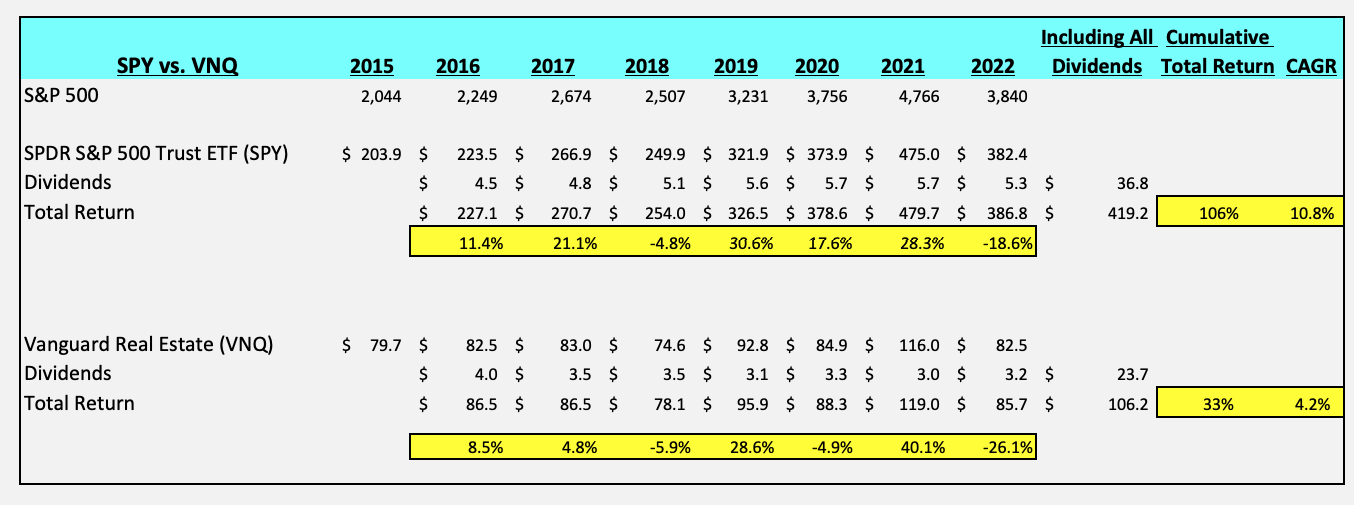

Lo and behold, and using the Vanguard Real Estate Index Fund (VNQ) as my proxy, for REITs, given the large AUM, strong liquidity, and underlying strong companies held within this fund, enclosed below, I compared the S&P 500 (SPY) to VNQ, from calendar year 2016 to 2022.

Author’s Chart

In the above chart, please note that it compares the SPY vs. VNQ, on a total return basis, for full year calendar years of 2016-2022. So inclusive of dividends, the total returns of the SPY index, over that seven year stretch, was 106%, which translates to a very respectable 10.8% CAGR. The VNQ total return was only 33%, which only translates to a 4.2% CAGR.

If you look at the chart, on a total return basis, the S&P 500 beat the VNQ index, five out of the seven years.

And again, on an overall basis, the S&P 500 dramatically beat REITs, using VNQ as our proxy.

What is even more puzzling is reading REIT articles telling retirees to buy security REIT ‘XYZ Hand Over Fist’ or how to become a ‘Millionaire’ by buying this basket of REITs. Shockingly, if you actually look at the empirical data, no one has gotten rich, investing in REITs. At least no one has gotten rich, in a Buy and Hold REIT strategy, over the past seven years. And I would argue seven years is a long enough period of time, for the 8th wonder of the world – the power of compounding – to work its magic.

So I’m kind of scratching my head and wondering why REITs are so wildly popular amongst retirees?

Don’t retirees look at empirical data before allocating their nest eggs?

Why is this very narrow and niche asset class purported perfectly suited for retirees, folks that are specifically looking for Buy-and-Hold and SWAN like financial assets (so think either bonds or equities)?

Moreover, why do I see freshly minted article after article, on what seems like nearly a daily basis, telling retirees to buy this new REIT or that new REIT?

In the same articles, retirees are told they should be out and about enjoying their golden retirement years. Activities like spending quality time with grandchildren, traveling, pursuing a hobby, volunteering, going back to school to quench a person’s intellectual curiosity. Or perhaps, playing Pickleball or Golf or engaging in some other fun social activity.

When will retirees find the time to read all of these new articles? Aren’t they supposed to be enjoying life and too busy to worry about their nest eggs? I kind of thought the Buy and Hold REIT portfolio was perfectly curated and designed to be set it and forget it.

There Are No Do-Overs In Retirement

For the vast majority of people, once they retire, that is it. Unless a person is absolutely gifted, a true expert in their field, or has a highly unique skillset, in an industry chronically undersupplied of human talent, when they retire, again, that is it. All they have is their nest egg (so think financial assets, real estate, net of debt), and social security. Unless a person is one of the lucky few, and that has some form of a pension. Generally speaking, though, for many companies, it is cheaper to hire young and energetic eager beavers, fresh out of school (college or trade school), looking to make their mark, because companies can pay a lot less and experience lower associated health care costs.

We can’t forget that there are also the issues of a person’s health, family situation, and other individual circumstances. And unfortunately, anecdotally, or on a personal level, all kinds of adversity can confront people, which is also a fact of life. Some people are luckier than others, and stay healthier, others do not.

For many people, and again circumstances vary widely, these are daunting obstacles and that is why people turn to financial advisors and financial planners. These folks are well compensated to construct bespoke solutions tailored to a person’s overall and unique situation. This includes understanding the full picture of their finances, family situation, and health.

Generally speaking, the more wealth you have, there is greater access to more talented or better advice (or perhaps these people are simply better asset gathers, it is debatable). That said, outcomes and experiences of retirees and their financial advisors and planners can vary widely.

My Criteria For Selecting A Good Steward

If I were asked for my criteria for selecting a good steward, my list would be very short:

- Make sure the advisor deeply understands your circumstances (financial resources, expenses, health situation, and risk tolerance).

- What kind of a documented track record does an advisor have for generating returns? Can they explain their process and explain how they achieved those superior risk adjusted returns (net of fees and expenses)?

- Are they intellectually honest?

- Do they have skin in the game?

Incidentally, switching gears a bit, just last week, the WSJ wrote a good profile piece: Here’s What Retirement With Less Than $1 Million Looks Like in America

Within the article, the WSJ cited this interesting statistic:

The typical family’s 401(k) and IRA-type accounts come to less than half that goal in the years approaching retirement age, according to the non-profit Employee Benefit Research Institute. Total household balances in retirement accounts for those 55 to 64 years old are $413,814 on average, according to its estimates based on 2019 data, the most recent available.

If the WSJ is using this statistic, as part of their reporting, I take it to be a fairly accurate yardstick.

Therefore, I’m perplexed, befuddled even, why the average retirement household is aggressively being pitched REITs, as the true pathway to making the quantum leap from $414K to millionaire status.

I just can’t get there on the math.

Putting It All Together

Today, I took the time to go through the actual data and create that simple comparison chart, capturing the S&P 500, represented by SPY, versus high quality REITs, represented by VNQ.

At least over the past seven calendar year stretch, from 2016-2022, the S&P 500 has dramatically outperformed REITs, using VNQ as our proxy.

For example, if your starting base of capital was $414K, the figure cited in the WSJ piece, it would have grown to over $850K with SPY over the seven year stretch from 2016-2022. With it invested in VNQ it would have only grown to $551K.

Notwithstanding the $300K IG SWAN portfolio that I curated, on behalf of my parents, aged 72 and 74, and shared on SA’s free site, the vast majority of my time is focused on small cap value and special situation stocks. However, I pride myself on being intellectually honest and forthright and we owe it to retirees to paint as realistic a picture as possible. At least for the vast majority of retirees, that $414k nest egg isn’t going to cross the rubicon of seven figures. Let’s keep it real. So going forward, if you are a retiree, that falls within the averages, please consider my easy four point check list. After all, this your retirement, and there are no ‘do overs’!

Be the first to comment