PM Images

As John D. Rockefeller once famously said:

The only thing that gives me pleasure is to see my dividends coming in.”

Now, most know that Rockefeller collected a lot of dividends in his life via his stock holdings in Standard Oil, in which he had a near-monopoly on the oil business in the U.S.

He lived to be 97 years old after turning his $4,000 investment (in a Cleveland refinery) into one of the largest fortunes in modern human history. At the time of his death in 1937, his net worth was equal to $340 billion after adjusting for inflation and taking into account relative GDP at the time.

For about 80 years, that inflation-adjusted net worth made Rockefeller by far the richest American of all time and the richest human in modern history. He was overtaken by Elon Musk on November 4, 2021.

So why are dividends so important?

Remember that dividends say a lot about a company and is one of the principal ways businesses communicate financial health and shareholder value. That’s because a dividend sends a clear message regarding the maturity of the company and its overall financial health.

After all, companies with the ability to distribute profits and increase the size of the dividend payments over time usually exhibit solid fundamentals. Importantly, companies that pay out dividends are serious about attracting investors and retaining their loyalty by rewarding them frequently.

That’s precisely why our team is laser-focused on dividends, because we recognize that dividend growth is the secret ingredient for achieving super total returns. Whenever a company has poor dividend policies, we generally avoid buying the shares.

For example, consider Gladstone Commercial Corporation (GOOD), a real estate investment trust, or REIT, that I have been negative on for quite some time.

Seeking Alpha

That article had over 200 comments, and many of them were from readers who disagreed with my bearish viewpoint:

Seeking Alpha

That’s right, I’ve been “playing the same song for 7 years,” suggesting that GOOD may cut its dividend…

Guess what?

Seeking Alpha

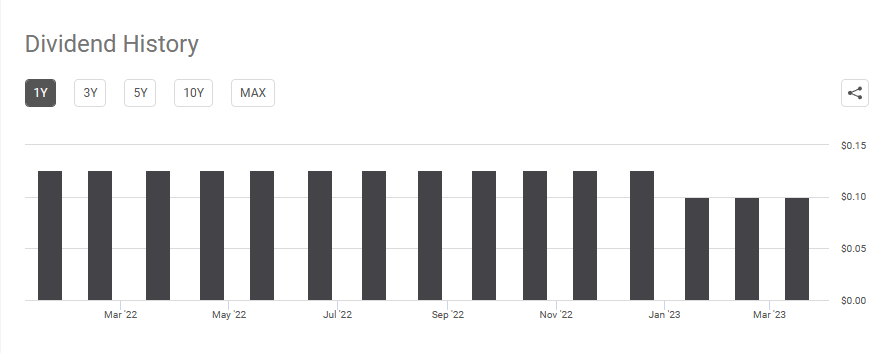

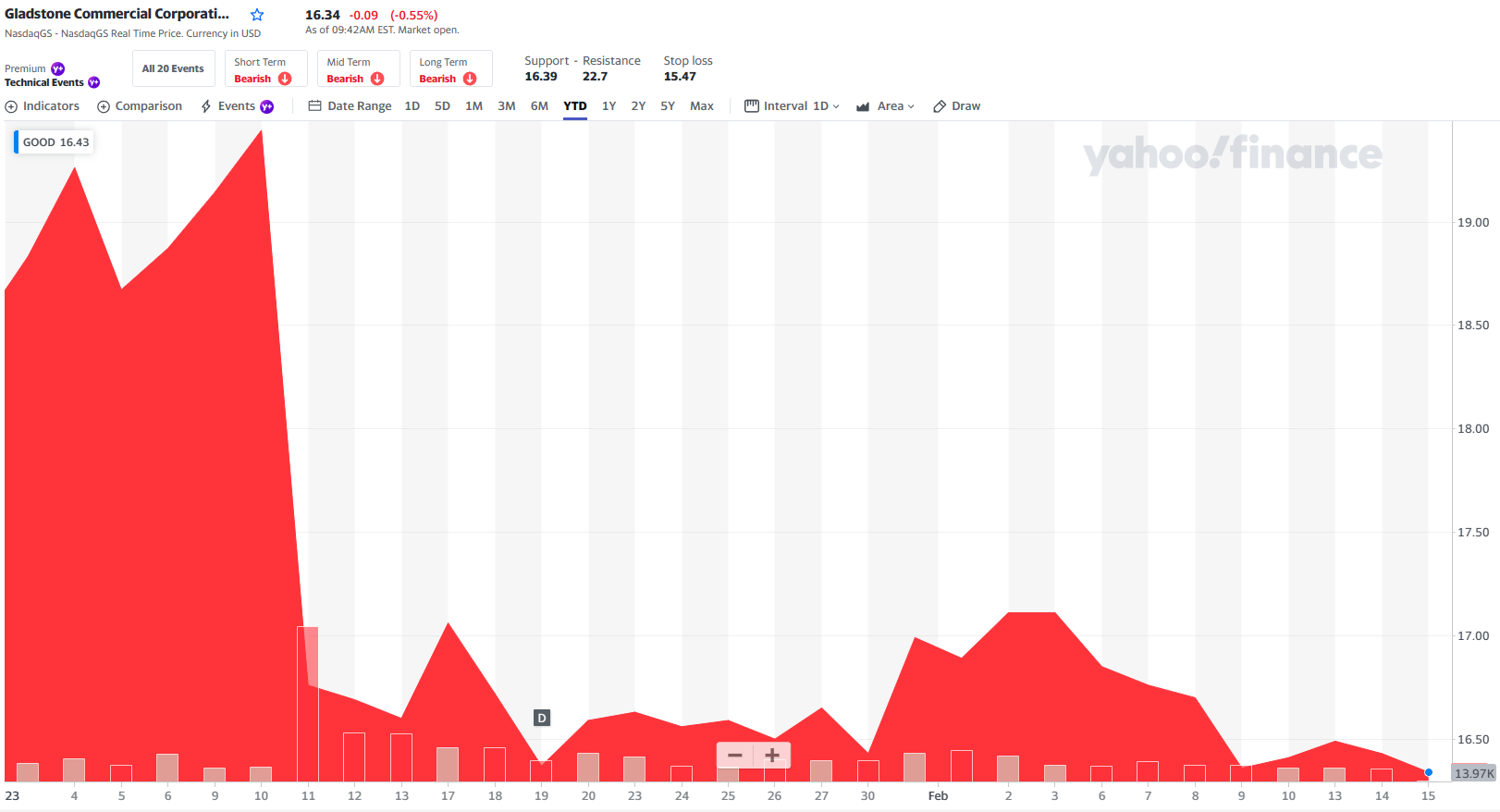

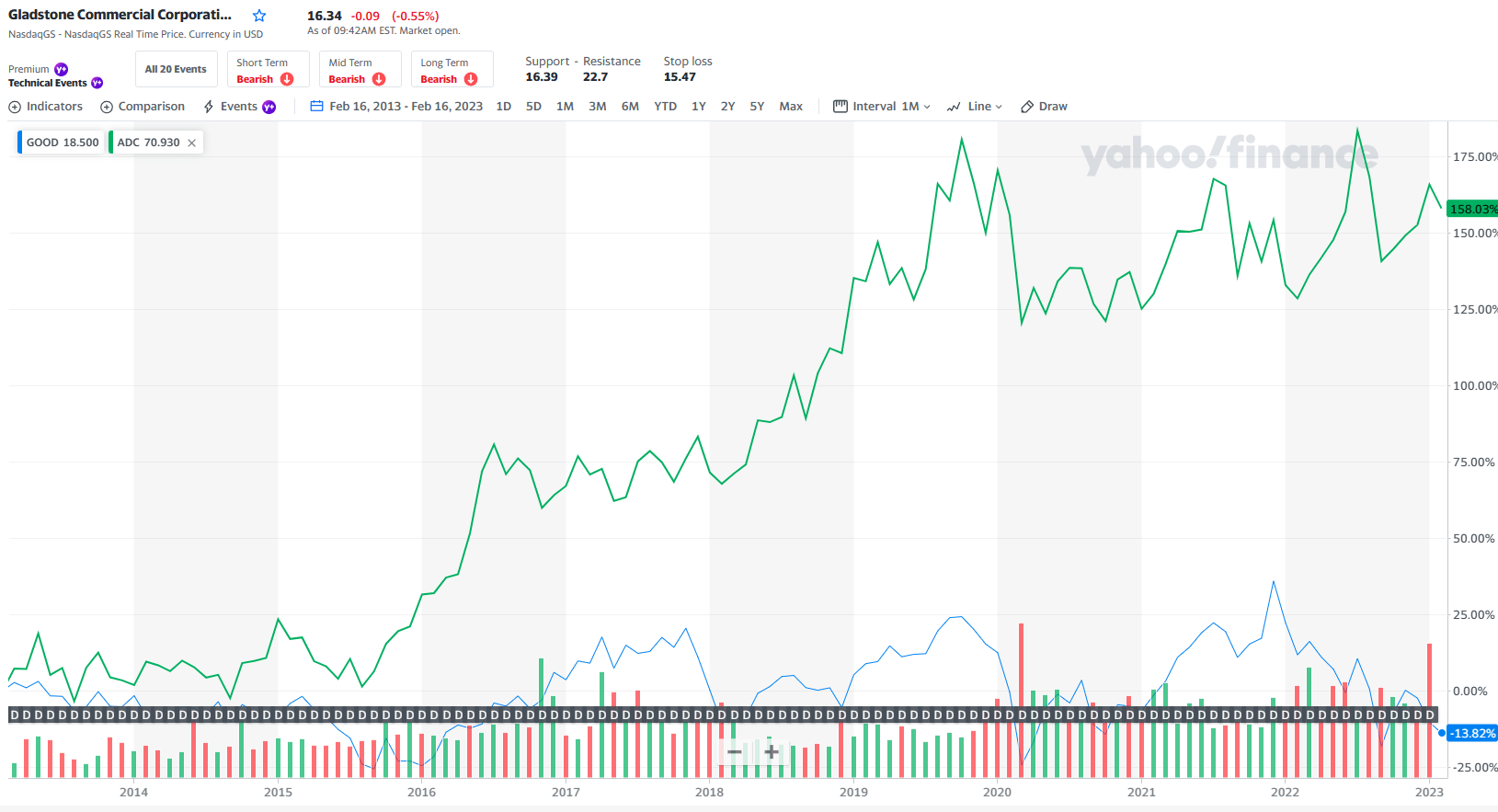

On January 10, 2023 GOOD cut its dividend by 20%, and Mr. Market reacted…

Yahoo Finance

But let’s look at GOOD over the last ten years and compare with a net lease REIT stalwart, Agree Realty Corporation (ADC):

Yahoo Finance

Get my point?

Dividend growth stocks are the ones to own, and you must always examine each prospective company closely to determine whether its dividend is growing, and if it’s not, always ask yourself why…

Okay, enough doom and gloom…and I hope you avoided buying GOOD…

Let’s focus on five of my top dividend growth REITs, and before we get started, please watch this video below:

Booyah Pick #1: VICI Properties Inc. (VICI)

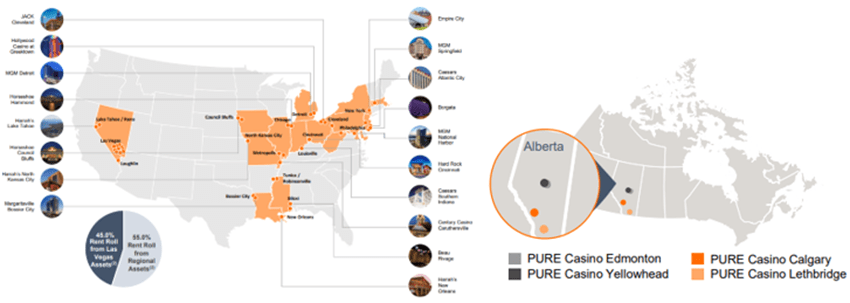

VICI Properties Inc. is a real estate investment trust in the gaming sector that specializes in hospitality and entertainment destinations. Their properties include Caesars Palace, MGM Grand and the Venetia Resort in Las Vegas, to name some of the more recognizable destinations.

While the bulk of their most well-known properties are in Las Vegas, they are well-diversified with a total of 49 gaming facilities in 15 states and Canada that cover roughly 124 million square feet and contain approximately 59,300 hotel rooms and around 450 bars and restaurants.

VICI – Investor Presentation

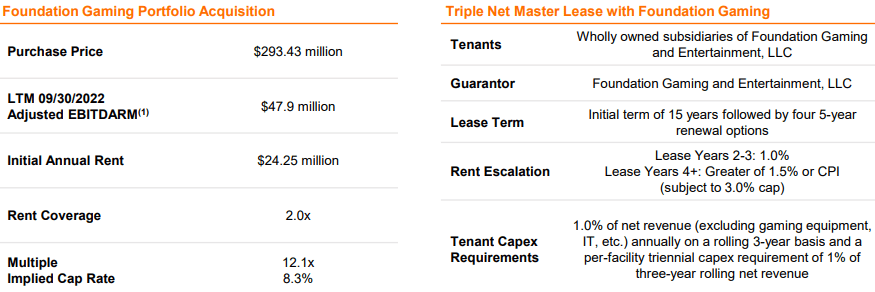

In December 2022, VICI entered into a sale / leaseback agreement with Foundation Gaming to acquire the Fitz Casino & Hotel and the WaterView Casino & Hotel for $293.43 million.

The triple net lease has an initial term of 15 years, with built-in rent escalation of 1.0% in years 2 and 3 and the greater of 1.5% or CPI after year 4 (capped at 3.0%).

The transaction was executed at an 8.3% cap rate with 2.0x initial rent coverage and is expected to be immediately accretive to AFFO per share. The acquisition expands VICI’s domestic presence into Vicksburg, Mississippi and makes Foundation Gaming VICI’s 10th tenant.

VICI – Transaction Overview

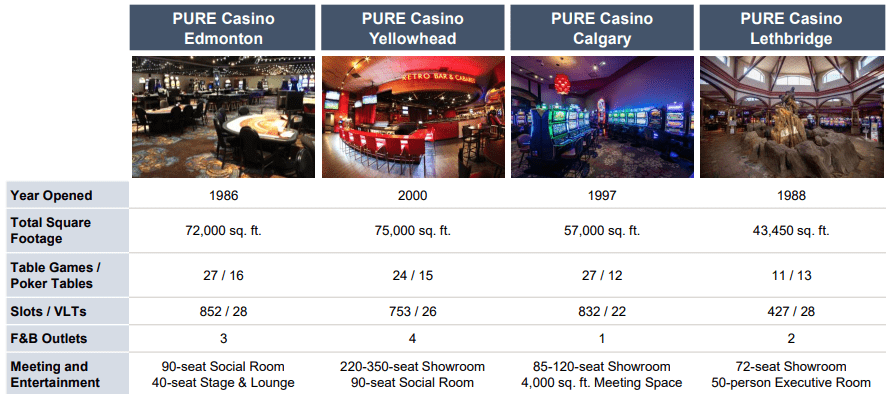

In January 2023, VICI branched out internationally with their $200.8 million dollar acquisition of 4 casino properties in Canada from PURE Canadian Gaming Corp (“PURE”).

VICI and PURE entered into a triple net master lease with an initial lease term of 25 years at an acquisition cap rate of 8.0% with 1.8x initial rent coverage. The lease provides for annual rent escalation of 1.25% in years 2 and 3 and then 1.5% after year 4 with escalations tied to the CPI (capped at 2.5%).

PURE is one of the leading gaming operators in Canada and the largest in Alberta and will become VICI’s 11th tenant. VICI expects the transaction to be immediately accretive to AFFO per share due to the attractive spread to their cost of capital.

VICI – Transaction Overview

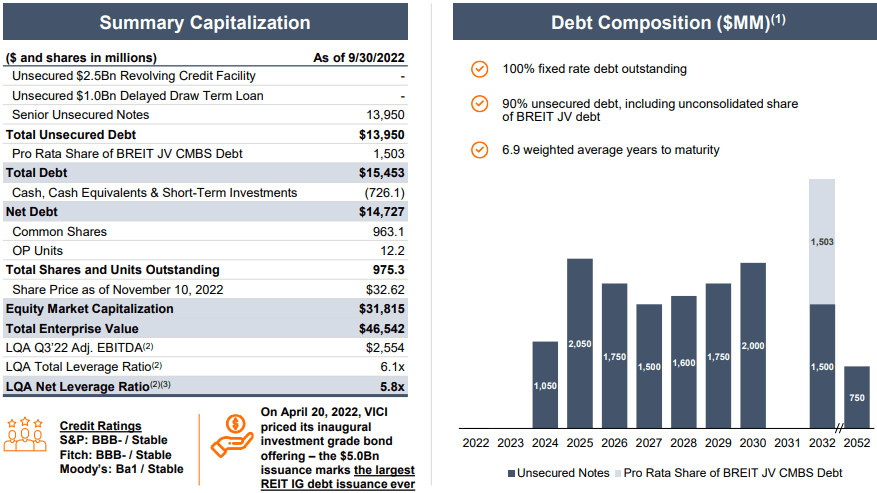

VICI has good debt metrics with a Net Leverage ratio of 5.8x (Latest Quarter Annualized) and an investment grade balance sheet with a BBB- credit rating. 100% of their debt is fixed rate and 90% is unsecured. Their outstanding debt has a 6.9 weighted average to maturity and no maturity comes due until 2024.

VICI – Investor Presentation

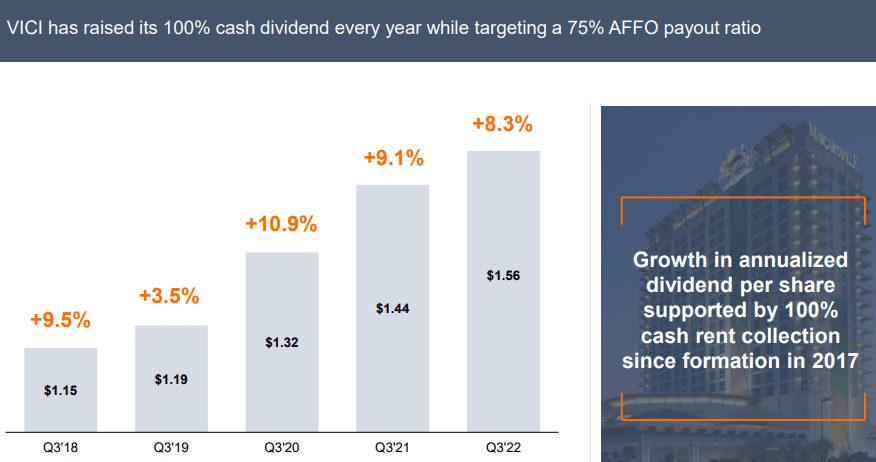

VICI currently has a dividend yield of 4.52% and has raised its dividend each year since becoming a public company. VICI has delivered quarter-over-quarter increases primarily ranging between 8 and 11%, and since 2019 has an average dividend growth rate of 10.8%. The dividend is well covered with an AFFO (Adjusted FFO) payout ratio of 78.13% in 2022.

VICI – Investor Presentation

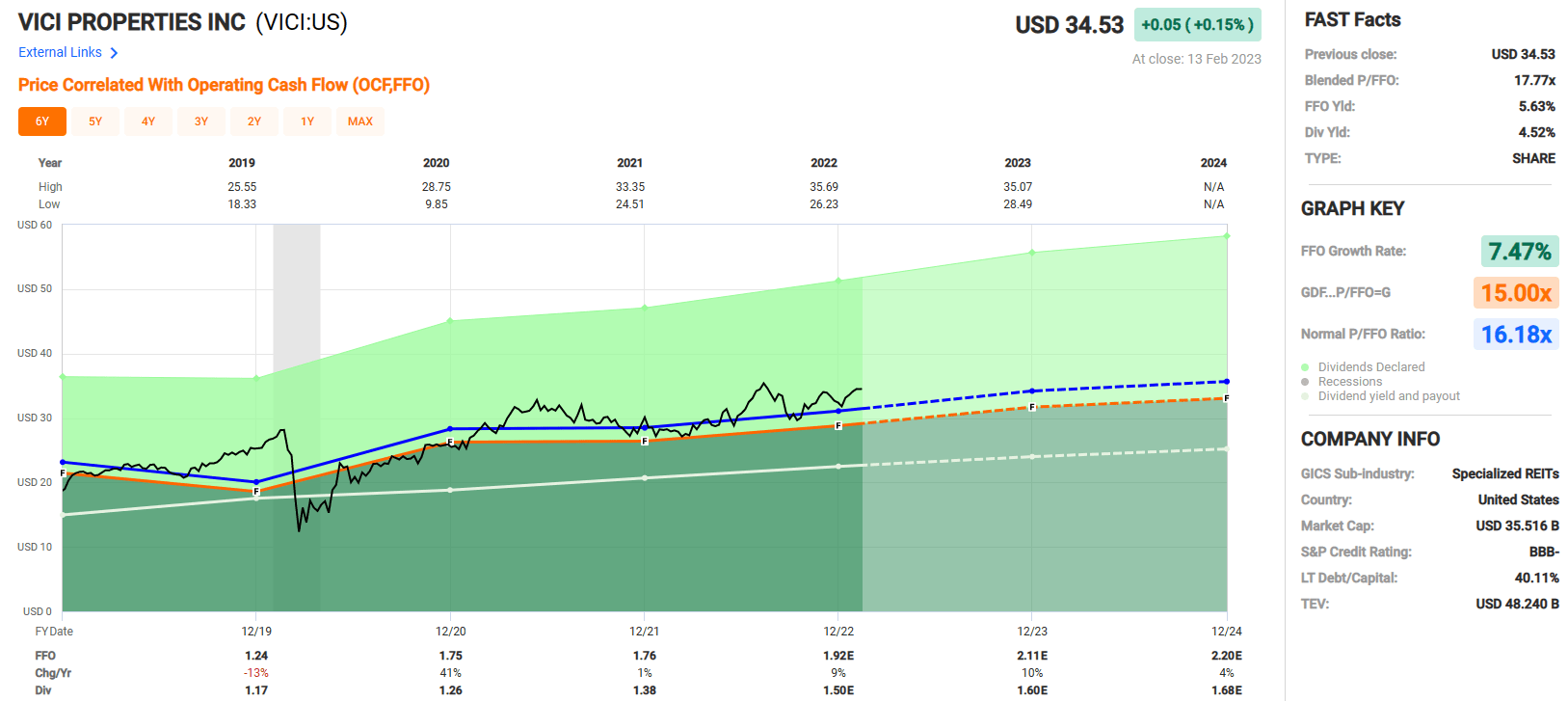

Currently VICI is trading at a blended P/FFO ratio of 17.77x, which is a slight premium to their normal P/FFO of 16.18x. They have strong FFO growth at 7.47% and are expected to increase FFO by 10% in 2023. VICI’s dividend track record is excellent in both consistency and growth and is well supported by the growth of its operational earnings. At iREIT, we rate VICI Properties a BUY.

FAST Graphs

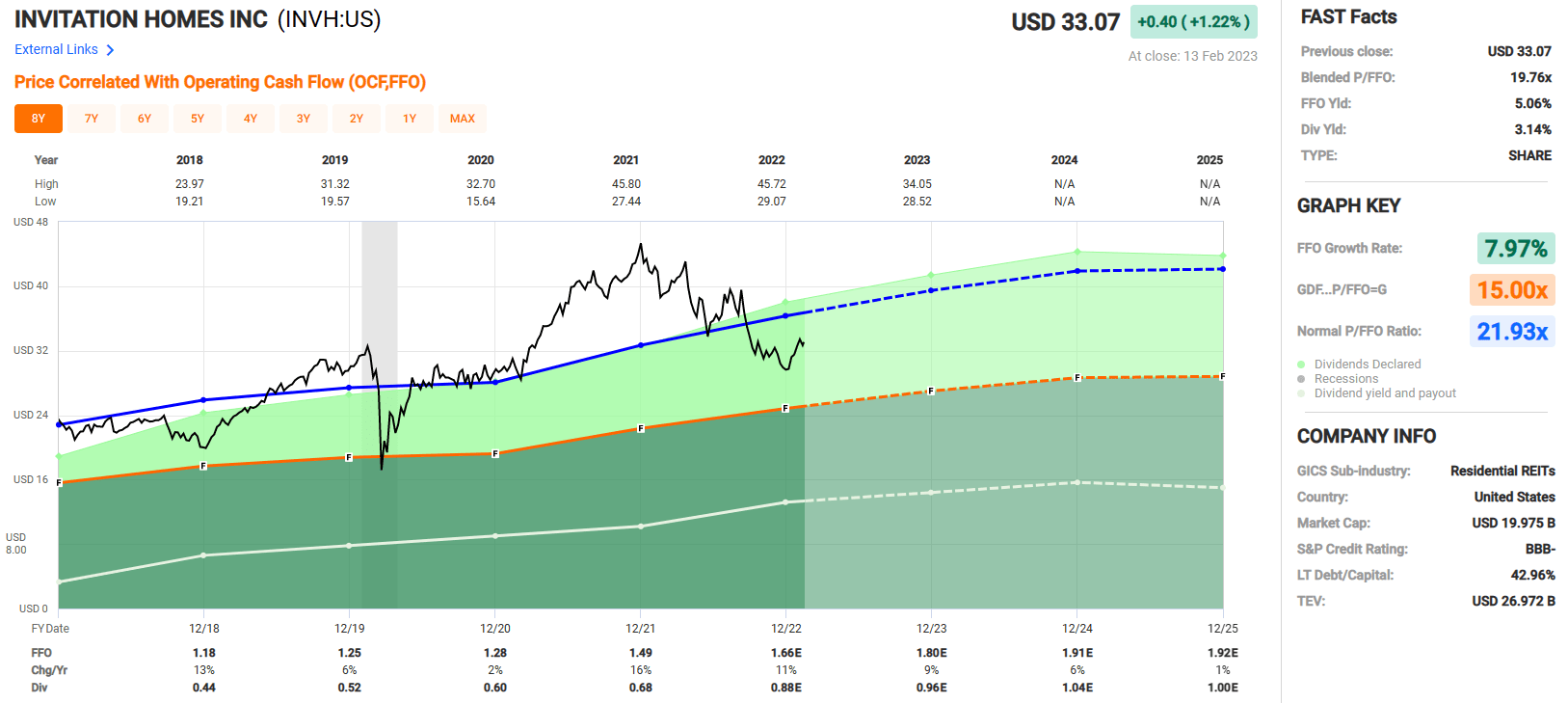

Booyah Pick #2: Invitation Homes Inc. (INVH)

Invitation Homes was founded in 2012 before becoming publicly listed in 2017. INVH is a REIT that specializes in single family homes and is one the few REITS with this area of focus.

Currently, INVH is the number one home leasing company in the nation with approximately 80,000 homes for lease across the nation. Their homes are within close proximity to schools and jobs and have roughly 80% resident retention.

INVH is well-diversified geographically, with a particular focus in the southeast and California with 95% of their revenue coming from the Sunbelt, Western U.S., and Florida.

INVH strategically acquires properties near areas with higher-than-average job growth. Since 2012, regions where INVH homes are located had two times more job growth and 38% more home price appreciation than the U.S. average.

INVH – Investor Presentation

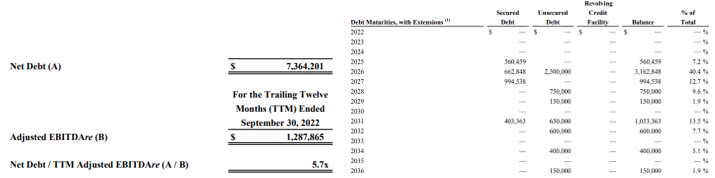

Invitation Homes has good debt metrics with a Net Debt to Adjusted EBITDAre of 5.7x, down from 6.2x the prior year, and a Fixed Charge Coverage ratio of 4.3x.

They have an investment grade credit rating of BBB- and $1.87 billion in liquidity. INVH has a relatively high amount of secured debt at approximately 33.5% but has no debt maturity due until 2025 (with extension options exercised).

INVH – Supplemental

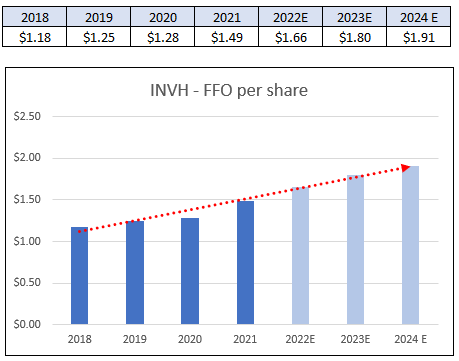

Invitation Homes has delivered strong growth in its Funds from Operations (“FFO”), with increases in FFO in each year since its public listing. Since 2018, INVH has had an average growth rate of 7.97%, with Analysts projecting a 9% increase in 2023 and a 6% increase in 2024.

FAST Graphs (data compiled by iREIT)

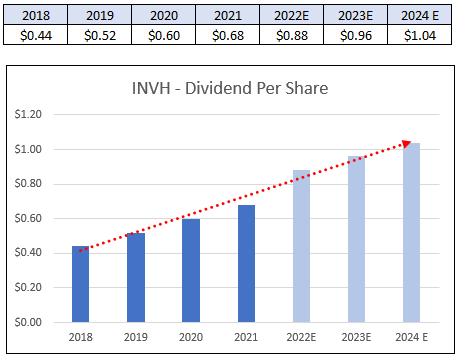

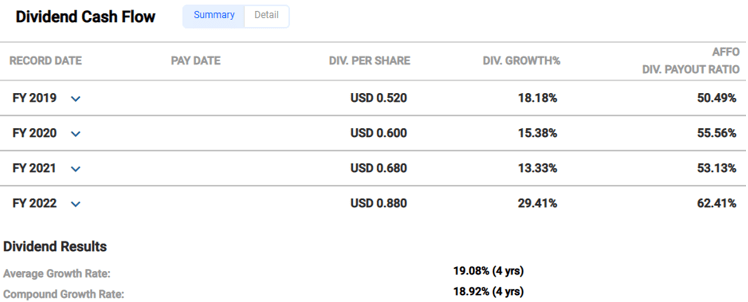

Similarly, INVH has delivered strong dividend growth with an average growth rate of 19.08% over the last four years. Currently INVH has a dividend yield of 3.12% and on February 3, 2023, they announced the quarterly dividend would be increased from $0.22 to $0.26 per share for an 18.2% increase in its cash dividend.

INVH – Press Release FAST Graphs (data compiled by iREIT)

In 2022, Invitation Homes increased its dividend by 29.41%, and as previously mentioned has an average dividend growth rate of 19.08%. The dividend is very safe, with a lot of room for future growth with an AFFO payout ratio of just 62.41%.

FAST Graphs (INVH Dividend)

Currently INVH is trading at a blended P/FFO of 19.76x which compares favorably to its normal P/FFO multiple of 21.93x.

The company is one of the few REITs with a focus on single family rentals and has delivered strong growth in its funds from operations and dividends since going public. It is investment grade, with good debt metrics and has a relatively safe AFFO payout. At iREIT, we rate Invitation Homes a BUY.

FAST Graphs

Booyah Pick #3: Hannon Armstrong Sustainable Infrastructure Capital, Inc. (HASI)

Hannon Armstrong is a Mortgage REIT (“mREIT”) based in Annapolis, Maryland with a focus on climate solutions. HASI provides capital to companies investing in energy efficiency, renewable energy, and other sustainable infrastructure markets.

HASI states its core purpose as making climate-positive investments while delivering superior risk-adjusted returns. Their vision is so centric to their investment strategy that they require all potential investments to reduce carbon emissions, or at least be carbon neutral or have some other benefit to the environment such as reducing water consumption.

HASI divides its markets and asset classes into three categories: Behind-the-Meter, Grid-Connected, and Sustainable Infrastructure.

- Their Behind-the-Meter category includes facility-specific solutions such as solar power generation, electric storage, and efficiency improvements with heating, air conditioning, ventilation, roofs, windows and lighting.

- HASI’s Grid-Connected category includes assets to generate wholesale electric power from cleaner sources such as solar, solar storage, and onshore wind.

- Their Sustainable Infrastructure segment includes assets that provide energy system resiliency such as renewable natural gas plants, water systems, ecological restoration, and transportation fleet enhancements.

HASI – Investor Presentation

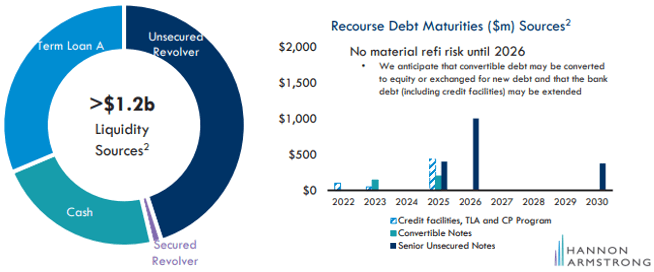

HASI has an investment grade (“IG”) rating by Moody’s with a credit rating of Baa3 but is just one notch under IG rated by S&P and Fitch with a credit rating of BB+ (Junk). They have a 1.7x debt to equity ratio and 93% of their debt is fixed rate. Additionally, they have $1.2 billion in liquidity and no material debt refinancing risk until 2026.

HASI – Investor Presentation

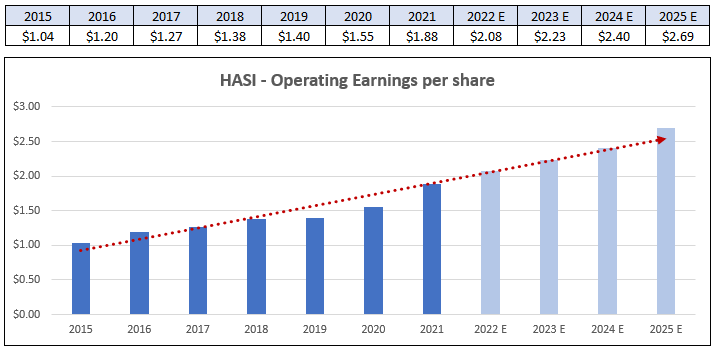

HASI has consistently delivered strong growth in its Operating Earnings per share with an average growth rate of 10.57% from 2016 to 2022. Operating Earnings are expected to grow by 7% in 2023, 8% in 2024, and 12% in 2025.

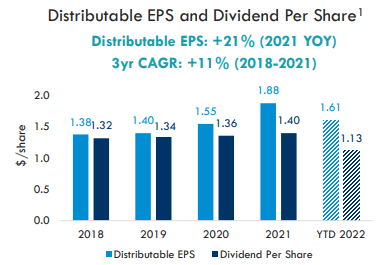

Similarly, HASI’s Distributable EPS has a three-year compound annual growth rate of approximately 11% and has covered the dividend in each year since 2018. Their dividend payout as a percentage of distributable earnings was 74.47% in 2021 and 70.18% as of November 2022.

HASI – Investor Presentation FAST Graphs (compiled by iREIT)

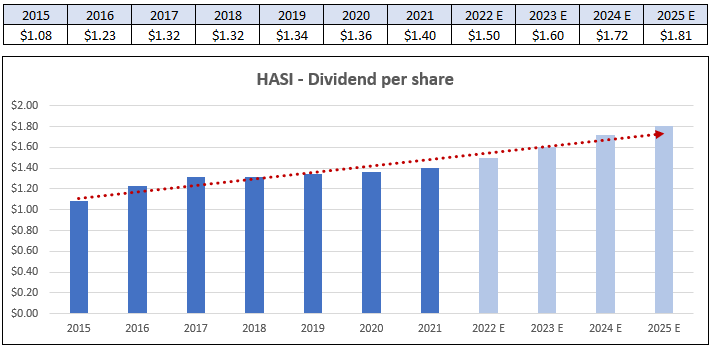

HASI has increased its dividend each year since 2015 with the exception of 2018 where it remained flat at $1.32. Overall HASI has been consistent with their dividend increases and has an average dividend growth rate of 6.46% over the last eight years.

FAST Graphs (compiled by iREIT) FAST Graphs (HASI Dividend)

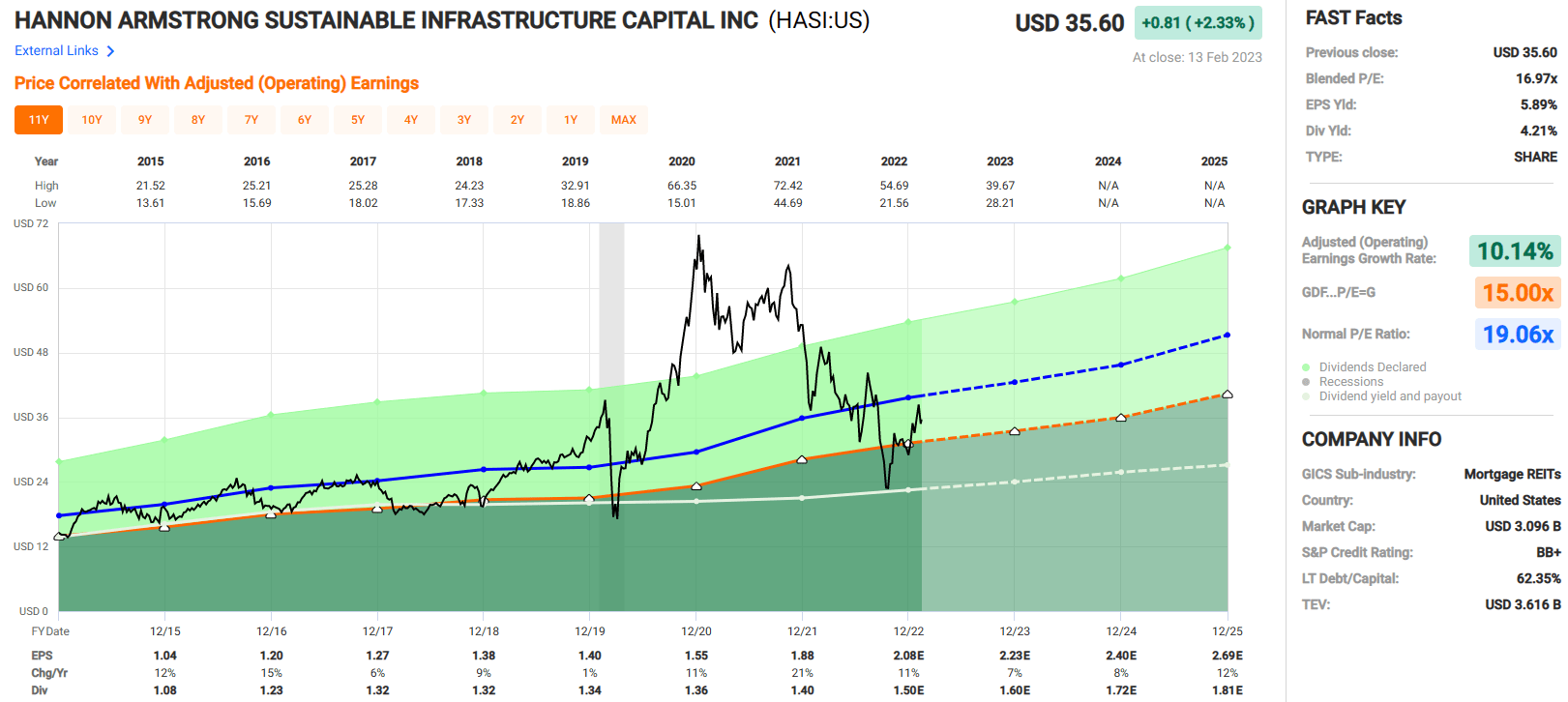

HASI currently offers a 4.21% dividend yield and is trading at a blended P/E of 16.97x, which is under their normal P/E ratio of 19.06x.

They have reliably paid and raised the dividend that is well covered by distributable earnings, and they offer exposure to the renewable energy industry that is expected to expand over time. At iREIT, we rate HASI a Spec BUY.

FAST Graphs

Essential Properties Realty Trust, Inc. (EPRT)

Essential Properties Realty Trust is a triple net lease REIT that owns single-tenant properties and specializes in experience-based or service-oriented businesses. EPRT is in 16 industries and has 329 tenants that occupy 1,561 properties in 48 states.

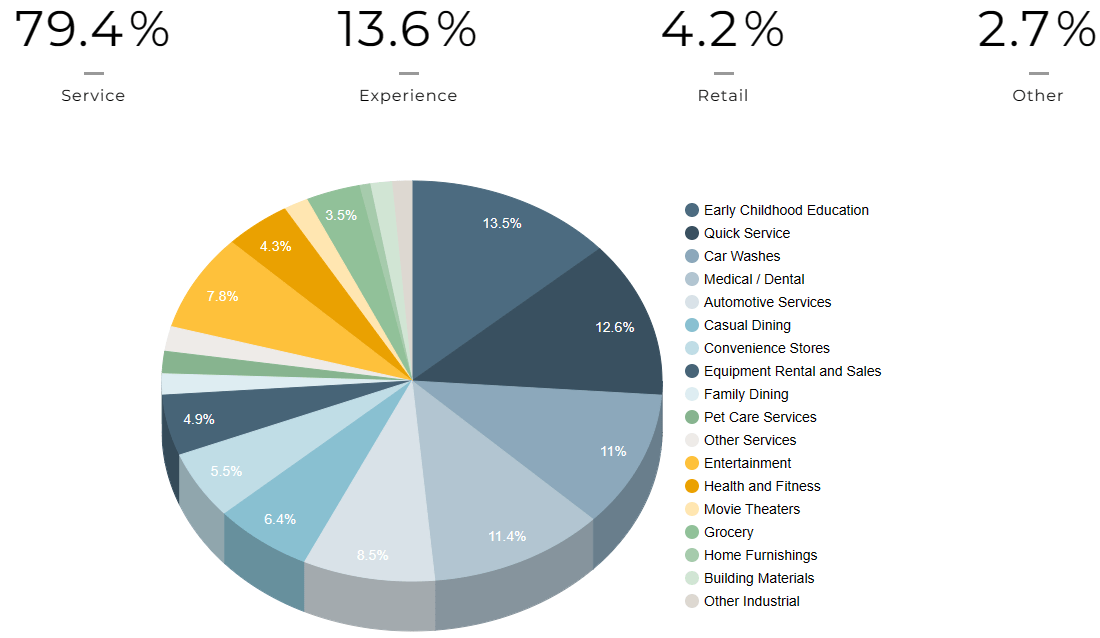

In all EPRT’s real estate covers 14.4 million square feet. They have a 99.8% lease rate and a weighted average lease term (“WALT”) of 14 years. 79.4% of their properties are classified as service, 13.6% as experience, and 4.2% as retail. Their largest categories include Early Childhood Education, Quick Service Restaurants, Car Washes, and Medical / Dental offices.

EPRT – Portfolio

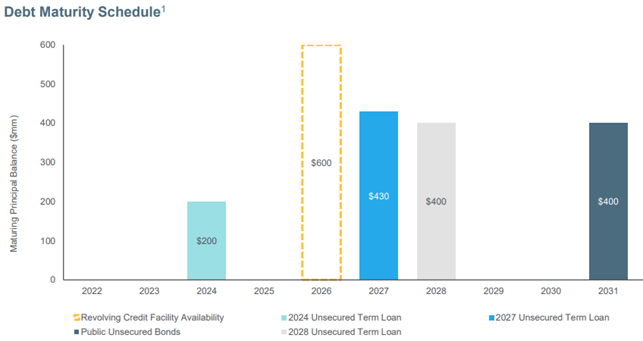

Essential Properties Realty Trust has good debt metrics and liquidity. They have $294 million in cash and full availability on their credit facility of $600 million for approximately $900 million in total liquidity as of the third quarter in 2022.

EPRT has a Net Debt to Adjusted EBITDAre of 4.4x and a Fixed Charge Coverage ratio of 5.7x. EPRT’s debt is 100% fixed rate and has a weighted average to maturity of 5.5 years. Their weighted average interest rate is 3.3% with no debt maturity until 2024.

EPRT – Portfolio

Since their IPO in June 2018 EPRT has delivered strong growth in its funds from operations. Since 2019 they have averaged an annual FFO growth rate of 11.59%. Analysts project FFO to increase by 4% in 2023 and by 8% in 2024.

FAST Graphs (compiled by iREIT)

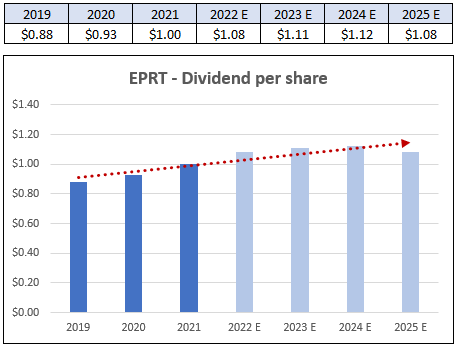

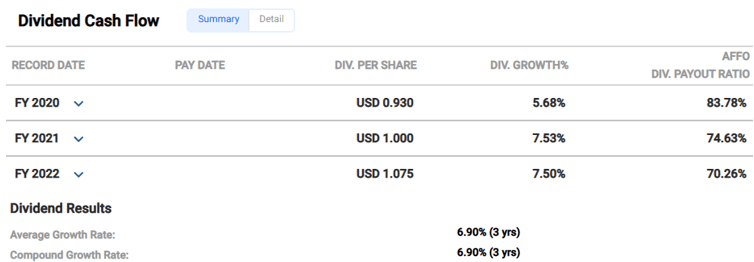

Over their short history, EPRT has increased its dividend each year and has averaged a growth rate of 6.90% since 2020. Analysts are projecting a dividend increase of 2.8% in 2023.

Along with the healthy growth rate, the dividend is very secure with an AFFO payout ratio of 70.26% in 2022. The strong FFO growth along with the low payout ratio should provide plenty of cushion for the dividend in case of an adverse event as well as provide plenty of room for future growth.

FAST Graphs (compiled by iREIT) FAST Graphs (EPRT dividend)

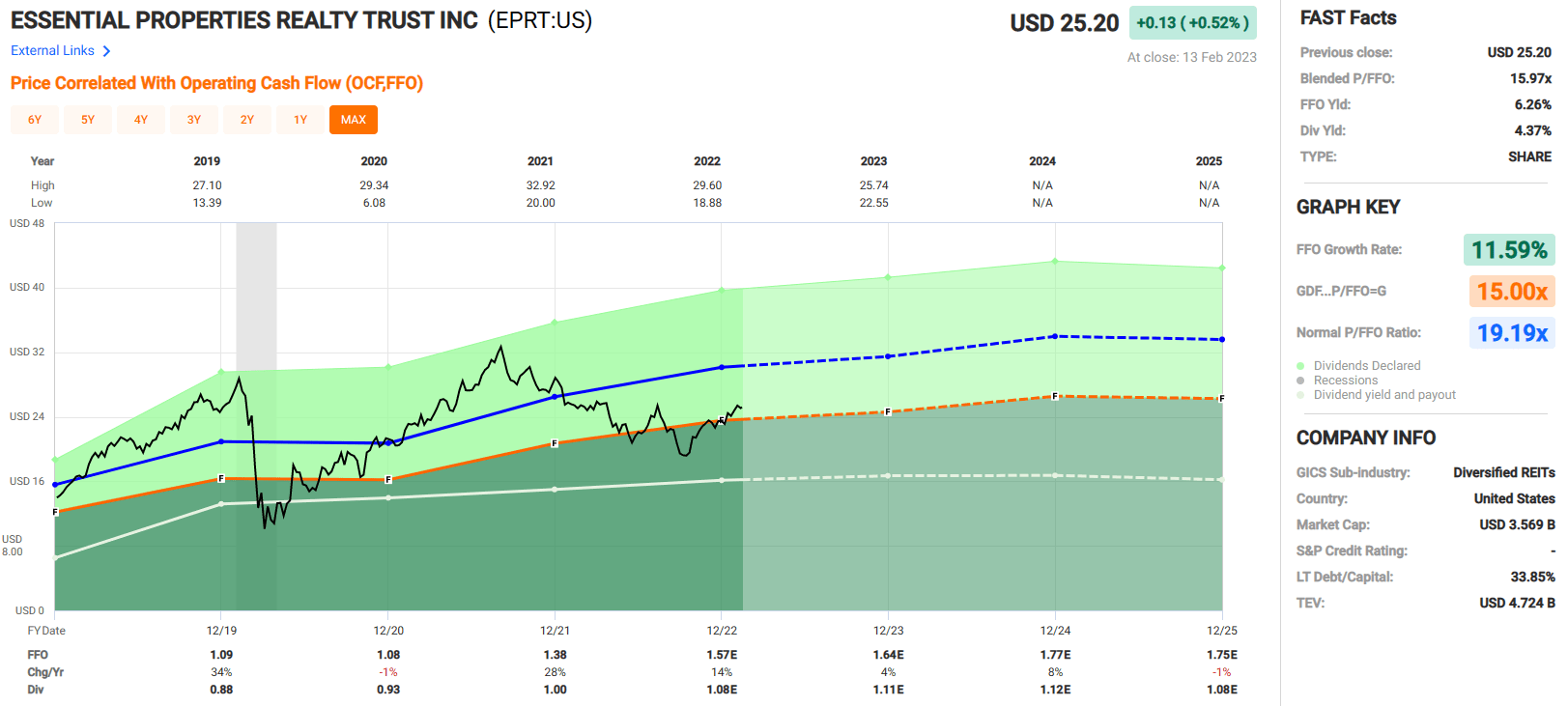

EPRT is trading at a blended P/FFO of 15.97x which is well below their normal P/FFO multiple of 19.19x. They currently pay a 4.37% dividend yield and have delivered high growth rates in both FFO and the dividend over their short history.

They have a strong balance sheet with good debt levels and a low payout ratio. Additionally, their service and experience-based properties should be well insulated from any e-commerce threats. At iREIT, we rate Essential Properties Realty Trust a BUY.

FAST Graphs

Booyah Pick #5: American Tower Corporation (AMT)

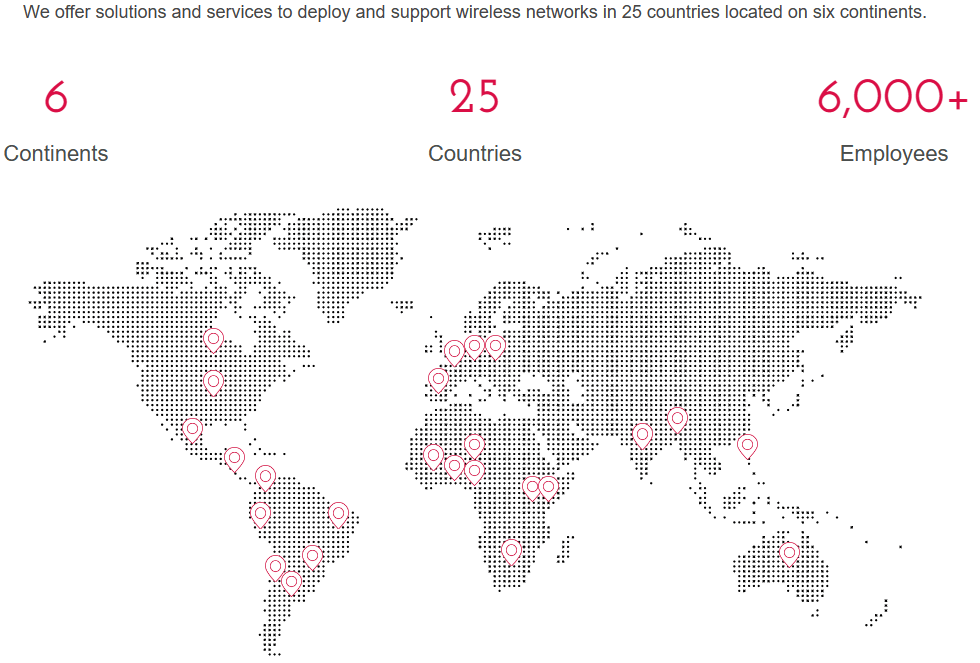

American Tower is one of the largest REITs, with a market capitalization of almost $100 billion and a global presence in 25 countries located on 6 continents. AMT was founded in 1995 and owns multitenant cell towers.

Their portfolio includes more than 43,000 properties in the U.S. and Canada and roughly 180,000 properties internationally, for a total of approximately 223,000 communication sites. Cell Towers are necessary for everyday activities such as sending a text, making a phone call, ordering merchandise online, saving a picture to the cloud, sending an email, etc.

Towers are critical infrastructure and part of the e-commerce trifecta (along with data centers and logistic facilities), and without them many of the conveniences we enjoy every day would not be possible. As we continue into the digital age and with the rollout of 5G there are many tailwinds to support future growth.

American Tower

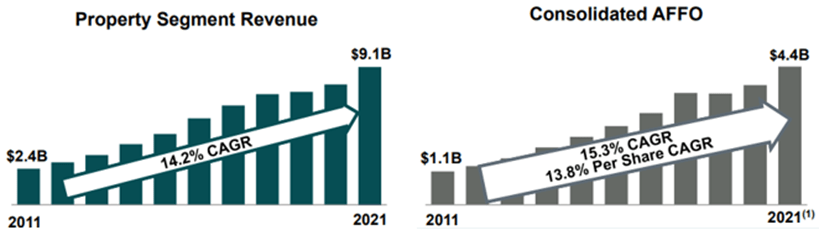

American Tower has delivered growth in pretty much every metric over the last decade. Since 2011 AMT has grown segment revenue by a compound annual growth rate of 14.2% and their Adjusted Funds from Operations (“AFFO”) at a compound annual growth rate of 13.8% per share.

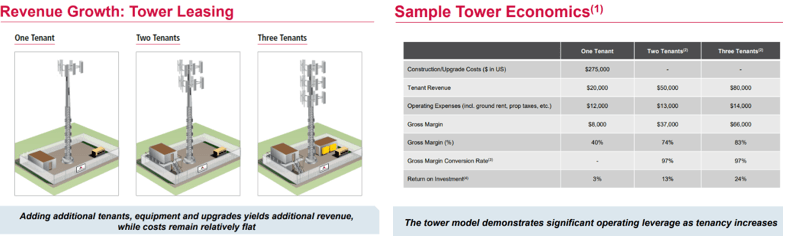

It makes sense that AMT has delivered such growth over the last decade, as e-commerce and digital communication has really taken off since that time. But another factor in their growth comes from their business model, in that they can absorb multiple tenants per tower with diminishing investment cost as more tenants share the same infrastructure.

AMT – Investor Presentation

As illustrated below, adding additional tenants increases revenue while costs remain relatively flat. The primary cost associated with cell towers is the construction and upgrade costs that would be incurred regardless of how many tenants lease the space.

As more tenants are added, total revenue increases proportionally, but there is no additional construction costs and operating expenses are only marginally impacted. This leads to a higher Return on Invested Capital (“ROIC”) for each additional tenant.

AMT – Investor Presentation

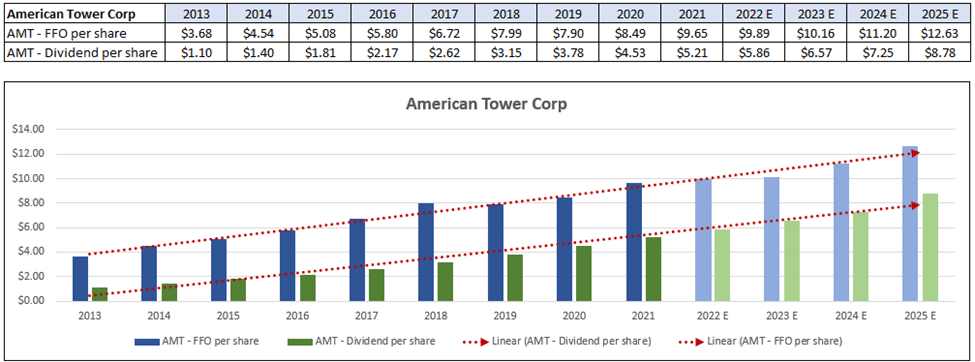

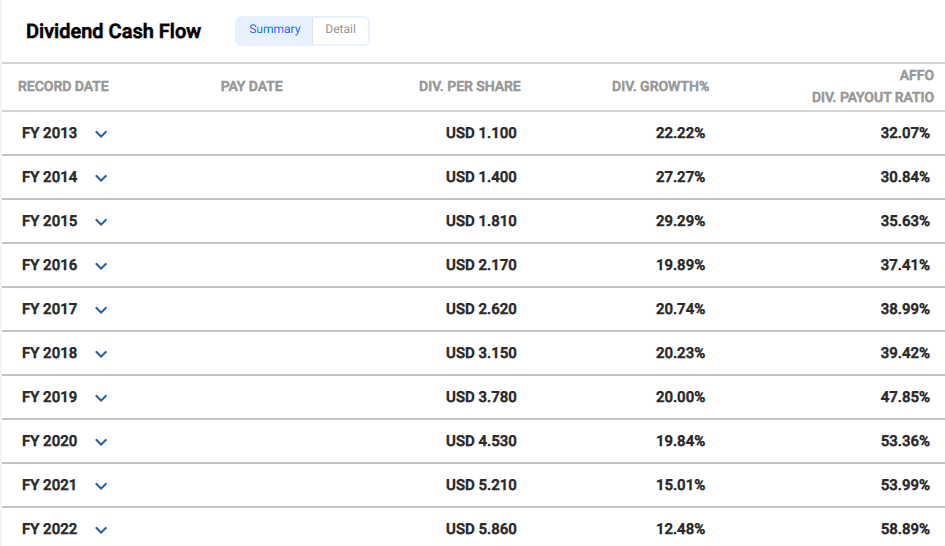

Between the structural advantages of their business model and the overall increasing demand for digital networking, American Tower has delivered impressive growth rates in revenue, funds from operations (“FFO”), adjusted FFO, and their dividend rate. Since 2013, AMT has an average FFO growth rate of 11.69% annually and an average dividend growth rate of 20.70%.

Additionally, AMT has increased its dividend each year consecutively since 2013 and has increased their FFO each year over the same time period with the exception of 2019 when FFO declined by 1%. Analysts are projecting a 3% increase in FFO in 2023, followed by an increase in FFO of 10% and 13% in the years 2024 and 2025 respectively.

FAST Graphs (compiled by iREIT)

Currently, AMT pays a 2.72% dividend yield that is very well covered with an AFFO payout ratio of 58.89%. The fact that they are able to grow the dividend at approximately 20% per year, while maintaining such a low AFFO payout is a testament to the high earnings growth they continue to deliver that supports the dividend.

Having such a low AFFO payout provides several advantages. Obviously, it secures the dividend and allows for future growth, but it also allows AMT to retain more cash for future investment.

Funding a portion of their investments with retained earnings lowers their overall cost of capital as opposed to issuing debt or equity. That’s not to say AMT does not need to raise capital by issuing debt and equity, but the more they can fund investments with retained earnings, the lower their overall cost of capital should be.

FAST Graphs (AMT Dividend)

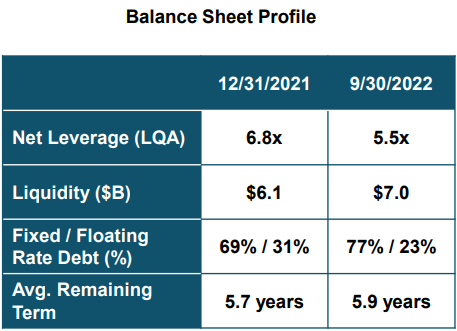

American Tower has good debt metrics that have improved over the prior year with their Net Leverage ratio going from 6.8x in 2021 to 5.5x as of 9/30/2022. Likewise, they improved the amount of floating debt from 31% in 2021 to 23% in 2022. AMT has plenty of dry powder with $7.0 billion in liquidity and have an average term to maturity of 5.9 years.

AMT – Earnings Presentation

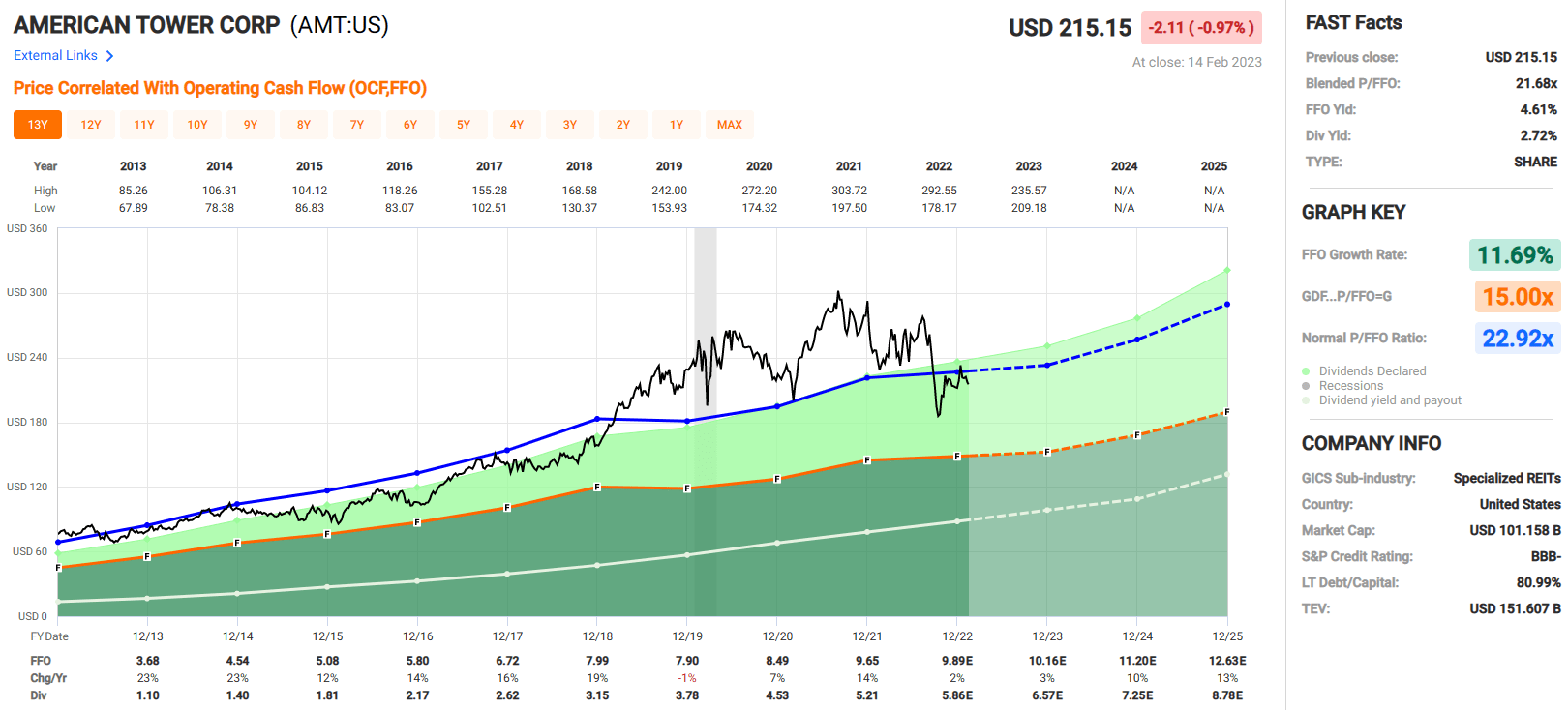

Currently AMT trades at a P/FFO multiple of 21.68x which is slightly under their normal P/FFO of 22.92x. This is a high-quality blue chip REIT with sound debt metrics and an investment-grade credit rating of BBB-.

They have delivered outstanding growth in revenue, FFO, AFFO, and dividend increases over the last decade and have plenty of room for future growth, given the tailwinds of e-commerce and digital networking. At iREIT, we rate American Tower a BUY.

FAST Graphs

Booyah!

Are you familiar with the Booyah button?

I’m not sure he coined the word, but I do know that it became popular in the financial world thanks to Jim Cramer. He would shout the word “Booyah” whenever he saw there was a popular trade.

At Wide Moat Research, we like to shout out the word “Booyah” whenever a company raises its dividend, because as you know,

“The Safest Dividend is the one that’s just been raised.”

Happy SWAN Investing!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment