franckreporter

The S&P 500/SPX (SP500) is approaching another crucial inflection point. We have several critical fundamental factors converging with technical elements that should enable the stock rally to continue moving higher from here. However, it’s going to be a hard ride in 2023. There could be more downside for stocks as the economy slows further, and recession fears produce more volatility spikes in the early parts of the year.

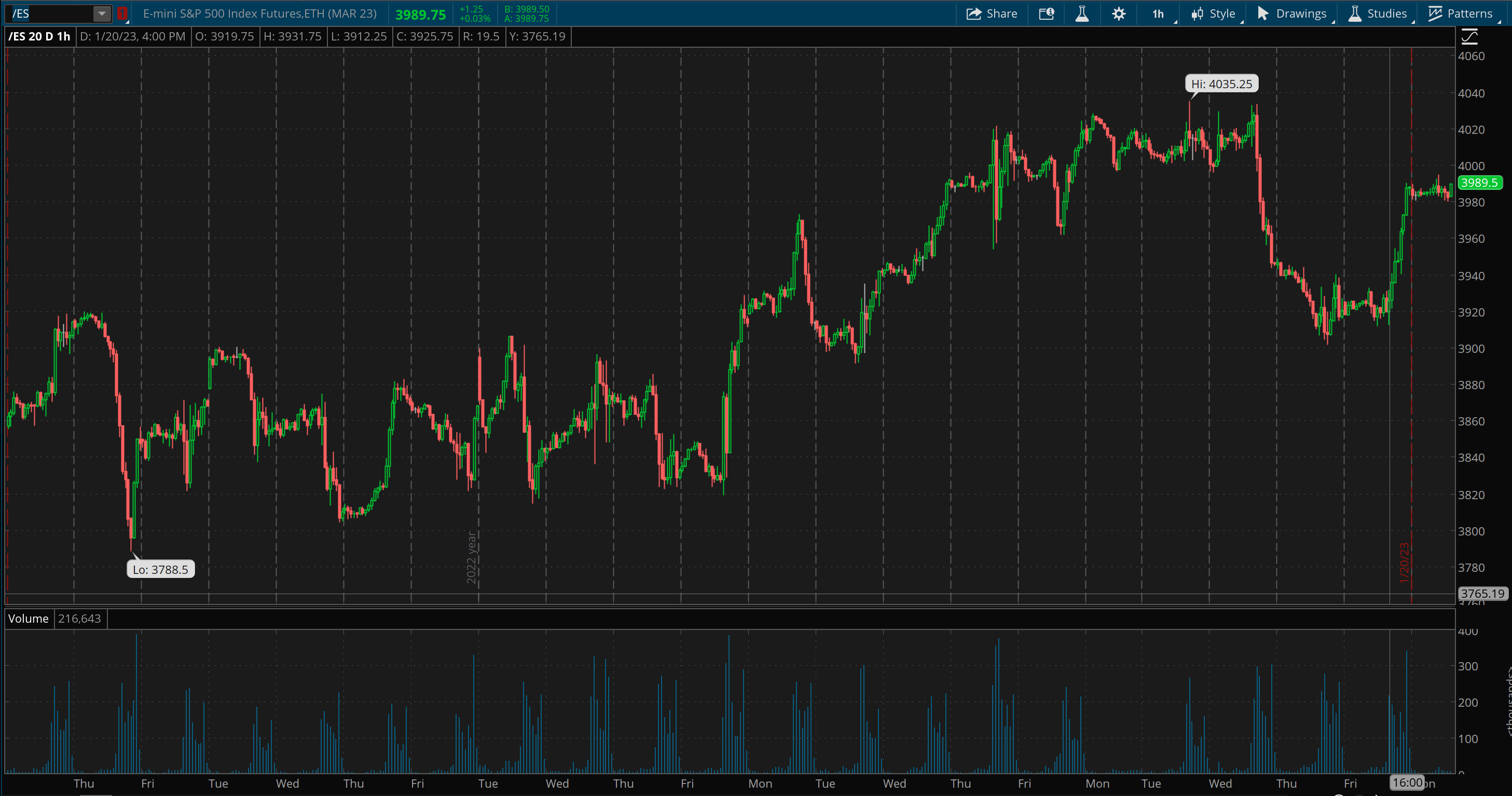

Futures Are Moving Higher This Morning

SPX (thinkorswim)

We have a beautiful, bullish cup and handle pattern shaping out her in SPX. 4,000 resistance is the next critical technical level to get above. After the successful and decisive penetration of 4K, the SPX should appreciate to the 4,200-4,300 zone next. Favorable fundamental factors such as constructive earnings results and a transitioning Fed (hawkish to more dovish) should enable stock prices to appreciate further in the near term. However, investors should remain aware of intermediate-term recession-related risks simultaneously. Therefore, while SPX and quality stocks could continue rising in the near term, there is still the risk of increased volatility in the months ahead. Nevertheless, since we are here, let’s see what the market has in store soon.

Earnings Image

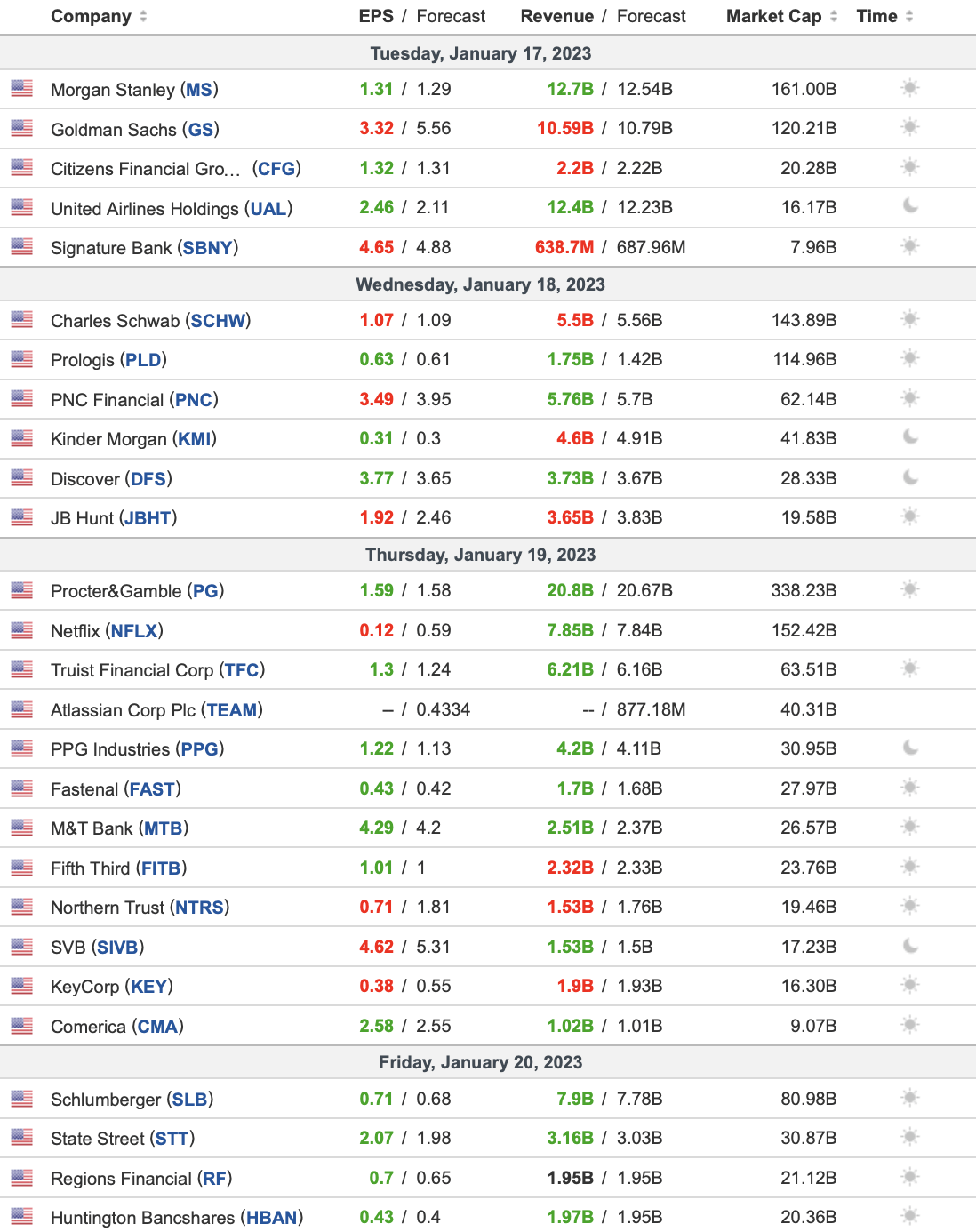

Recent Results

Earnings (Investing.com)

Despite several minor disappointments like Goldman Sachs (GS), most earnings came in better than expected. Netflix (NFLX), Procter & Gamble (PG), Schlumberger (SLB), and others have put up solid numbers for the last quarter, and this positive trend of better-than-anticipated earnings announcements will likely continue as we advance.

This Week’s Upcoming Earnings – A Crucial Mix

Several prominent and market-leading and potentially market-moving companies reporting in the coming days include Microsoft (MSFT), Tesla (TSLA), J&J (JNJ), Danaher (DHR), Verizon (VZ), AT&T (T), 3M (MMM), Raytheon (RTX), Lockheed Martin (LMT), and others. However, the following week looks even more critical with tech giants like Alphabet (GOOG) (GOOGL), Amazon (AMZN), Apple (AAPL), and others reporting soon. Therefore, the next two weeks will be crucial in deciding whether this rally will continue or if it is time to fade the move.

In The End, The Market Always Wins

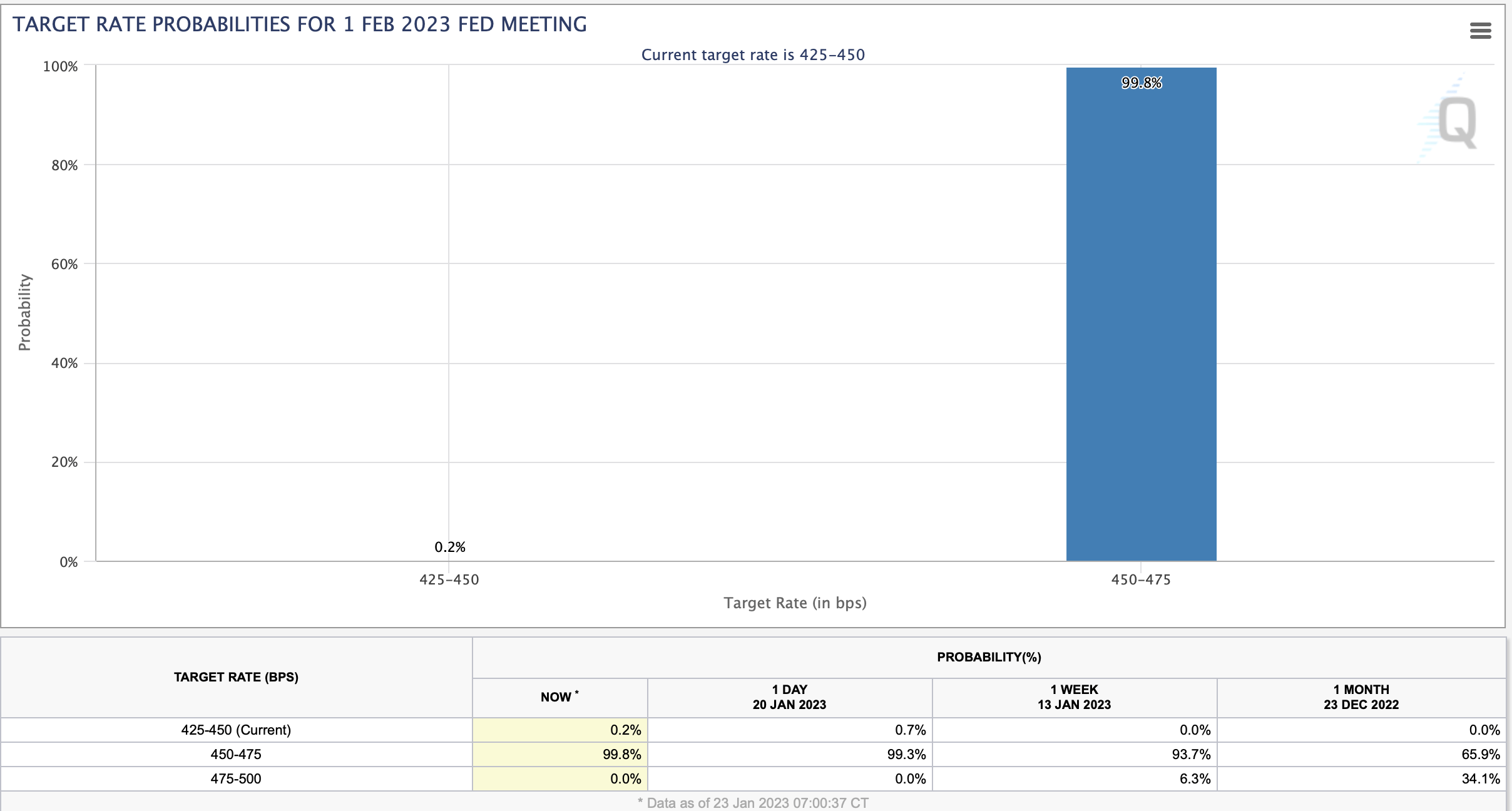

It matters little that the Fed, led by Chair Powell, uses tough rhetoric. In the end, the market is always right. The market will likely get its pivot from the Fed, and we continue seeing increased dovishness in the latest target rate probabilities.

Target rate probabilities (CMEGroup.com)

About a month ago, we debated whether the Fed would follow through with another 50 bps move. However, now we see that there is even a tiny chance that the Fed will keep rates unchanged in its next meeting. I expect another 25 bps move, but the supporting rhetoric is bound to get more dovish as we advance. The Fed is now confronted with dropping inflation, but many other critical economic indicators are starting to stall. Therefore, the Fed must walk a fine line between bringing down inflation and keeping the economy from coming to a halt.

Economic Weakness Becoming Evident

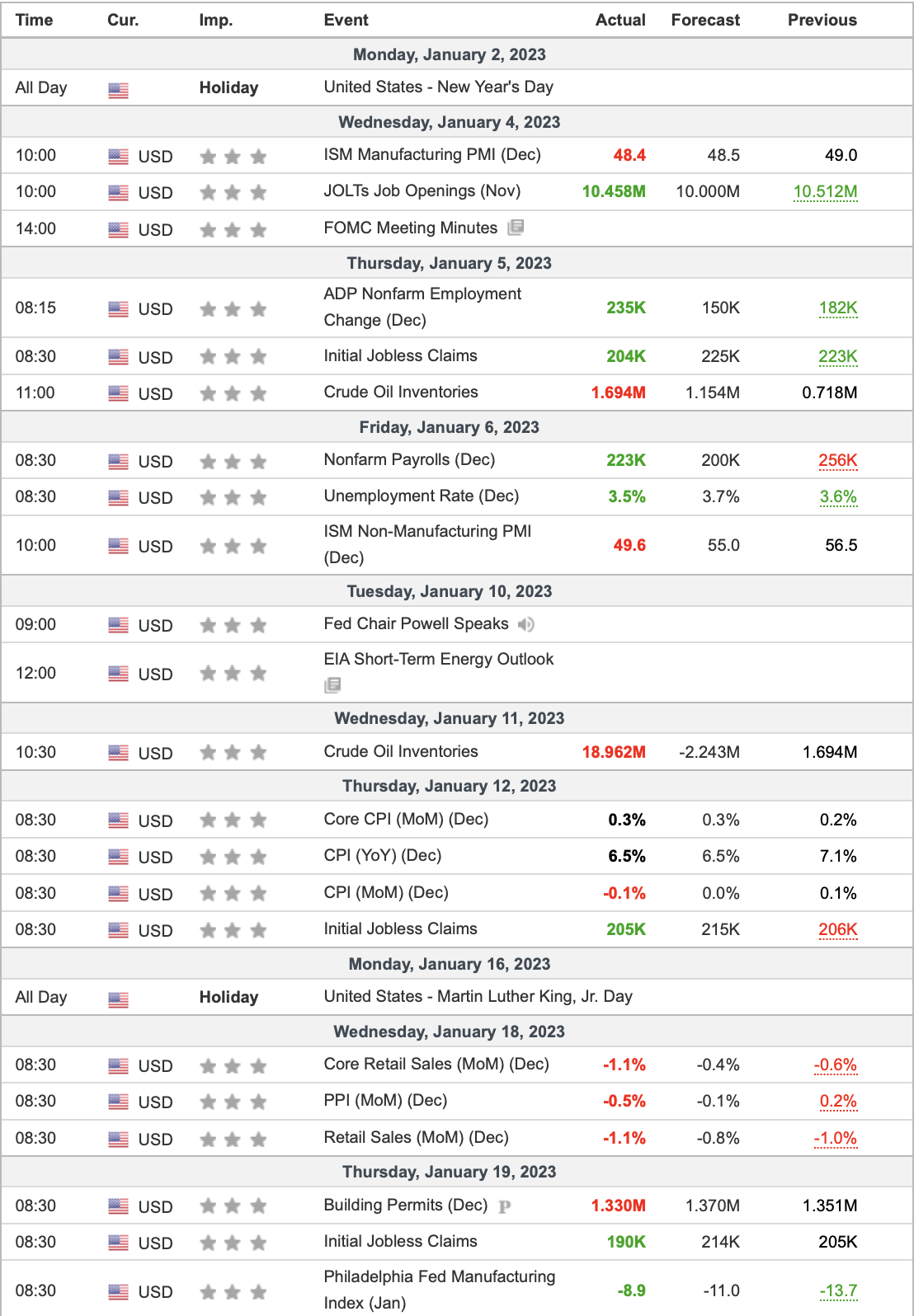

Economic indicators (Investing.com)

Let’s look at some of these recent indicators. Yes, it’s excellent that inflation is coming down, but it is taking many things down simultaneously. ISM manufacturing PMI shows that the manufacturing side of the economy is in contraction. Also, look at the ISM non-manufacturing PMI coming in well below estimates and contracting now. This phenomenon illustrates that the services part of the economy is in more trouble than anticipated in prior months. Possibly most alarming, retail sales (for December) declined by more than expected. A weakening consumer may be the last nail in the coffin the economy needs before falling into a deep recession.

Employment: The Last Domino to Fall

I hear many analysts saying that the labor market is strong, which is excellent for the economy and the stock market. While this dynamic may be true in most cases, the current downturn may take unemployment down soon. While the latest nonfarm payroll report illustrated a significant beat, it may be about as good as it gets for a while.

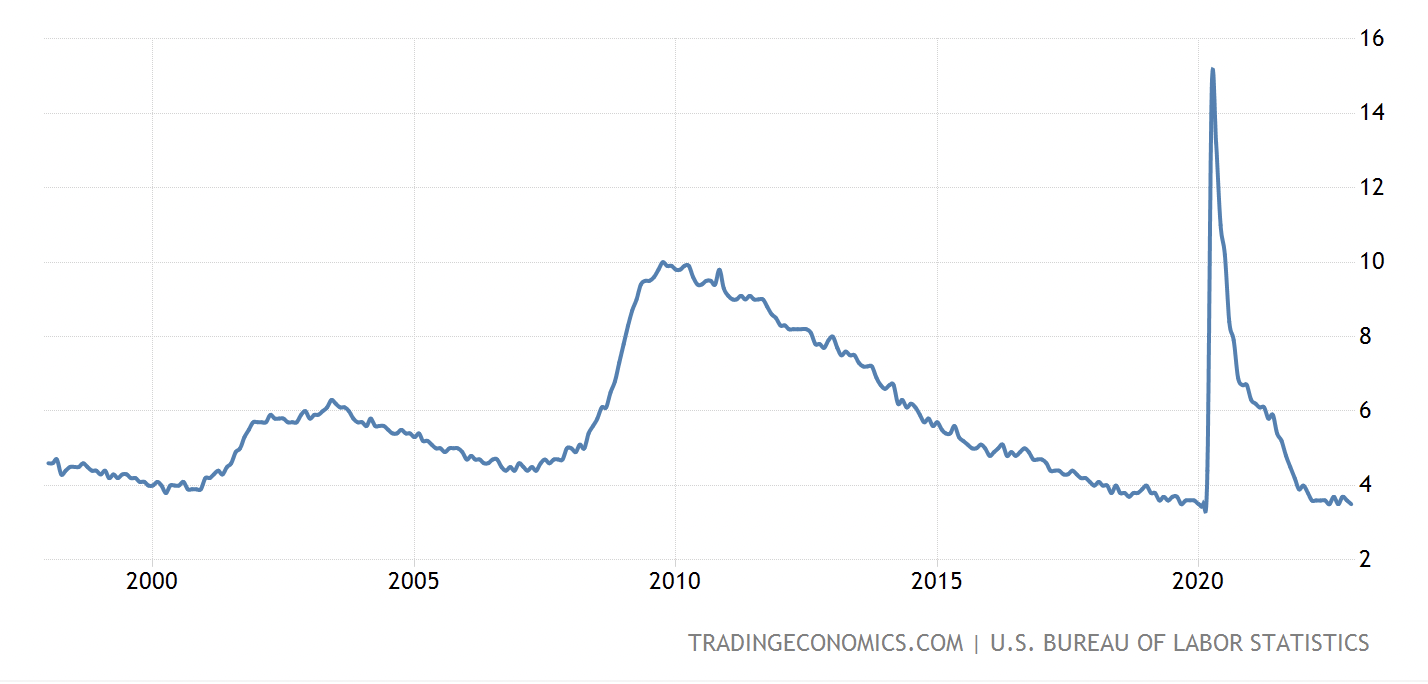

Unemployment Rate – Last 25 Years

Unemployment rate (TradingEconomics.com)

We typically see unemployment bottom around significant recessions and market downturns. The unemployment rate bottomed at around 4% in early 2000, then again we saw a low before the 2007-2009 downturn, and then we saw another low before the coronavirus-induced crash in 2019. Now unemployment is around 3.5%, which is exceptionally low. We have plenty of recent examples that imply we could see a sharp rise in unemployment soon. This phenomenon may be the next shoe to drop, and it will likely lead to more selling in the market, contributing to the Fed’s switching stance and leading to an eventual pivot later, possibly around Q3/Q4 2023.

Portfolio Strategy – Keeping It Simple

I’m staying with what works. We’ve seen significant success in the cryptocurrency segment this year. The QTD return in Bitcoin (BTC-USD) and other digital assets is around 42%. The segment is relatively small, but the performance has been excellent. Of course, if general price action worsens, I will reduce risk first in the crypto space. The AWP’s stock and ETF segment are up by about 11% QTD, crushing the SPX’s and Nasdaq’s performances. I believe in the AWP’s core positions‘ intermediate and long-term potential. The GSM segment is also up significantly this quarter, with significant potential for more advances.

While the AWP is positioned aggressively, I am prepared to decrease risk positions and implement hedges if price action worsens in the coming weeks. If the bear market persists, it could take the SPX down to around the 3,000-3,300 area. Nevertheless, after the bear market bottoms, buying should be fierce, and the stock recovery will likely be rapid. Therefore, my year-end SPX target remains at 4,300.

Be the first to comment