Maddie Meyer/Getty Images News

When it comes to smaller restaurant chains, one of the most iconic in the US has got to be The Cheesecake Factory (NASDAQ:CAKE). Although the company has never been a prime restaurant play from an investment perspective, it has established for itself a nice niche and has had shares trade at levels that would be considered fundamentally attractive. Even throughout the 2022 fiscal year, revenue for the company was increasing nicely. Although the firm is now facing some bottom line pressure. Add on top of this the fact that the stock is not as cheap as it once was, and I have decided to change my own view of the company from being bullish to being neutral. As such, effective as of this writing, I am decreasing my rating on the company from a ‘buy’ to a ‘hold’ to reflect my view that shares should generate upside or downside that is more or less in line with what the broader market should achieve.

The picture has changed

Back in March of 2022, I wrote my first article on The Cheesecake Factory since a prior article that I had published in 2015. I was pleased to find myself looking at a company that I felt had attractive upside potential. Although the company had experienced a rough couple of years because of the COVID-19 pandemic, management’s plans, combined with how cheap shares were, left me feeling bullish enough about the company to rate it a ‘buy’, a rating that reflected my view at the time that shares should outperform the broader market for the foreseeable future. So far, the company has done just that. While the S&P 500 is down 10.7% since the publication of that article, shares of The Cheesecake Factory have generated upside for investors of 2.1%.

Author – SEC EDGAR Data

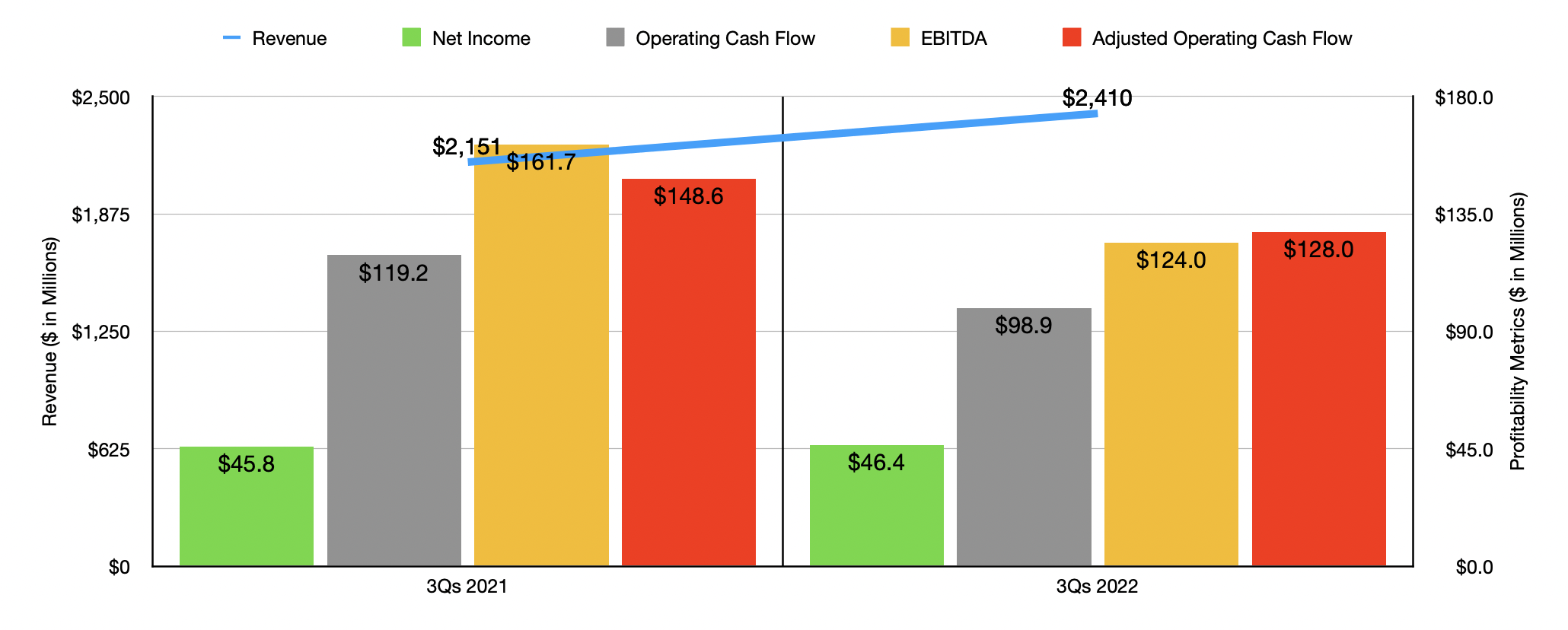

This rather material return disparity comes at a time when revenue for the company remains robust. For the first nine months of its 2022 fiscal year, for instance, the firm reported revenue of $2.41 billion. That’s 12% higher than the $2.15 billion reported the same time one year earlier. Although the company benefited from a rise in location count from 308 properties to 311, the biggest driver for the firm was an 8.2% increase in comparable restaurant sales at its The Cheesecake Factory locations. Even though we have been dealing with inflationary pressures, management attributed this increase to a 9.2% rise in customer traffic. By comparison, a lower average check size decreased sales by 1%. This 1% decline came even at a time when the firm benefited from a 4.8% increase in menu pricing and was actually driven by a 5.8% negative impact from order mix. The company also benefited from a 17% rise in comparable restaurant sales from its North Italia locations, with a 14% increase in customer traffic leading the way.

Profitability figures for the company during this time were somewhat mixed. Net income, for instance, inched up from $45.8 million to $46.4 million. At the same time, however, operating cash flow dropped from $119.2 million to $98.9 million. On an adjusted basis, which ignores changes in working capital, the metric fell from $148.6 million to $128 million. Even EBITDA took a hit, falling from $161.7 million to $124 million.

Author – SEC EDGAR Data

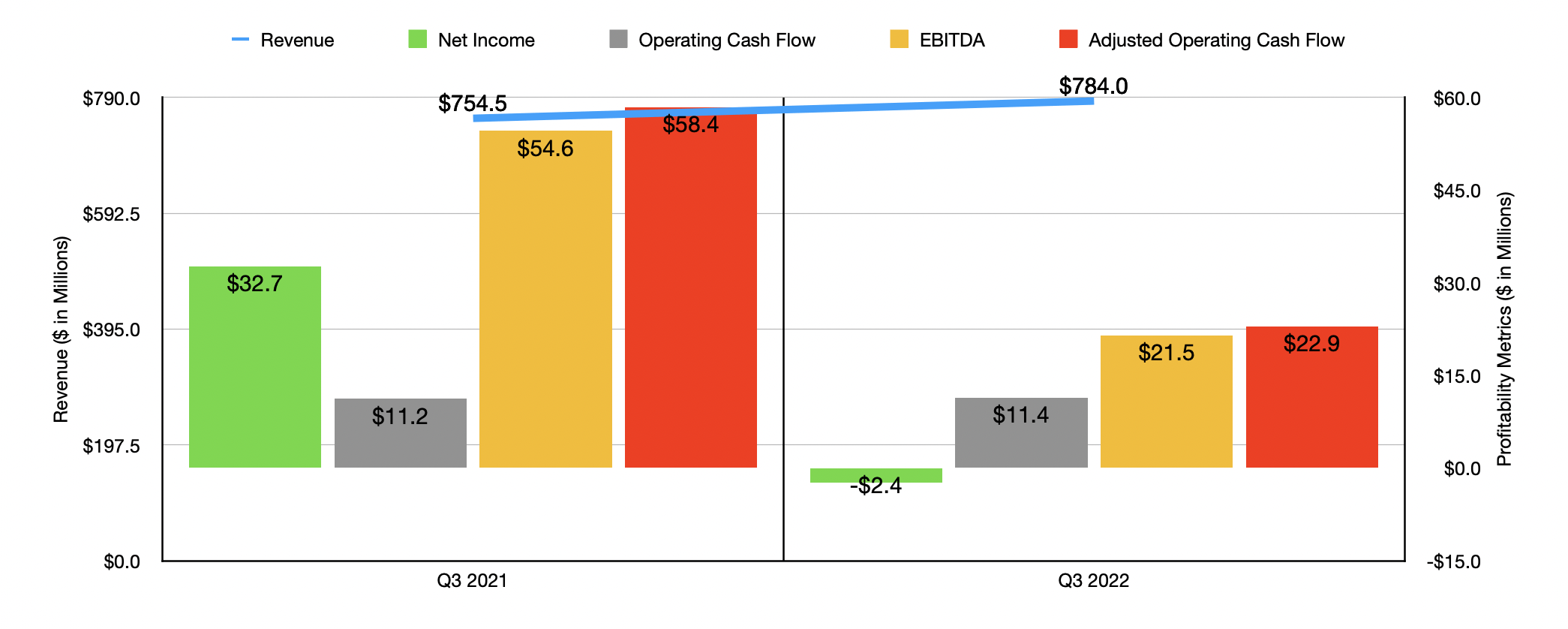

Although the data for the first nine months of 2022 was mixed, it could be described as generally positive. That is less true when looking at data for the third quarter alone. Yes, sales did increase still year over year, climbing from $754.5 million to $784 million. The comparable restaurant sales increase for the company’s hallmark brand came in at only 1.1%. At the same time, however, the company went from a profit of $32.7 million to a loss of $2.4 million. Operating cash flow barely increased, rising from $11.2 million to $11.4 million. But on an adjusted basis it plunged from $58.4 million to $22.9 million. A similar decrease can be seen when looking at EBITDA. According to management, this metric fell from $54.6 million to $21.5 million.

Author – SEC EDGAR Data

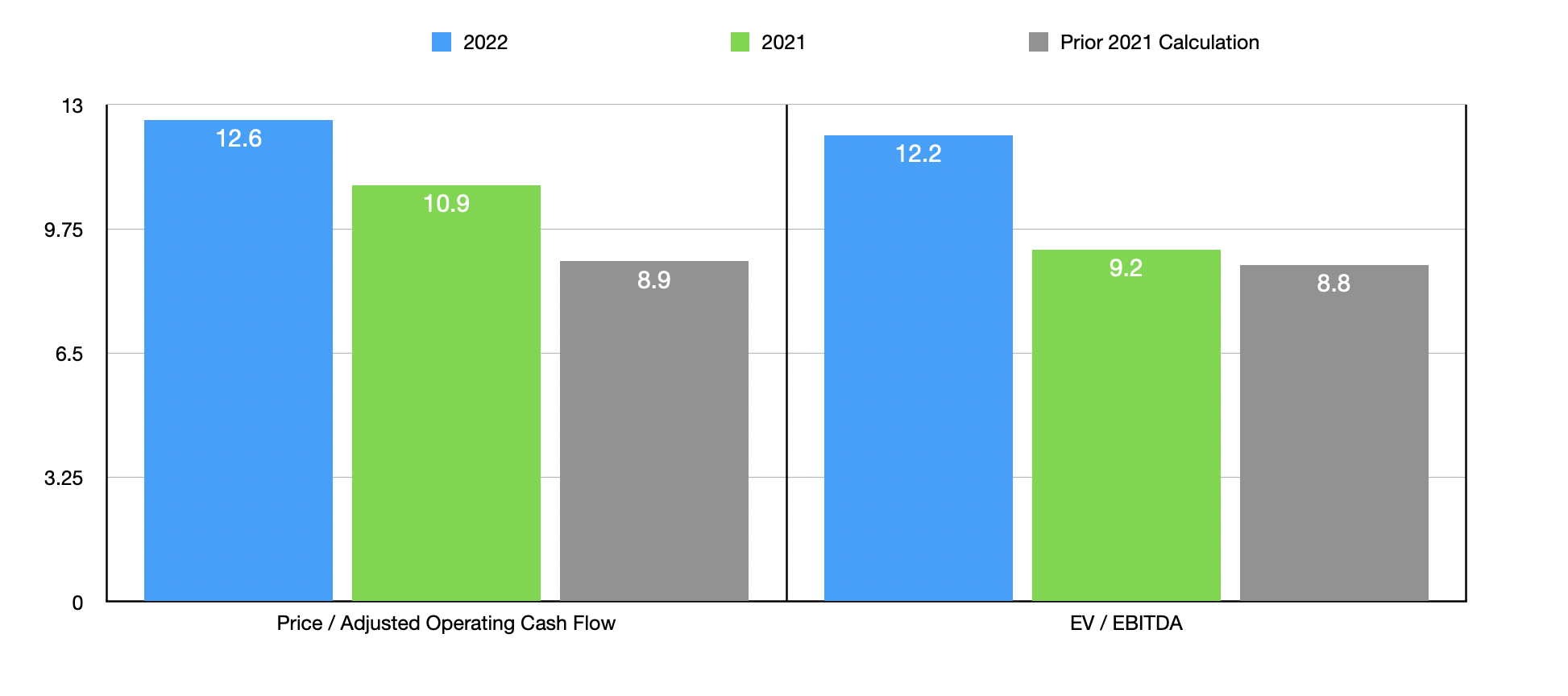

We don’t really know what to expect for the 2022 fiscal year in its entirety. But if we annualized results experienced so far for the year, we would anticipate net income of $49.7 million, adjusted operating cash flow of $156.9 million, and EBITDA totaling $188.9 million. Given the company’s track record with earnings, I don’t believe that they are critical in valuing the enterprise. So using the other two metrics, we get a forward price to adjusted operating cash flow multiple of 12.6 and an EV to EBITDA multiple of 12.2. By comparison, using data from the 2021 fiscal year, these multiples would be 10.9 and 9.4, respectively. When I wrote my last article, I did not look at 2022 estimates. But for context, using the 2021 figures, these multiples were 8.9 and 8.8, respectively. As part of my analysis, I did also compare the company to five similar restaurant operators. On a price to operating cash flow basis, these companies ranged from a low of 5.1 to a high of 10. And when it comes to the EV to EBITDA approach, the range was from 6 to 10.8. In both cases, The Cheesecake Factory was the most expensive of the group.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| The Cheesecake Factory | 12.6 | 12.2 |

| Bloomin’ Brands (BLMN) | 5.9 | 7.9 |

| Dave & Buster’s Entertainment (PLAY) | 5.2 | 8.5 |

| Jack in the Box (JACK) | 10.0 | 10.8 |

| Arcos Dorados Holdings (ARCO) | 5.1 | 6.0 |

| Brinker International (EAT) | 7.1 | 9.4 |

Takeaway

Based on the data at my disposal today, it seems as though The Cheesecake Factory has done its job as a ‘buy’ candidate in my book. And that job was to outperform the broader market. Having said that, I do believe that a downgrade to a ‘hold’ rating is appropriate at this time. The stock has gotten more expensive on an absolute basis, plus it is now pricey relative to similar firms. Add on top of this the fact that bottom line results are deteriorating, and I have a hard time believing that further outperformance can be on the table until the uncertainty about all of this is mitigated. All combined, the ‘hold’ rating just makes a lot more sense right now.

Be the first to comment