It’s time to talk about one of the most annoying stocks in my portfolio: The Andersons (NASDAQ:ANDE). This agriculture giant has been one of my best performers since the agriculture bottom of 2020. Yet, it has run into resistance. It had issues with crop margins last quarter and now traders are selling the stock because of weak energy prices. I believe this is a mistake as energy prices are to remain high, providing a basis for strong earnings in ethanol and related crops like corn. The Andersons is now trading at a very attractive valuation, benefiting from a longer-term tailwind, and favorable political developments.

In this article, I’m going to update my The Andersons’ bull case.

So, bear with me!

Agriculture & Energy

When it comes to commodities there are a few key themes I have discussed in recent weeks. I added an article to each theme for more background info.

Accelerating global natural gas demand yet not enough supply – article

The pressure on oil supply, causing oil prices to remain elevated – article

Global net-zero efforts are hitting metal shortages – article

Agriculture commodities remain in a strong bull market – article

All issues above are somewhere related, yet only the metals one doesn’t apply here.

As I will discuss in this article, The Andersons isn’t just an agriculture play but the company is increasingly tied to energy. Agriculture and energy are two highly-correlated industries for many reasons.

Agriculture requires energy as an important input to production. Agriculture uses energy directly as fuel or electricity to operate machinery and equipment, to heat or cool buildings, and for lighting on the farm, and indirectly in the fertilizers and chemicals produced off the farm.

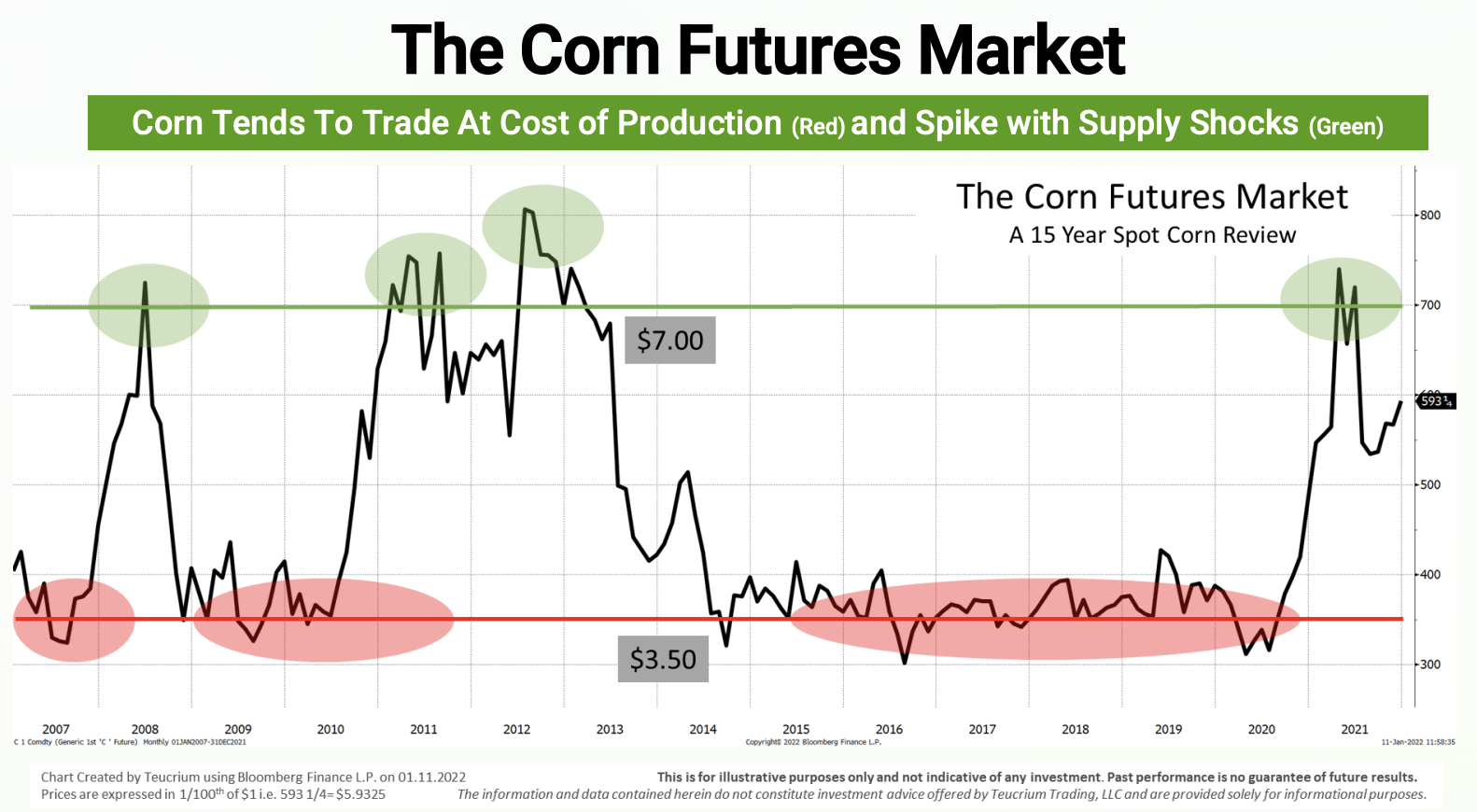

Energy is the main driver of crop production costs, which mainly determines where crop prices trade outside of supply shocks.

Teucrium

With that said, corn is the number one grown crop in the US. It is not only food for animals, but a feedstock for ethanol plants producing (you guessed it) ethanol. That’s an energy commodity. Roughly a third of US corn is processed into ethanol at some point.

And speaking of ethanol, The Andersons are huge in ethanol.

The Andersons & Energy

The Andersons is a large ethanol producer. As I wrote in an article on April 16, 2022:

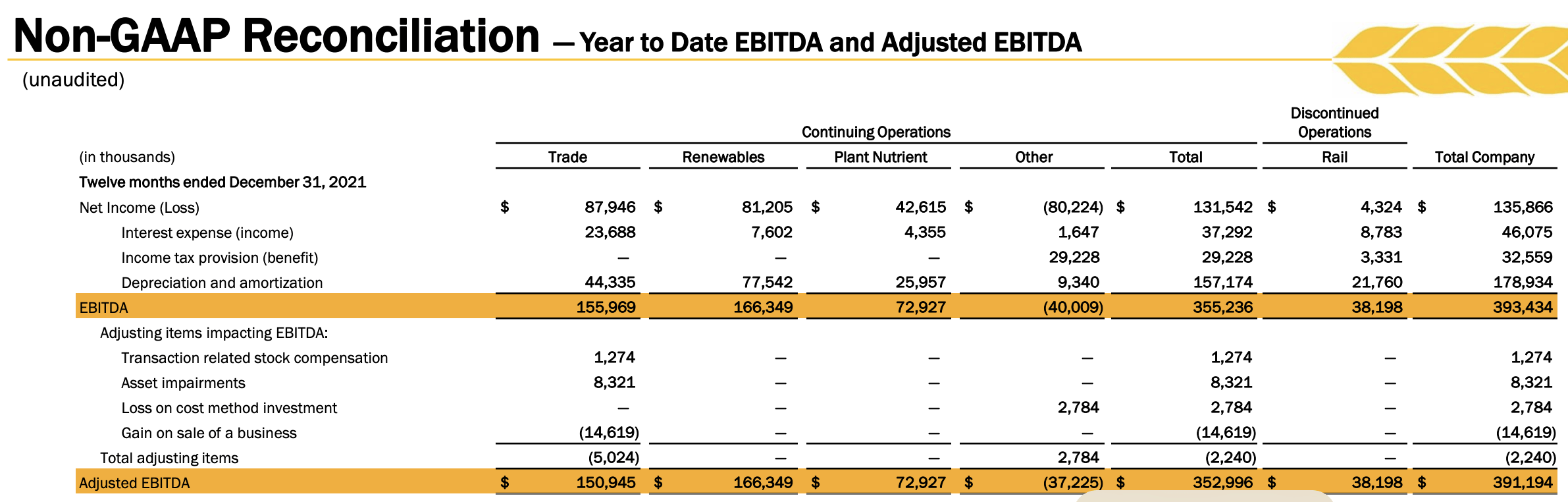

“In 2021, the ethanol/renewable segment did roughly $166 million in adjusted EBITDA. That’s 47% of the total adjusted EBITDA. And again, other segments also benefit from strong ethanol production as it’s more or less the backbone of the US agriculture industry. This is what the company commented on that:

We think we can play an interesting position. We’re a little bit of a unique company in that we have a fertilizer business and we work closely at the farm with the fertilizer inputs with growers and our grain buyer and an ethanol producer, so we work across the whole chain to the end market. So we think there’s opportunities there.

The Andersons

As a result of the merger, the Company and Marathon Petroleum Corporation (“Marathon”) own 50.1% and 49.9% of TAMH equity, respectively. The transaction resulted in the consolidation of TAMH’s results in the Company’s financial statements effective October 1, 2019. […] The four ethanol plants within TAMH are located in Iowa, Indiana, Michigan, and Ohio. These plants have a combined production capacity of 480 million gallons of ethanol, with a nameplate capacity of 405 million gallons.

The Company also owns 51% of ELEMENT, LLC (“ELEMENT”), and ICM, Inc. (“ICM”) owns the remaining 49% interest. In 2019, ELEMENT completed the construction of a 70 million-gallon-per-year bio-refinery in Kansas which began limited production in the third quarter of 2019. ICM managed the initial construction of the facility, while the Company operates the facility under a management contract, and provides corn origination, ethanol marketing, and risk management services.”

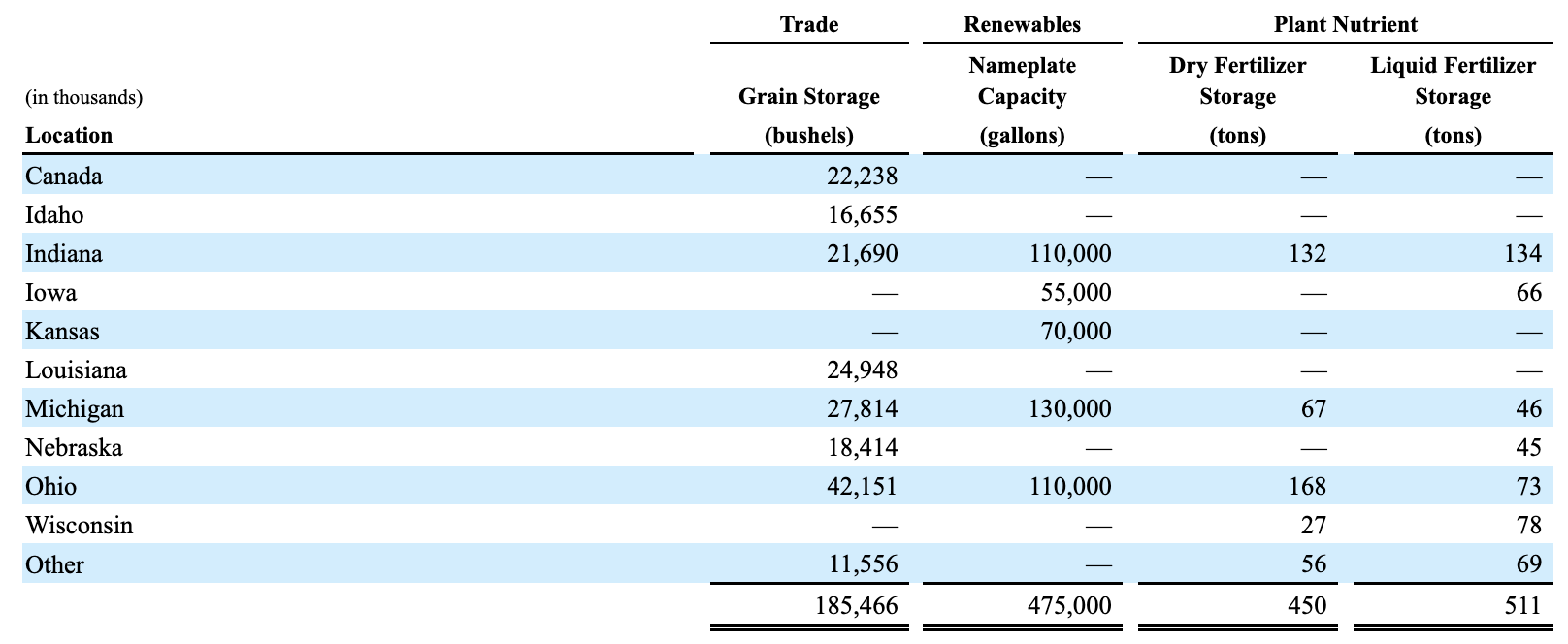

The table below shows the company’s renewable locations including production capacity.

The Andersons/SEC

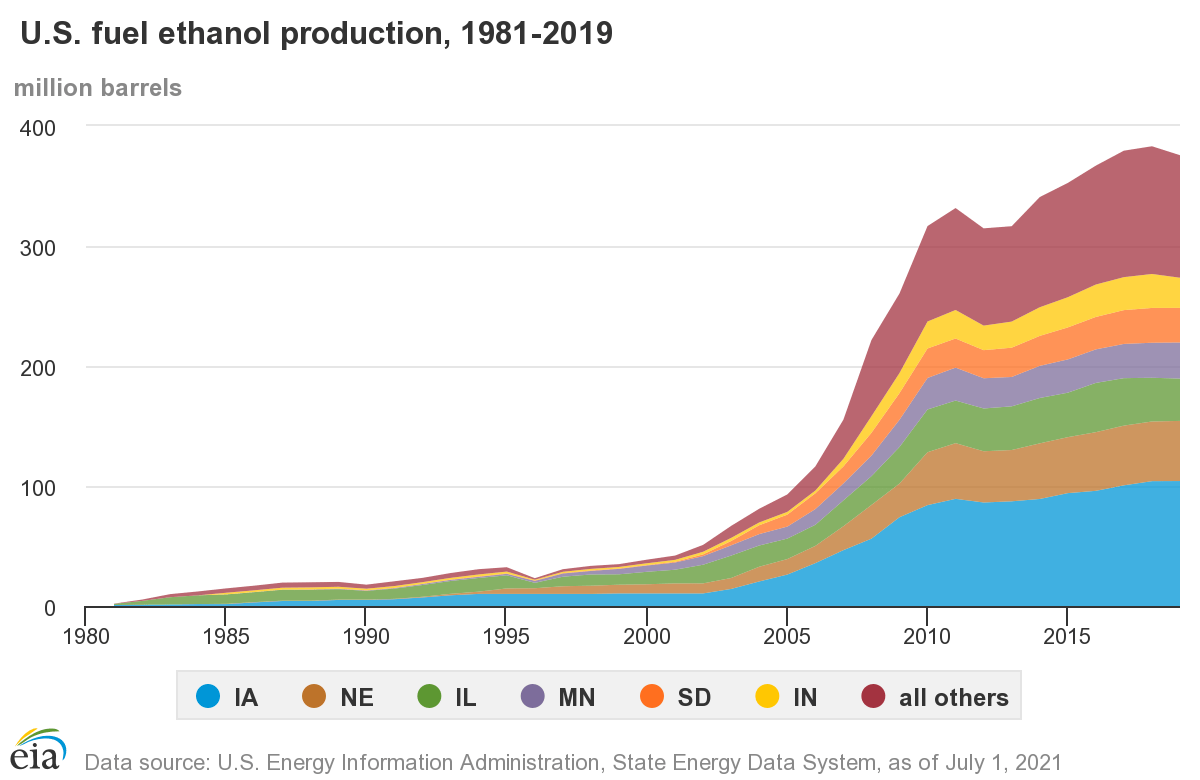

If my math is correct, The Andersons produced 3.2% of total ethanol production in the US in 2021 based on 475 million gallons of capacity (assuming 100% utilization for the sake of this quick calculation) and domestic production of 15 billion gallons.

This is what domestic ethanol production looks like:

EIA

Production has peaked. The same goes for the production of oil and gas. This is very inflationary.

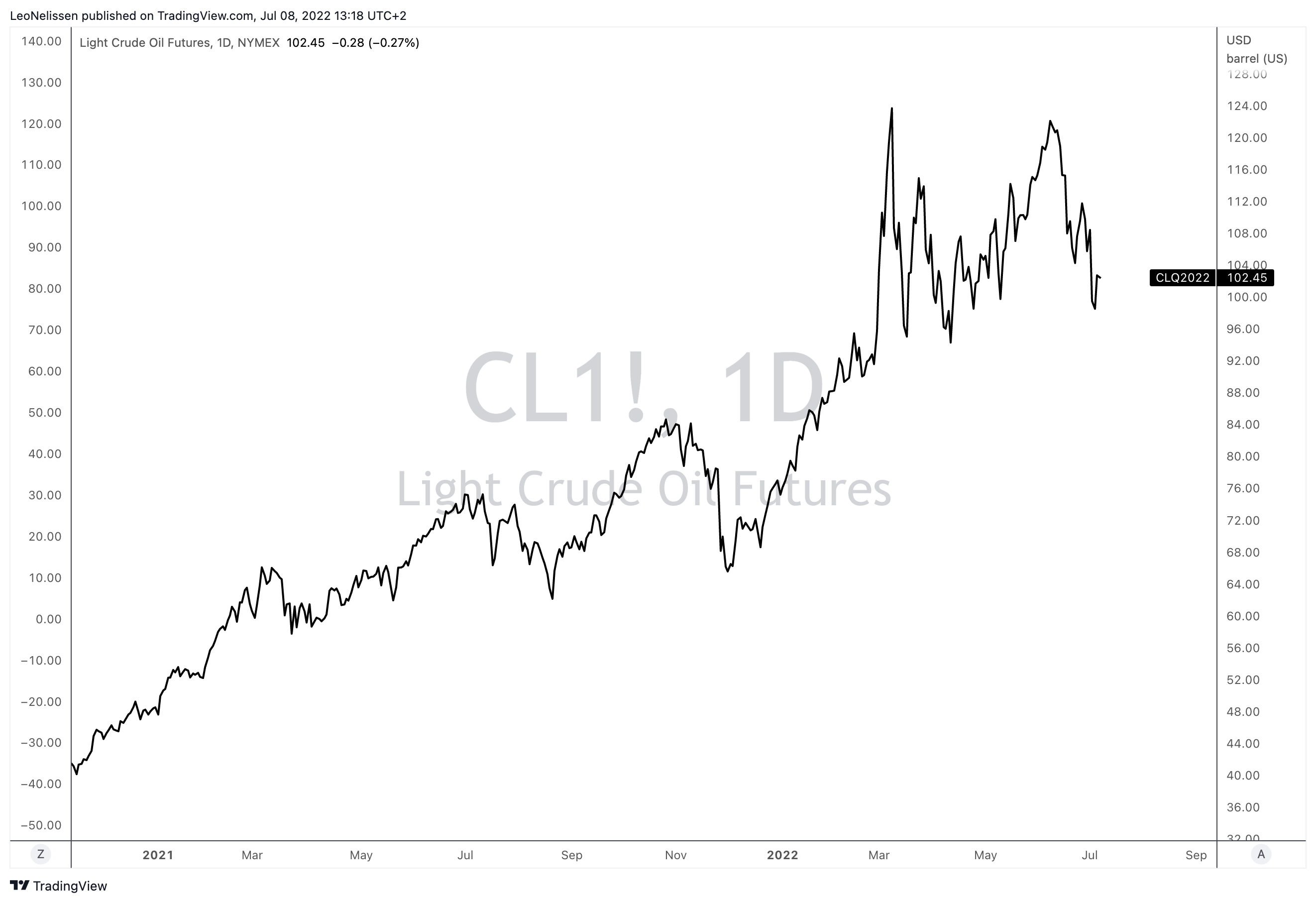

With that said, energy has suffered lately as oil prices fell back below $100 (both Brent and WTI).

TradingView (WTI Crude)

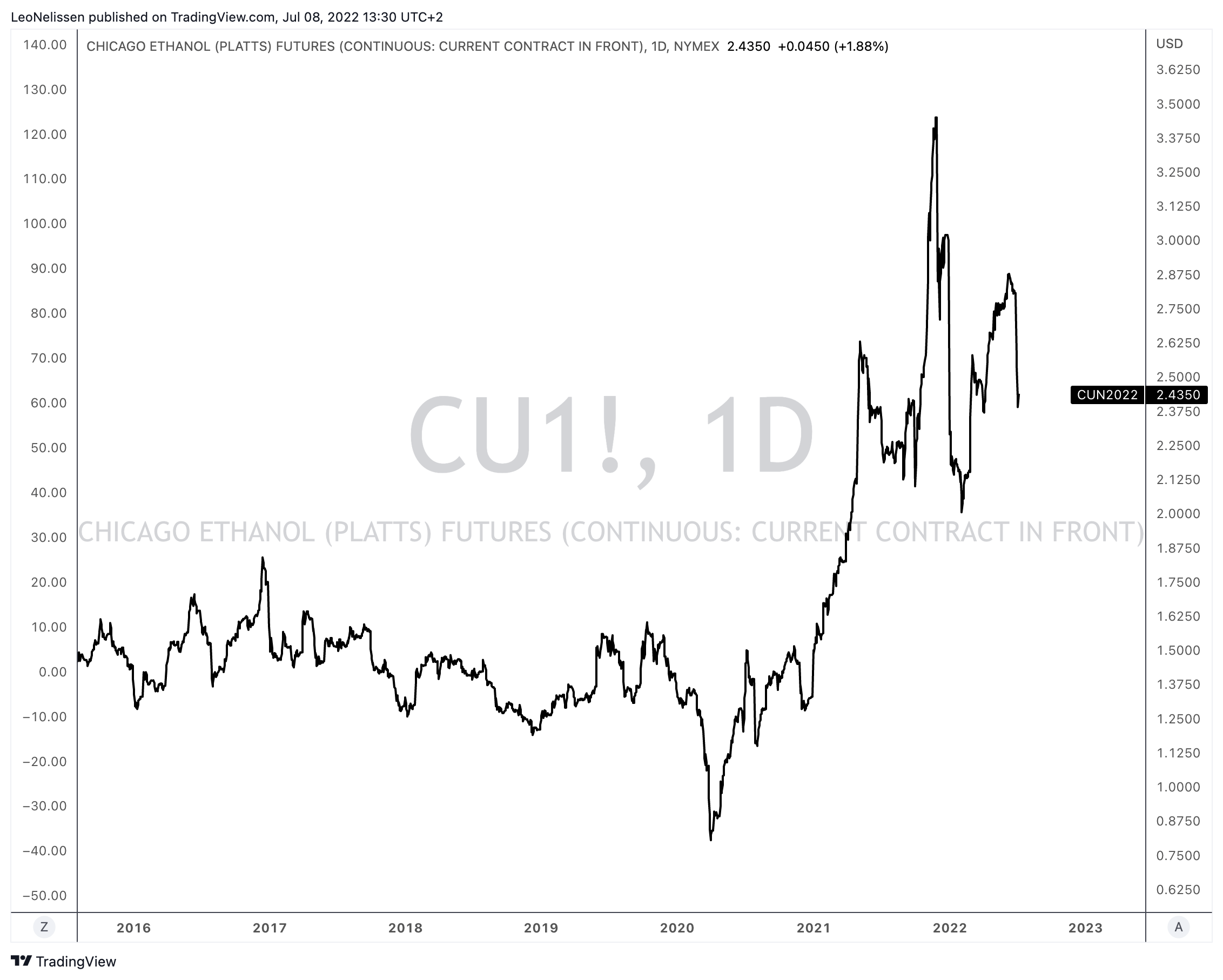

Ethanol prices continue to be steady at $2.16 per gallon, which is down from 2021 highs but well above anything we’ve seen in the years prior to the pandemic.

TradingView (Ethanol futures)

This has something to do with high demand as ethanol blending requirements have been raised to offset high gas prices as a just-released Wall Street Journal article reports:

Several agencies at the state and federal levels have taken measures to slow increasing prices. Some states have suspended their gas taxes. The U.S. Environmental Protection Agency issued an emergency waiver in April that allows gas stations to sell high-ethanol content gasoline this summer, despite concerns about increasing air-polluting emissions.

The biggest headwind for ethanol is lower gasoline demand, which is unlikely as Biden has called for a three-month suspension of federal gasoline and diesel taxes on June 22, which I believe is a major reason supporting ethanol demand/prices.

With that said, the ANDE bull case is intact but frustrating. First, the stock imploded after its 1Q22 earnings results. These results were fine, in general, but the company ran into headwinds related to price differences (the basis):

The significant run-up in commodity prices resulting from the conflict in Ukraine and the smaller South American crop caused a dramatic drop in basis values, primarily in corn and soybeans. While the lower basis values allowed us to buy new bushels at favorable basis levels, existing domestic positions experienced large basis reductions, which impacted first-quarter results.

After that, the company sold off further as energy prices came down – causing investors and traders to dump everything related to energy.

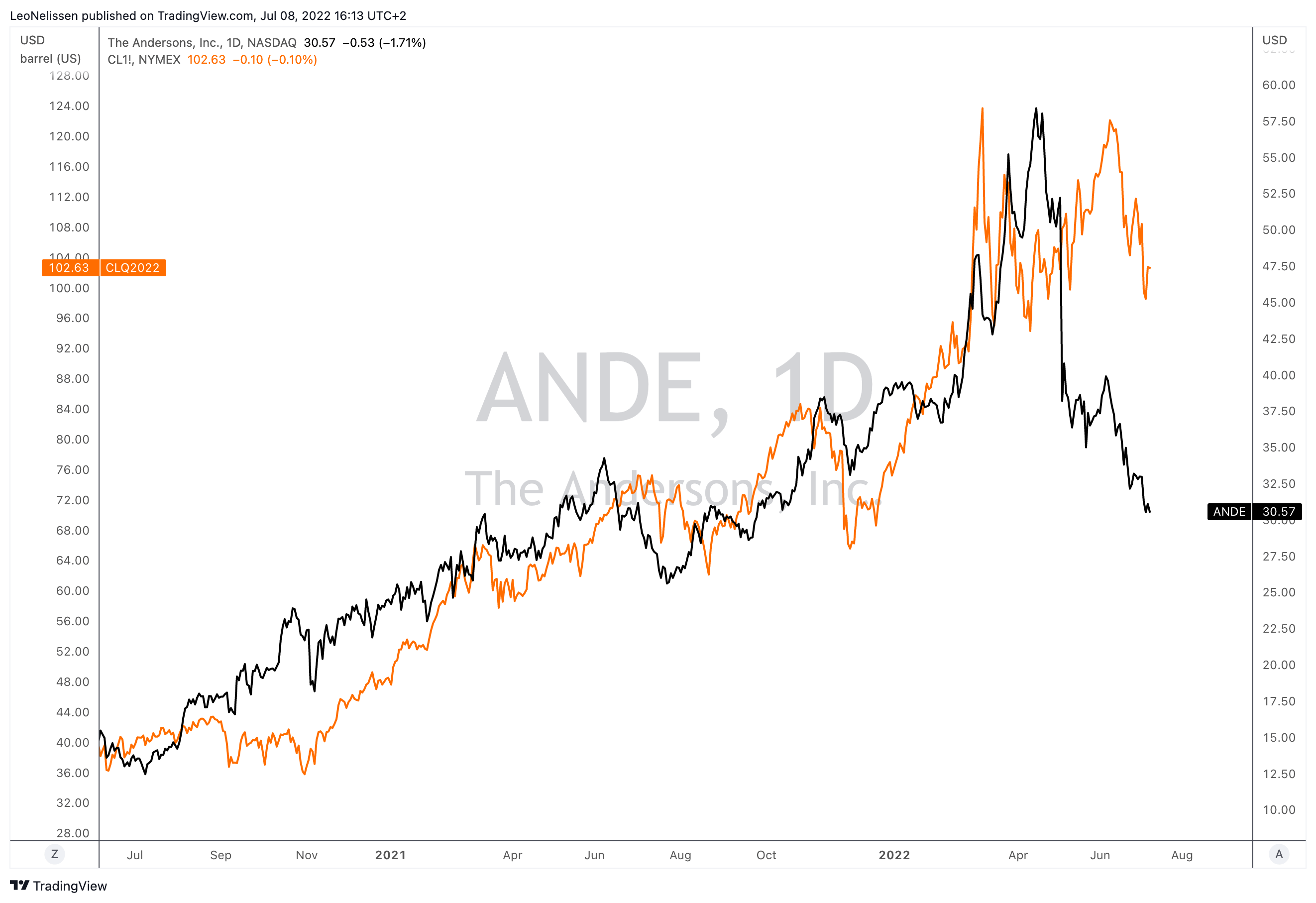

Note how well ANDE and the price of oil moved together prior to its 1Q22 results.

TradingView (Orange = WTI oil, Black = ANDE)

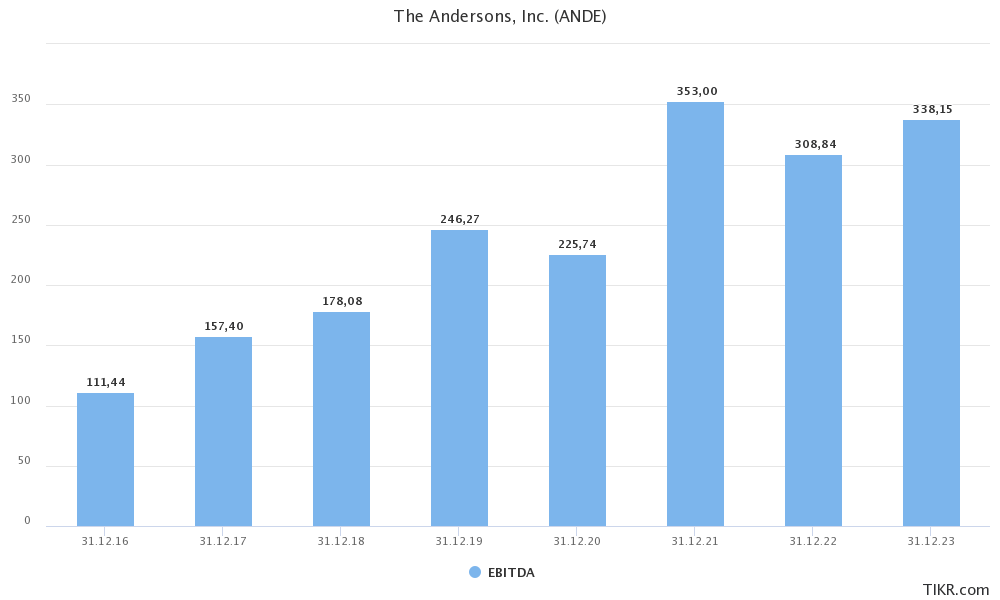

So far, 2022 EBITDA estimates have fallen by only $4 million. 2023 EBITDA estimates have gone up by $2 million since my most recent article. I believe that makes sense. ANDE’s earnings power remains fantastic and I believe that higher grain volumes compared to 2021 (better yields) will further boost its bottom line.

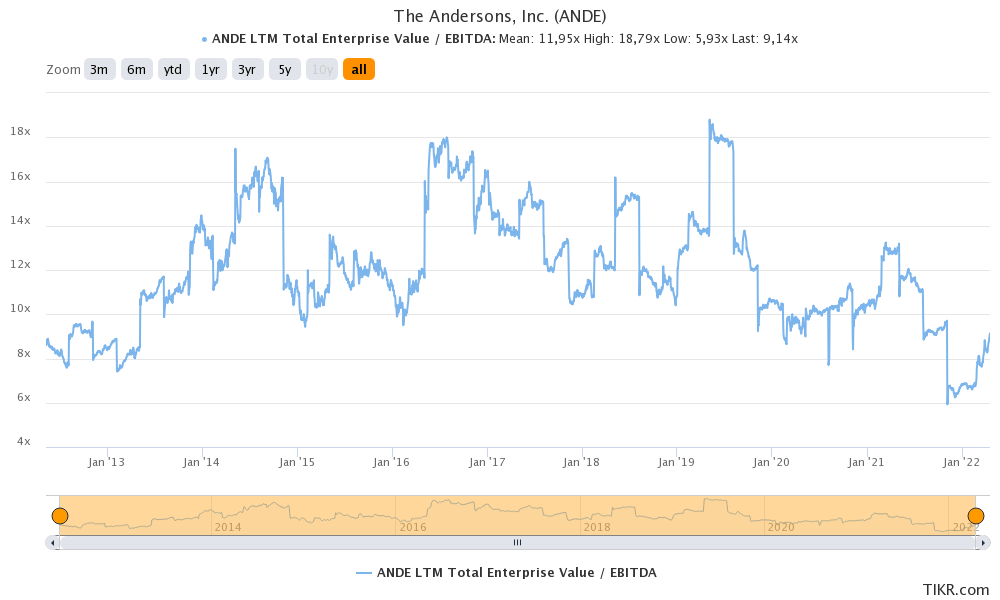

TIKR.com

With that said, the company is trading at 7.6x EBITDA if I incorporate all needed liabilities and market cap. This includes the $1.06 billion market cap, $1.2 billion in expected 2023 net debt (roughly 3.8x EBITDA), $230 million in minority interest (tied to its ethanol joint venture), and a mere $25 million in pension-related liabilities. I used $330 million in EBITDA as that is the base case of what the company can do in this environment.

TIKR.com

This valuation is too cheap as investors are pricing in a decline in sentiment and agriculture prices on a longer-term basis. I don’t see that happening.

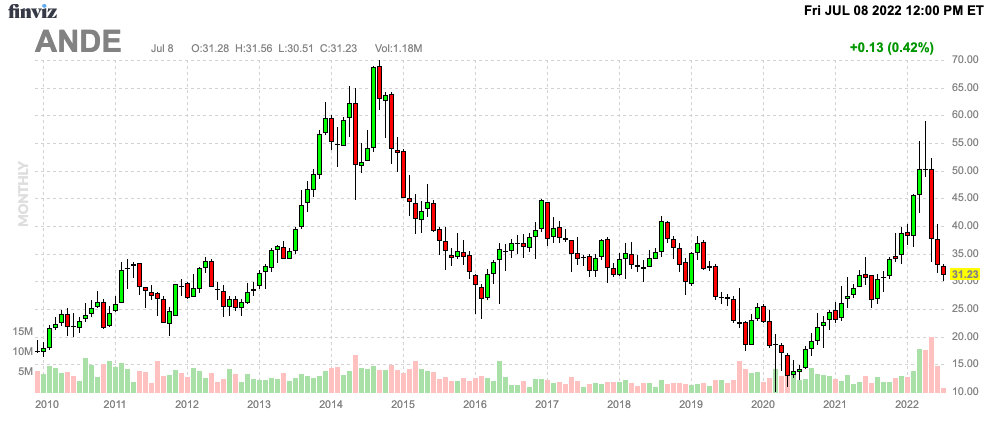

Hence, I stick to my fair value of $65-70. However, as I said in my prior article, we’re more than likely not getting there this year. I hope to see a rebound towards $45 this year followed by a move to my target by the end of 2023.

FINVIZ

The biggest risk is demand risk. The most recent decline in oil was triggered by traders who started to price in a recession. If demand weakens, ANDE may hover between $20 and $40 on a prolonged basis.

Takeaway

The Andersons’ stock price is down 20% after a stellar start. The company first suffered from pricing issues in 1Q22 followed by weakness in energy commodities. The good news is that energy continues to benefit from a strong tailwind. Supply is tight, demand is strong. This is helping ethanol prices and volumes.

The Andersons is a major producer of ethanol, which has helped EBITDA estimates despite its first-quarter issues.

Moreover, agriculture commodities, in general, are likely to remain in a long-term uptrend. Production costs are high, weather-related factors are pressuring supply, and demand continues to be strong.

Hence, I believe that The Andersons is significantly undervalued, offering opportunities for both agriculture- and energy-focused investors.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment