jetcityimage/iStock Editorial via Getty Images

Growth stocks that were left for dead earlier this year have suddenly roared back to life. Whether that move sticks or not is still up for debate, with rates moving wildly and the prospect of at least a mild recession looming. However, what we have today is very strong up moves in growth leaders, which must be respected regardless of your view on the outlook for the rest of the year.

One such growth leader is Tesla (NASDAQ:TSLA), which is up almost 60% since the bottom it made just over a month ago.

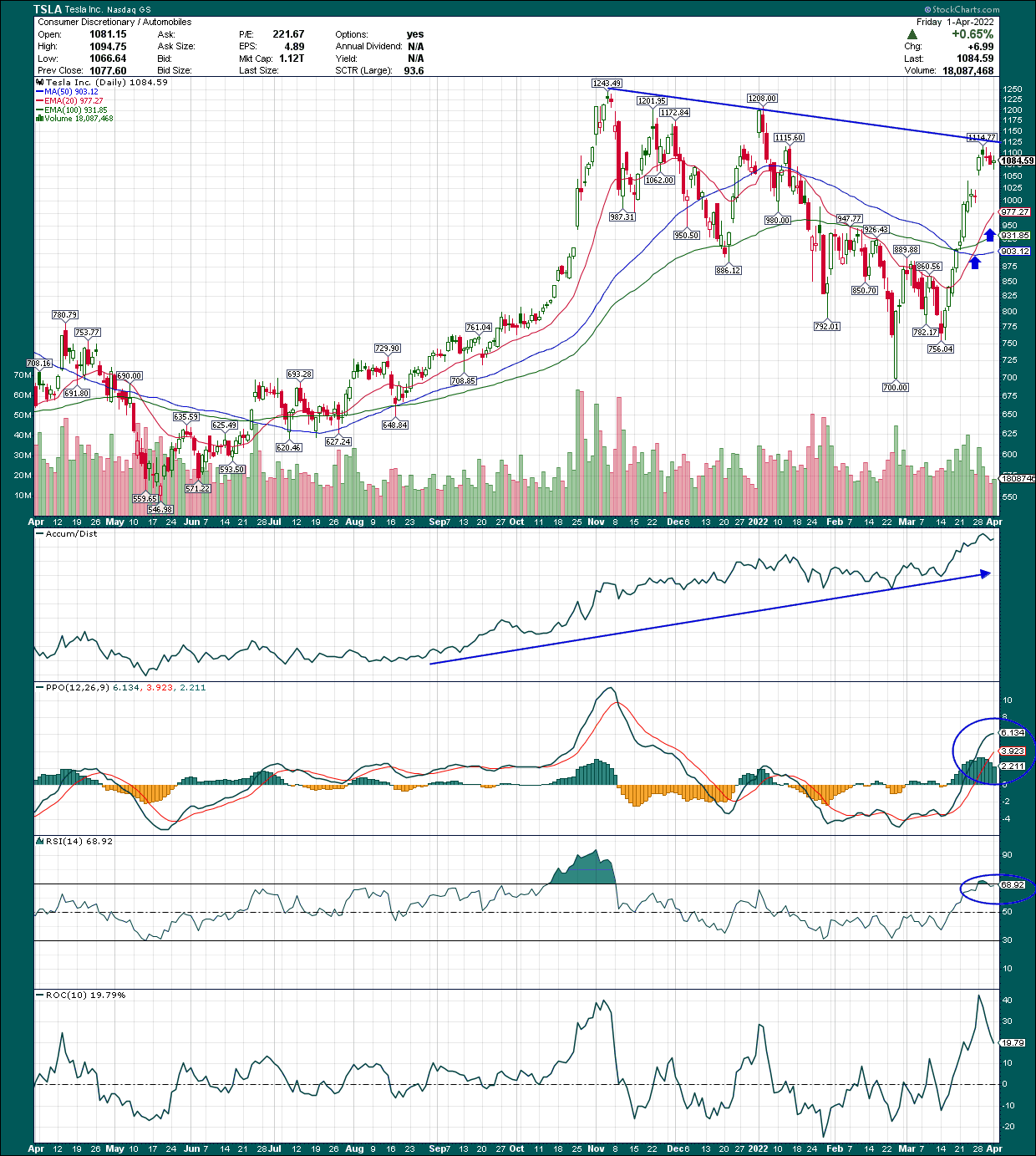

StockCharts

The daily chart shows a downtrend line from the ATH that was made late last year, and which proved to be resistance in the past few trading days. I don’t believe this will be a persistent issue for Tesla, but is something that could cause a temporary delay in the rally. Once Tesla clears that downtrend line, next resistance is the prior relative high at $1,200, and then finally, the ATH near $1,250. Tesla will crest those, I believe; it is just a matter of when.

The accumulation/distribution line remains tremendously strong and is at its own all-time high, indicating this rally is once again the real deal. That’s not surprising given Tesla’s prior leadership, but it’s good to see nonetheless.

The PPO made its way well into bullish territory, which is a great sign for the long-term health of this bull run. It’s pulling back slightly now but remember we saw a nearly 60% move in the space of a few weeks, so it needs to come back a bit. Moves like this in the PPO show very strong bullish momentum that portends more strength in the weeks ahead.

The same is true of the 14-day RSI, which reached overbought territory. That’s yet another bullish sign that shows buying momentum is strong, and after a consolidation/pullback, I fully expect this move to continue.

Let’s now briefly look at the weekly chart, because I think there’s further proof we’re closer to the beginning of this rally than the end.

StockCharts

The weekly PPO recently tested the centerline after being overbought for some time, and has turned higher. The last time this happened, the stock ran from just over $500 to its ATH at $1,243. That doesn’t guarantee the same sort of thing this time, but it definitely helps. Big transitions like this in weekly charts often portend bigger, longer-term moves, and that’s what I think we’re seeing in Tesla right now.

Now, Tesla is in process of splitting its stock (again), a move that catalyzed the move to the ATH last year. Investors love a stock split and this is either a bullish catalyst, or no catalyst at all. In other words, the split will either produce further rallying from FOMO’ing investors, or it won’t change anything; it’s not a negative catalyst. I personally don’t understand the obsession with buying splitting stocks because the actual impact to shareholders is nothing, but as I mentioned, splitting kicked off a massive rally last year, and it could do the same this time around.

In addition, Tesla is due to report earnings in about three weeks, and the stock tends to rally into earnings. What happens after the report comes out is another matter, but there is a good chance this buying continues through the end of April, as Tesla is due out with earnings on the 26th.

To be clear, the split and the earnings date are not part of the core bullish thesis here, but they are key short-term catalysts that could keep the stock afloat in the weeks ahead.

Tesla keeps delivering

The reason Tesla has delivered world-beating returns over the years is because, well, its business has been unbelievably strong. You don’t reach a trillion dollar valuation through luck, and the fact is that Tesla continues to outpace its competition.

Seeking Alpha

Revenue revisions have been a bit choppy, but over time, they go higher. Despite the fact that we’ve seen meteoric rises in revenue over the years, trend is still higher. This is what you want/need from growth stocks that you own, because the second revenue estimates begin to roll over, the stock price will follow suit. That’s why Tesla is volatile, and that volatility will remain for the foreseeable future. However, if you can stomach the up and down moves, you stand to do well over time.

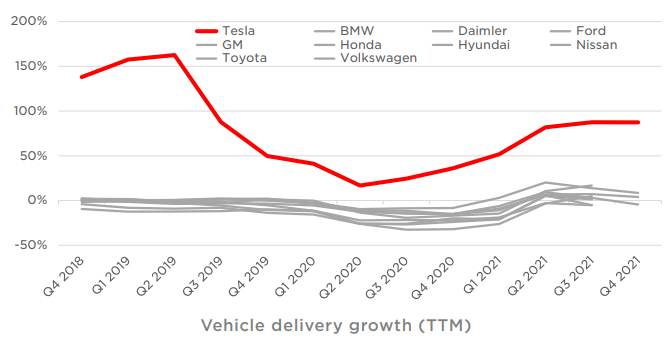

Tesla’s specific growth catalysts are tied to vehicle production, which it has continued to ramp over time. The company has facilities in Germany, China, and the US pumping out vehicles at ever-increasing rates, and that’s because Tesla continues to ramp production to meet ramping demand. As the company can decrease the cost of production per unit, it can either lower prices, or keep more revenue as operating profit. As we can see below, Tesla’s growth rate continues to blow past the competition globally, and as long as this is the case, Tesla’s share price will almost certainly move higher.

Investor presentation

If anyone needs a reason why Tesla is valued so highly against other automakers, I believe this one chart here is all you need to understand. When a company is so dominant, the share price follows, and Tesla isn’t any different.

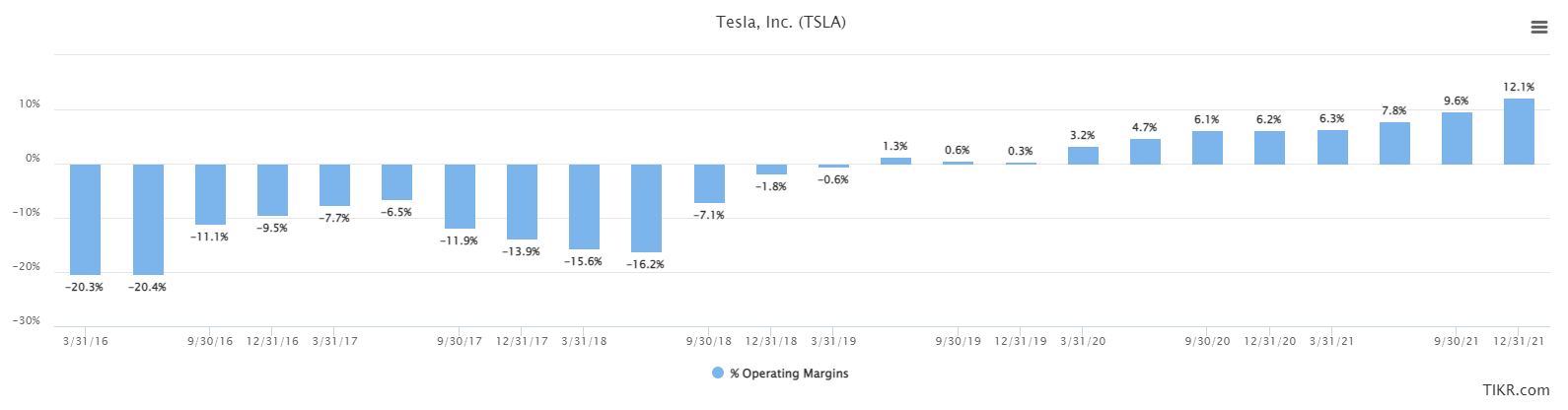

Now, I mentioned operating profits, which Tesla has done an exemplary job of improving in recent quarters after so many years of losses. Below we have trailing-twelve-months, or TTM, operating profits as a percentage of revenue.

TIKR

We know Tesla has world-beating gross margins on its cars and services, but up until a couple of years ago, that margin was spent on relatively inefficient production. Production is much more efficient now, thanks to the ramping of new factories built to produce a lot of vehicles at lower costs, and the growth in operating margins has been nothing short of outstanding.

These are the kinds of margins the likes of the Big 3 and European automakers would drool over, but Tesla is doing it, with further improvements likely ahead.

Operating margin growth is subject to continued growth rates in vehicle production, which lowers per-unit costs, which will be offset somewhat by rising SG&A costs, as well as input cost inflation. Batteries in particular take a lot of expensive raw materials, and with supply chain shortages and geopolitical risk of some of these commodities, Tesla isn’t immune to input cost shocks from time to time. However, on the whole, it’s employing a tried and true strategy of boosting production to lower per-unit costs, and I don’t see input cost inflation as a big derailer at the moment.

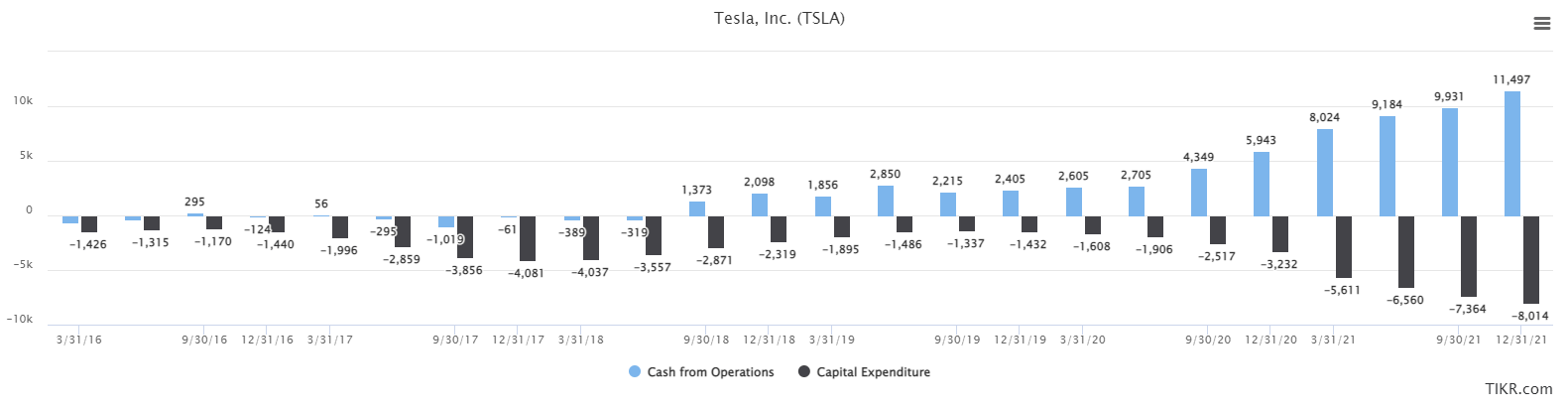

Let’s now take a look at cash flow, because for many years, Tesla was cash flow negative, which created nearly constant financing issues. However, positive operating profits have fixed that issue, as we’ll see below with TTM operating cash flow and capex, both in millions of dollars.

TIKR

The growth here has been exponential, and what’s interesting is that Tesla is not sitting back and collecting this new found cash; it is investing most of it. Capex was $8 billion in the TTM period, against operating cash flow of $11.5 billion, so Tesla is investing heavily in future growth while funding its operations. While that sounds like a given, for many years the company was unable to do this, and issued a huge amount of stock to fund operations. That was a headwind for shareholders, but I do think that headwind has well and truly gone.

Below we have the share count and the YoY change for the past several years to see what I’m on about.

TIKR

You can see some pretty massive moves in the share count over time, but the past few quarters have seen essentially no movement in the share count. For a company with a history of diluting shareholders, you cannot really say investors are out of the woods entirely. However, because Tesla has ample cash flow to invest in the business and run its operations, you have to say the incentive for Tesla to issue more shares is certainly reduced. This isn’t a tailwind for the stock, but it does effectively remove a headwind, which is sort of the same thing.

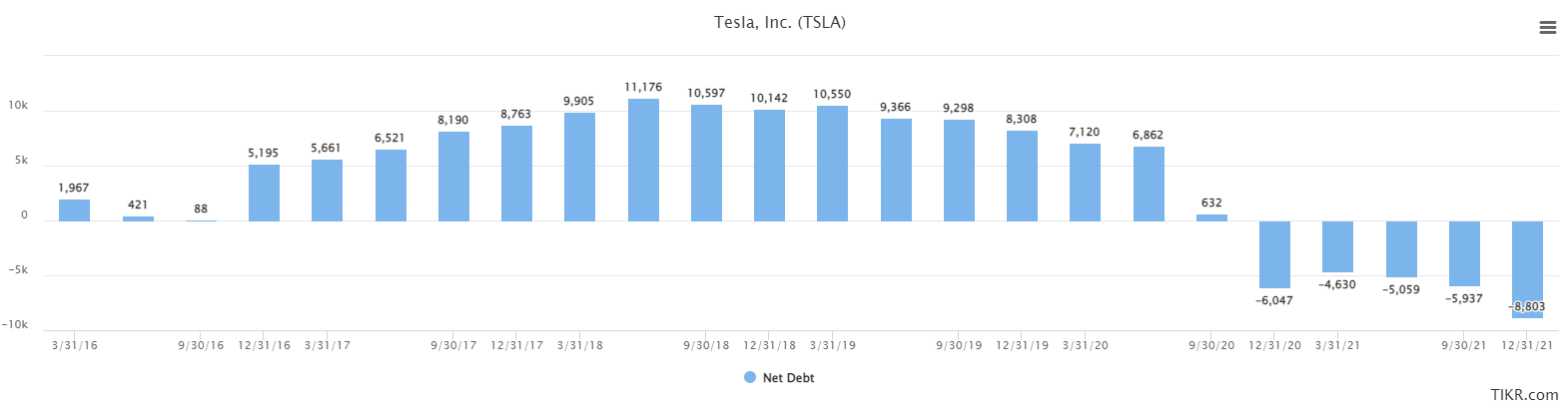

Indeed, this set of conditions has enormously improved Tesla’s balance sheet, which we can measure via net debt, which is below in millions of dollars.

TIKR

Net debt is negative, meaning Tesla has more cash than obligations by almost $9 billion. That gives it supreme financial flexibility, which should scare competitors. Tesla was always hindered by its lack of financial flexibility, but that is no longer the case, and it can do essentially whatever it needs to do in order to compete and win.

Squint to see the value

Of course, valuing a stock like this takes some faith because you’re buying a stream of future growth that may or may not occur. In Tesla’s case, I believe it is doing everything it needs to do to win in the future, but there are risks that it may not be able to overcome. We’ll get to that in a second, but for now, let’s take a look at earnings and the valuation to see what’s what.

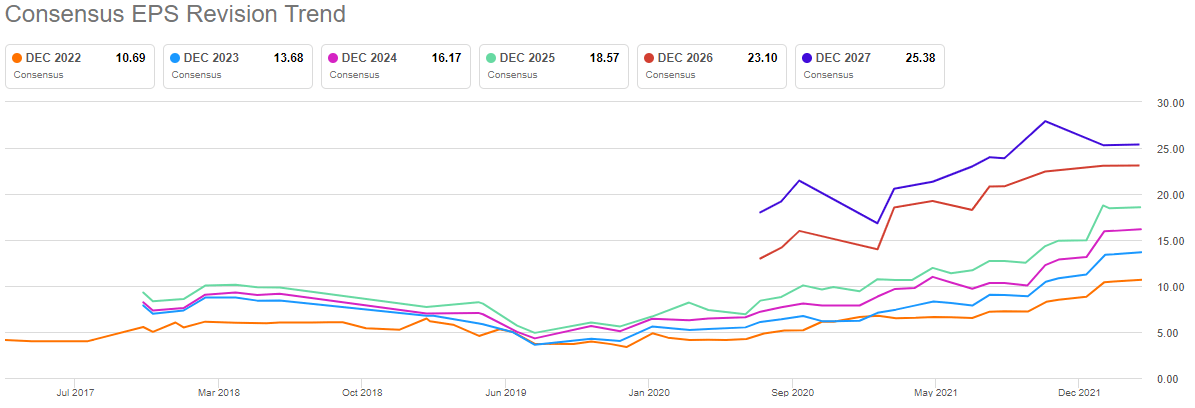

Seeking Alpha

EPS revisions remain very strong, which you’d expect given the company’s ramping revenue and soaring profit margins. This virtuous cycle is incredibly lucrative for shareholders, and you can see the product of it above. As long as these lines move up and to the right, Tesla shares should do very well. I have zero concerns about this and I believe EPS revisions support an ever-higher share price.

Now, let’s take a look at the valuation, which we can use price-to-sales for; it’s plotted below.

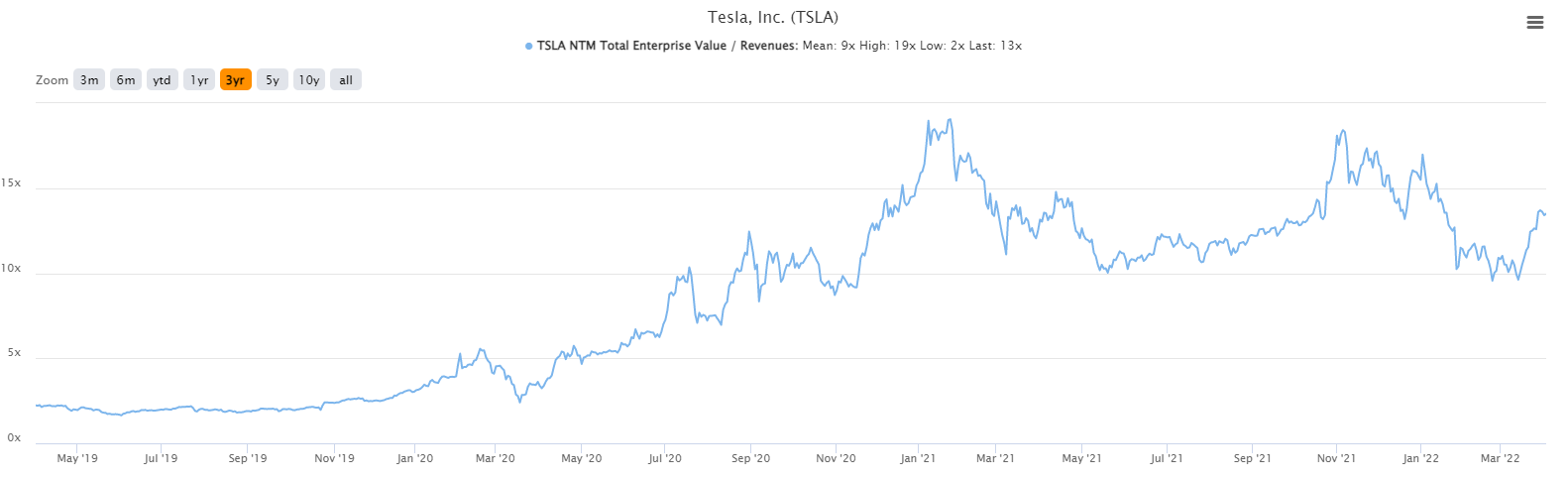

TIKR

This stock is never going to be “cheap” in the traditional sense; it’s a disruptor in a gargantuan industry with world-beating growth rates. Thus, comparing it to the old-world manufacturers is useless, but we can compare it to its own history. Shares go for 13X forward sales today, which is somewhat elevated against its historical mean. The stock has been 15X forward sales or better a handful of times, but the point here is that Tesla looks pretty fairly valued to me. I don’t think it’s particularly cheap right now, which raises the risk of a consolidation or pullback to help with the valuation.

One thing that’s very clear to me is that if Tesla pulls back to 10X or 11X sales, it’s a screaming buy. The times that has happened in the past were outstanding buying chances, with the most recent one being its trip to $700 earlier this year. Something to keep in mind going forward but for now, the stock looks fairly valued to me.

Risks and final thoughts

The valuation is one risk, because Tesla is much closer to the top of its historical valuation range than the bottom. That doesn’t mean it absolutely has to revisit 10X forward sales, but the point is that I think valuation expansion from here is likely limited for the time being. That increases the risk to the bulls.

In addition, input cost inflation is a real threat to margins. It shouldn’t impact unit sales – unless raw materials simply become unavailable – but it is already impacting operating margins, and certainly could in the months to come. I believe the company can raise prices and/or offset some of this with manufacturing efficiencies, but input cost inflation is largely out of Tesla’s control, and is a risk to consider if you’re bullish.

While I noted share issuances have decreased enormously in the past few quarters, Tesla has proven it is willing to use its stock as an ATM in the past, and that could certainly be the case going forward. Employee compensation and share issuances for corporate purposes could drive the share count ever higher over time, which dilutes shareholders, and makes it more difficult for the price to move higher.

Finally, the biggest risk to Tesla is that unit sales rates fall off of their current trajectory. An automaker with a valuation of 13X forward sales is pricing in a huge amount of future growth. I don’t believe we have any reason to think we won’t see that growth, given Tesla’s history of delivering. However, it is possible the growth trajectory doesn’t meet expectations, and the share price would suffer if this were to occur. In fact, Q1 deliveries were a bit light against expectations, so it’s a real risk.

Despite all of this, I still think Tesla has ample room to grow in the years to come, and I think the share price will ultimately go much higher. We’ve had a massive move in the past few weeks, and the stock looks fairly valued, so it wouldn’t be unusual to see a consolidation or pullback. However, any such event would be a chance to buy, and I’m quite bullish on Tesla despite its big move.

Be the first to comment