MarsBars

Financial stocks have had a hard time catching a break over the past year, with many names down materially over the past year. While there are short-term headwinds for this sector, savvy investors know that the time to buy cyclical industries is when market sentiment is working against them.

This brings me to Synchrony Financial (NYSE:SYF), which as shown below, has seen a 31% decline in its stock price over the past 12 months. At the current price of $32.80, SYF is trading far closer to its 52-week low than its 52-week high of $50. This article highlights why now may be a great time for value investors to layer into the stock.

SYF Stock (Seeking Alpha)

Why SYF?

Synchrony is a well-respected consumer financial services company that was spun off from General Electric (GE) back in 2015. Its offerings include innovative consumer banking products across key industries including digital, retail, home, auto, travel, and health. It’s also one of the largest issuers of private label and co-branded credit cards in the U.S.

One of the key strengths of Synchrony Financial is its partnerships with major retailers and e-commerce companies. The company has private label credit card agreements with more than 300 partners, including major brands such as Amazon (AMZN), eBay (EBAY), and PayPal (PYPL). These partnerships provide Synchrony Financial with a steady stream of revenue and have helped to drive growth in recent years.

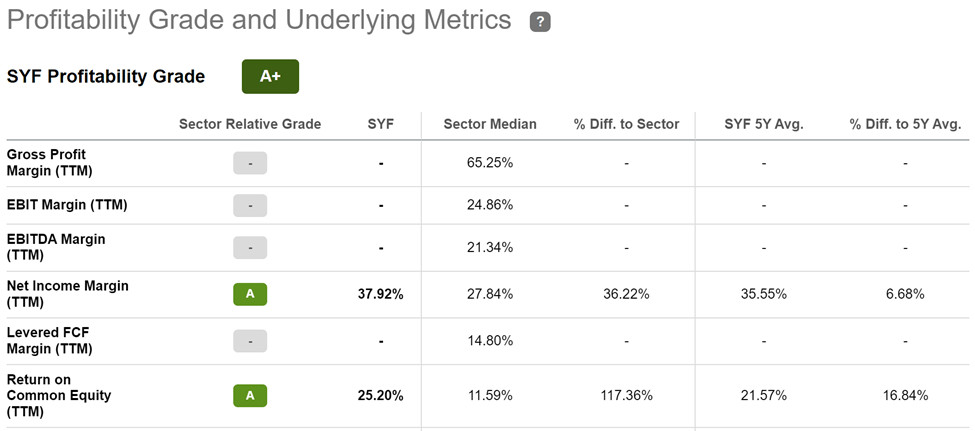

This wide-reaching platform and scale enables it to earn above average margins relative to its sector. As shown below, SYF scores an A+ grade for profitability, driven by strong Net Income Margin and return on equity of 38% and 25%, respectively.

SYF Profitability (Seeking Alpha)

Notably, SYF also carries a very strong efficiency ratio, which is calculated by total operating expenses divided by revenue. Its efficiency ratio stood at 36.5% as of the end of the third quarter, which is much lower than the ~50% average for most banks, and marks a 220 basis point YoY improvement. It also has a strong balance sheet, with a 14.3% common equity tier 1 ratio, sitting well above the required 4.5% for large banks.

Meanwhile, SYF is seeing overall strong results. While average active accounts declined by 1.3% YoY to 66.3 million during the third quarter, consumer spending remained strong with purchase volume increasing by 6% YoY to $44.6 billion. Moreover, average balance per account rose by 8% and the higher receivables resulted in net interest income growing by 7% to $3.9 billion.

Risks to SYF include the potential for a recession, which may hamper consumer spending and if unemployment goes up, that may impact borrowers’ ability to repay their loans. It appears that management is preparing for these potential headwinds, as it has added $294 million to its reserve build this year, bringing the total provision for credit losses to $929 million. SYF also maintains strong total liquidity, which amounts to $20.3 million including undrawn credit facilities. This equates to 20% of its total assets and is consistent with 2021-levels.

Management also highlighted its risk mitigation practices with respect to consumer credit. This is driven by its big data expertise in combining account information with external information enabling better credit decisions, as highlighted by during the last conference call:

Once our customers begin utilizing our credit products, Synchrony leverages real-time indicators to monitor any shifts in our borrowers’ financial well-being, from transaction and payment behavior characteristics to credit bureau alerts.

We are closely in tune with our customers and can make both account and portfolio level adjustments quickly. And of course, Synchrony’s responsive digital capabilities are complemented by our fully scaled, highly experienced servicing teams to ensure that our customers have appropriate support when they need it.

In short, Synchrony’s dynamic technology platform is what powers our ability to have a finger on the pulse of each customer and harness the data into actionable insights so that we can optimize the outcomes for all stakeholders. We are able to say yes to more customers, more consistently and for the same level of risk even as market conditions change.

Meanwhile, SYF remains a cash rich business, enabling it to return $1.1 billion in capital to shareholders during the last reported quarter, with $950 million of that being in the form of share buybacks. Plus, while SYF’s 2.8% dividend yield is low, it’s very well covered by a 14% payout ratio.

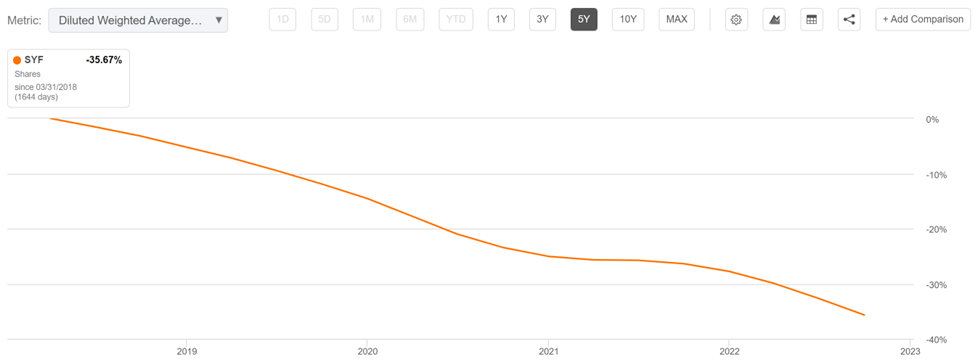

Furthermore, SYF should be considered as more of a total return story, as share repurchases at the currently low PE are highly accretive to shareholders. As shown below, SYF has retired 36% of its outstanding shares over the past 5 years alone.

SYF Shares Outstanding (Seeking Alpha)

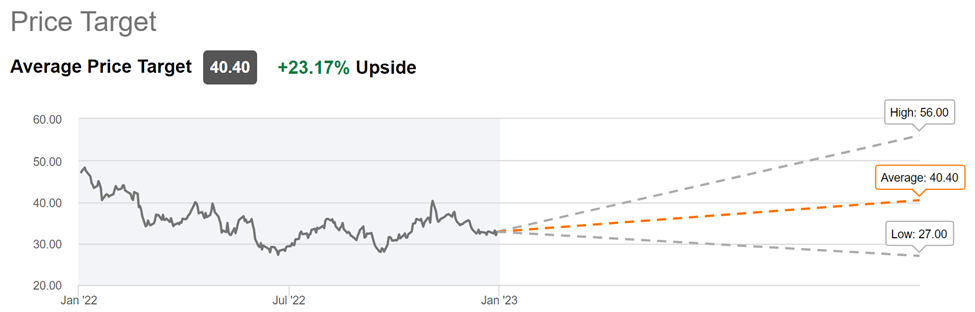

SYF offers plenty of value at the current price of $32.80 with a forward PE of just 5.5, sitting well below its normal PE of 10.2 since inception as a standalone company. Analysts expect some earnings headwinds this year, with an estimated 14% decline in EPS in 2023, before resuming 11% growth in the year thereafter. They also have a consensus Buy rating with an average price target of $40, equating to a 23% upside potential based on share price appreciation alone.

SYF Price Target (Seeking Alpha)

Investor Takeaway

Synchrony Financial has a robust credit card platform and is seeing overall strong operating fundamentals. While there are some risks on the horizon with respect to the macroeconomic environment, management has taken steps to reserve for potential losses. Meanwhile, it continues its track record of strong capital returns and it appears that many of the risks are already baked into the share price. As such, SYF at current levels may be a smart purchase for long-term value investors.

Be the first to comment