gorodenkoff/iStock via Getty Images

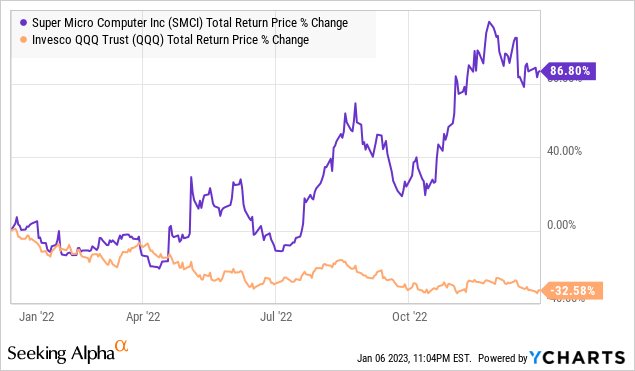

Super Micro Computer, Inc. (NASDAQ:SMCI) stood out as an exception to the tech sector sell-off in 2022, with shares climbing more than 85% and earning a spot in the S&P MidCap 400 Index (IJH). The story has been the strong sales and earnings momentum with the company benefiting from increased manufacturing capacity and shipments of its high-performance server and storage systems.

The attraction here is that beyond macro headwinds, rack-scale “Total IT Solutions” continue to capture high-growth themes across data centers, cloud computing, artificial intelligence, 5G, and IoT edge applications. Indeed, we covered SMCI with an article last year highlighting how its effort to integrate software and services was working to differentiate the company’s profile and drive margins, supporting a positive long-term outlook.

Our update today recaps recent developments while reaffirming a bullish view. In many ways, the trends have evolved better and faster than previously anticipated in what may still be the early stages of an ongoing transformation. While we don’t see shares doubling again from here in the near term, investors should expect more upside through earnings strength in 2023.

SMCI Key Metrics

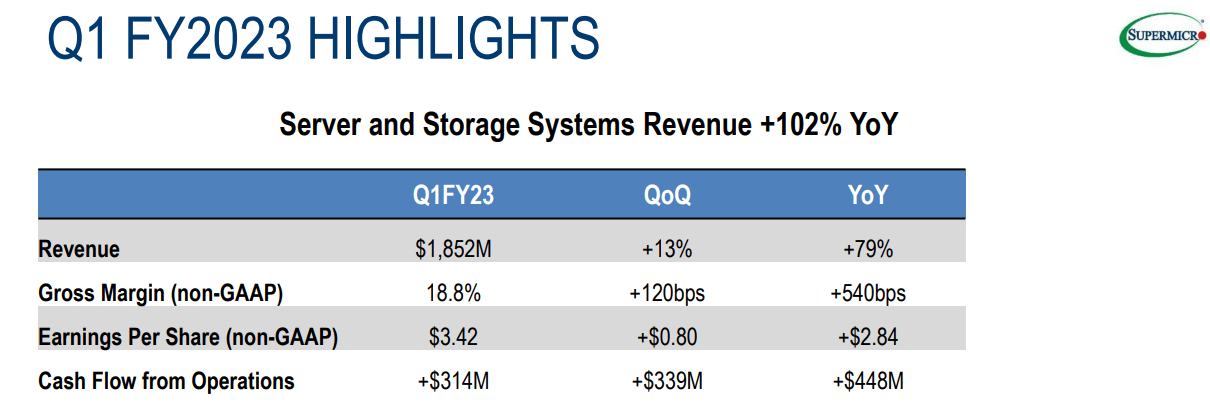

SMCI last reported its fiscal 2023 Q1 results in early November with a headline EPS of $3.42, a whopping increase compared to $0.58 in the period last year. The result also came in above expectations with the surprise coming from both the stronger top-line momentum, as well as the gross margin reaching 18.8% compared to 17.6% in the prior quarter.

Revenue of $1.9 billion increased by 79% year-over-year which reflects the scaling manufacturing including from its expanded Taiwan facility. The segment of server and storage systems saw revenues grow 102% which also indicates market share gains in various industry verticals.

source: company IR

The company has been shifting production towards new technologies including liquid-cooled solutions that have received a positive response from customers. Management explained that global utilization is still below capacity suggesting more sales upside with higher shipments to meet demand.

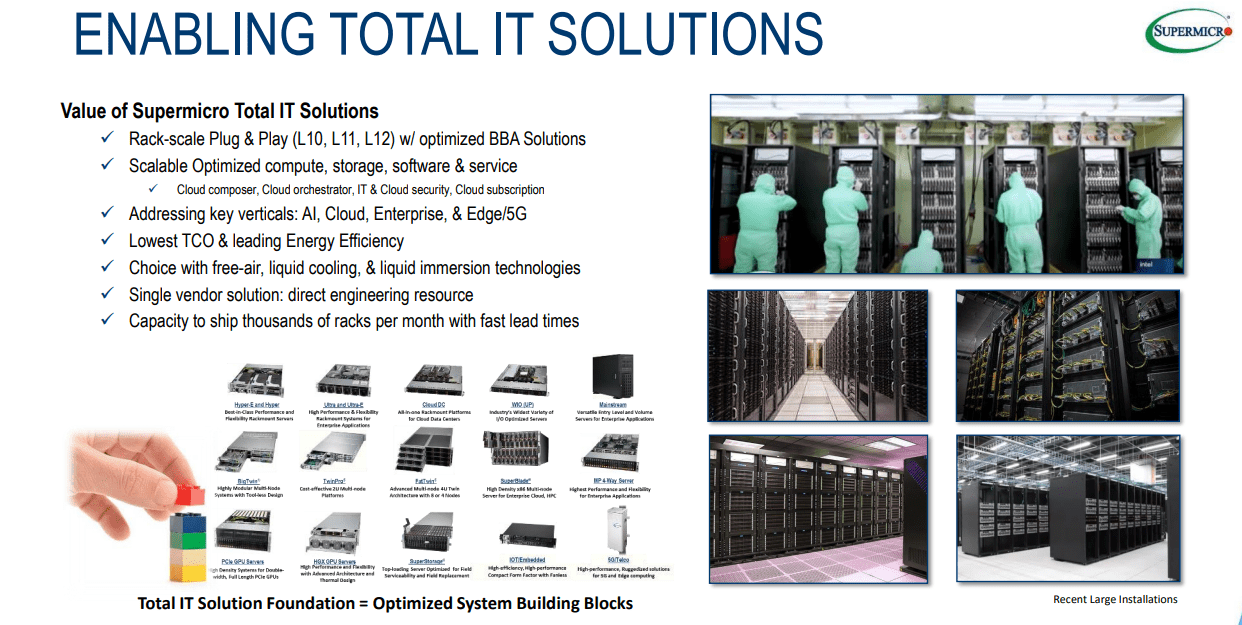

The best way to understand SMCI is to recognize that its “Building Block Solutions” as an open architecture and modular design, represents an innovative server platform compared to larger competitors. These are typically room and industrial-size data center equipment that integrate other industry components like CPUs, GPUs, memory, etc. Customers are choosing Super Micro Computer based on a lower total cost of ownership from its efficient technologies as the value proposition.

By this measure, the recent operating and financial trends are even more eye-opening against the headlines of supply chain disruptions in 2022 and the semiconductor industry shortages. Management summed it up well in the conference call when it said conditions have “dramatically improved”. From the conference call:

Three months ago, they have seen a shortage everywhere, but as of today, the shortage problem has been dramatically improved, so not much shortage at this moment. And we believe looking for growth in the coming quarters we won’t have a shortage problem. After this, that won’t be too bad and that’s why we prepared to grow market share.

source:company IR

Compared to fiscal 2022 revenue of $5.2 billion, management is guiding for 2023 sales between $6.5 billion to $7.5 billion. Notably, this estimate was revised higher from a prior midpoint target closer to $6.6 billion. On the earnings side, SMCI is expecting to reach adjusted EPS between $9.00 and $11.30 this year. If confirmed, the result at the midpoint would represent an increase near 80% as a continuation of the Q1 trends.

Finally, we note the company ended the quarter with $238 million in cash, nearly covering the approximate $250 million in total debt. This is in the context of $303 million in free cash flow last quarter as evidence of a rock-solid balance sheet and liquidity position.

Is SMCI A Good Stock?

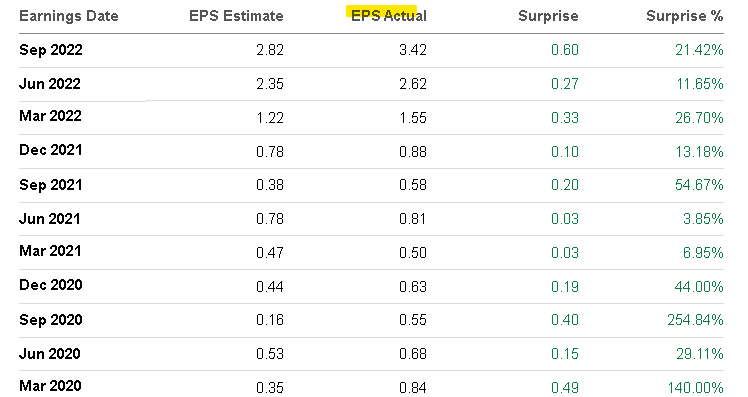

To explain how SMCI broke out in 2022 with its stock price performance, the best measure likely comes down to the string beating quarterly EPS and revenues expectations that goes back to early 2020. Management has earned some clout with this history of solid execution which has all the pieces to continue, in our opinion. With earnings growth recognized as a major driver of stock market performance, the potential for more of this trend should be positive for Super Micro Computer as an investment.

Seeking Alpha

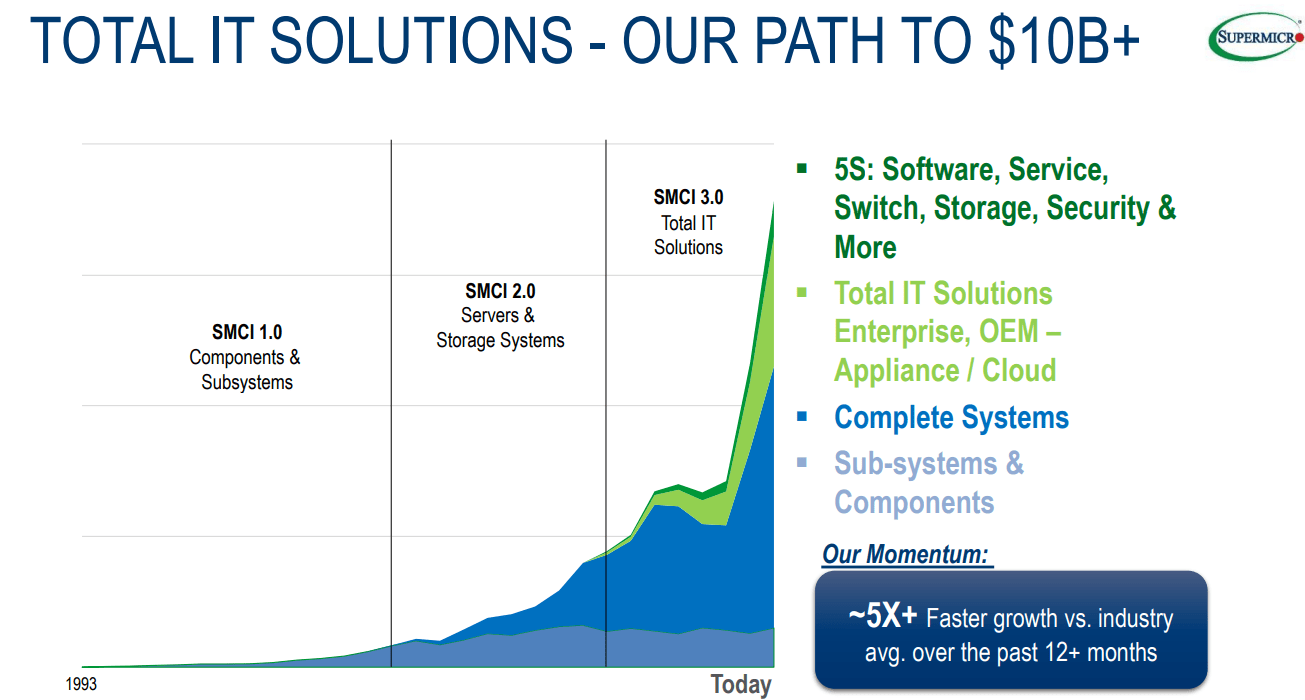

The company sees a path to reach $10 billion in annual sales, or double the result last year. The path considers further momentum in its core systems segment while capturing new growth drivers including the ongoing expansion into software, services, switch, storage, and security as the “5S”. The ability to consolidate market share should add to that potential as customers expand their relationships.

source: company IR

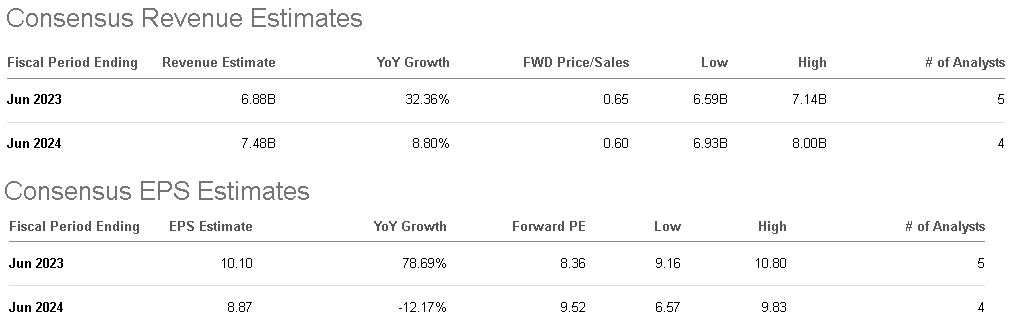

Looking at the consensus estimates, the market forecast for 2023 revenue growing by 32% and EPS 79% higher y/y are roughly in line with management guidance. For 2024, the data expects a moderation in growth with a 9% revenue increase while EPS faces some volatility, pulling back -12% which could be related to a tough comparison period. Nevertheless, these estimates could prove to be too conservative in a scenario where the macro backdrop improves adding to the organic growth tailwinds.

source: company IR

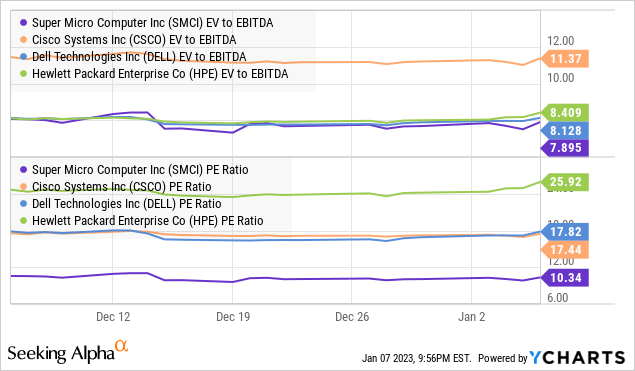

In terms of valuation, SMCI continues to trade relatively attractive next to global peers and large-cap leaders like Cisco Systems Inc (CSCO), Dell Technologies Inc (DELL), and Hewlett Packard Enterprise Co (HPE). These companies are directly cited in the company’s annual report as key competitors, particularly in the x86-based general-purpose servers and components market.

SMCI trading at a 7.9x EV to EBITDA multiple is below DELL at 8.1x, HPE at 8.4x, and CSCO at a higher 11.4x. Similarly, SMCI looks “cheap” with a P/E ratio of 10.3x on earnings over the last twelve months compared to DELL and CSCO close to 17.5x.

To be clear, it’s not a direct comparison as each of these players operates across different segments and specialties. Cisco, for example, trades at a premium likely justified based on its operating tilt more toward software which can generate higher margins.

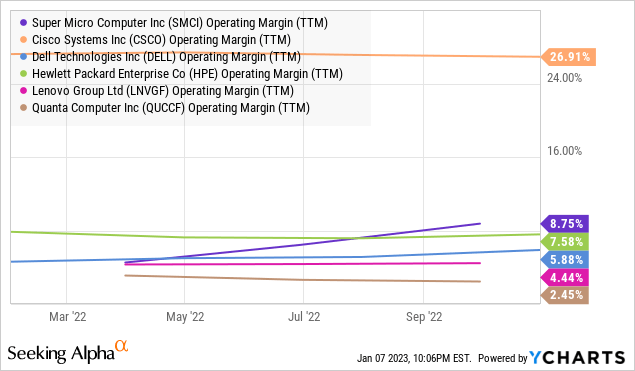

Still, if we expand the scope to include foreign vendors and original design manufacturers (ODMs) like Lenovo Group Ltd. (OTCPK:LNVGF) and Quanta Computer Inc. (OTC:QUCCF), SMCI stands out with not only its stronger growth momentum but also a higher operating margin at 8.75% over the trailing twelve months.

Putting it all together, we believe that the stock deserves a higher premium as part of the bullish case into 2023. Again, a sense that the shift towards more value-added products and services is still in the early stages could push SMCI’s positioning more towards a services-centric Cisco, and away from simply a hardware name. With that same thought, the stock should also be rewarded by its enhanced visibility entering the S&P MidCap Index, breaking away from its history as an underfollowed small-cap.

SMCI Stock Price Forecast

There’s a lot to like about SMCI as a stock that should be on more investors’ radars. Paring back some of the positive outlook and optimism, the other side to the discussion is that shares have been on fire, up 70% just since hitting a low near $50 in October. There’s a case to be made that the boat from last year has left the station and the next leg higher will be more difficult.

If the otherwise lofty expectations are already priced in, the result could be a backdrop of higher volatility with less room for error on the financial side. Into the Q2 earnings report, the operating margin will be a key monitoring point which further increases critical for the stock to maintain positive momentum.

The other risk to watch could simply be a deterioration of the economic outlook for any number of reasons which would likely translate into further market volatility. Weaker-than-expected growth would also open the door for a leg lower in shares.

To conclude, we are bullish from here with a buy rating and price target for the year ahead at $100 implying a 9x multiple on the upper end of management’s EPS guidance. This level would help the valuation premium converge with global industry peers and reflect the company’s fundamental strengths. From the chart, it will be important for shares to hold the long-running trendline with $75 appearing as an area of technical support to watch.

Seeking Alpha

Be the first to comment