ImagineGolf

Paul Singer and Elliott Investment Management have long held more of an interest in buying energy companies than many funds, currently holding material stakes in Marathon Petroleum (MPC), APA Corporation (APA), Peabody (BTU), and several others. Early April saw the firm take another stake in the space: beleaguered Canadian oil giant Suncor (NYSE:SU), which fits their typical investment to a tee – relative underperformance, poor public perception, potential segment spin-off or sale opportunities, and the potential for increased capital returns to shareholders.

Corporate activism can take time to bear fruit, but investors are quickly starting to see the effects of their involvement in Suncor. Some of this was driven by an unfortunate catalyst: the loss of another employee at one of its mines after Elliott highlighted a dismal safety record and poor corporate culture in its initial letter to the Board. This spurred support from other more passive institutional owners, and likely drove the quick time to an agreement to work together. See the below quote from its initial letter to the firm:

Our research suggests that missed production goals, high costs, and, tragically, a number of employee fatalities and other safety incidents, all find their roots in a slow-moving, overly bureaucratic corporate culture that appears to have lost the dynamism that not long ago made Suncor the most valuable energy company in Canada.

Thus, CEO Mark Little was offered up as the sacrificial lamb by the current Board of Directors. His resignation was effective immediately, not surprising as fatality rates over the past ten years exceed those at all of its oilsands peers combined. Someone has to fall on the sword for that, and it should stem from the top. As part of its arrangement, Elliott has won three board seats as part of the deal, and two of those will serve on the committee designated with finding a replacement either internally or externally.

One of the next stages is unlocking value within the portfolio. This is going to be the largest point of contention, as management has long held that a big part of the value proposition for Suncor – and really many of the oilsands giants – is their integrated portfolios. Alongside their upstream production, Suncor has 450,000 barrels per day of refining capacity, 50mm barrels of storage, and Petro-Canada, a network of nearly 2,000 retail and wholesale locations for selling fuel. Third party buyers for refineries are few and far between, so Elliott is focusing on copy and pasting its Marathon Petroleum playbook, looking to monetize Petro-Canada just as it helped push for a sale of Marathon’s Speedway business.

Explore opportunities to unlock the value of high-multiple assets outside of the core Oil Sands business, including a strategic review of retail.

I think pretty important here is that the focus is on its retail business, or “rack forward”. This is after all blending is done, additives, and getting the product into the proper distribution market. Suncor is going to aim to retain its wholesale operations, keeping all that behind the rack infrastructure. This is about $600mm in purported EBITDA, and should fetch a solid price tag. Note that 7-Eleven paid 7.1x post synergy EBITDA for Speedway, so it would not be all that surprising to see a $4,000mm+ price tag for a retail divestiture. With the company trading at just a bit more than 3.0x EV / EBITDA even on 2024 estimates – a time when most expect upstream and downstream profits to be closer to mid-cycle – such a divestiture would be highly accretive.

Cost Savings (Suncor)

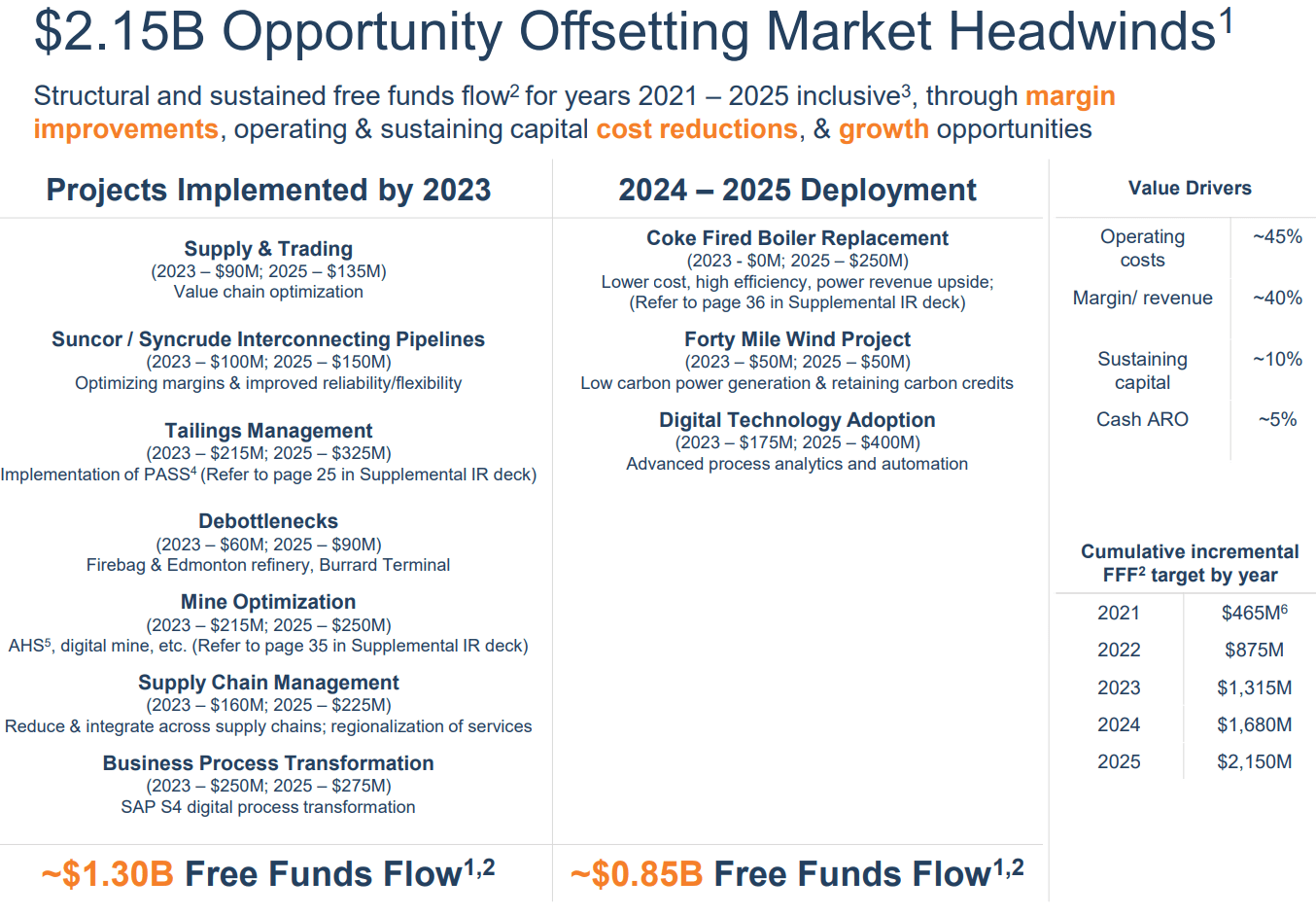

Don’t forget other opportunities. Prior to Elliott taking a stake, Suncor had already outlined $2,150mm in identified opportunities through 2025 to “offset market headwinds”. Roughly two thirds of these cost savings are expected to be implemented by 2023, including refinery debottlenecking, mine optimization, supply chain management, tweaks to trading operations, and a variety of other things. There will, of course, be significant spending associated with implementing many of these initiatives. Proof of concept as far as savings are still illusive on this cost cutting program, but admittedly we are still early stages. Having Elliott involved means that management is going to be held to task on execution.

Takeaways

Corporate activists can have an iffy reputation, but I think it’s a net positive here in Canada where price multiples remain depressed and there are some issues that need to be addressed (safety) or management held to task on promises (multi-billion dollar savings initiative). Having Elliott in their corner gives equity owners a voice that is – at least in the short term – aligned with them. This might bring back some investors that have given up on the Canadian energy large caps in recent years.

Suncor is pretty catalyst-rich at this point. The market would likely warmly accept the announcement of a CEO with an excellent pedigree, as well as positive outcomes on its strategic initiative research that will contemplate a sale of retail operations, as well as others. We should see news on both of these items by end of year.

Investors also get paid to wait. Suncor already recently increased the base dividend and, alongside its normal course issuer bid, investors could see dividends and stock buybacks total up to 14.0% of the current market cap over the next year. The early stages of 2022 already provided some foundation for the free cash flow opportunities that Suncor can throw off in this kind of environment where both upstream and downstream margins are both high. Tough to fault the bull story here, and I think there is a great opportunity for share price improvement here even as the company faces lower EBITDA in forward periods after arguably peak Q2 2022 earnings.

Be the first to comment