zhaojiankang

Investment Thesis

Steel Dynamics (NASDAQ:STLD) is one of the largest steel producers in the United States.

Not only were Q4 EPS figures dramatically better than expected, but most importantly, analysts were totally caught off guard with their 2023 EPS estimates.

I believe that STLD could see $15 or even $17 of EPS in 2023, compared with analysts’ estimates of $11.

Note that ironically, the biggest investment risk here is high steel prices. I explain the bull and bear case.

Steel Dynamics Prospects for 2023

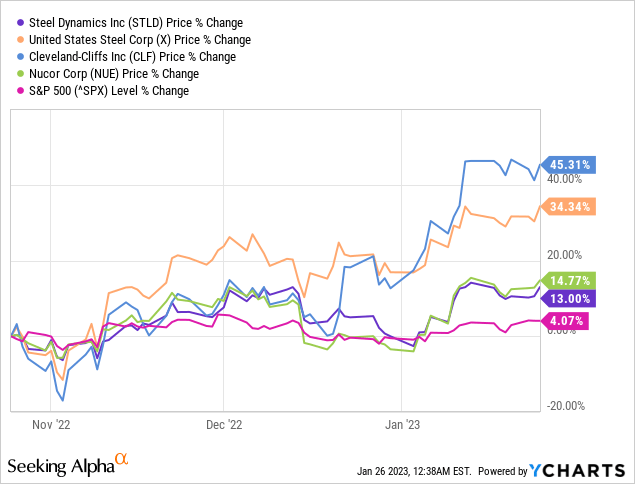

Before discussing 2023 prospects, let’s take a moment to realize how much of a winning trade steel stocks have been in the last 3 months.

The group has easily outperformed the S&P 500 (SPX) in the same time frame. Consequently, Steel Dynamics had much to prove as it headed into Q4 earnings.

Indeed, there were many investors holding onto rapid gains, with their finger hovering over the sell button, looking to profit-take in STLD. To take profits, unless, they strongly believed that there were even better times ahead.

With that in mind, let’s discuss what’s ahead for Steel Dynamics.

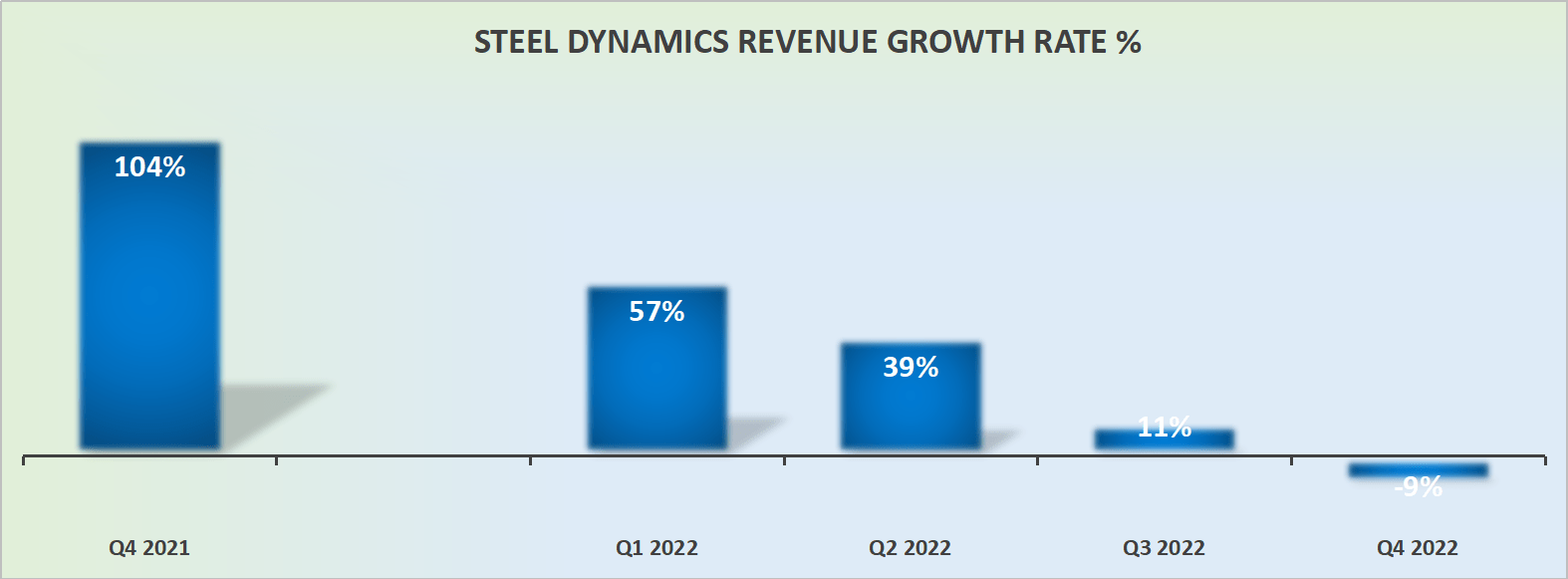

Revenue Growth Rates Slow, But That’s OK

STLD revenue growth rates

As you can see above, Q4 saw its revenues fall 9% y/y. But when you think about it, this is OK. It tells you two things.

Firstly, it shows that despite Q4 being up against a really tough comparable with the prior quarter, Steel Dynamics’ Q4 2022 didn’t fare all that badly.

Secondly, if this is as bad as it gets for Steel Dynamics, once we understand the key drivers, there’s a lot to be bullish about buying into this name.

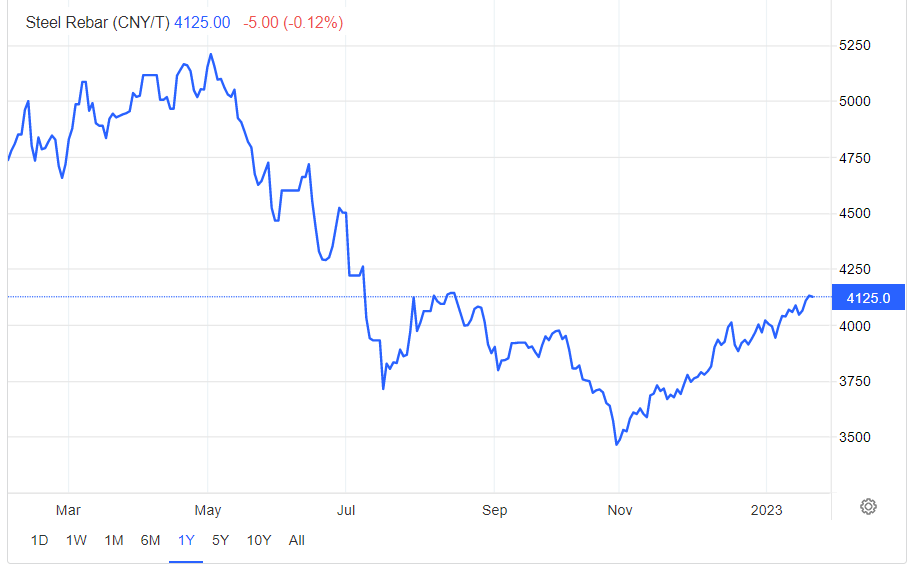

The Key Drivers Discussed

The main driver for Steel Dynamics is steel prices. And you can see here that steel is rapidly sizzling higher.

Trading Economics

And the reason why steel prices are moving higher is mostly, but not solely, due to China’s reopening. Or more specifically, China’s real estate market finding government support.

This is contrary to what many investors believe. Many investors believe that steel prices are being buoyed by the construction and automotive sectors in the US. This also plays a role. But it’s not the best near-term driver of steel prices.

I’ve discussed this in prior steel articles throughout SA. The capital infusion from Chinese banks to Chinese real estate is small in the grand scheme, but it’s the signal that the Chinese government is ready to step in and support matters if they get too dire. The intent is what matters, not the absolute figures.

With that in mind, let’s talk about getting paid with capital returns.

Capital Returns, Steel Dynamics Repurchases 12% of the Company

Look back at the titles of my SA work on STLD. I’d been consistently stating that STLD dynamics was going to repurchase a significant amount of shares in 2022.

All told, Steel Dynamics repurchased 12% of its market this year. And as we look ahead, I believe that together with its dividend, STLD could be in a position to return to investors at least a further 5% via buybacks and dividends combined.

STLD Stock Valuation — 5x 2023 EPS

For 2022, Steel Dynamics reported $22.68 in non-GAAP adjusted EPS. For investors, this means that the stock is trading at less than 5x trailing EPS.

But as you know, the market is always looking 6 months ahead. So, investors are considering the fact that Q4 2022 just reported $4.37, and if the steel prospects are already starting to improve, that could mean through further share repurchases, STLD could probably see close to $22 per share yet again in 2023.

Perhaps I’m being too bullish and extrapolating too aggressively for the rest of 2023. And that’s certainly very possible.

After all, with higher steel prices, many competitors in China and Europe which have now curtailed production due to prohibitively high energy costs will rapidly resume steel production. The speed at which overseas will flood the market could take many people off guard, and that’s something to keep in mind.

Nevertheless, my point is this. Presently analysts expect 2023 EPS to be around $11 per share. But in my estimates, this figure is woefully inaccurate.

The Bottom Line

Steel Dynamics is a steel-based US company with a US labor workforce. This means an expensive labor workforce compared with overseas competitors. So, I caution investors to be mindful of how they invest in this business.

That being said, despite it being a commodity company, reliant on steel prices that are fully outside of its control, I believe the risk-reward here is very attractive.

Be the first to comment