Spencer Platt/Getty Images News

While Spotify (NYSE:SPOT) built a remarkable music streaming business, we would urge investors to stay away from the stock, given slowing subscriber growth, increasing churn, lofty valuation, limited differentiation and increasing competition. With Eastern Europe in turmoil with the Ukrainian war, we expect revenue growth and subscriber growth rate to slow. In addition, we also expect the churn to increase due to inflation, as subscribers will likely prioritize other essential goods and services over a Spotify subscription. With Amazon (AMZN), Google (GOOG) (GOOGL) (YouTube), and Apple (AAPL) increasing the push to grow their streaming businesses, we do not expect Spotify to weather the increasing competition well. Therefore, we continue to believe there is more downside for the stock from the current levels. Even though the stock price declined some 50% from its 52-week high of $306, the stock is still fairly expensive. On a P/E basis, the stock is trading at an elevated level compared to the peer group. Therefore, we believe there will be a better entry point for the stock at a much lower level. We would not be surprised to see the stock below $100 levels within the year. Below $100 levels, we could get more constructive, depending upon its position within the industry. Therefore, we urge readers to sell the stock at these levels to either lock-in their profits or look for better investments to make money.

Music labels control Spotify’s destiny

Spotify continues to distribute content produced by other parties. Spotify is at the mercy of the content creators for its business. The content creators and music labels who license the content to Spotify for streaming will likely demand higher payments as inflation continues to edge higher. The company will have no choice but to pass the costs to subscribers to remain barely profitable. Passing costs to subscribers can only work for so long and will likely increase the churn for the company. Therefore, we believe Spotify will less likely able to withstand royalty payment increases than Amazon, Google and Apple, each of which have bigger balance sheets and multiple other businesses to absorb the costs. Eventually, we believe the streaming services business will be two or three horse race – Apple, Amazon and Google in much of the western world.

F1Q22 results could be dicey

We are concerned that F1Q22 results would be problematic for many companies we regularly cover. Spotify is no exception. Spotify generates a majority of revenue in the US and UK, but has significant exposure to many countries in Europe. Given uncertainty in Europe due to the war in Ukraine, we expect many companies would need to reset C2022 expectations. We expect analysts to revise estimates down impacting the stock. We would certainly not be long the stock going into the earnings given the uncertainty. Spotify is expected to report its F1Q22 results on 04/27/2022.

Wall Street expectations are way too optimistic

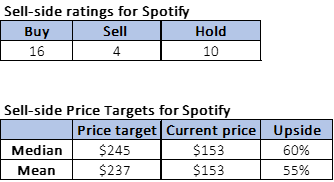

A majority of the analysts covering Spotify rate the stock a buy. Out of the 30 analysts covering the stock, sixteen are a buy on the stock, while ten are hold rated and the remaining four are sell rated. The consensus median price target is $245 and the mean is about $237. With F1Q22 and FY22 estimates at risk, we believe there is a lot of downside for the stock. The stock can go below the 52-week low of $118 and could approach about $100 over the next one year. Therefore, there is no reason to own this stock at the current levels. We would urge readers to sell the stock if they own it now. The following charts illustrate the sell-side consensus mean/median price targets and stock ratings.

Refinitiv

Valuation

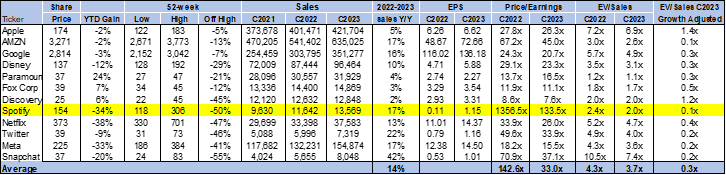

Spotify is not cheap and is barely making any money on an EPS basis. On an EV/Sales, or Price/Sales basis, it may seem cheap when compared to other loss making entities, but, we believe there is lot more downside on this stock. The stock can easily get to $100 from here. We do not believe the company has any moat that is not insurmountable. Apple, You Tube and Amazon music recommendation engines will get better eventually. Eventually means we do not need to wait forever to get there. Spotify’s moat is even shallower than Netflix’ moat and Netflix moat is way over-hyped. We would need Spotify stock to pull back significantly before recommending the stock. For longer-term investors, we believe there are better names to own. The following chart illustrates Spotify’s valuation versus the media peer group.

Refinitiv

What to do with the stock

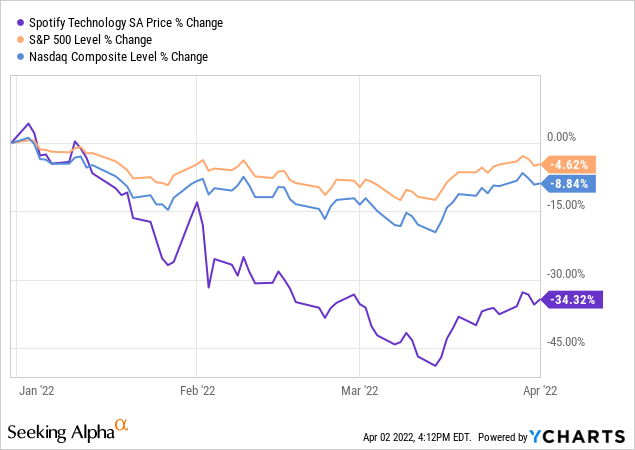

Spotify underperformed Nasdaq and S&P, YTD, in 2021 and over last three years. This is not surprising to us, given that the company barely makes any money, continues to invest aggressively to acquire new subscribers and will likely lose share to large players such as Apple, Google and Amazon. The company keeps investing in podcasts and other money losing ventures, trying to ignite growth and command higher multiples.

YTD, Spotify stock is down 34%. In 2021, Spotify stock was down about 26%, while Nasdaq was up 21% and S&P was up about 27%. Over the last three years, Spotify was up about 10%, while Nasdaq is up about 82% and S&P is up about 59%. We do not expect Spotify to do any better in the next two or three years, given the increasing competition from Apple, Amazon and Google. The following chart illustrates Spotify’s performance YTD, in 2021 and over the last three years.

YCharts

YCharts

Therefore, we recommend investors to sell the stock at the current levels. We believe the sentiment on Spotify has peaked some three years ago, just after their IPO, and its best days are behind it. The pandemic drove subscriber additions last two years, and we expect subscriber growth to slow for the company. More importantly, we also believe churn will likely increase as many subscribers will look to deploy their hard-earned cash elsewhere in an inflationary environment. We also believe Spotify will have to increase the cost of subscription at some point, as the music producers demand higher payments. We do not see Spotify’s ability to increase subscription prices without increasing the churn. Finally, Spotify is not cheap, and there is no compelling reason to own this stock at the current times.

Be the first to comment