Kevin Dietsch/Getty Images News

Why Did Southwest Cancel Thousands of Flights?

Travelers of Southwest were not feeling the LUV after an unusually high number of employees called in to work over the holidays. Southwest VP of ground operations Chris Johnson had to call a “state of operational emergency” after the airline canceled nearly 3,000 flights Monday, and there’s nothing “transparent” about that! With nearly 71% of its schedule canceled- more than any airline carrier over the Christmas holiday – a total of 12,000 flight cancellations have occurred since Friday, December 23rd.

From an operational standpoint, Southwest is in dire need of a turnaround. But the popular passenger airline company Southwest Airlines Co. (NYSE:LUV), known as a leisure-centered, low-cost carrier with a laser focus on creating value for customers and shareholders, is under pressure after suspending operations nationwide. So what happened?

Attributing the cancellations and delays to Winter Storm Elliott, according to flight tracking website FlightAware, Southwest received scrutiny from all angles, including the Department of Transportation. Passengers in disbelief stood by as their holiday plans were foiled. And while the airline carrier prides itself in customer service, it has reduced its schedule to nearly one-third “for the next several days,” prompting its stock to trade near a 52-week low of $30.20 per share, after shares slid nearly +6% amid airline cancellations.

Southwest Airlines’ memos confirmed that its systems to coordinate airplanes and flight crews failed. “Part of what we’re suffering is a lack of tools…We need to be able to produce solutions faster. We need to be able to communicate with each other where it doesn’t involve a phone call,” said Jordan, a 34-year Southwest veteran, in a Bloomberg report. System and communication failures are risks when investing in airline stocks, but there are a few other risks to consider in this cyclical business.

Risks: Investing in Airline Stocks

COVID-19 has impacted travel, with its effects persisting. Despite increasing demand for travel and flights, high fuel prices, inflation, and other factors are disrupting the highly cyclical industry. Three of the biggest risks when investing in airline companies in the current environment involve:

-

Labor Shortages – As evidenced by the flying experience post-COVID, airlines are understaffed and having difficulties hiring individuals to service flights. Staff is overworked and underpaid. Additionally, pilots have strict guidelines on how much and frequently they can fly. Factor in potential pilot strikes, as many have rejected pay raises of 20% or more amid long hours and staffing difficulties, and the industry could be in for continued pressures.

-

Consumer Demand – One primary driver of airline profitability is consumer demand. While airlines are not yet experiencing diminished consumer demand, a recession is expected in 2023. Should airlines experience less demand, they’ll have to lower costs. Lower prices eat into revenue production and profitability. With consumer spending already trending down, this creates one of the biggest obstacles that airline companies may have to overcome in 2023.

-

Fuel Prices – Like all of us feeling the pain at the pump, the cost of jet fuel skyrocketed. Those costs were passed on to consumers. Should consumer demand in 2023 be reduced, airlines will be forced to lower costs, eating into profitability. And while fuel cost is coming down, which can help lessen the impacts, less demand equates to less revenue and profits.

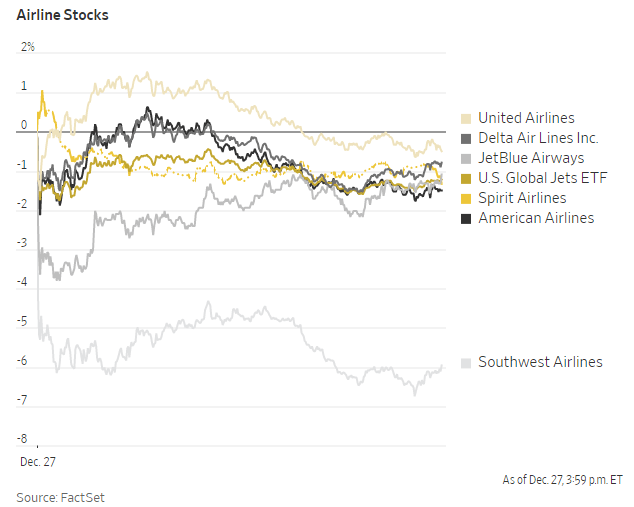

While many airline stocks like JetBlue, Spirit and American Airlines (AAL) lost ground over the holiday season, one of the biggest decliners was Southwest Airlines, a stock with strong quant-rated fundamentals worth watching.

Airline Stock Declines (12/27/22)

Airline Stock Declines (12/27/22) (FactSet, WSJ)

Southwest has showcased its ability as a low-cost carrier to maintain higher yields than larger competitors, including some of the larger legacy carriers like American Airlines. Offering a solid business model, Southwest has outperformed the competition and showcased resilience despite a recessionary outlook. Southwest is building part of its growth strategy around business travel through attractive partnerships that include banks for their Rapid Rewards frequent-flier program. Consider a cost-saving company like Southwest for a portfolio, especially when they possess the collective characteristics of businesses that stand to benefit.

Southwest Airlines (LUV)

-

Market Capitalization: $21.43B

-

Quant Rating: Buy

-

Quant Sector Ranking (as of 12/27): 67out of 628

-

Quant Industry Ranking (as of 12/27): 8 out of 29

Serving more than 121 U.S. and ten international destinations, Southwest has done a solid job recovering from the lack of travel shock presented in 2020 by the pandemic. With COVID-19 distressing the airline industry, Southwest has made a turnaround but has struggled with labor shortages. Winter weather hit airline stocks over the Christmas holiday, catapulting Southwest as the largest midday airline stock decline by -5%. Seeking Alpha News reported:

“According to flight-tracking website FlightAware, the major airline canceled nearly 3,000 flights on Monday, amounting to 71% of scheduled flights. In addition to cancellations, 16% of scheduled flights were delayed, leaving only 13% of flights on time. On Tuesday, 62% of flights have already been canceled, with disruptions expected to continue toward the year-end.”

Although the travel chaos resulted in the U.S. Department of Transportation indicating they will be closely monitoring the company to ensure cancellations were controllable and LUV has a plan going forward, the carrier has been resilient in the face of unforeseen events.

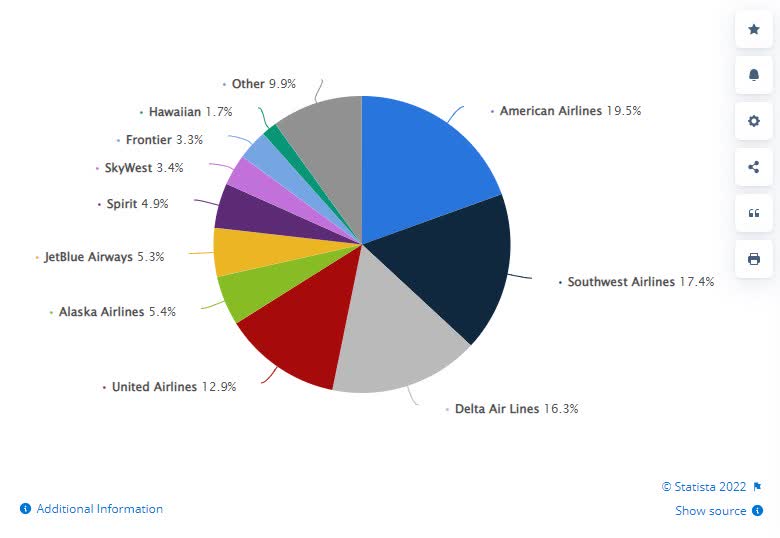

Southwest has managed costs better than many big-name legacy carriers due to their single aircraft flying into less popular airports to ensure reduced fees. And while keeping costs low for the carrier and its customers, Southwest has managed to set itself apart by earning comparable yields to legacy carriers, possessing leading domestic market share compared to its competitors.

Domestic Market Share of U.S. Airlines (Jan to Dec 2021)

Domestic Market Share of U.S. Airlines (Jan to Dec 2021) (Statista 2022)

When you factor in Southwest’s strong fundamentals and buy rating, LUV is a stock to consider for investment into 2023.

LUV Stock Growth & Profitability

Based upon its third-quarter earnings and investor presentation, Southwest maintains strong leisure revenue trends going into 2023, anticipating increased business revenue and passenger share, +10% going into Q4 2022. Southwest has built a multi-year fuel hedging plan to aid with surging fuel costs and plans to modernize its aircraft fleet as part of its growth plans.

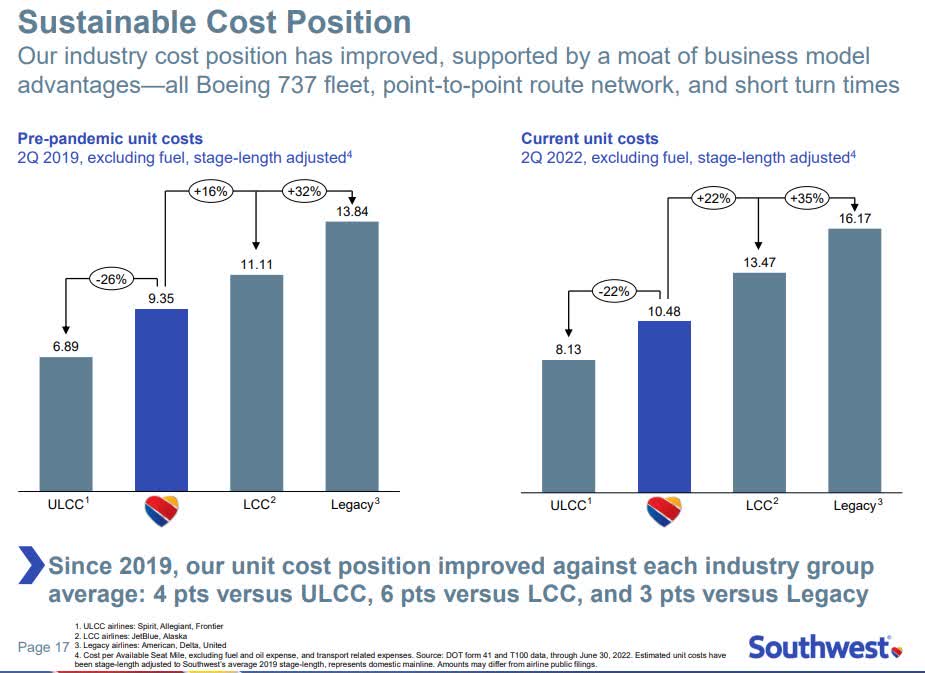

Southwest Stock Sustainable Cost Position (LUV Q3 2022 Investor Presentation)

Compared to its competitors, Southwest continues to improve its cost position since 2019. Entering new markets, which included Hawaii amid the pandemic. Southwest’s goals for consistent profitability are primed for increased margins while reducing debt.

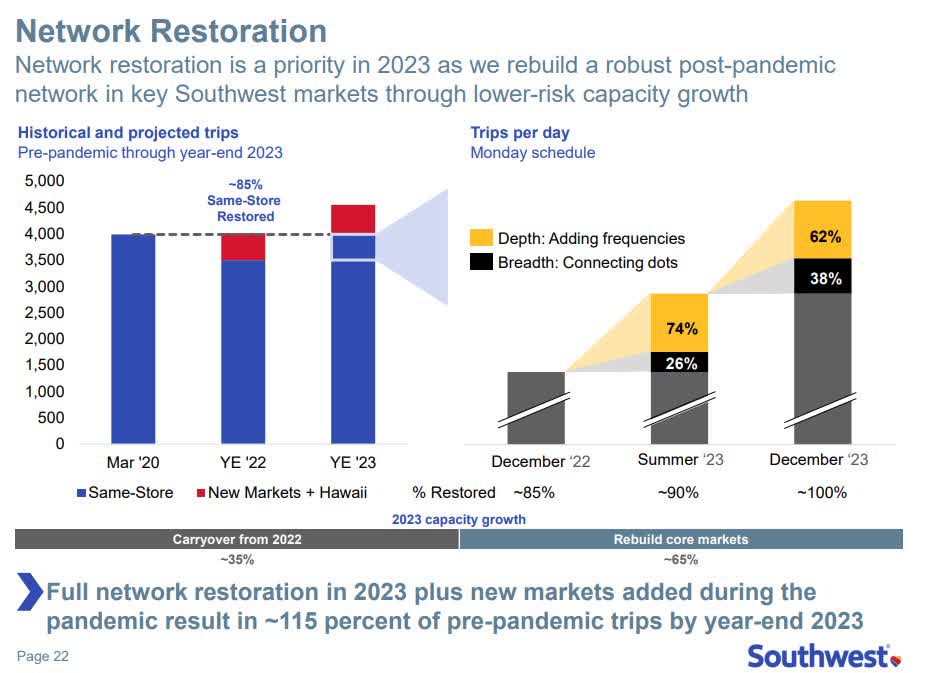

LUV Network/Market Growth Plans (LUV Stock Q3 2022 Investor Presentation)

Despite missed revenue for Q3 2022, Southwest’s EPS of $0.50 beat by $0.08. With only 7% of its flights being international, 93% of its income is from domestic travel. American Airlines is the only domestic carrier that outperformed Southwest by revenue. Given that a portion of its revenues is derived from cargo and 16% from international flights, I prefer the outlook for Southwest.

With elevated fuel prices, LUV remains 61% hedged going into Q4 and expects healthy hedging gains. CEO Bob Jordan said:

“We continue to expect both inflationary cost pressures and cost headwinds from lower productivity and efficiency in fourth quarter. This is all anticipated in our full-year guidance. And other than some timing of cost between 3Q and 4Q, our cost trends have been very stable. We’ve been executing well on our full-year 2022 cost plan since we provided our full-year CASM-X guidance back in January…Specific areas of focus for 2023 are to maintain adequate staffing and get caught up in pilot staffing, get new contracts with all labor groups currently in negotiations…While we expect a healthy amount of capacity growth next year, it is nearly all going back into key Southwest markets.”

The demand for airline travel continues to grow post-pandemic, and Southwest Airlines remains the only U.S. airline with investment-grade ratings and is ranked by J.D. Power as one of the best airlines in America.

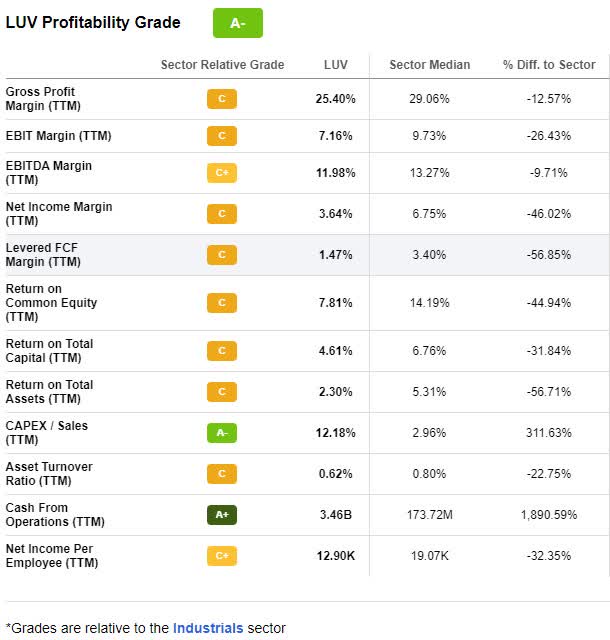

Southwest Airlines Stock Profitability (Seeking Alpha Premium)

Offering a strong balance sheet, repurchasing $689M of their convertible notes, ~30% of original issuance, and continued focus on LUV’s shareholders and long-term capital returns, Southwest Airlines reinstated its dividend of $0.18, payable in January 2023. Tremendous cash from operations of $3.46B has provided some cushion for the airline. Its solid momentum and discounted valuation showcase a stock worth considering for portfolios as it continues to navigate headwinds.

LUV Stock Valuation

Southwest is a low-fare carrier known for managing costs to bring value to its customers and shareholders, so it should be no surprise that the stock comes at a reasonable price. Despite LUV – 22.86% YTD and down 18.94% over the last year, the company has done a tremendous job with its strategic initiatives, which are focused on creating $1B to $1.5B in EBIT by 2023. Forward EV/EBIT currently stands at 8.47x, a -42.96% difference to the sector, and offers an A+ forward PEG ratio of 0.36, a -51.62% difference to the sector. Although the “volume and magnitude” of weather challenges have prompted Southwest to reduce its schedule, consider buying the dip into the new year, particularly given its momentum and solid growth and profitability metrics.

Southwest is still primed to take flight in the New Year.

Increased fuel costs are one of the biggest headwinds facing airlines coming into the New Year. Southwest and the airline industry as a whole have struggled with staffing shortages that could get worse should we see a recession in 2023. With that in mind, both recent earnings and forward analysts’ earnings estimates showcase solid figures. Over the last 90 days, 15 analysts revised up, with some industrial stocks proving to be solid buys.

Despite its fall in share price, Southwest has room to take flight. Despite selling off amid the winter storm and logistical issues over the holidays, Southwest is a buy, as showcased by the quant ratings.

Although a cyclical business, Southwest possesses a track record of cost controls, strong financials, and excellent growth and profitability, with forward revenue growth of 43.85% and forward EPS growth rates (3-5 year CAGR) at 44%. Likewise, the combined growth rate and P/E in the form of the PEG ratios show Southwest is trading at more than a 75% discount to the sector. Consider LUV for a portfolio, or if you’re interested in alternate Top Rated Stocks, equip yourself with our tools to help ensure your portfolio contains substantial investments that stand to increase over time.

Be the first to comment