Justin Sullivan

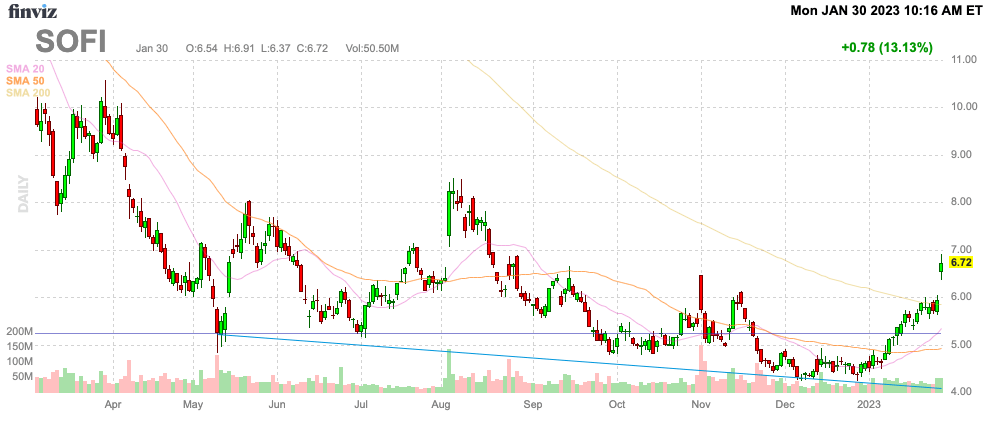

Despite major headwinds, SoFi Technologies (NASDAQ:SOFI) continues to blow away expectations. The fintech remains far more profitable than the market thought and the fast growth justifies a far higher stock price. My investment thesis remains ultra Bullish on the stock trading around $7 in initial trading.

Source: FinViz

Marketing Machine

The market shouldn’t be shocked by SoFi reporting another quarter with growth in excess of 50%. Amazingly, the stock did just spent the last couple of months trading in the $5s with CEO Noto loading up on shares in the $4s.

In total, SoFi reported revenue growth of 58% in Q4’22 with record adjusted revenues of $443 million. Most importantly, the additional revenues dropped to the bottom line.

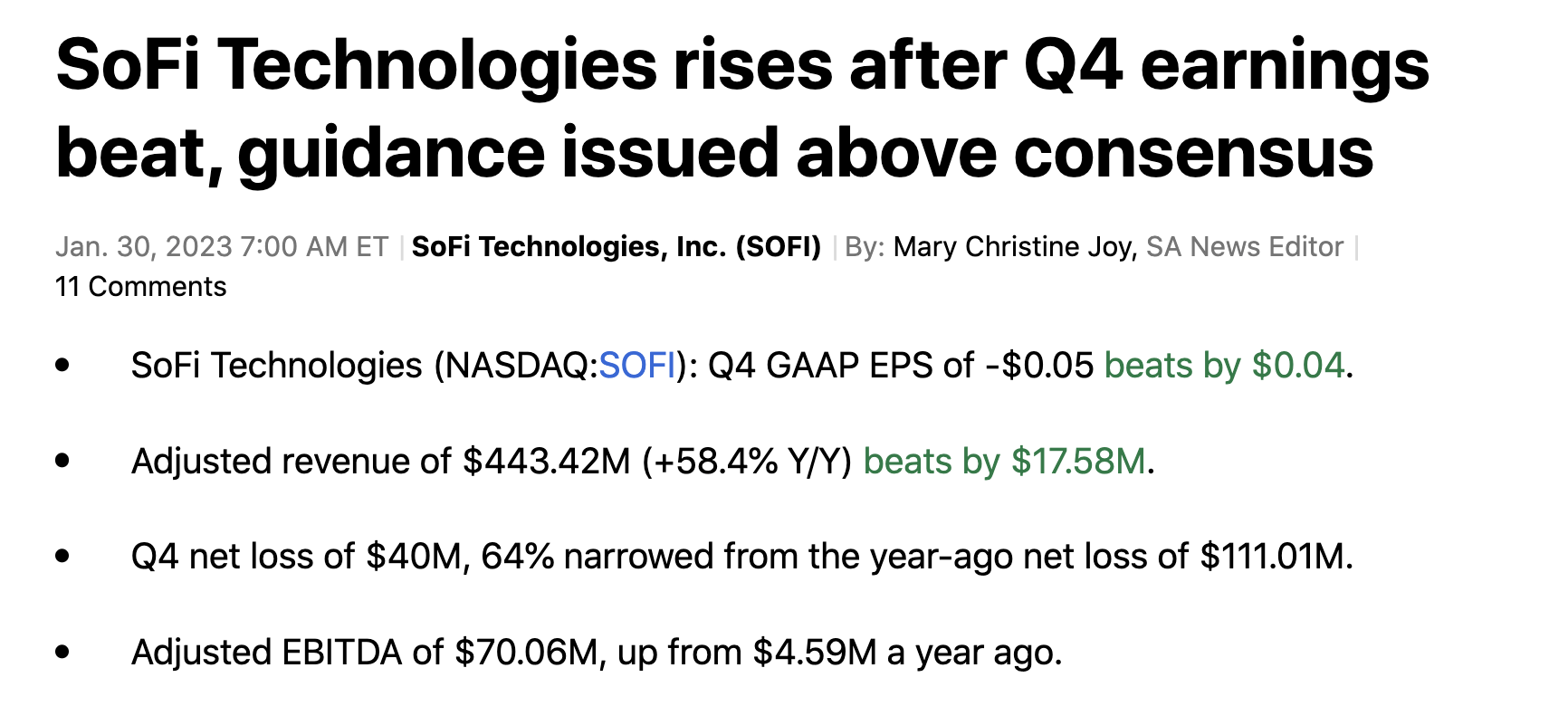

Source: Seeking Alpha

SoFi reported adjusted EBITDA of $70 million for a 16% margin in the quarter. The market doesn’t trust the adjusted EBITDA numbers, but remember just about all of the adjustments are for actual non-cash charges.

For Q4’22, SoFi reported a GAAP net loss of $40.0 million, but the company reported $71.0 million of stock-based compensation and another $42.4 million in mostly amortization charges. When excluding just the interest expenses and income tax, the adjusted EBITDA turns into an adjusted profit of $62.9 million.

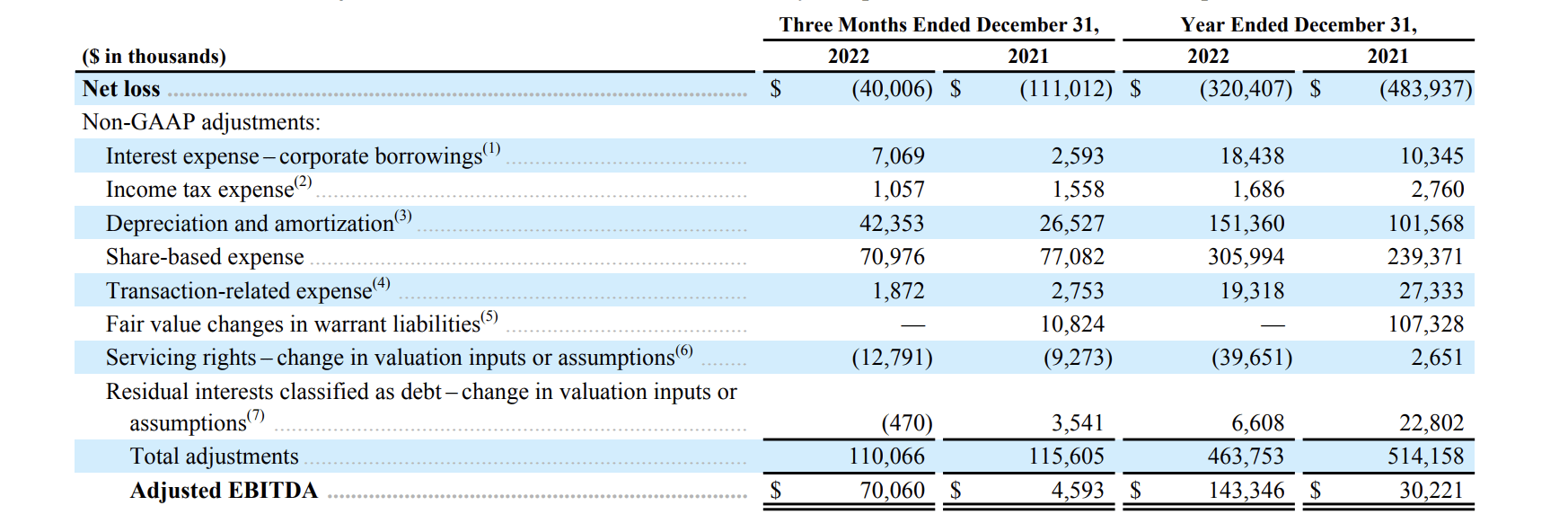

Source: SoFi Q4’22 earnings release

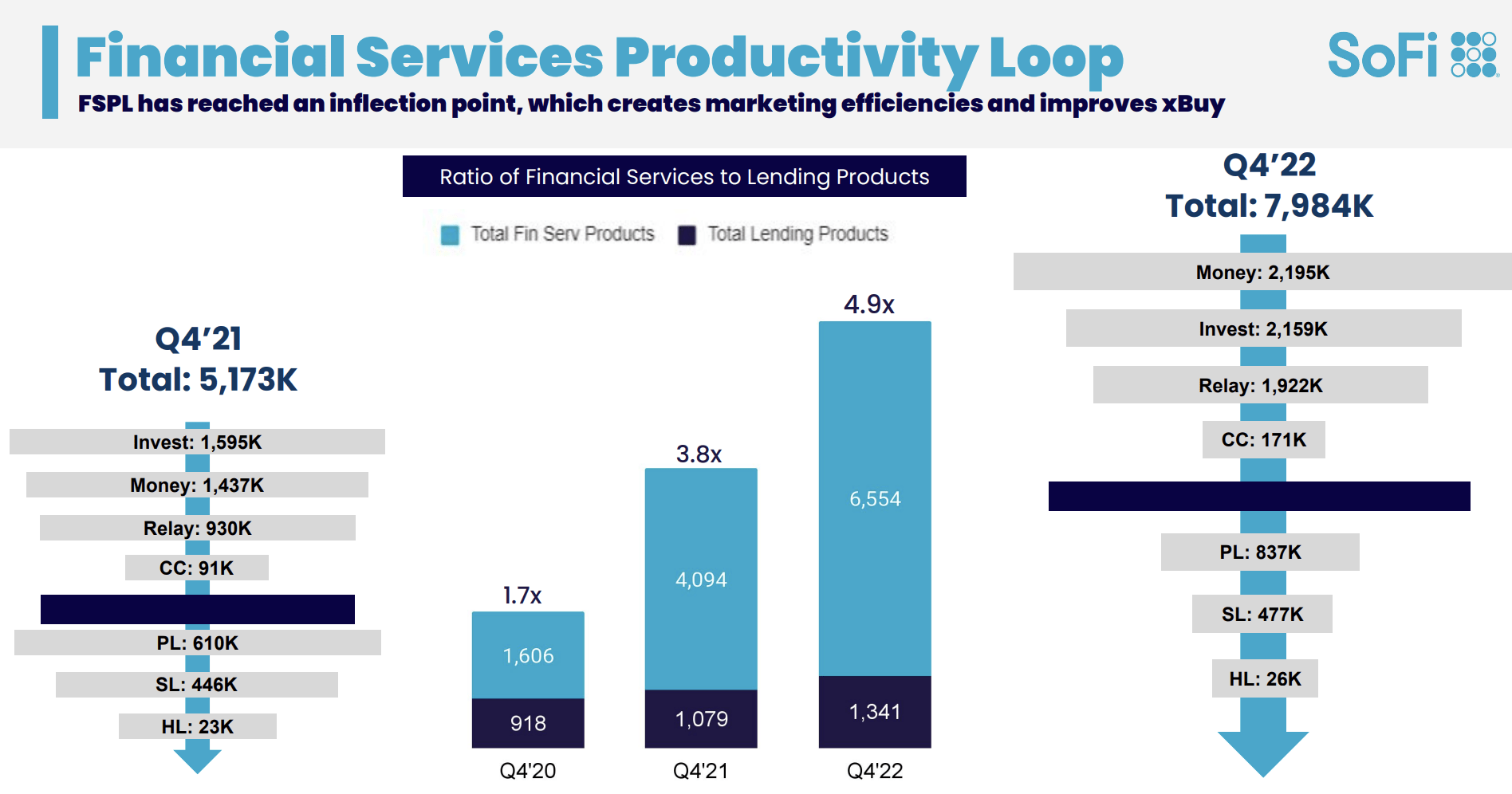

The prime reason SoFi has thrived despite the headwinds from the Biden Admin. pushing out the student loan moratorium is their marketing machine. The Financial Services Productivity Loop (FSPL) strategy now takes new members via lending products and turns them into a member using nearly 5 financial services products, such as credit cards and investment accounts.

Source: SoFi Q4’22 presentation

Financial Services revenue surged 195% during Q4 to $64.8 million, up from only $22.0 million last year. Even the Technology Platform grew Q4 revenues by 61% to $85.7 million. SoFi continues to successfully transition to a financial platform far beyond the student loans refinancing beginning.

The amazing part of the story is that SoFi overcame a massive decline in student loan demand with originations down YoY by over $1 billion. The company saw personal loans surge over $800 million in Q4, but total loan origination volume was down $800 million in the quarter. The business grew at nearly 60% in the quarter despite this huge headwind in their primary revenue driver.

Party Isn’t Over

SoFi provided strong guidance for 2023 sending the stock much higher. The fintech provided the following numbers for the year ahead:

- Q1’23 revenue: $430 to $440 million, up 34% to 37%

- Q1’23 adj. EBITDA: $40 to $45 million, up 360% to 417%

- 2023 revenue: $1.925 to $2.0 billion, up 25% to 30%

- 2023 adj. EBITDA: $260 to $280 million, up 81% to 95%

The company guided to quarterly GAAP net income profitability by Q4’23, but investors are far better off focusing on the adjusted profits picture. The adjusted EBITDA number corresponds very closely to adjusted profits providing a solid metric for basing the stock valuation.

SoFi guided for 2023 adjusted EBITDA to nearly double to $270 million this year. The stock has a market cap of ~$6.2 billion based on 923 million shares outstanding. SoFi only trades at 23x EBITDA targets despite the management team guiding to nearly 100% EBITDA growth for the year and analysts forecasting to targets topping $400 million in 2024.

Remember, SoFi still has major headwinds as the Biden Admin has taken the student loan forgiveness plan to the Supreme Court. The U.S. Secretary of Education Miguel Cardona proposed some new rules to reduce the cost of federal student loan repayments for low- and middle-income borrowers.

At some point during the year, student loan repayments should begin pushing students to refinance with SoFi. All of those new loans will feed into the marketing machine with the fintech signing up these new members into additional financial products over time.

Takeaway

The key investor takeaway is that SoFi remains far cheap for the growth opportunity ahead. The fintech has a great marketing machine that turns new members into customers with 5x the products.

The stock shouldn’t trade at only 23x 2023 adjusted EBITDA targets knowing SoFi has substantial growth in the years ahead with the headwinds of the student loan moratorium ending at some point.

Be the first to comment