The social media space has been decimated during the market collapse on fears that ad revenue from small and medium businesses will not only disappear in the short term but never return in the future. Due to ongoing free cash flow losses, Snap (SNAP) remains the stock at most risk of a protracted slowdown. My investment thesis wanted investors out of the stock up at $17 and the relative value proposition hasn’t gotten any better with the dip to $10.

{kind=link}

Mounting Losses

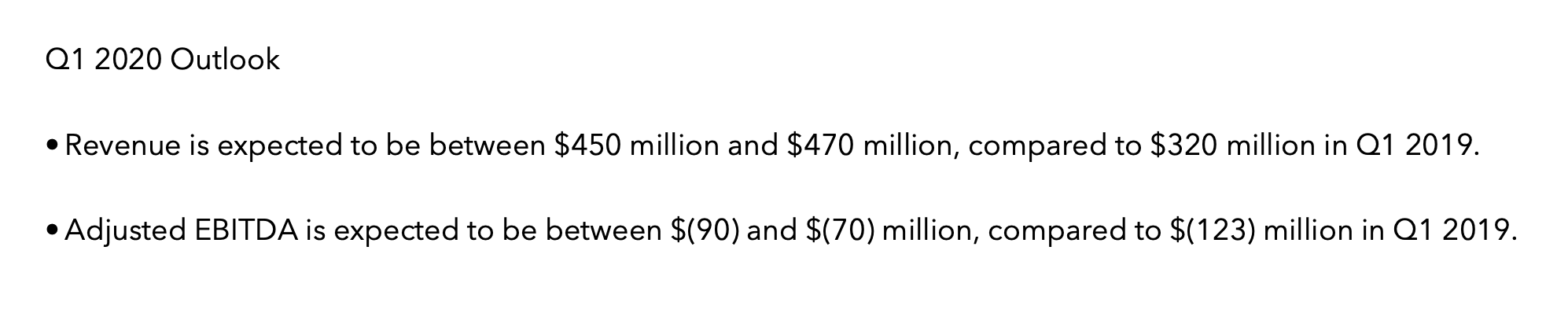

The easy story here is that Snap is cash flow negative and the coronavirus outbreak is only going to make these numbers worse. The company already guided to an adjusted EBITDA loss for Q1 of at least $80 million.

Source: Snap Q4’19 presentation

These numbers were based on revenues growing up to 45%. All of this growth might be over for now. Snap forecast revenues growing $140 million over last Q1 with the EBITDA losses improving by $43 million.

The numbers suggest a $100 million boost to operating expenses year-over-year and Snap might not see revenues rise at all. The EBITDA loss in Q1 and especially Q2 could exceed the levels from 2019 vs. the expected improvement. Snap had a combined adjusted EBITDA loss of $202 million in first half 2020.

The balance sheet is solid with a cash balance of $2.1 billion while Snap does have convertible notes of $892 million. The net cash balance is ~$1.2 billion.

Source: Snap Q4’19 earnings release

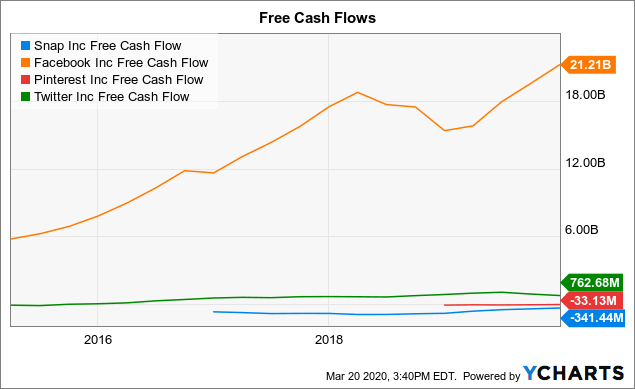

The company burned free cash flow of $341 million last year. An investor can probably make an easy assumption that Snap won’t improve cash flows in 2020. Just a repeat of this cash flow loss in 2020 and the company would see the net cash balance dip close to $800 million.

A doubling of the cash burn due to a protracted recession and Snap could end the year with a net cash balance of closer to $500 million. Of all the social media stocks, Snap is the least prepared for a downturn having not solved how to generate profits in the booming 2010s. At the end of the crisis, the social media company could be very far from breakeven again.

Not Even The Cheapest

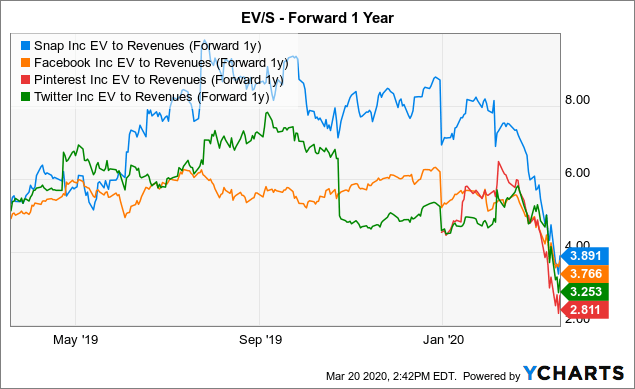

The worst part of the investment story for Snap is that all the other social media stocks are cheaper. Facebook (FB), Pinterest (PINS) and Twitter (TWTR) all trade at lower forward EV/S multiples.

Data by YCharts

Data by YChartsThe relative multiples are remarkable due to Facebook having $55 billion in net cash and Twitter having enough cash to recently agreeing to utilize $2 billion for a share buyback. Both of these companies are likely taking advantage of the downturn to reduce the diluted share count.

Clearly, Snap isn’t richly valued here at an EV of only 4x ’21 sales, but the stock doesn’t offer the relative value of the other stocks, nor does the company offer the balance sheet to protect investors from a protracted downturn in ad revenues. Facebook and Twitter don’t have any concerns regarding cash and Pinterest was projected to generate a positive EBITDA this year.

The best stock to own always is the one with the lower risk and better value. In a quick economic rebound, all of these stocks will bounce back anywhere from 50% to 100%. The typical EV/S multiple was closer to 6x in a more normal market. The easy way to avoid this risk is to own the social media stocks without cash flow issues.

Data by YCharts

Data by YChartsTakeaway

The key investor takeaway is that Snap is the one social media stock to avoid due to obvious cash flow issues. All of the stocks in the sector should rebound sharply on a quick economic rebound, but Snap remains the one at higher risk in a protracted economic downturn. Invest in the social media stocks with a lower risk profile due to better cash flow situations.

Looking for a portfolio of ideas like this one? Members of DIY Value Investing get exclusive access to our model portfolios plus so much more. Signup today to see the stocks bought by my Out Fox model during this market crash.

Looking for a portfolio of ideas like this one? Members of DIY Value Investing get exclusive access to our model portfolios plus so much more. Signup today to see the stocks bought by my Out Fox model during this market crash.

Disclosure: I am/we are long TWTR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.

Be the first to comment