mihailomilovanovic

(Note: This article was in the newsletter on January 3, 2023.)

Simon Property Group, Inc. (NYSE:SPG) has repeatedly been hit by fears that have not materialized. Mr. Market appears to be at the stage of “throw them all out” based upon what might happen. But it has not happened yet, and this appears to have created a value opportunity that seldom happens with a company of the quality of Simon.

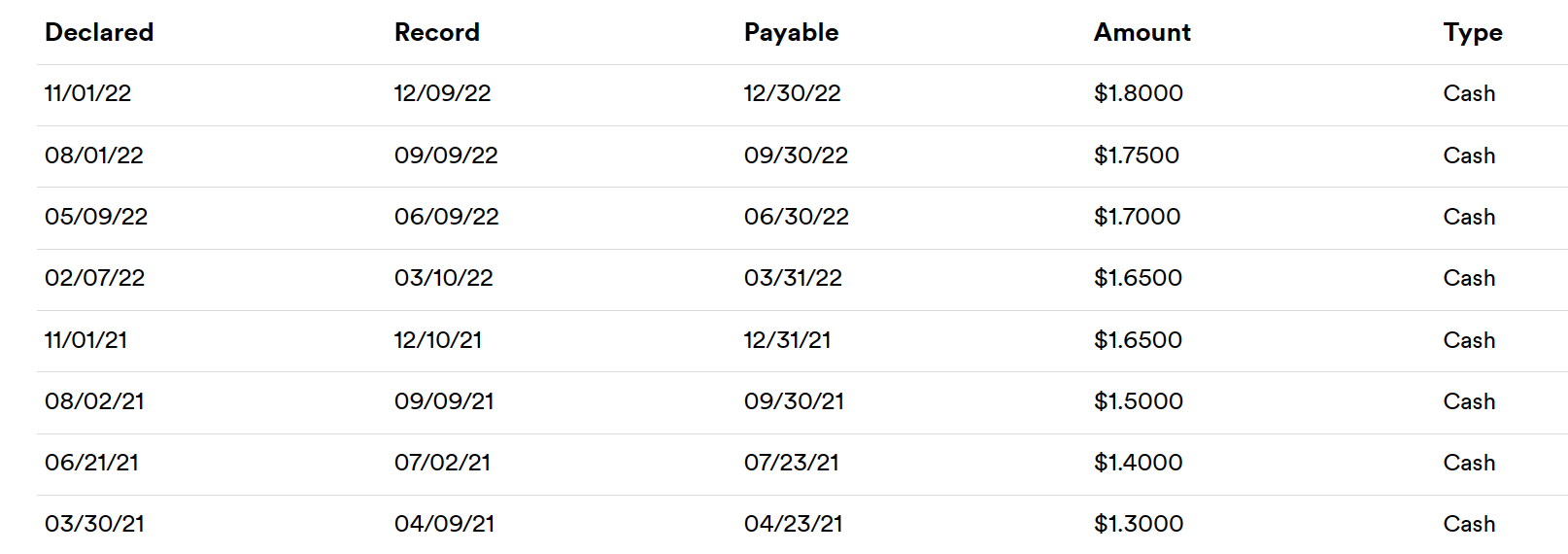

Simon Property Group Recent Dividend History (Simon Property Group Website January 2, 2023)

Management has been raising the dividend at a decent clip recently. That is in contrast to the stock price action. When the dividend goes up and the stock price goes down, the conditions for an above-average yield are present.

Management had cut the dividend due to pandemic considerations. Before that, there was a cut around the financial mess of 2008. Each time management has been recovering that cutback at a pretty good clip despite market fears.

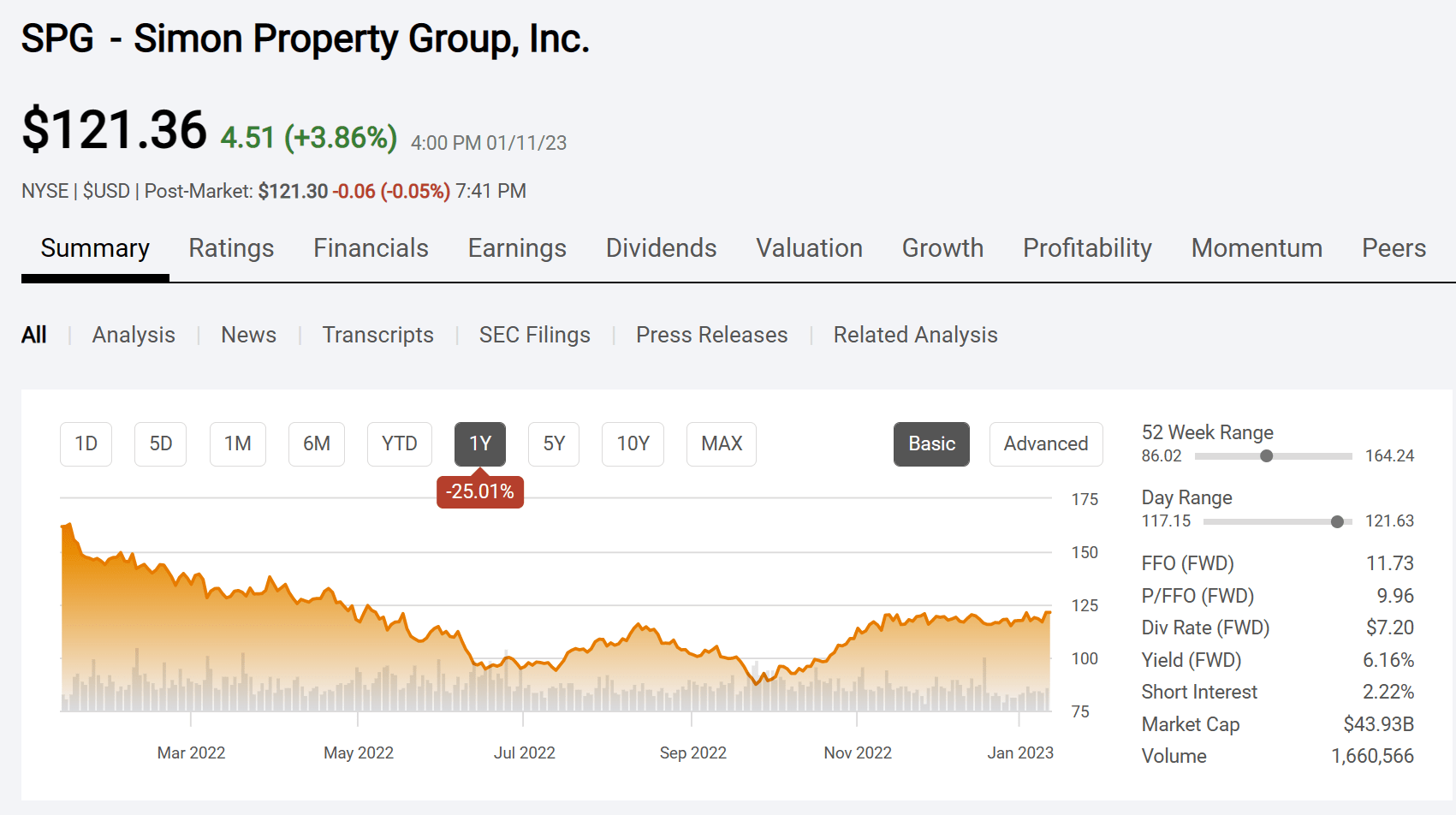

Simon Property Group Common Stock Price History And Key Valuation Measures (Seeking Alpha Website January 11, 2023)

It should be no surprise that the yield on the stock has now climbed to 6%. With management well on its way to restoring the dividend to previous levels, future yields on the current price look enticing.

Now, many of the companies I follow, including this one, still have some work to do to fully recover from the pandemic. However, the stock price clearly is reacting to new fears of yet another set of challenges that have really not materialized yet.

There is an old saying that the safest dividend is one that has just been raised. With a company of the stature of Simon, that is likely to prove true. If that is the case, then the company has more good news ahead. The fears that have knocked the stock price down about one-third from its high price this year are likely to prove unwarranted.

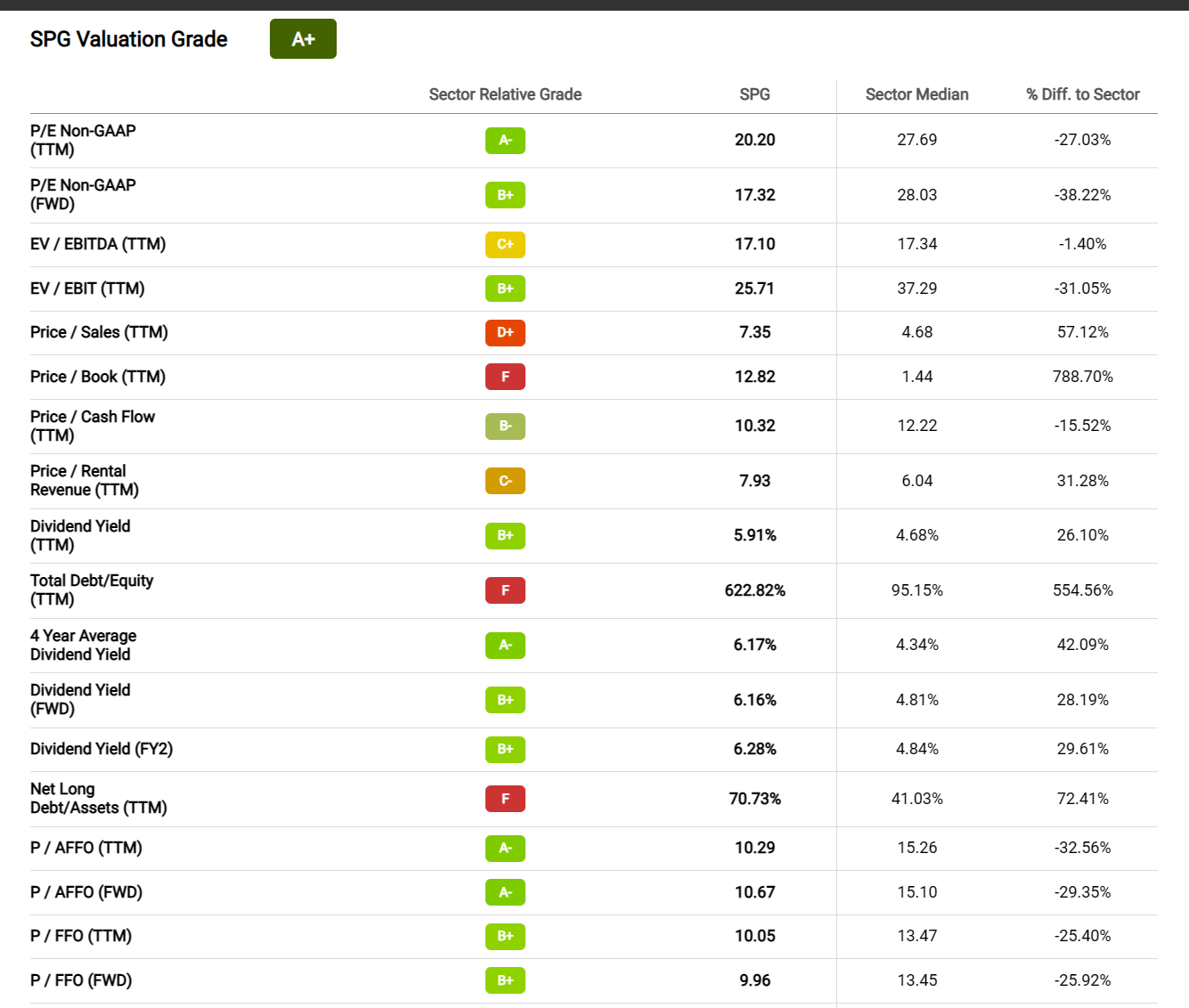

Simon Property Group Valuation On Seeking Alpha Website (Seeking Alpha Website January 11, 2023)

Similarly, it is clear from the Seeking Alpha valuations that the Simon Property Group, Inc. business has not suffered to the extent that the market has feared. The result of that is that SPG stock is not at bargain levels by several measures.

The forward price-earnings ratio shows a bargain, as does the dividend yield. Actually, the dividend yield is the highest I have seen for this quality issue in quite a few years. The four real estate investment trust (“REIT”) measures at the bottom point to a rare and very positive situation for a quality stock like this one. It is not often that an issue like Simon goes “on sale.”

This company has an investment grade rating. So, the debt level evaluation is not real scary to me. This company is a REIT. Therefore, debt levels will be typical than the usual company against which this company is measured. What is pertinent is that the value of the company is at a low by many measures shown above.

So many investors believe that to make a killing, one needs to find financial leverage and usually even more risk. But the recovery potential of a good (investment grade) company like this one where business appears to be doing well enough that the dividend is constantly raised, could rival the riskier investments without the risk.

The safest time to buy a solid company like Simon is when it is out of favor. Then, even if a dividend cut were to unexpectedly happen, it is already factored into the price (as a rule). That is why the low expectations provide a considerable safety cushion for downside protection. Many times, there is negative press coverage that makes an investment like this look risky. But really, the press coverage usually follows a stock down. Only rarely does the press coverage lead a stock decline. So, the negative current environment towards Simon Property Group stock is an excellent contrary indicator.

The Business

The market has worried endlessly about what the rising interest rates and Federal Reserve monetary tightening moves would do to the business of REITs. So far, those worries have proven to be unfounded for Simon Property Group, Inc.

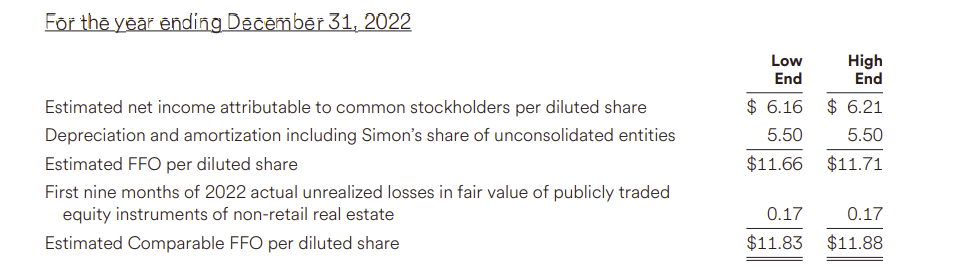

Simon Property Group Revised Upward Guidance For The Fiscal Year (Simon Property Group Third Quarter 2022, Earnings Supplemental Materials)

The stock price action has clearly ignored management guidance that resulted in the upward revision (by a couple of percentage points) shown above. Probably the fears of a recession need to abate before the stock price responds, and that could take a few months.

But a recession is nothing close to what faced the company and the country in fiscal year 2020 with the pandemic challenges. Even if we officially get into a recession, this recession currently appears to have one of the highest economic activity levels on record. As a result, this may be one of the easiest recessions for companies to get through.

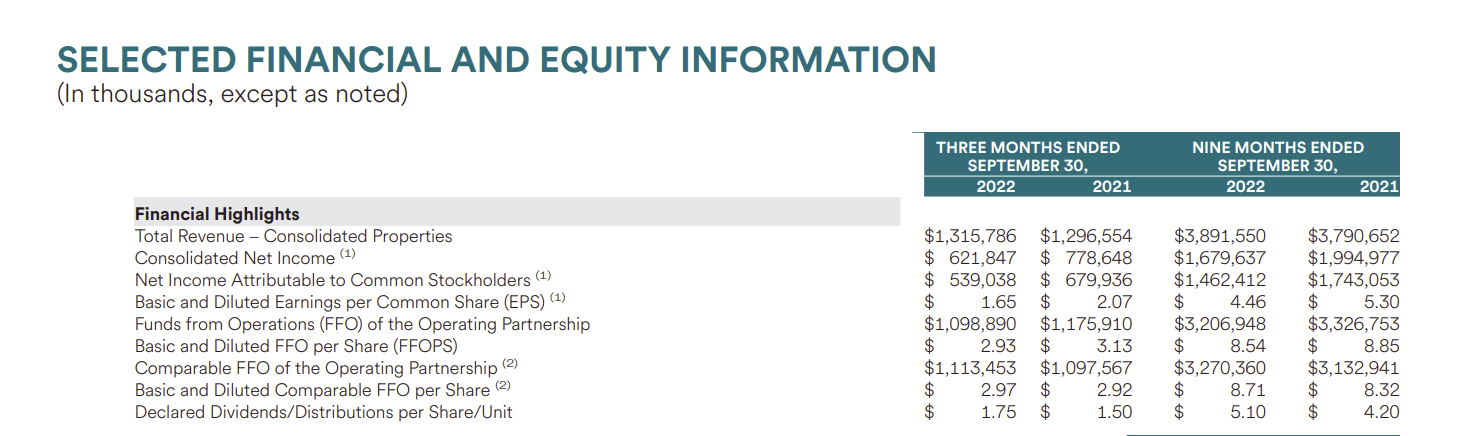

Simon Property Group Key Financial Data Summary (Simon Property Group Supplemental Release Third Quarter 2022)

The bears will note that earnings comparisons were negative by omitting the fact that there were nonrecurring gains in the previous year. That is kind of a typical thing to do for the bear case. But as shown above, recurring operations are making progress at a time when the stock price clearly does not expect that progress.

Simon Property Group, Inc. has a financial rating of A- from Standard and Poor’s. As the largest operator of its kind, there is considerable geographic diversification behind that rating. Any feared problems will likely be met with considerable financial resources that outweigh many in the industry.

One of the things about a high financial strength rating is the ability to recover fast during industry recoveries and perform better during the good times. This gives a contrarian a measure of long-term safety that may not exist with a lower rated or smaller operator.

Going Forward

Simon is diversified enough to withstand just about anything short of a depression. Even if the worst happens, the finances are rated high enough to deal with that as well.

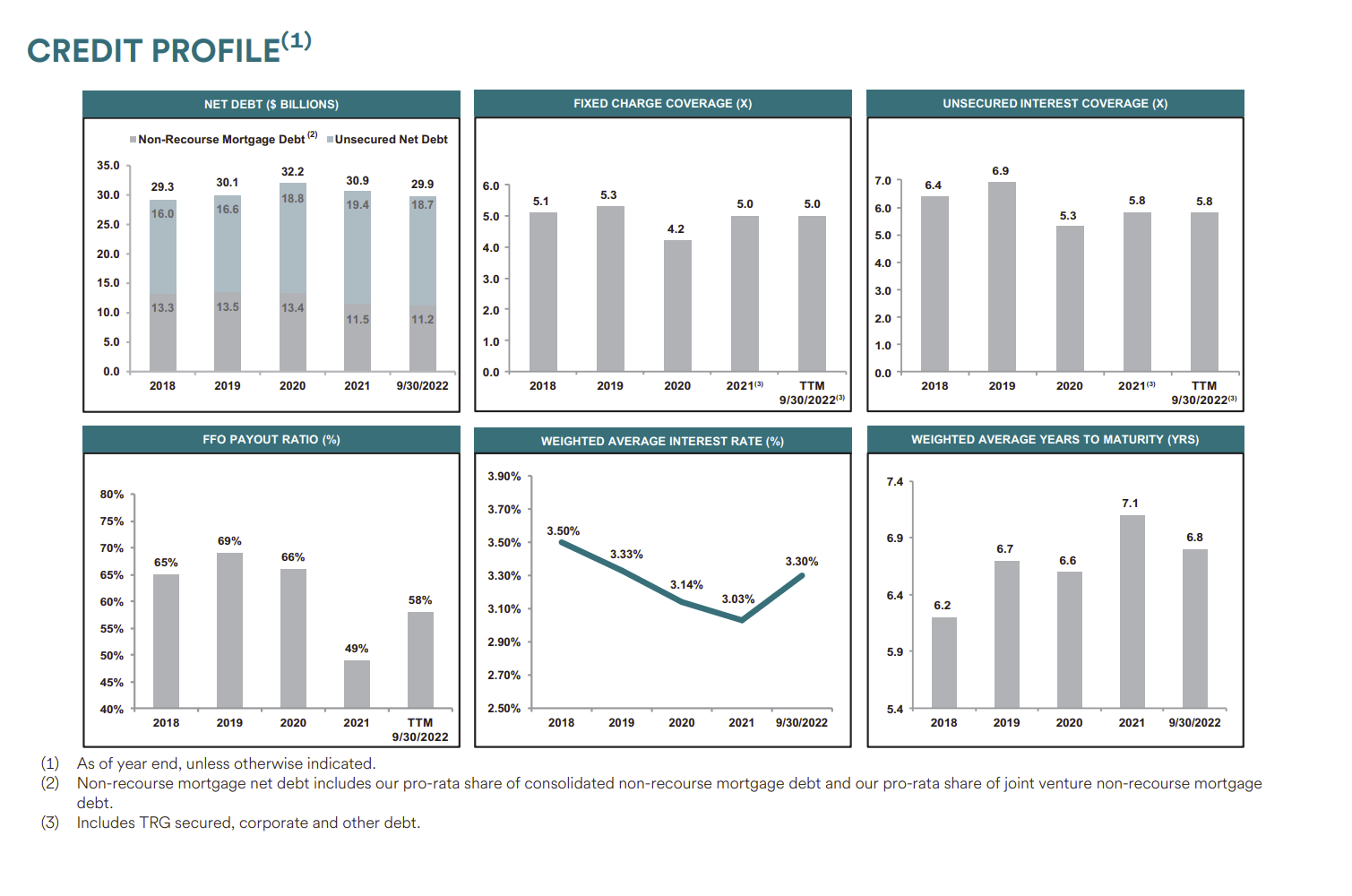

Simon Property Group Credit Profile (Simon Property Group Third Quarter 2022, Supplemental Materials)

Notice that even with the recent acquisition the amount of debt is about the same as it was a few years ago. The payout ratio remains one of the lowest of all the REITs that I follow. Management chose a deliberately conservative course when cutting the dividend. Any time there is a challenge like a recession or covid challenges, this management tends to be very conservative about dividend payments. That also means that the money is there for that dividend in the future.

There is a huge difference between cutting the dividend because there are serious financial issues ahead and cutting the dividend “just in case.” The conservative course preserves balance sheet strength and the financial ratings. That keeps the interest costs down at the expense of some current income. When the worries blow over, conservative management can easily restore the dividend.

So, as the current inflation expectations extinguishment runs its course, Simon Property Group management will be able to restore the dividend and will likely be able to go higher. All that is required is shareholder patience. The key ratios shown above have really not suffered at all. The fact is that should the ratios deteriorate, they would be deteriorating from a very high level before there is really any shareholder worries about the business. That is how you can tell when the market is overreacting. This is still one very high-quality issue with a well-covered dividend.

As inflation concerns ease, SPG stock should return to at least $150, which provides a generous return from the current price for what is usually seen as an income investment. When combined with some more likely dividend increases, this may be one of the best income deals out there at the moment.

Simon Property Group, Inc. management at some point will resume the usual slow growth with an occasional opportunistic acquisition. In the meantime, a wide variety of investors can take the opportunity to buy a very good quality stock such as Simon Property Group, Inc. at bargain levels.

Be the first to comment