VioletaStoimenova

There are a lot of interesting companies that are tied to the crypto industry that are currently trading at attractive valuations. I think both Silvergate Capital (SI) and Signature Bank (NASDAQ:SBNY), who are both banking service providers to said industry, are in that group. Silvergate is under a lot more pressure, as I’ve written about recently when it dropped 45% in a day. It appears more attractive from a valuation standpoint, but in some major backlash scenario from regulators, it could also suffer a lot more. Signature has a more diversified customer base and is doing some exciting things in the traditional banking.

Yesterday both banks reported earnings. I’ve published notes on Silvergate for subscribers (I’ll release a public version later.) Even though I’m not involved with Signature, it is beneficial to compare and contrast these earnings calls and the situations these banks are in. I’ll go over a few select quotes from the Signature call, add emphasis on essential sentences and provide my general takeaways from the event.

I’ll say upfront, as a Silvergate shareholder, I thought the Signature earnings call was very well executed and its management team made a much better impression. I’m not sure why but possibly it is because Silvergate is 1) much more dependent on the crypto industry 2) under a lot of pressure due to a short-selling campaign.

On December 6 Signature announced its plan to decrease total deposits in the digital asset banking space by reducing the size of relationships. This strategy results in a more granular deposit base, which leads to greater stability in this funding source.

I didn’t love that announcement. I still think it is a peculiar tactic. They should take the deposits but make sure they are making enough money off these customers to offset the volatility associated with their deposits. With short-term rates where they are, this should be doable.

On the call details of the plan became available and the narrative of Signature bank leaving the space proved extremely exaggerated:

As part of the plan, we are focused on reducing high-cost excess digital deposits. Our strategy when is expected resulted in a decline of $7.4 billion in digital deposits. Prospectively, the bank will further reduce these digital deposits by an additional $3 billion to $5 billion by the end of 2023, however, most likely much, much sooner.

If I’m not mistaken, Signature should still have something like $15 billion in digital asset deposits remaining after it cuts unprofitable clients loose. The CEO also said this:

Yes. We’re committed to the business. We think that it’s not going away. Let’s put it this way. It’s not going away. And we have a number of examples that show that it’s not going away. If you think about the government, if we could get the regulators and Congress on the same wavelength, they would give us regulations that we could follow and then others could follow. What this ecosystem needs is regulation. We need to be able to function where the economy is confident. Having this FTX situation clearly put a lot of confidence in that ecosystem.

Now what we need to do is to get regulation, get confidence back in the system and we can go from there. It occurs to a lot of people that when you do innovation, you always – in the initial part of the innovation, there’s always looked upon initially down upon. And that’s what I think is the situation here. There’s new financial innovation is being looked out upon. And we believe that somewhere in the next few years, the banking system as it conducts transactions today will not be the way they conduct transactions tomorrow. So we’re very much in tune to wanting to support this ecosystem.

There was also a very important question from an analyst about the BSA, AML and KYC processes of the bank in light of the FTX implosion. The Signature CEO gave a great answer (in contrast to the Silvergate team) and said the following:

Well, I’ll say this with FTX, it wasn’t a matter of BSA AML. Everyone thought that he was [indiscernible] and he ended up being very made offline(author: the transcript should likely say “Madoff like”). So I don’t think anyone could say that they knew that, and we catch it. What we’re talking about regulation is we just want to know which way you go because we had Signet and we try to make enhancements on it, and some were okay by the regulators and some were not. It puts us in a difficult position as to what we do – what do we do next? And not knowing regulation-wise what’s going to happen puts us really at behind everyone else that is in the crypto world.

I will tell you this. We’ve had – we’ve had a number of discussions with the regulators, and they seem to be waiting for other regulators. So I don’t know if the Fed is waiting for the FDIC. The FDIC was waiting for the OCC. But I think they have to get together, meet with Congress because Congress was going to put some before the end of the year. Congress is going to put some of those across to get some loss put on the books for regulation. And they were not things that we thought were good for us or good for the industry.

So we need to get them to get on the same level of field and give us some guidance. There’s no – I think what happens is when the regulations come out, that will eliminate a number of players. I don’t know if [indiscernible], but I would say a number of players couldn’t want to look to the regulation, whether it’s capital integrate or just doing AML DSA. But again, FTX was not a BMA AML. It was a Bernie [ph] made of like a situation that no one really thought that Sam [ph] was a bad asset.

The CEO is basically inviting clear regulation but also saying FTX was not a BMA AML problem. He’s saying FTX was likely a fraud and these processes don’t tend to stop fraud. If you are running a Ponzi scheme (like Madoff was) you are probably not too bothered by giving banks information that isn’t correct.

I pulled up a table of peer valuations through Seeking Alpha. I replaced the fifth listed competitor with Silvergate because I know it is an interesting comparison. The others are all U.S. banks with a market cap similar to Signature (between $6 to $8 billion). I’ve emphasized metrics I think are most important:

|

SBNY |

ZION |

WAL |

WBS |

PB |

SI |

|

|---|---|---|---|---|---|---|

| P/E Non-GAAP (FY1) |

7.64 |

9.11 |

6.66 |

8.45 |

13.05 |

8.19 |

| P/E Non-GAAP (FY2) |

6.74 |

7.67 |

6.00 |

7.03 |

12.15 |

8.82 |

| P/E Non-GAAP (FY3) |

– |

7.66 |

5.46 |

6.59 |

11.59 |

7.21 |

| P/E Non-GAAP (TTM) |

5.83 |

9.82 |

6.89 |

9.00 |

13.30 |

3.62 |

| P/E GAAP (FWD) |

7.63 |

9.07 |

6.66 |

12.46 |

13.03 |

15.54 |

| P/E GAAP (TTM) |

5.84 |

9.59 |

6.91 |

14.21 |

13.32 |

NM |

| PEG Non-GAAP (FWD) |

0.80 |

3.14 |

0.66 |

– |

0.65 |

NM |

| PEG GAAP (TTM) |

0.15 |

NM |

0.54 |

NM |

NM |

– |

| Price/Sales (TTM) |

2.88 |

2.63 |

2.95 |

3.75 |

6.01 |

NM |

| EV/Sales (FWD) |

– |

– |

– |

– |

– |

– |

| EV/Sales (TTM) |

– |

– |

– |

– |

– |

– |

| EV/EBITDA (FWD) |

– |

– |

– |

– |

– |

– |

| EV/EBITDA (TTM) |

– |

– |

– |

– |

– |

– |

| Price to Book (TTM) |

0.95 |

1.79 |

1.48 |

1.10 |

1.03 |

0.70 |

| Price/Cash Flow (TTM) |

5.87 |

6.66 |

3.38 |

6.46 |

11.68 |

1.84 |

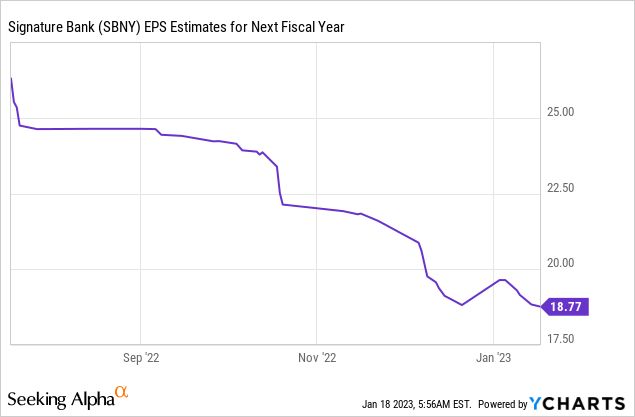

Price to book is likely the most important multiple. Both Signature and Silvergate trade at the bottom end of the range. On a forward P/E basis Signature trades very attractively as well. Earnings estimates have been coming down fast, so I do think analysts have been adjusting their numbers based on the crypto crunch:

What I really like about Signature is that they aren’t embedding crypto services within a regular run-of-the-mill bank. They are actively looking for customers (in other industries) that really benefit from a platform that allows them to move money 24/7 (as required by the crypto industry). They are servicing container shipping companies and growing in the payroll industry. It reminds me of the model of defense companies. Develop, and get funded by the DoD, military-grade technology. But after you have developed that technology, you can utilize the IP or platforms to service the private industry. I like how Signature has set things up, I think they are much more relaxed and that comes across on their earnings call.

At the same time, concerns about them exiting the crypto industry seem overblown and there’s nothing stopping them from growing this segment in a responsible way as the industry recovers. In terms of valuation, it looks really attractive compared to a set of normal small banks while it has an interesting upside angle through the Signature platform. I’m already overweight companies tangentially or directly exposed to the crypto industry, but after this call, I’m tempted to make room for Signature.

Be the first to comment