Stocks move for all sorts of reasons and you can never be certain what exactly contributed to the cause. Nonetheless, when a bullish or bearish thesis plays out flawlessly, one can attribute at least some price movement to that. When we first wrote a standalone article on Shopify Inc. (NYSE:SHOP), we told the bulls why they were about to be carted out on a stretcher.

The COVID acceleration in e-commerce was in our opinion, a pull forward of demand and not a source of new demand. In other words, by 2024 end, we will be back to exactly where SHOP revenues would have been, in the absence of COVID-19. What does that mean for the stock? Pre-COVID-19 we would have estimated a 40% growth rate for 2020 and a slowdown to 25% by 2024. That would get us to about $8.0 billion in revenues. That’s a massive gap vs. where consensus stands.

Seeking Alpha

That was our forecast very early in 2022 before the bubble began to unravel fully. SHOP also acquired Deliverr after that and obviously none of our forecasts included that. Deliverr is supposed to be growing far faster than SHOP as a whole based on management commentary. Now despite all that, just look where the 2024 estimates are headed.

Seeking Alpha

Why We Are Not Done Yet, Not Even Close To It

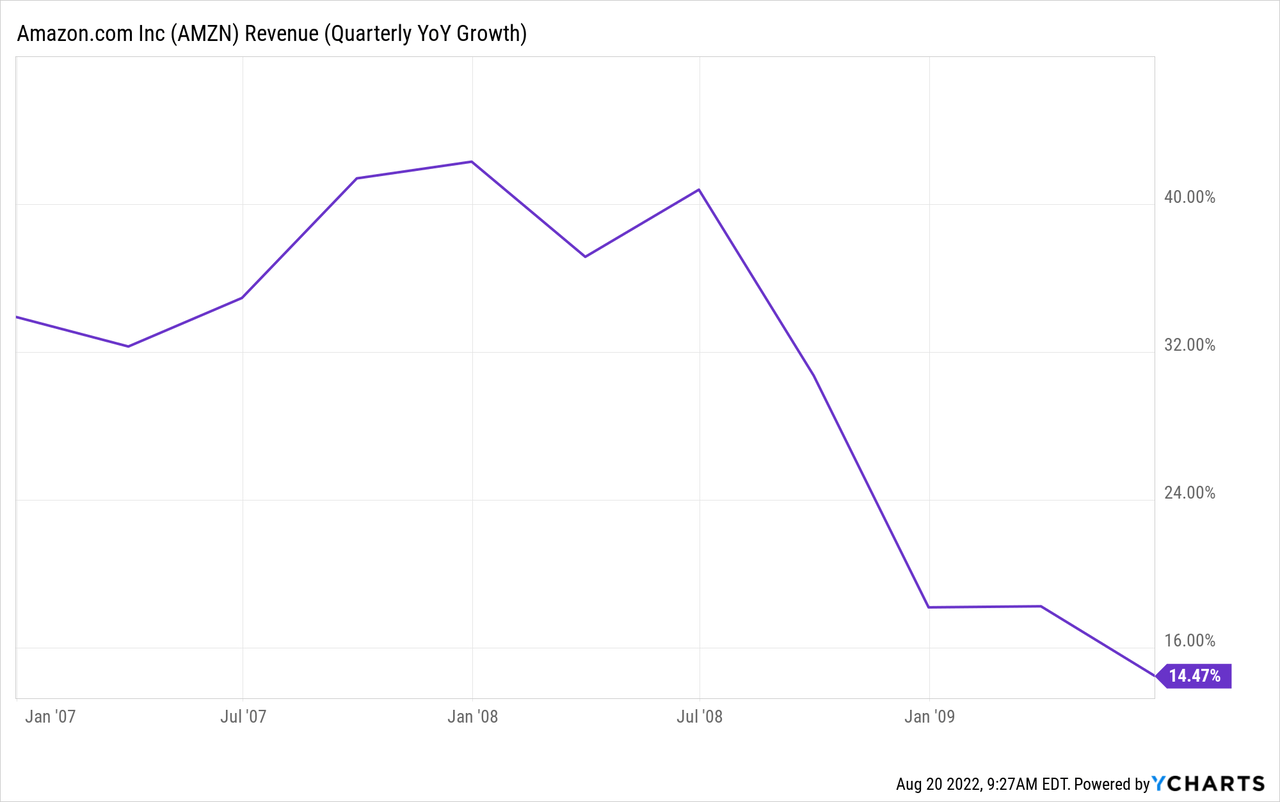

Bulls may cry about “what’s another $800 million between friends”? But with a recession likely on the horizon, SHOP’s challenges are about get far worse. We are about to get the dual forces of recession and payback for the pull forward, hit at the same time. Even without the second problem, we would forecast growth to move to less than 15%. Amazon Inc. (AMZN) was the fastest grower in e-commerce and slowed to 14% revenue growth during the global financial crisis.

AMZN Revenue (Quarterly YoY Growth) data by YCharts

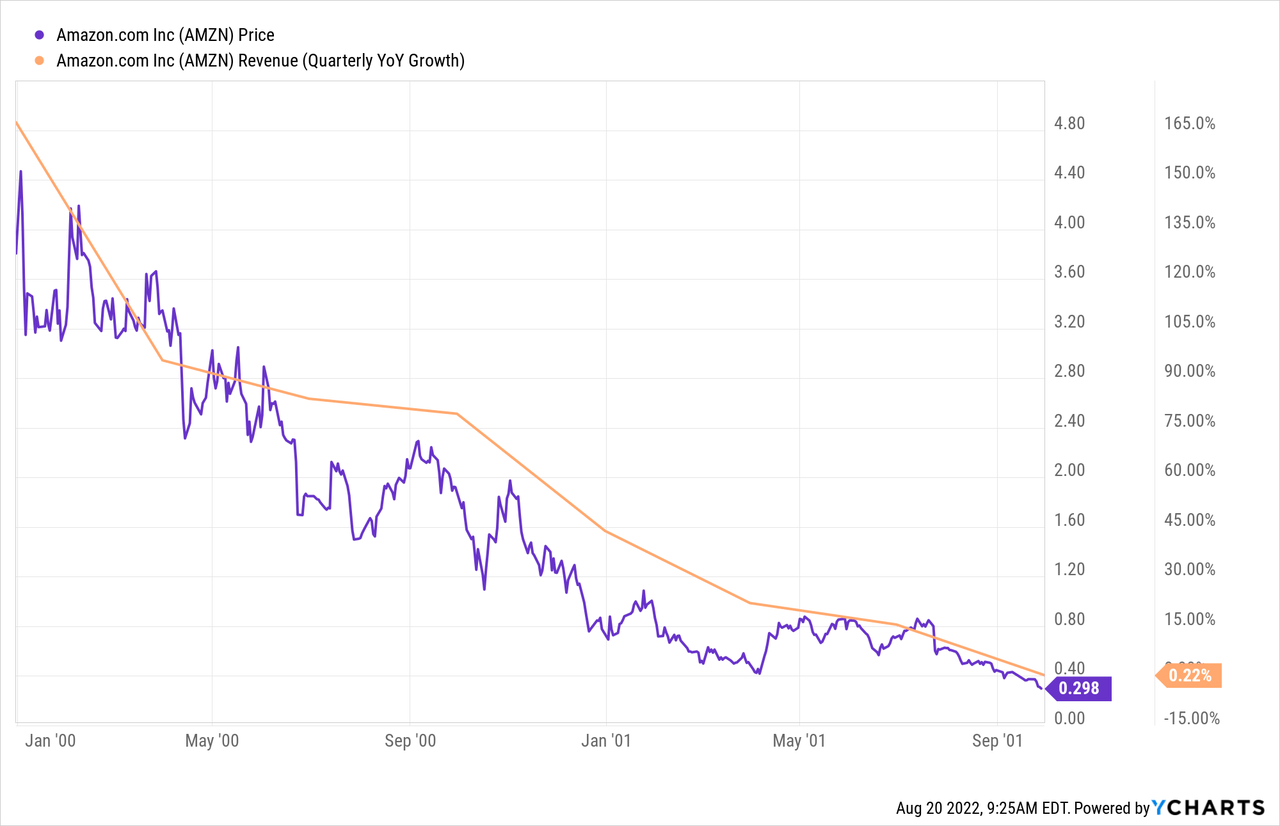

In 2001, growth came to stall speed and troughed at just 0.22% year over year.

AMZN data by YCharts

SHOP is different in many ways but that makes the position worse. There is likely to be far more competition this time around against the company. Our estimates here for revenues are as follows.

2022: $5.2 billion

2023: $5.7 billion

2024: $6.2 billion.

These may seem outlandish, but we already have one analyst at $6.64 billion in revenues for 2024, and as a rule, none of them tend to accurately price in recessions.

Valuation

Putting a valuation on loss makers is a murky exercise. We freely admit that. As a general rule, though, these tend to get extremely undervalued when the damage ends. Keep that in mind. With that said, we can make some guesstimates.

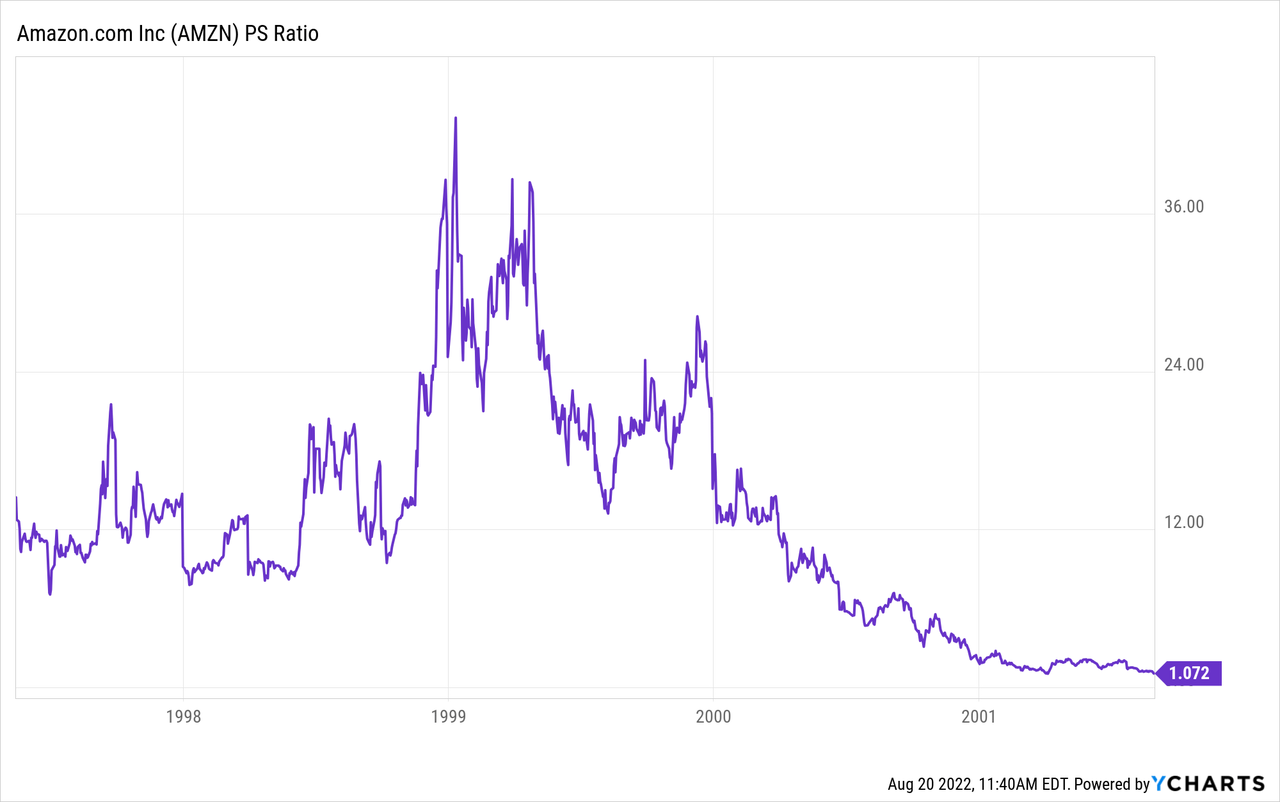

Many models tend to focus on price to sales (or EV to sales) and we think that is a good one to follow. AMZN, our former comparative, bottomed at 1X sales in 2002.

AMZN PS Ratio data by YCharts

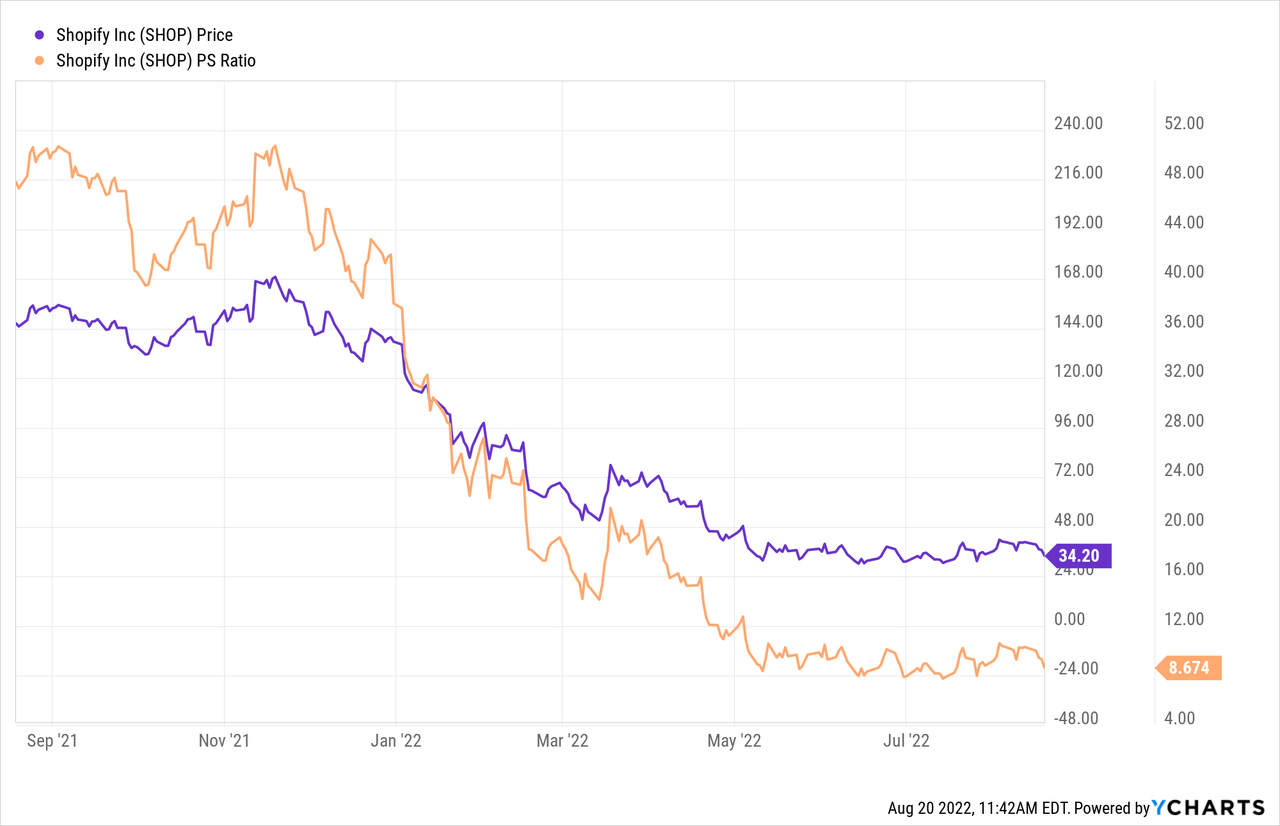

A similar number was seen in 2009. If SHOP hits the same in 2023, we would still see a very severe drawdown from here as it is at a stunning 8.6X sales.

SHOP data by YCharts

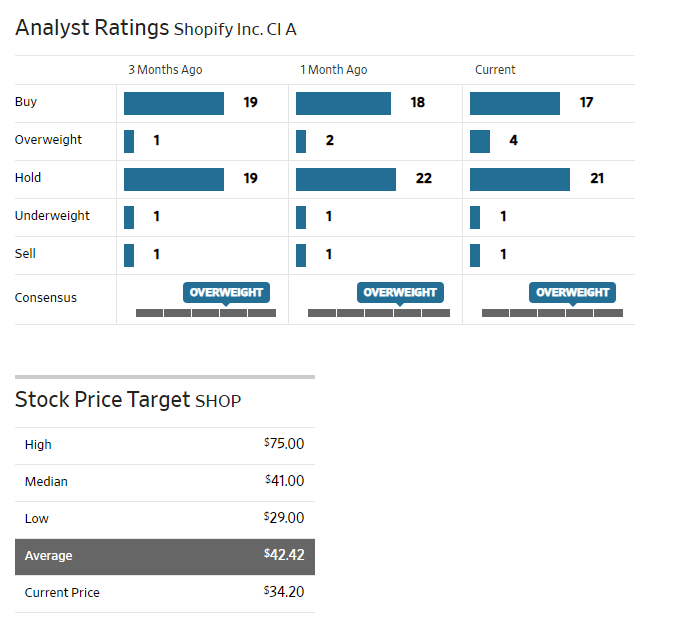

Most of the analysts are still using 6-7X revenue multiples, which are laughable if we do actually hit a recession. That is why the price targets are still sky high and the bulk of them have not thrown in the towel.

WSJ

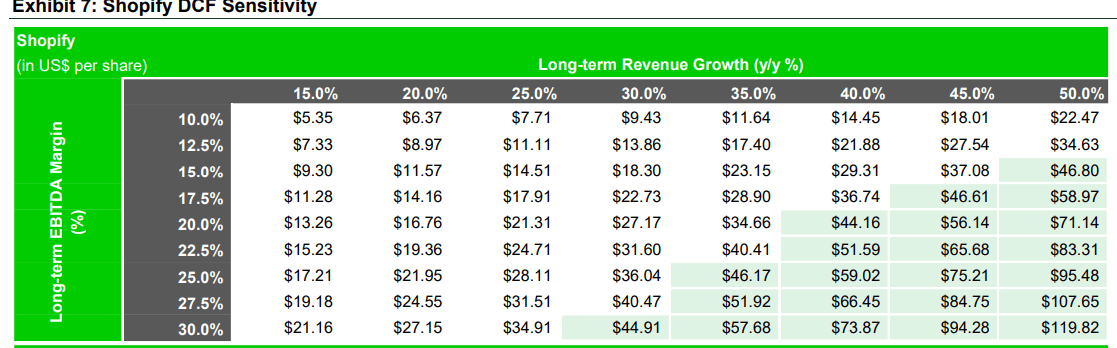

Another way to look at this is to see what they use to justify their 6-7X sales multiples for an unprofitable company. The Toronto-Dominion Bank (TD) analysts use a long term revenue growth rate of 30%-35% with an EBITDA margin of 20%-25% to support a 7X revenue multiple.

TD Research

What is weird about those numbers is that revenue growth is falling far below that and EBITDA margins in Q2-2022 were negative 2.5%. It is a very long and painful journey from negative 2.5% to positive 25%. Assuming SHOP can miraculously get to 15% revenue growth in 2023 and increase EBITDA margins to 10%, their model would call for $5.35/share. In fact, their model assumes that SHOP will grow in 2023-2026 faster (10% more, or 40% actual) than their long term growth rate.

Verdict

SHOP is the highest conviction case we have that we think investors should bail on. Like most epic bubbles, this one continues to draw dip buyers who think the stock is now “cheaper”. We cannot argue with the fact that it has gone down, but we are not close to being done. Investors buying here are likely to lose another 70% in our bull (yes that is correct) case of ending with 3X sales multiple.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment