US Dollar, Singapore Dollar, Thai Baht, Indonesian Rupiah, Philippine Peso, Indian Rupee, ASEAN, Fundamental Analysis – Talking Points

- US Dollar weakened against ASEAN currencies this past week

- Quiet week may open door to SGD, THB, IDR and PHP gains

- Bank of Indonesia is on tap, keep an eye on intervention threats

Discover what kind of forex trader you are

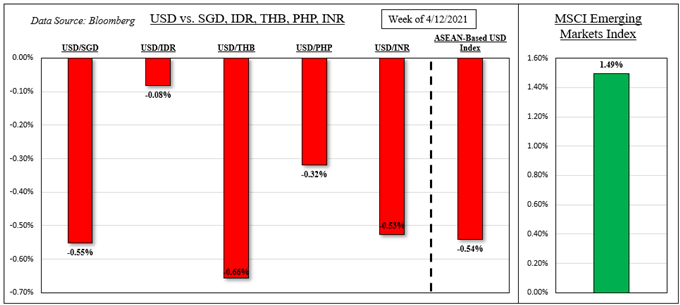

US Dollar ASEAN Weekly Recap

The anti-risk US Dollar experienced its worst week since early February when averaging its performance against a few ASEAN currencies. These include the Singapore Dollar, Indonesian Rupiah, Thai Baht and Philippine Peso. The focus for these currencies was likely on external developments. USD/SGD fell slightly after the MAS largely left monetary policy settings unchanged at its semiannual meeting. Meanwhile, the MSCI Emerging Markets Index (EEM) rallied about 1.5%, also the most since early February.

US Dollar, MSCI Emerging Markets Index– Last Week’s Performance

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

External Event Risk – Treasury Yields, Earnings Season, US Markit PMI

Similar to last week, the focus for ASEAN and developing market currencies in parts of the Asia-Pacific region will likely remain on external event risk due to the importance of capital flows. This past week, all eyes were on US Treasury yields. It was the worst 5-day period for the 10-year rate since the beginning of December. This was despite higher-than-expected US inflation and retail sales data.

Ongoing dovish commentary from the Federal Reserve likely continued pouring cold water on hawkish monetary policy expectations. Market implied odds of a rate hike by the end of 2022 dipped to about a 50-50 split, down from roughly 90% confidence at the beginning of this month. As a result, the US Dollar weakened, cooling concerns about foreign debt repayment costs in Emerging Markets.

Month-to-date, Thailand stock exchange foreign net investment surged to its highest in about a month as USD/THB turned lower. As such, continued weakness in Treasury yields may benefit ASEAN currencies and Emerging Markets. The week ahead is relatively quiet in terms of economic event risk, allowing markets to marinate on recent broader fundamental themes.

Still, US earnings season is in full swing. Thus far, surprises have been rosy and more of the same may continue pressuring USD. Notable companies reporting ahead include Intel and Netflix. US Markit manufacturing PMI is also on tap, but a rosy outcome could fail to inspire much of a reaction from bond markets if the Fed is adamant about standing by on policy for the time being.

Recommended by Daniel Dubrovsky

How can you overcome common pitfalls in FX trading?

ASEAN, South Asia Event Risk – Bank of Indonesia, USD/IDR

Focusing on the ASEAN economic event risk, the Bank of Indonesia interest rate decision is on April 20th. Benchmark lending rates are expected to be left unchanged. Rather, USD/IDR will be closely eyeing commentary about the exchange rate. Bank of Indonesia continues to see its currency as undervalued and may reiterate its view, pressuring the pair lower.

Check out the DailyFX Economic Calendar for ASEAN and global data updates!

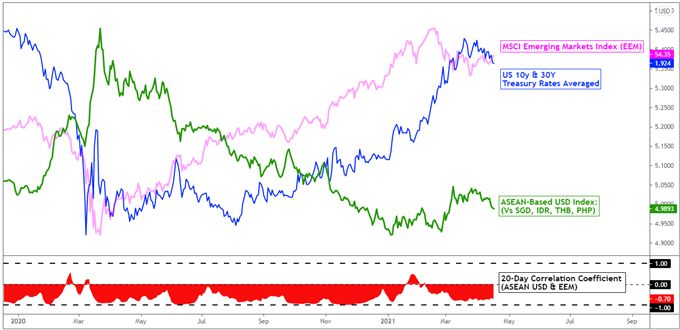

On April 16th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets index changed to -0.70 from -0.72 one week ago. Values closer to –1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-Based USD Index Versus EEM and Treasury Yields – Daily Chart

Chart Created Using TradingView

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP

— Written by Daniel Dubrovsky, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter

Be the first to comment