Lari Bat/iStock via Getty Images

Investment thesis

The last 3-to 4 months (since I published an article about SAR) have been rough in terms of price appreciation if you already held a position in Saratoga Investment Corp. (NYSE:SAR) and watched your position closely. But if you are about to execute a buy position, it is time to do so. The management continued the debt restructuring in January and I am certain they will continue to do so in the near future by redeeming high floating rate notes and issuing fixed-rate notes instead. NAV grew in the last 4 months, and Return on Equity slightly grew. The company has a better valuation than in December (partly because of the general market downturn). It is trading at a better dividend yield and due to the first interest rate rise in March, the broader economic environment is turning in SAR’s favor.

Portfolio structure

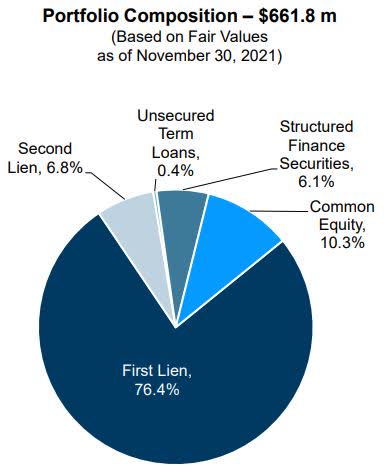

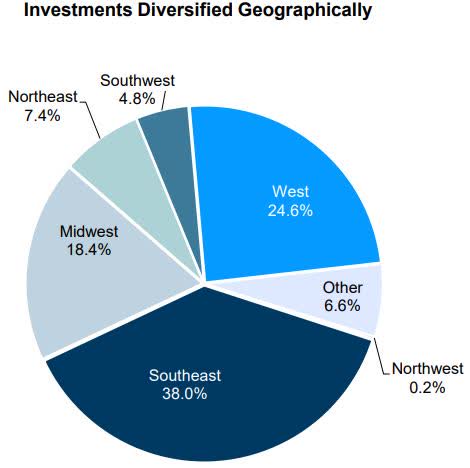

Saratoga Investment is one of the 49 publicly traded business development companies that provide customized financing solutions for middle-market companies located in the U.S. The company focuses on firms that have EBITDA of $2 million or greater and revenues of $8 million to $250 million. SAR invests through direct lending as well as participation in loan syndicates. Three-quarters of its portfolio consists of first-lien loans and the management likes to not only be on the top of the capital stack but if possible, make additional money from its equity holdings beyond the interest payments on loans. Their riskiest holdings are the Structured finance securities but the 280 basis point risk premium to first-lien loans could justify their part in SAR’s portfolio. Their total portfolio is well-diversified geographically and I am not expecting any significant change in the upcoming years.

2022 Q3 Shareholder Presentation Q3 2022 Shareholder Presentation

Financials & Earnings

Q3 results

SAR has continued to perform well in its third quarter. The ROE grew from 14.4% ttm in Q2 to 14.6% ttm by Q3 2021. The total net assets grew by 5.71% and the fair value of the investment portfolio also slightly grew compared to second-quarter results. SAR’s loan investments held in performing credit ratings remained strong (95%) compared to year-on-year data (92.8%) and second-quarter results (93.2%). The net investment income decreased from Q2 to Q3 by approximately 21.1% but grew on a year-on-year basis by 12.5%. The reported NII per share was $0.45.

The debt restructuring has been accelerated as the management wants to secure SAR’s place in a rising interest rate environment. By January 19th SAR closed a public offering of $75 million 4.35% notes due 2027. The final yield to maturity will be approximately 4.5%. This will be highly advantageous to SAR with expectations that by the end of 2022 the fed funds rate could be realistically 1.5-1.75%.

Earnings statistics

SAR will announce its fourth-quarter results on May 3rd, 2022, after market close and has an EPS estimate of $0.54. In the last 10 years, SAR outperformed the EPS estimates 79% of the time and only underperformed the previous estimates 21% of the time. The biggest price drop after a worse than expected earnings was 3.97% and the average price drop after a worse than expected EPS is 2.91%. So now you can see the statistics and decide if this risk is too much for you to take a position in SAR before the next earnings results in May or not. (These numbers are based on standardized EPS.)

Debt profile and valuation

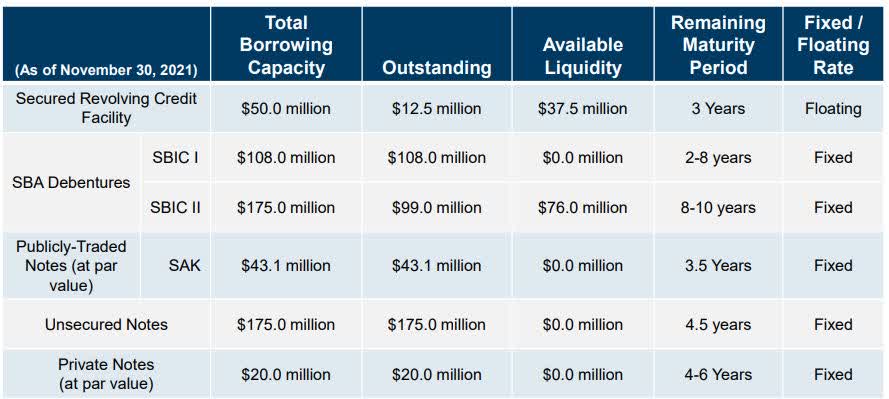

SAR has total debt outstanding of $457.6 million as of November 30, 2021. The management is well prepared for a rising interest rate environment because $445.1 million of the total outstanding is fixed-rate debt and only a tiny fraction (2.73%) is floating rate. Going forward, available liquidly is $76 million at a fixed rate and $37.5 million as floating-rate loans. (Plus, the $144.1 million of cash and cash equivalents).

Q3 2022 Shareholder Presentation

SAR is fairly valued at the moment but income investors can lock in the trade with a great dividend yield. In addition, SAR is a bit undervalued compared to my last publication. SAR has a price to book ratio of 0.93 lower than in my last publication (0.99). In the last 3 months as the overall markets declined SAR declined sharply as well and is now stabilized at approximately 4.5-5% below its November-December price range which means there is upside potential.

Seeking Alpha

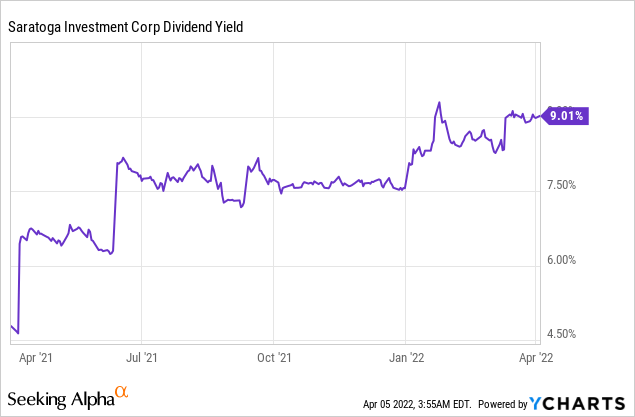

In terms of dividend yield, income investors can buy in at a great point because SAR has been trading above 8.9% dividend yield only approximately 12% of the time in the last 12 months. Looking at the 4-year average yield we can see an 8.07% figure and the current dividend is 11% higher than this average.

SAR’s dividend

Current dividend

I have already shared my thoughts about SAR’s dividend in my previous article so I am going to add bits and pieces since not many things have changed. SAR is paying a $0.53 per share dividend and is yielding at 9.01% while in my last publication the dividend yield was 7.34%. The management continues the DRIP and some share repurchases. These buybacks only decrease NII per share by $0.01 while adding $0.01 to the NAV per share but those only count for 0.03% of the NAV per share.

Future sustainability

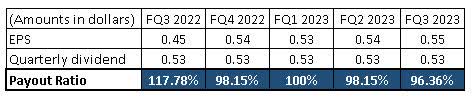

As I mentioned before SAR’s payout ratio is overstretched and this has not changed since. I am aware that due to its BDC status they need to pay out a certain amount for dividends to keep up the BDC status, however, I am still not convinced about SAR’s long-term dividend safety. Although, it is worth noting that the management is still keen on paying dividends regularly and the company has all the necessary fundamentals to do so. I am not expecting any dividend cuts in the upcoming years due to the expanding NAV and because of the company’s low debt profile combined with floating-rate investments. This means the broader economic cycle and the interest rate increases are in SAR’s favor and could support the current payout ratio.

The table is created by the author. All figures are from the company’s financial statements and SA Earnings Estimates.

Final thoughts

I am certain that SAR can be a good choice to hedge inflation risk. The company could grow in many segments and the debt restructuring was a great management decision. When the interest rate will be above 1.5% the fixed-rate debt of SAR combined with its floating rate investments will bear fruit. The only part I am reluctant about is the dividend coverage but if the broader economic environment supports the company’s growth, the payout ratio will decline despite any minor dividend increases. For investors looking for a longer-term position in a BDC, Saratoga can be the right choice.

Be the first to comment