hxyume/E+ via Getty Images

SalMar (OTCPK:SALRF) is one of Norway’s premier salmon aquaculture companies. It has superb assets and generates phenomenal returns. The problem is that the government seems to have noticed that their assets, all pens in the fjords and archipelagos of Norway, are profitable, and the Norwegian government likely wasn’t getting to profit on its limited awards of licenses to the aquaculture companies. A new proposed tax will seriously impact SalMar’s multiple, likely doubling their forward PEs given the current capital structure. They should have a much lower multiple than they currently do, given that you can get cheaper peers with much more limited exposure to the taxes.

SalMar’s Q3 Note

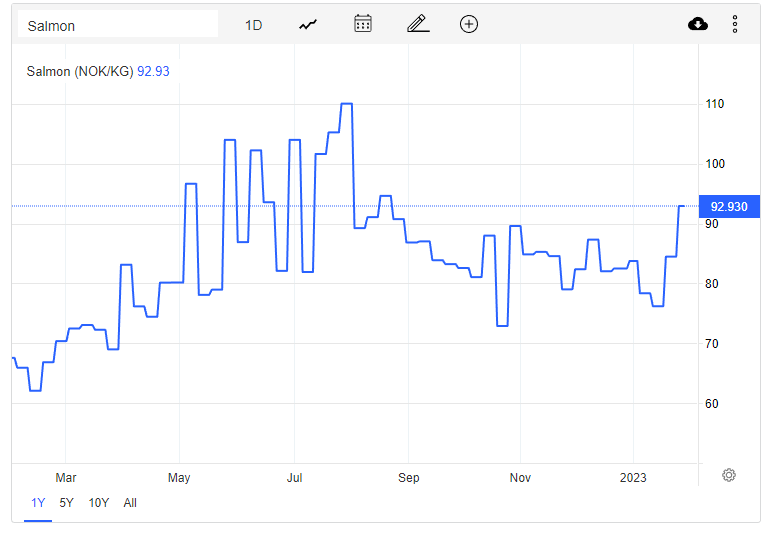

The Q3 naturally looked good. Salmon prices continued to rise, and cost inflation was outrun without much trouble. We detailed why we thought salmon as a commodity would do well in the current environment, specifically with respect to Ukraine, in our coverage of Mowi.

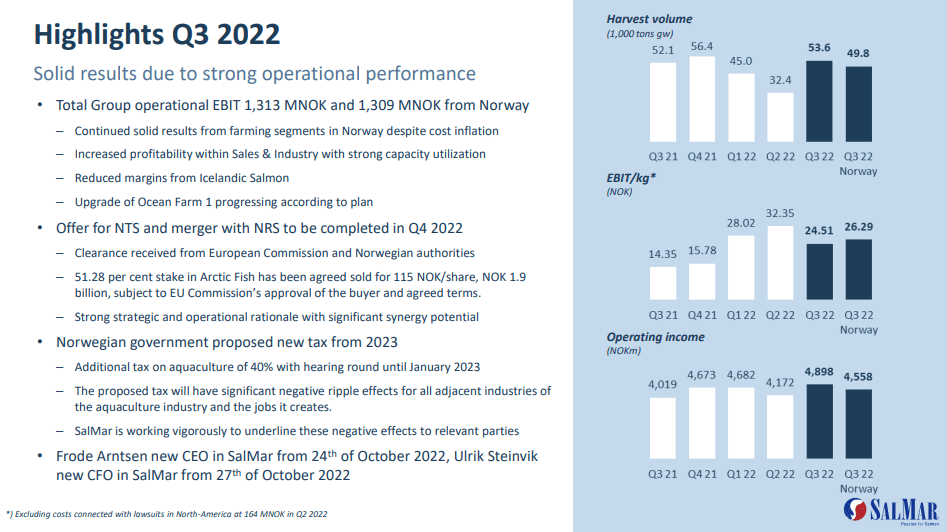

Q3 Highlights (Q3 2022 Pres)

Feed costs rose, but both harvest volumes and a relatively strong salmon price development YoY created a nice lift in the operating income.

Salmon Price (Tradingeconomics.com)

As usual, the company is performing with a very high return on its assets, with operating margins well in excess of 20%, and invested capital levels being quite low, the ROIC is also over 20%, which is phenomenal as financing rates in Norway remain lower than the new global averages.

Major Challenges

The problem is this newly proposed tax on the aquaculture industry in Norway, specifically targeting the largest players, SalMar very much included. Effective tax rates could skyrocket as a result. While they are about 22% now on the basis of the Norwegian corporate tax rate, they will go up to over 60% with the introduction of this new tax. The government, controlled by the socialist Labor Party, does not appear to be yielding to industry lobbyists. The only concession they made is that they’d not use a norm price based on the Nasdaq Salmon Index to calculate the tax base, and instead allow for actual price realization of the companies to determine the tax base. In the latter scheme, all the fixed price agreements would create huge tax exposures if they were at lower than spot prices, and therefore effective tax rates for companies that had fixed price agreements with offtakers would be substantially higher than even the wildly high 60%.

There is a tax-free allowance for all income on the first 5k tonnes of biomass harvested. This basically means that the vast majority of producers, who are small, will not be affected. Despite a huge business differential, SalMar remains painfully overvalued.

Bakkafrost (OTCPK:BKFKF), whose exposures are not in Norway (they are in the Faeroe Islands), and generates similar margins to SalMar and quite similar ROICs, trades at the same EV/EBITDA multiple on a TTM basis, and more relevantly because we are considering tax effects, trades at about a 20% premium in terms of PE, despite the fact that FWD PEs for SalMar are going to be 3x what they were TTM once the tax comes into effect based on SalMar’s current capital structure. We think they will have every incentive to take on a whole lot of leverage until the Labor Party in Norway possibly gets ousted in future elections, and hopefully, lobbies can reverse the tax – although this is perhaps a fool’s hope. They will continue to try to lobby against this before it comes into force, but we have zero expectations of success in this regard.

While the SalMar price is already very discounted on account of this, and Bakkafrost recovered sharply on account of it dodging these taxes by not operating on Norwegian licenses, there is still an unnecessary premium on SalMar’s forward multiple. The problem is SalMar is Norway’s major blue-chip stock that everyone owns, and we think we are likely seeing the bias from less-sophisticated actors on the stock price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment