nespix/iStock via Getty Images

Tech stocks have taken a beating since the start of April, as concerns around inflation have caused the market to discount the valuations of this sector. This brings me to Salesforce (NYSE:CRM), which has fallen back towards its 52-week low after a brief rally last month. This article highlights why the recent dip creates a great buying opportunity for total return investors, so let’s get started.

Salesforce: Fast Growth To Offset Inflationary Concerns

Salesforce is a global leader in CRM software, and its solutions are used by businesses of all sizes to manage their sales channel pipeline and customer relationships. In addition to its core CRM offerings, Salesforce also provides a number of other enterprise software solutions, including Sales Cloud, Service Cloud, Marketing Cloud, Commerce Cloud, and more.

The company has been one of the biggest beneficiaries of the shift to cloud computing, and its share price has reflects this, rising from around $40 per share in 2012 to $189 per share today.

However, Salesforce shares have come under pressure in recent weeks as investors have started to worry about inflationary pressures. While inflation is generally a good thing for the economy, it can be bad for certain sectors, such as tech, which tend to have high valuations. That’s because inflation causes the market apply a higher discount rate on future cash flows, thereby resulting in a lower net present value.

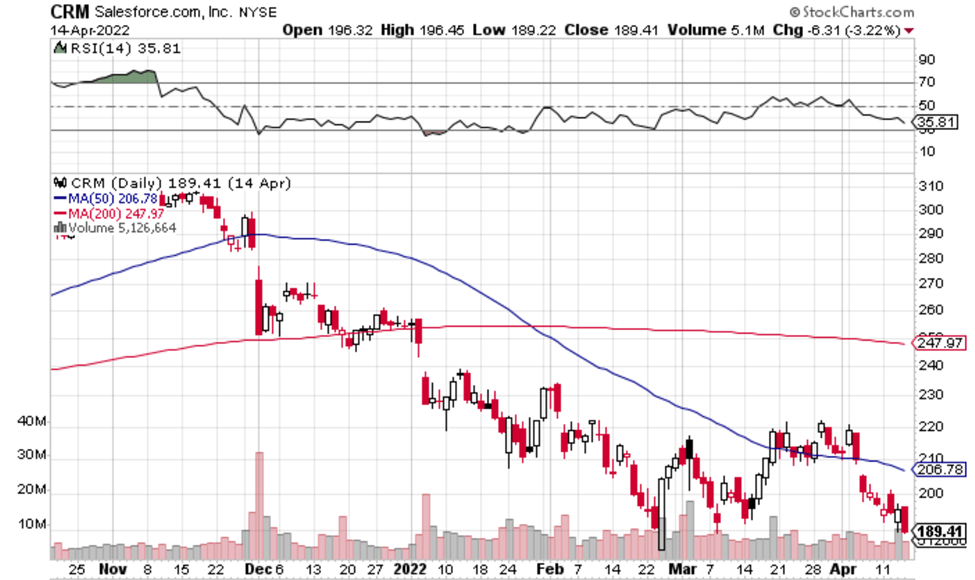

As shown below, CRM currently trades below its 200 and 50-day moving averages of $248 and $207, respectively, and carries an RSI score of 35.8, indicating that it’s approaching oversold territory.

CRM Stock Technicals (StockCharts)

While inflationary concerns can be discouraging, I see CRM’s fast-growth as being able to offset this headwind. This is reflected by the respectable 26% YoY revenue growth that it saw in the fourth quarter, and the 25% revenue growth for the full year FY 2022 (ended January 31st).

Moreover, CRM maintains strong profitability, with an adjusted operating margin of 18.7%. This is driven by CRM’s pricing power and operating leverage, helping it to earn an A+ score for Profitability relative to its sector.

Looking forward, both Tableau and Mulesoft could be meaningful growth drivers for the company, as they racked up recent wins with large enterprises: Southwest Airlines (LUV), IBM (IBM), Sunrun (RUN), Deloitte, and Ford (F). These two products saw a robust 23.5% YoY growth in the latest reported quarter.

In addition, Slack puts CRM in a competitive position against Microsoft’s (MSFT) Teams product, and its performance is exceeding management expectations with recent wins at Carvana (CVNA) and Netflix (NFLX).

Notably, Morningstar assigns a wide moat to CRM and highlights its competitive strengths in its recent analyst report:

Salesforce’s critical differentiator was that the software was accessed through a web browser and delivered over the Internet, thus inventing the SaaS software delivery model. Service Cloud brought in customer service applications, and Marketing Cloud delivers marketing automation solutions. These solutions encompass nearly all aspects of customer acquisition and retention and, in our view, are mission critical.

In our view, Salesforce will benefit further from natural cross-selling among its clouds, upselling more robust features within product lines, pricing actions, international growth, and continued acquisitions such as the recent deals for Slack and Tableau. Salesforce is widely considered a leader in each of its served markets, which is attractive on its own, but the tight integration among the solutions and the natural fit they have with one another makes for a powerful value proposition, in our view.

CRM Stock: Buy The Dip

I see the recent drop in CRM’s share price to $189 as presenting an attractive opportunity for the above reasons and considering the fact that the share price traded as high as $311 as recently as November of last year.

Wall Street analysts estimate continued double-digit revenue growth this year, and double-digit EPS growth next fiscal year, which may justify CRM’s forward PE of 40.6. Sell side analysts have a consensus Strong Buy rating on CRM stock with an average price target of $298 and Morningstar has a fair value estimate of $320. This implies a potential 58% total return based on the lower of the 2 price targets.

Investor Takeaway

The recent sell-off in Salesforce’s stock presents an attractive opportunity for long-term investors. The company is a market leader in the cloud-based CRM space and its products are mission critical for many of its customers. It has strong pricing power, operating leverage, and profitability, which should help it to continue to grow at a fast pace. As such, CRM may be a good addition to a growth portfolio at the current price.

Be the first to comment