sharrocks

Earnings season is now in full swing. After the big banks reported huge annual net interest income gains, smaller financials are slated to report this week. One name has been on the move higher lately, but some have called into question how well regional banks can perform now that yields might have put in a top.

Let’s take a look at PNC Financial (NYSE:PNC), one of the most prominent regional banks in the country.

Q4 Earnings Season Cadence

Wall Street Horizon

According to Bank of America Global Research, The PNC Financial Services Group, Inc. is a Pittsburgh-based financial services organization with approximately $600 billion in assets. Founded in 1983 with the merger of Pittsburgh National and Provident National, PNC has grown to become a top 10 bank in the US by deposits. PNC offers a wide array of financial products ranging from retail and business banking to wealth and asset management.

The Pennsylvania-based $68 billion market cap company within the Financials sector trades at a low 12.4 trailing 12-month GAAP price-to-earnings ratio and pays a high 3.7% dividend yield, according to The Wall Street Journal.

BofA recently downgraded the stock as they see much of the bank’s balance sheet strength and defensive nature in a cyclical industry as discounted. Moreover, the prospects of weaker GDP growth could hurt the entire space. Back in October, PNC beat on the top and bottom lines while boasting strong operating leverage.

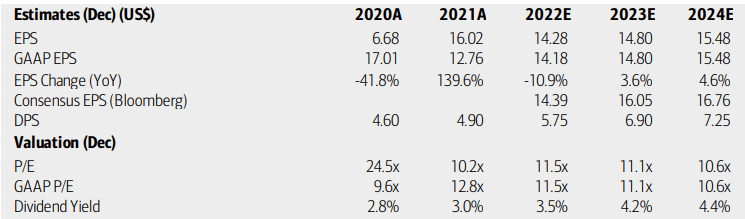

On valuation, analysts at BofA see earnings having fallen about 11% this year before bouncing back modestly by 3.6% in 2023. Per-share profits are then expected to rise by less than 5% in 2024. The Bloomberg consensus forecast is more sanguine than what BofA projects, though. Dividends, meanwhile, are seen as rising quicker than EPS while both the stock’s operating and GAAP P/Es should remain attractive.

Being a bank, it is key to look at the price-to-book ratio, and that multiple certainly reflects PNC’s high industry standing. At 1.61 on a forward basis, it’s at a high 25% premium to the sector media and 17% above PNC’s 5-year average P/S. Overall, the stock might be cheap to the market, but I see shares as being less of a value today. Still good for a long-term buy though.

PNC: Earnings, Valuation, Dividend Forecasts

BofA Global Research

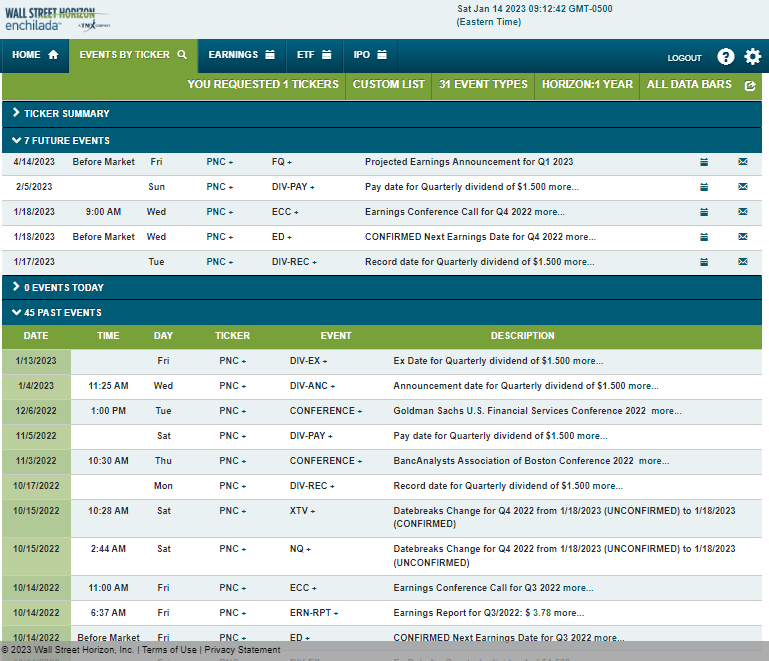

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Wednesday, January 18 BMO with a conference call later that morning. You can listen live here. Shares have a dividend record date on Jan 17 ahead of earnings to be paid out on Sunday, February 5.

Corporate Event Calendar

Wall Street Horizon

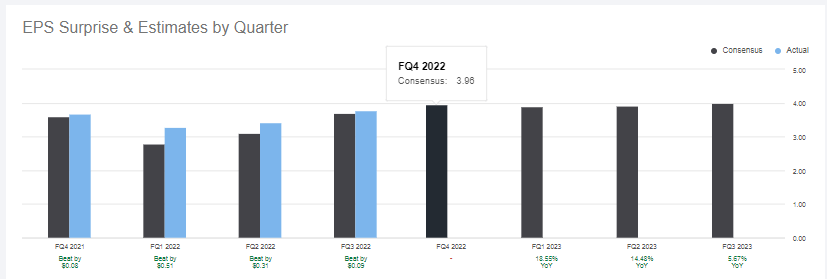

Seeking Alpha reports that the consensus Q4 EPS figure is $3.96 which would be a solid 7.6% increase from $3.86 of per-share profits earned in the same quarter a year ago. PNC has topped analysts’ earnings estimates in 7 of the previous 8 reports.

PNC: Earnings Surprise History

Seeking Alpha

The Technical Take

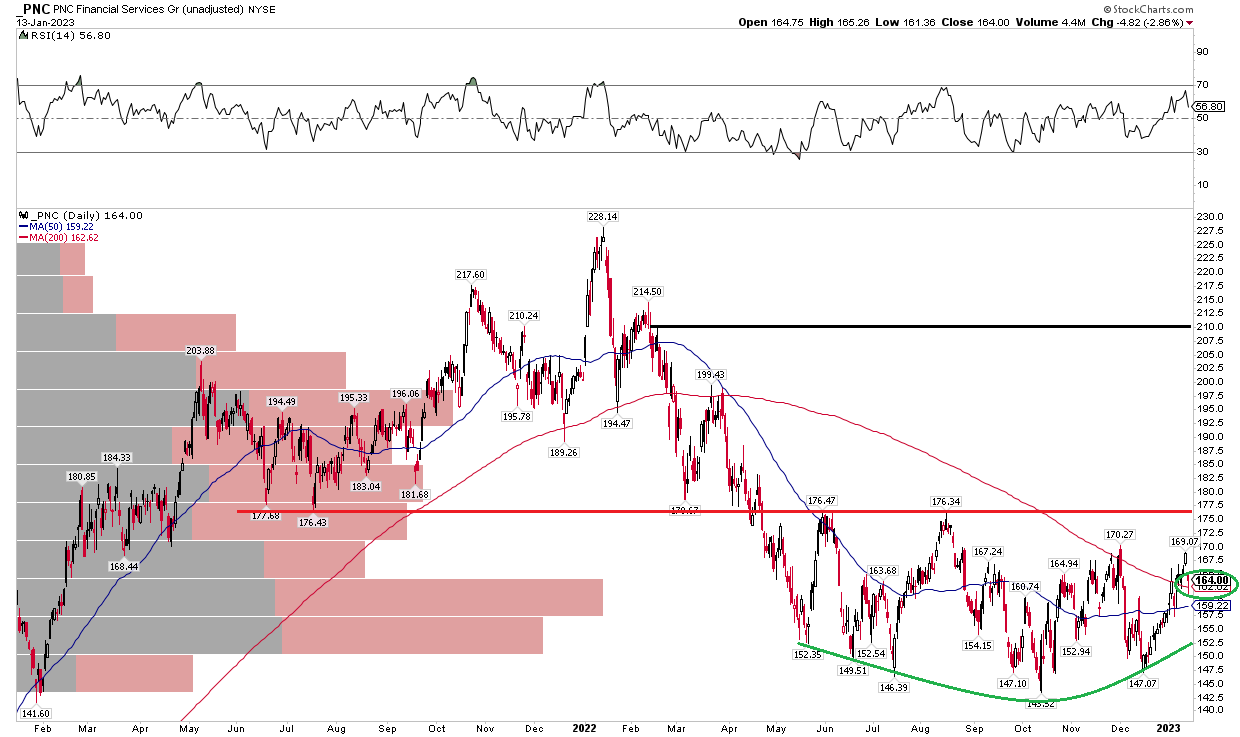

Back in October, ahead of Q3 results, I had a buy recommendation on PNC. Since that was right near the market bottom a few days later, shares are of course up nicely on a total return basis. I would call that favorable timing more than anything, but does the chart still suggest now is a good time to be long? I think so but would like to see the stock clear a key spot.

Notice in the chart below that PNC is putting in a bullish rounded bottom after notching a low near $144 back in October. I see resistance near $170 and $176. If shares rise above that zone, though, a bullish measured move price objective to $210 would be in play – near the peak from Feb-March of last year.

What’s also ideal about the setup is that there is ample support from high volume-by-price in the $150 to $160 zone over the last two years. PNC managed to settle above its currently falling 200-day moving average to finish last week – I would like to see the 200dma turn up along with a golden cross from the lower 50dma. One at a time, though. Long here with a stop under $140 looks good.

PNC: Bullish Rounded Bottom Working

Stockcharts.com

The Bottom Line

With a solid EPS beat rate history, a decent valuation, and bullish chart features building, being long PNC here still makes sense going into earnings on Wednesday.

Be the first to comment