Fundamental Forecast for the Euro: Neutral

- The Euro had a mixed performance last week, gaining against safe havens but giving up ground versus the commodity currencies by the close on Friday.

- The economic calendar will take a backseat again this week, as few ‘high’ rated data releases means that focus will continue to revolve around developments between Russia and Ukraine.

- ECB rate expectations are evolving, but the ECB continues to push back on the idea of rate hikes anytime soon.

Euro Week in Review

With hopes springing for a ceasefire between Russia and Ukraine, risk appetite proved resurgent, helping prop up the recently decimated Euro. EUR/JPY rates led the way higher, adding +2.9% on the week, posting their second highest weekly close of the year. EUR/USD rates gained +1.28%, nearly erasing all of the losses over the past two weeks. Similarly, EUR/CHF rates added +0.98%, closing just a few pips away from where they opened on February 28.

But not all EUR-crosses rallied. Indeed, the rebound in risk appetite and sustained move higher in commodity prices continued to benefit the trio of the Australian, Canadian, and New Zealand Dollars. EUR/AUD rates fell by -0.37%, EUR/CAD rates gained a mere +0.13%, and EUR/NZD rates slipped by -0.17%. Long upper wicks on these pairs’ weekly candles suggest more downside pressure may be imminent.

Eurozone Economic Calendar Quiets Down

Markets continue to focus on the Russian invasion of Ukraine and its knock-on effects for the European economy, dwarfing data releases. This tendency will be amplified in the coming week, insofar as a thinner economic calendar – marked mainly by speeches from European Central Bank policymakers – will leave plenty of room for headlines out of Eastern Europe to catalyze volatility.

That said, here are the key events in the week ahead on the Eurozone economic calendar:

- On Monday, March 21, and Tuesday, March 22, ECB President Christine Lagarde will give speeches pertaining to the economic outlook for the Euroarea.

- On Tuesday, March 22, ECB Executive Board member Fabio Panetta will give remarks at 13 GMT, followed by ECB Chief Economist Philip Lane at 13:15 GMT.

- On Wednesday, March 23, the European Council meeting begins at 8 GMT and will take place over the course of the next three days. The flash March Euroarea consumer confidence report will be released at 15 GMT.

- On Thursday, March 24, there is an ECB General Council meeting at 8 GMT. The flash March German PMIs (composite, manufacturing, and services) will be released at 8:30 GMT. At 9 GMT, the ECB Economic Bulletin will be published at 9 GMT, as will the flash March Euroarea PMIs (composite, manufacturing, and services). ECB Vice-Chair of the Supervisory Board Frank Elderson will speak at 9:30 GMT and 13 GMT.

- On Friday, March 25, the March German Ifo business climate survey will be released at 9 GMT.

For full Eurozone economic data forecasts, view the DailyFX economic calendar.

ECB Rate Hike Being Pushed Back?

Following the Federal Reserve’s rate decision last week, markets began to price-in a greater likelihood that the ECB will follow suit with its own policy tightening efforts later this year. After briefly being eliminated in early-March, rates markets are now pricing in 50-bps of rate hikes by the ECB by the end of 2022.

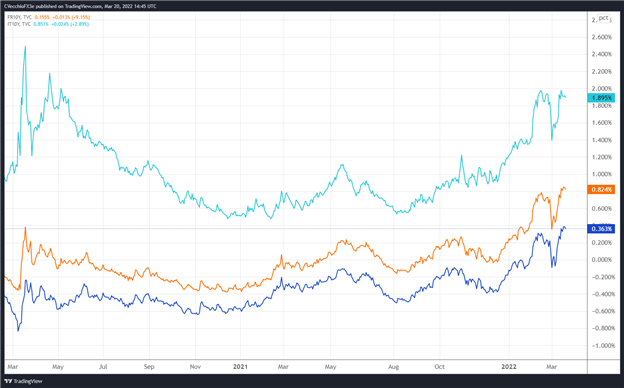

Consistent with the expectation for a more aggressive ECB, European sovereign bond markets saw higher yields over the course of the week. Long-end bond yields in France, Germany, and Italy have all rebounded to fresh yearly highs after swooning in early-March. In particular, the German 10-year Bund yield touched its highest level since late-2018.

French, German, Italian 10-year Yields (March 2020 to March 2022) (Chart 1)

But conflicting signals are coming from the ECB itself. While several ECB policymakers have suggested that interest rate hikes may be appropriate later in 2022, ECB President Lagarde continues to suggest otherwise. Last week, in a speech titled “Monetary Police in an Uncertain World,” ECB President Lagarde hinted that rate hikes may not materialize in 2022, noting, “we have adjusted our forward guidance on interest rates to temper expectations of any abrupt or automatic moves.We now say that the adjustment of key ECB interest rates will take place ‘some time after’ the end of net purchases.”

Thus, while rising European sovereign bond yields may have insulated the Euro against steeper declines in the very near-term, the real prospect of growing divergence between interest rate policies deployed by the ECB relative to other major central banks (the Fed, the Bank of England, etc.) may prevent the Euro from staging a significant rally henceforth.

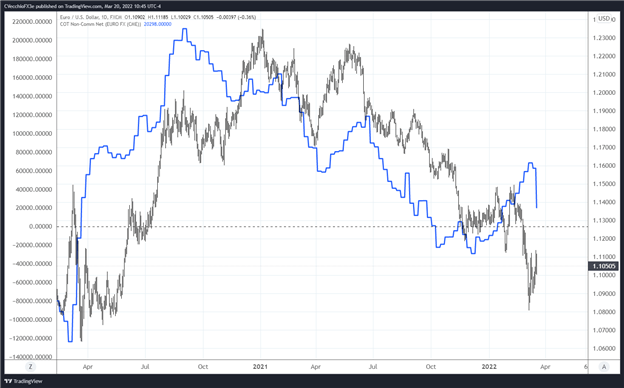

CFTC COT Euro Futures Positioning (March 2020 to March 2022) (Chart 2)

Finally, looking at positioning, according to the CFTC’s COT for the week ended March 15, speculators sharply decreased their net-long Euro positions to 20,298 contracts from 62,536 contracts. Net-long Euro positioning, which has been slowly building through 2022, has been nearly erased, with the fewest net-longs held by speculators since the third week of January.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment