kali9/E+ via Getty Images

By Padhraic Garvey, CFA, Benjamin Schroeder, Antoine Bouvet

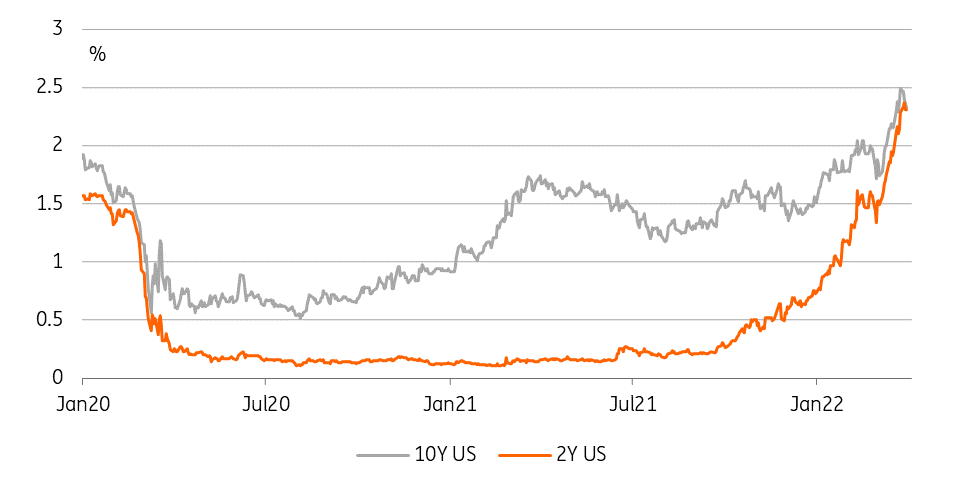

When the 2/10yr curve very briefly inverted earlier this week, it was a moment where the 10yr yield dipped below the 2yr yield (and not the 2yr shooting above the 10yr). This is important, as since then there has been a tendency for market rates to drift lower. It looks as if the 10yr is attempting to mark the 2.5% area as the peak in the cycle. It’s far too early to tell whether it is, but the market will map out a technical path here to assess whether it was.

Our view is that there remains upside potential for market rates, beyond 2.5% and likely up as far as the 2.75% area, particularly as the Fed has not even started to unwind its balance sheet yet. When they do, there will be some USD 2-3 trillion of paper moving off the Fed’s balance sheet and on to the open market – a significant supply-side event, likely starting from July (at the latest).

Payrolls today will help to frame where the market mindset is. The number itself is, of course, important. But the number itself is not always the issue. Often, it’s the market registering the payrolls event and pushing beyond it that matters. Should market rates continue to drift lower after payrolls, it will feel like a local peak has certainly been reached. At the same time, the payroll event could be used as an excuse to halt the downside test, and instead revert to testing towards higher yields.

2Y-10Y had briefly inverted – triggered by 10Y heading lower, not 2Y higher (Refinitiv, ING)

Strong US data and High EZ CPI readings set the stage for next week

Today’s data releases should set the tone for the upcoming week. US jobs data should confirm the strong labour market backdrop, against which markets will then also interpret the upcoming FOMC minutes. It was the notable meeting where the Fed felt the need to step up the speed of tightening ahead.

Similarly, the high inflation readings in the eurozone set the stage for the ECB speakers next week. It may be their final dash to better align market expectations, with ECB thinking before the communications blackout period starts on Thursday ahead of the April 14 policy setting meeting. So far, the cautious tone from the ECB has been largely brushed aside by markets. But increasing concerns surrounding natural gas supply and the economic knock-on effects may mean that markets become more receptive. The release of the ECB minutes next Thursday can add to the understanding of the ECB’s more cautious stance.

In our view, the bear-flattening of the eurozone curve is a near-term phenomenon which should eventually give way to a more healthy resteepening of the curve. As the more technical flattening pressure stemming from month-end rebalancing flows has now passed, perhaps the upcoming week could see dynamics change already.

2Y-10Y had briefly inverted – triggered by 10Y heading lower, not 2Y higher (Refinitiv, ING)

Today’s events and market view

The main event for the day is the US job market data, where the market consensus is looking for a 490k non-farm payrolls increase. The issue remains a lack of supply of workers to fill the vacancies available while demand is strong. Other data to watch today is the ISM manufacturing. All in all, data should support calls for 50bp Fed hikes at least at the next two meetings.

On the Fed speakers front, Evans will discuss the economy and the policy outlook.

The eurozone will focus on the CPI flash estimate, where the consensus is still for a 6.7% y/y rise, however upside surprises in the country data the market should be primed for a higher reading already. The busy slate of ECB speakers will underscore the gap between market pricing and ECB rhetoric, though the nearing blackout period ahead of the next ECB meeting may see members stepping up their tone.

In supply, Belgium conducts a smaller optional reserve inquiry auction today.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Be the first to comment