PhoThoughts

Yesterday, the German sporting goods manufacturer Puma SE (OTCPK:PMMAF) (OTCPK:PUMSY) posted its half-year results. We predicted a good quarter, and Puma is finally delivering in line with our expectations. Indeed, the company was able to increase its sales and profits in the second quarter thanks primarily to the good performance achieved in Europe and America.

Ahead of the Q2 results, we anticipated higher sales by looking at the inventories in the warehouses and forecasted a strong rebound in turnover in North America thanks to the re-entry into the basketball business. Looking at the just-released three-month numbers, our predictions were correct.

Q2 Results

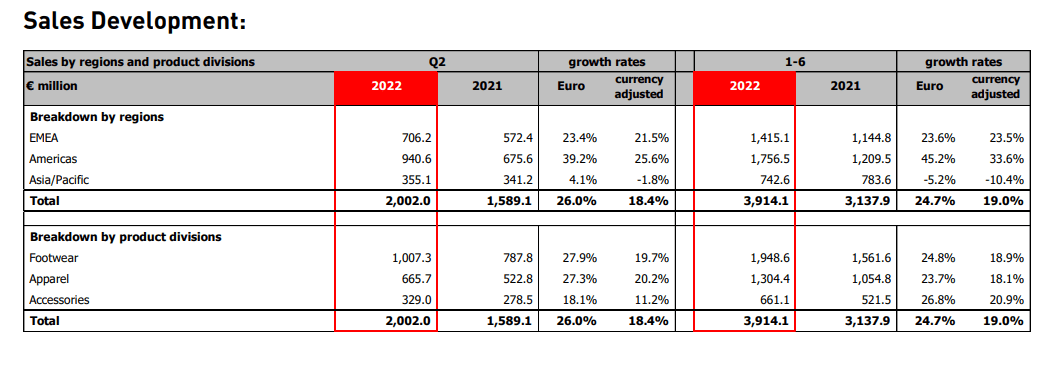

By analyzing the quarter, top-line revenue stood at €2 billion, increasing by 26%. This performance was recorded thanks to a strong wholesale business and was the best ever achieved in Puma’s history. Adjusting for the FX development, sales increased by 18.4%. As we already mentioned, both EMEA and America region recorded solid growth, whereas the revenue in APAC fell slightly, this was due to the prolonged COVID-19 restrictions still applied by the Chinese government.

Puma sales development

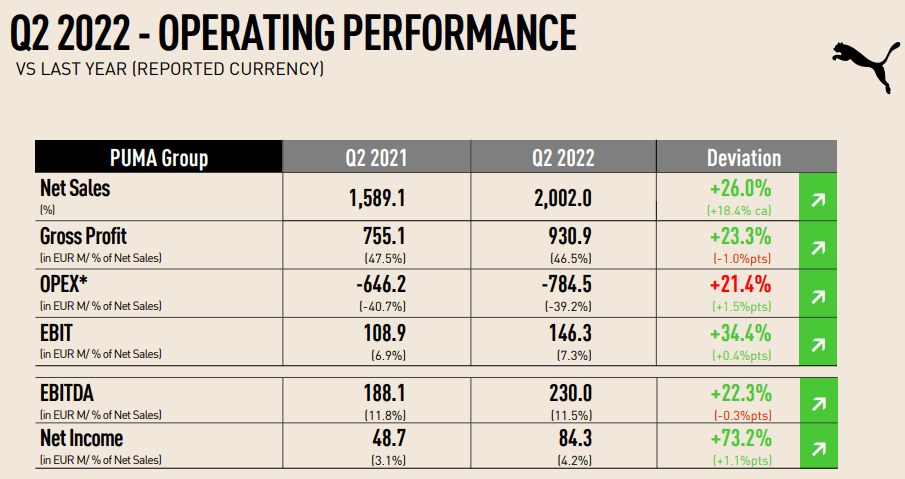

Despite higher marketing and freight cost, operating profit reached €146 million. In the press release, we note that the management is focusing more on sales growth and market share gain rather than margins. Going down to the bottom line, Puma delivered a plus 73% compared to the previous year’s quarter reaching a net profit of €84 million.

Puma financial snap

Conclusion and Valuation

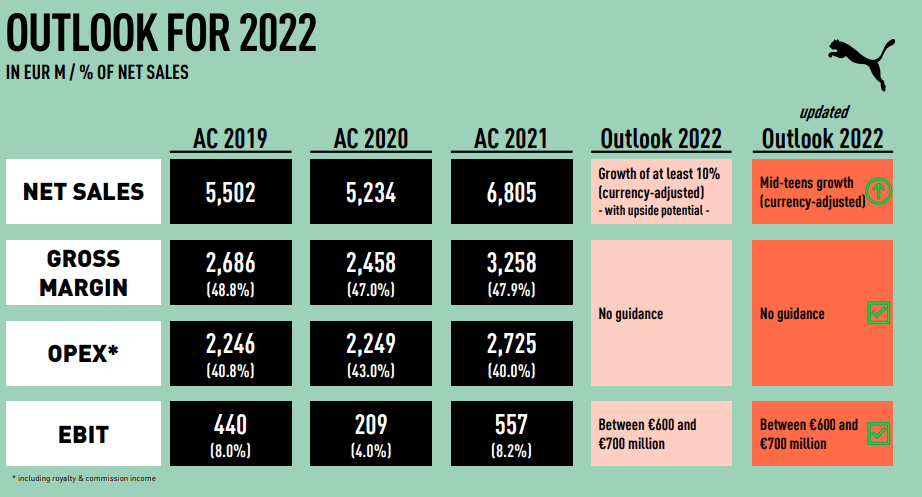

Due to the positive outcomes, Puma raised its sales forecast. In the meantime, adidas (OTCQX:ADDYY) (OTCQX:ADDDF) is downgrading its revenue outlook for the year. The reasons for this were the weaker-than-expected recovery in China and the feared deterioration in consumer sentiment. We should say that the China business is not as important for Puma as it is for adidas. Concerning the margins, Puma is sticking to the goal of €600/700 million for 2022. At a specific question during the analyst call, the CEO explained that he wants to remain cautious when it comes to price increases to not scare off customers. Puma’s strategy is to avoid higher prices for existing models and only “set new price points” for new collections, with price increases in the inflation range (5/9%), emphasizing that sales growth is more important than “short-term profit optimization“.

Year to date, Puma’s stock price is down by almost -30%. At the stock price level, the company is one of the worst performers in the sector. Having analyzed the strong Q2 performance and looking at the closest competitors, we reaffirm our valuation at €98 per share. With the higher guidance provided by the management, we see the German sporting goods manufacturer well positioned compared to its peers. Our valuation is also supported by an important discount compared to its history.

Puma 2022 outlook

Be the first to comment