ramihalim

Introduction

Despite what were likely high hopes for a good year ahead several months ago, the shareholders of Ovintiv (NYSE:OVV) are not having a lucrative year thus far into 2023 with their share price already losing around one-quarter of its value year-to-date. This is not without reason with natural gas prices enduring a significant and painful slump on the back of a warmer-than-expected winter that is sadly occurring as they move away from hedges attempting to capture upside potential. Since this is likely to see their free cash flow choked, it could be said that a warm winter might have put their dividend growth on ice for the moment, metaphorically speaking.

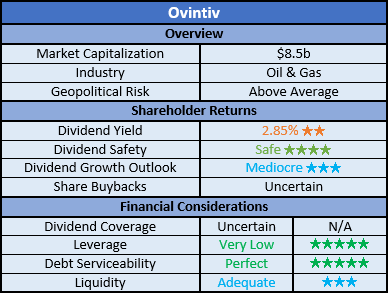

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

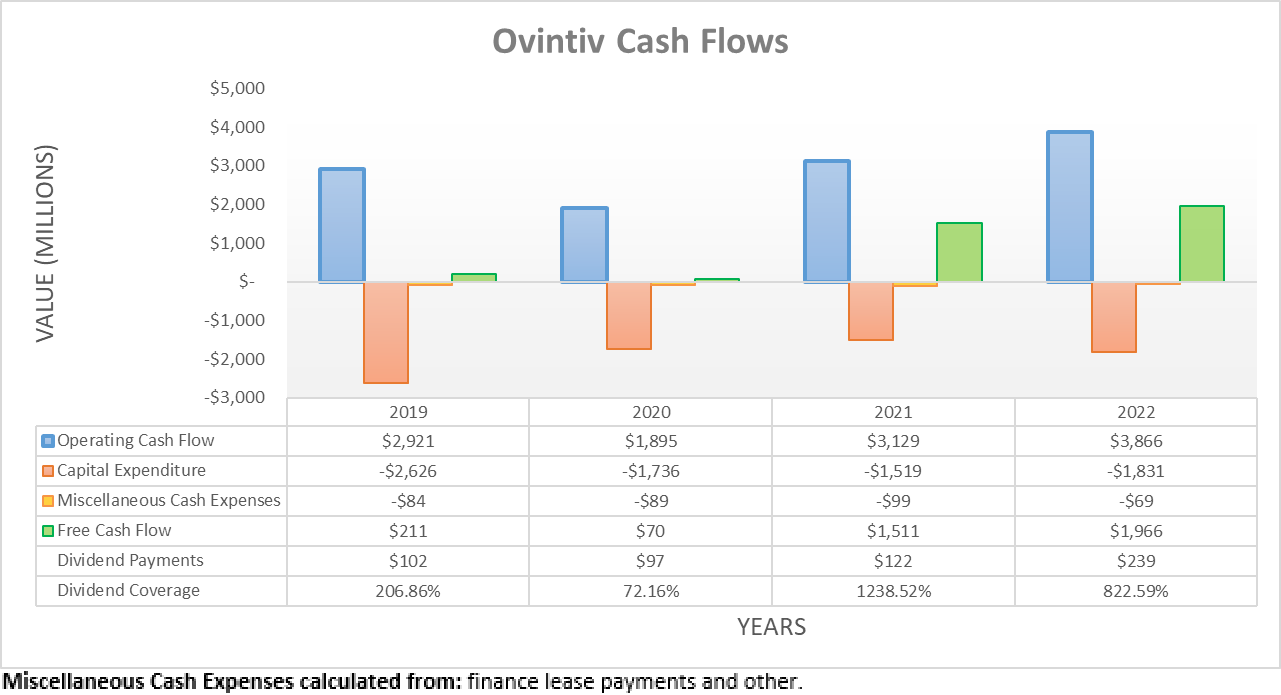

One of the biggest stories of 2022 was booming oil and gas prices, which started the year on a strong note before getting turbocharged in the aftermath of the Russian invasion of Ukraine, which lead to a global energy shortage. This quickly saw the pockets of energy companies overflowing with a massive cash windfall that few people would have ever expected, metaphorically speaking. Although in this instance, their benefit was muted as their operating cash flow only increased modestly to $3.866b during 2022 versus their previous result of $3.129b during 2021.

Whilst still an improvement, it nevertheless falls well short of what most oil and gas companies enjoyed, who often saw their 2022 results at least doubling that of 2021. In this instance, the culprit was their hedges that limited downside risk but came at the cost of partially missing out on the booming oil and gas prices. When looking at their income statement, it shows they incurred a staggering $1.867b of losses on risk management, which pertain to their hedges of which, their cash flow statement shows $741m was left unrealized. If netted out, this implies a massive realized loss of $1.126b that weighed on their operating cash flow during 2022, which effectively wiped out circa 30% of their result.

Author

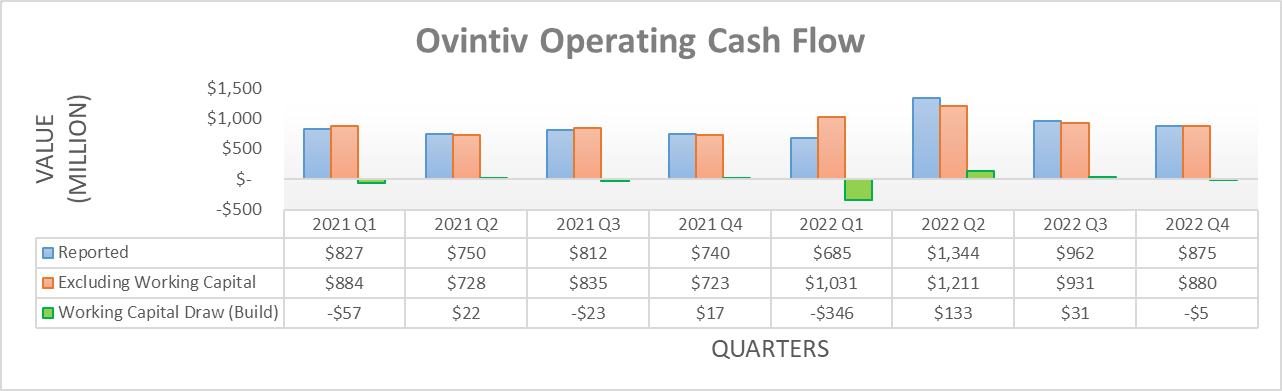

When looking at their operating cash flow on a quarterly basis, the impacts of their hedges are more easily visible with their results being reasonably stable for an oil and gas company that is left at the mercy of notoriously volatile commodity prices. This situation persists regardless if viewing their reported results or their underlying results that exclude working capital movements. Whilst disappointing, ultimately nothing is free in life and thus as evident during 2022, the cost of limiting downside risk is limiting upside potential.

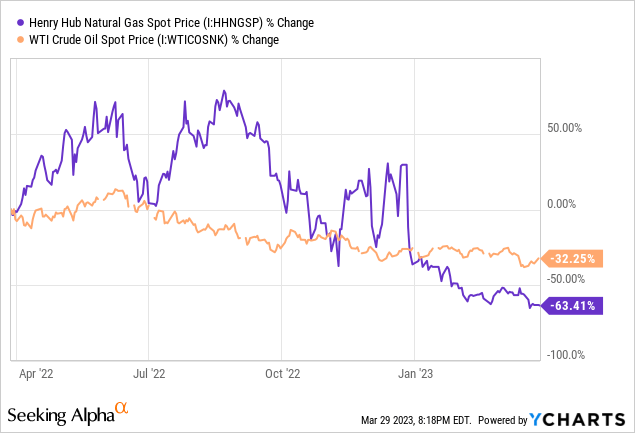

Going forwards into 2023 oil prices have slumped on the back of economic concerns, especially following the recent banking crisis that as of the time of writing, sees Western Texas oil prices down to circa $70 per barrel. That said, the far more significant impact they face is not necessarily oil but rather, natural gas that is being impacted not only by these economic concerns but also by a warmer-than-expected winter in the United States and Europe that eased critical supply concerns. Since weather forecasts still show no signs of improving catalysts for natural gas demand on the horizon, it now sees Henry Hub natural gas prices down to only a painful $2.00 per MMbtu, which is loss-making for many companies.

Y-Charts

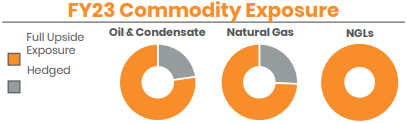

When it comes to their production, it is effectively a 50-50 split between natural gas and liquids, which includes oil, condensate and natural gas liquids, as per slide six of their fourth quarter of 2022 results presentation. As a result, they are heavily exposed to the far more significant and painful slump in natural gas prices from the warmer-than-expected winter and whilst this is normally when hedges would save the day, unfortunately, they entered 2023 attempting to capture the upside potential that so far remains elusive.

Ovintiv Fourth Quarter Of 2022 Results Presentation

It seems as though fate is being cruel to shareholders because after partially missing out on the booming oil and gas prices of 2022, they have only hedged around one-quarter of their natural gas production during 2023 with oil and condensate hedges being slightly less, whilst natural gas liquids see no hedges. We are now effectively one-quarter of the way through 2023 and unless operating conditions improve, it is likely to hinder their operating cash flow year-on-year versus 2022.

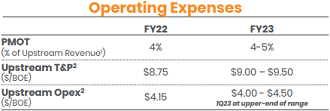

Due to the inherent volatility of oil and gas prices, it is impossible to accurately predict their operating cash flow but at the same time, the recent banking crisis and prospects for weaker economic conditions nevertheless create headwinds even if weather conditions improve for natural gas. Even though we cannot foretell oil and gas prices, at least there is guidance for their expenditure, both operational and capital.

Ovintiv Fourth Quarter Of 2022 Results Presentation

When looking at their guidance for operating expenses during 2023, they are forecasting mid-to-high single-digit increases year-on-year across the board for both their upstream T&P as well as operating expenditures. Hedges or not, this also further hinders their operating cash flow whilst their higher capital expenditure will also add pressure to their free cash flow.

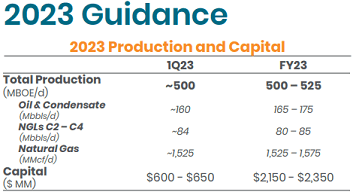

Ovintiv Fourth Quarter Of 2022 Results Presentation

Despite the less-than-stellar outlook for their operating cash flow going forwards into 2023, their guidance also forecasts capital expenditure should be $2.25b at the midpoint, which represents an increase of almost 23% year-on-year versus their spending of $1.831b during 2022. More capital expenditure instantly equals less free cash flow and therefore, all of these variables wrap together and make it seem as though their free cash flow is going to be choked during 2023, barring a sudden recovery of natural gas prices and to a lesser extent, oil prices.

When it comes to shareholder returns, less free cash flow normally means fewer dollars heading back to the pockets of shareholders. Although in this instance, it is particularly notable because their share buybacks are tethered to half of their excess free cash flow after dividend payments, as per slide twenty-four of their previously linked fourth quarter of 2022 results presentation. Since their present quarterly dividends cost $61m per quarter or $244m per annum, along with their capital expenditure guidance, this already consumes circa $2.5b of operating cash flow.

In light of this situation, I suspect they are likely to be left with minimal excess free cash flow after dividend payments going forwards into 2023 and thus as a result, the $719m of share buybacks conducted throughout 2022 are likely to fall off the proverbial cliff. Apart from hindering their share price itself, it also hinders their dividend growth perpetually into the future as a result of not reducing their outstanding share count as much as otherwise would have been the case. Additionally in the short-term, it would take a very brave management team to materially push their dividends higher in the face of these headwinds outlined so far and thus one way or another, I suspect their dividend growth is likely to be put on ice in the foreseeable future.

Author

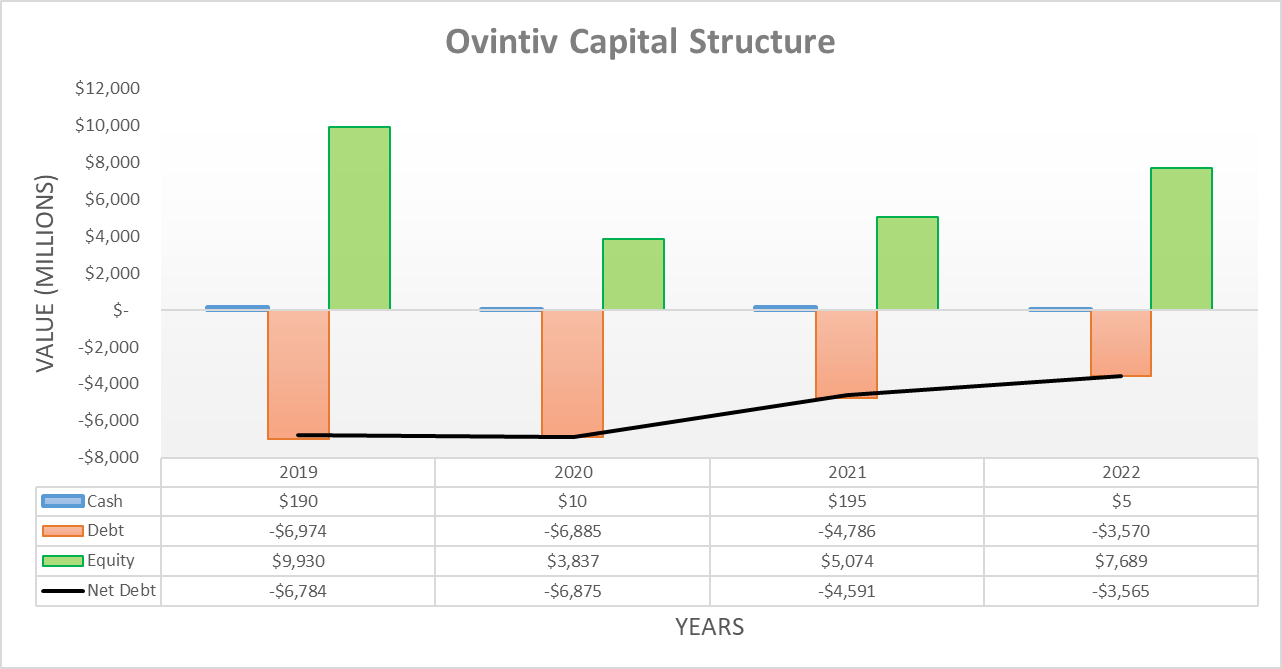

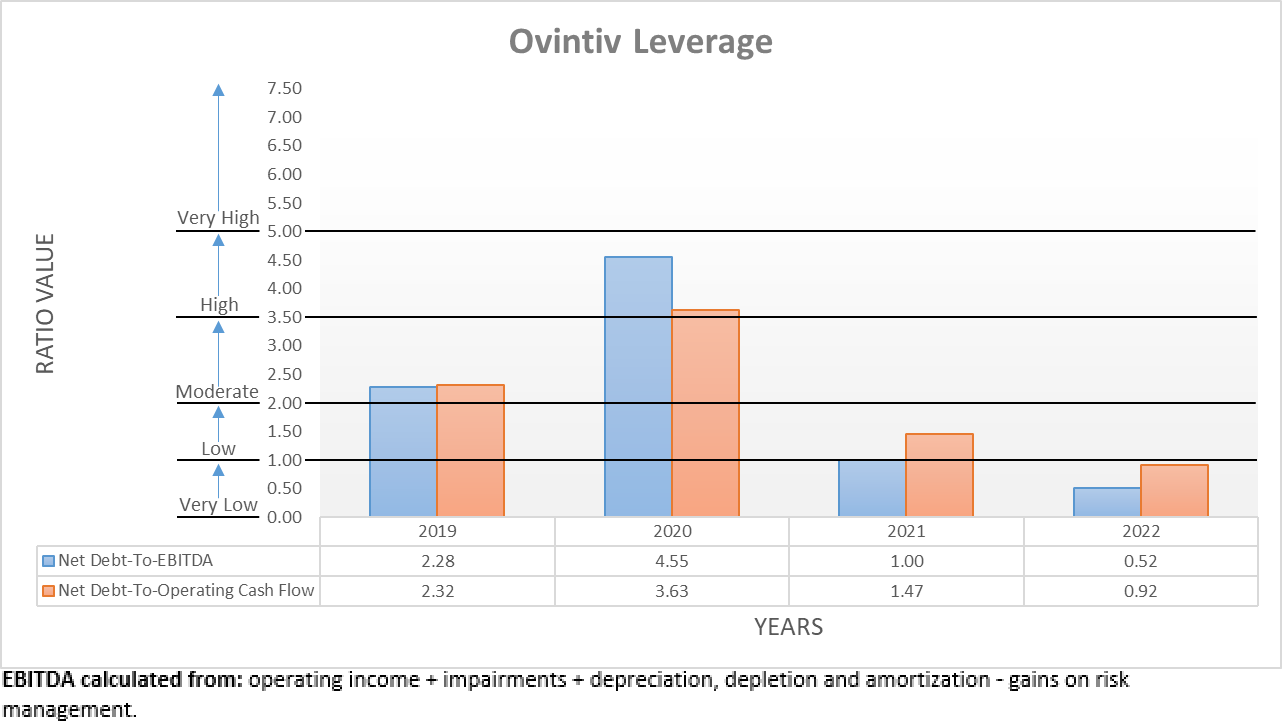

Despite partially missing out on the booming oil and gas prices of 2022, they still made a material difference to their capital structure. Most notably, their net debt was pushed down to $3.565b and thus a very impressive circa 22% below their previous level of $4.591b at the end of 2021. Going forwards into 2023, it would be prudent to assume their net debt does not decrease to any material extent to provide a margin of safety given the aforementioned outlook for their free cash flow. Since they tether their share buybacks to their excess free cash flow after dividend payments, at least their net debt should not spiral out of control regardless of where oil and gas prices head but obviously, this comes at the cost of fewer shareholder returns.

Author

At least they are heading into these uncertain times from a rock-solid base with both their net debt-to-EBITDA of 0.52 and net debt-to-operating cash flow of 0.92 beneath the threshold of 1.00 for the very low territory. Whilst partially missing out on booming oil and gas prices of 2022 was disappointing, the fact they could still post very low leverage without relying completely upon off-the-chart earnings is positive and bodes well for their ability to navigate whatever 2023 might hold. That said, it nevertheless does not stop their free cash flow from being choked and thus, it still does not resolve the accompanying limits upon their shareholder returns.

Author

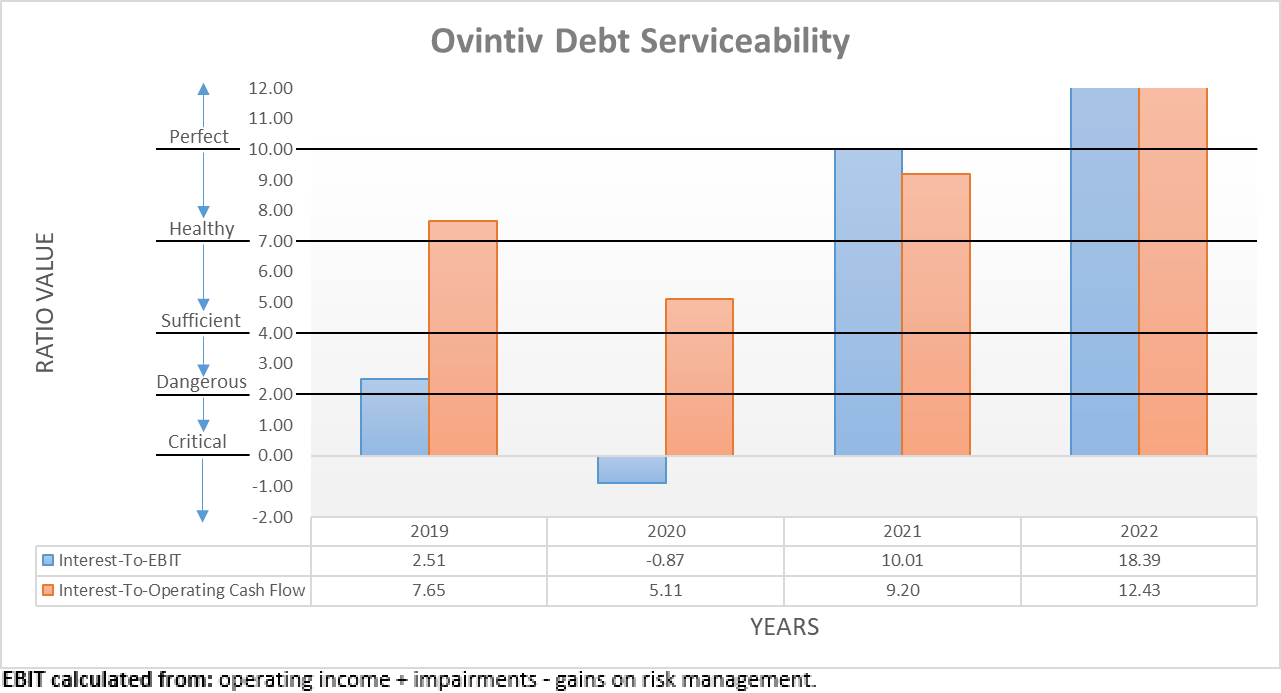

Similar to their leverage, their debt serviceability also sees the company starting from a rock-solid base with their interest coverage seeing perfect results of 18.39 and 12.43 when compared against their EBIT and operating cash flow, respectively. Regardless of where monetary policy heads going forwards into 2023, at least only $393m of their total debt of $3.57b pertains to their credit facility and thus carries a variable interest rate. Whilst they cannot avoid the impact to their financial performance from the oil and gas price slump, at least they do not face any material impact from monetary policy.

Author

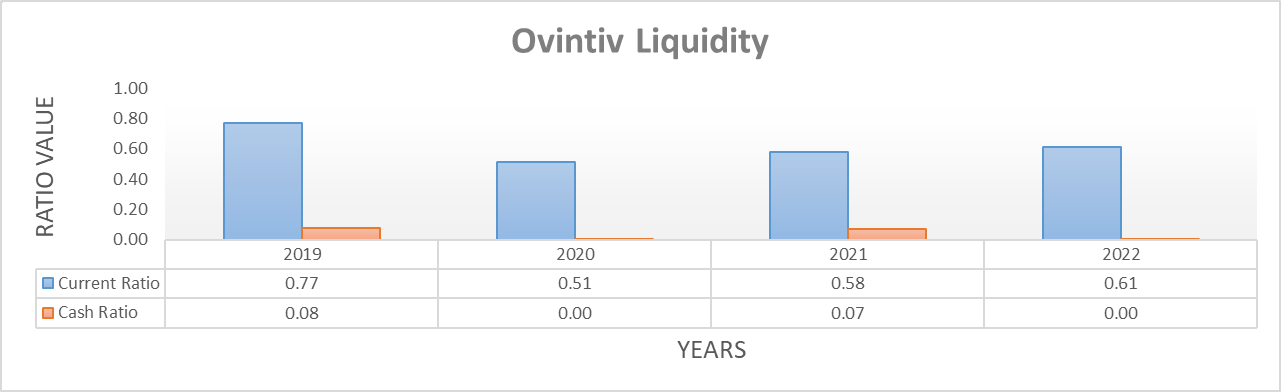

Whilst their leverage and debt serviceability are rock-solid, alas the same cannot be said for their liquidity that only sports a current ratio of 0.61. This is clearly on the low side and worryingly, their cash ratio is 0.00 as their cash balance is virtually non-existent. Since their aforementioned excess free cash flow after dividend payments appears likely minimal going forwards into 2023, this means they are reliant upon capital markets to support their liquidity. In normal times, this would not be too concerning but given the recent banking crisis, it is particularly important to consider this aspect and what avenues they have open.

Thankfully, their credit facilities still retain $3.107b of availability from their combined $3.5b borrowing base, which do not mature until July 2026. As for their other debt, nothing else matures until January 2026 and therefore given this breathing room, their liquidity remains adequate to transverse the uncertain year ahead.

Conclusion

When it comes to oil and gas companies, no one can accurately predict their financial performance without the majority being hedged. Quite painfully, after partially missing out on the booming oil and gas price during 2022, their lack of hedges during 2023 now leaves them exposed to the slump in oil prices along with the far more significant and painful slump in natural gas prices following a warmer-than-expected winter. It remains to be seen how much longer these painful natural gas prices persist but given the economic concerns creating headwinds even if weather conditions improve, their free cash flow is likely to be choked going forwards into 2023.

Since this situation means fewer share buybacks, it also sadly hinders their future dividend growth and thus right now, it could be said that a warm winter might have put their dividend growth on ice for the moment. Even though their financial position can withstand a downturn, I still believe that only a hold rating is appropriate given the economic uncertainties and their only low dividend yield of less than 3%.

Notes: Unless specified otherwise, all figures in this article were taken from Ovintiv’s SEC filings, all calculated figures were performed by the author.

Be the first to comment