Prepared by Stephanie, analyst at BAD BEAT Investing

To our surprise we were asked tonight about the small regional bank Fauquier Bankshares, Inc. (FBSS). It is a name we have not looked into in years, but given our professional commentary on many other financials recently, we gladly decided to opine on behalf of this inquisitive follower. We all know that COVID-19 has led to a massive selloff in the bank stocks, both large and small. There is a real risk of loan losses in the space, but given the stock has been cut in half, the risk of some losses is offset by the discount and the dividend yield of these regional banks. In this column, we discuss performance showing year-over-year improvement, including a steady improvement in assets, loan growth, and deposit growth. We believe that this stock is a buy in the $12-$13 range.

Q1 headline numbers impress

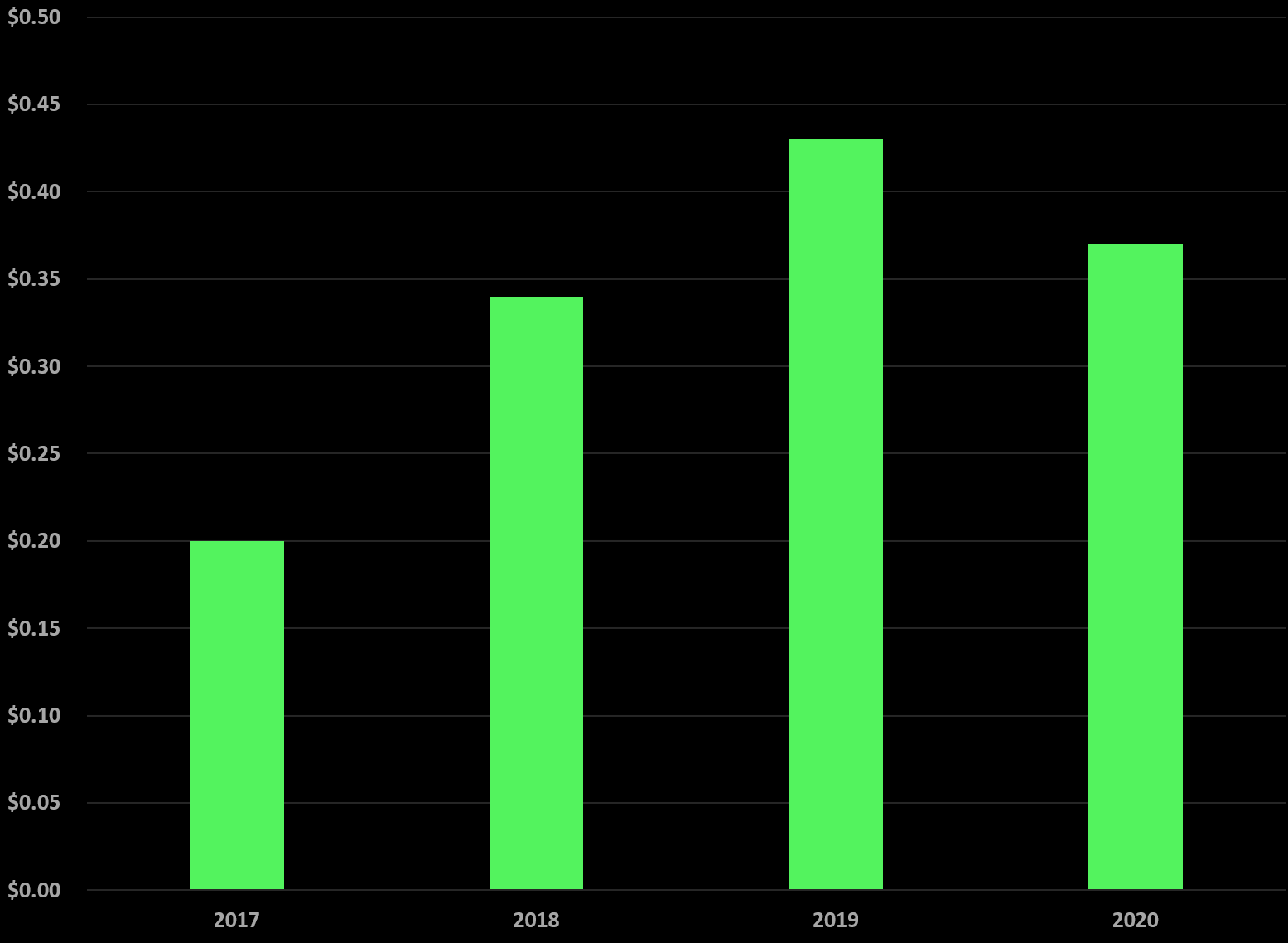

In the just reported quarter, we see that FBSS followed most other banks with a reduction in earnings per share in Q1:

Source: SEC filings, graphics by BAD BEAT Investing

As reported, the company earned $0.37 per share on net income of $1.4 million. This compares with $1.6 million, or $0.41 per diluted share for the sequential quarter. In addition, it is down from the $1.6 million or $0.43 per diluted share for the first quarter of 2019. The decline of course stems from pressure in the quarter associated with loans. Let us take a look at the impact to income from lower interest rates and reduced economic activity

Net interest and non-interest income

The headline numbers completely overshadow much of the strength the company has seen in recent years. Yes, it was a down quarter, and Q2 will be too. That is just the reality of this economy. Like many banks and other financials, net interest margin was a concern thanks to the massive reduction in rates, but Fauquier saw a decent margin. It came in at 3.76% for Q1 2020, widening from the sequential Q4 2019’s 3.65%, but down slightly from the 3.89% in the comparable 2019 quarter. With rates slashed, we can expect margins to continue to be reduced moving ahead, as we have detailed in many other analyses of other banking institutions. That said, net interest income and non-interest income were both strong, all things considered.

Net interest income increased to $6.2 million versus the $6.1 million a year ago. That was a surprise given rates, but there are more assets under management. How about non-interest income? Well, non-interest income fell to $1.3 million in Q1 2020 compared to the same quarter in 2019, down from $1.5 million. Overall, we were impressed with the growth.

One thing that we consider with FBSS, unlike many of the mega-corporations we cover, is that this is a true community bank. You can tell from the numbers. This is a strength, but also a weakness. It helps real people, in the community. But the bank is at risk from an economy that is shutdown. It is a true bread and butter traditional bank. FBSS makes money by taking deposits and issuing loans. We are pleased with the progress in loans and deposits.

Loan and deposit growth

We think it is important to note that loans and deposits continue to grow. Total loans were $562.1 million to end the quarter compared with $545.0 million in the sequential Q4, and $539.7 million a year ago. That is solid growth, though there is risk of default given COVID-19 putting so many out of work.

We were pleased to see that unlike some other small banks we have covered, there was not a ‘run on the bank’ moment of people grabbing their cash. There may have been a little, but deposits grew. Total deposits were $629.6 million to end the quarter, compared with $622.2 million for the sequential Q4 2019, and $592.4 million a year ago. Low-cost transaction deposits (demand and interest checking accounts) were $378.6 million to finish the quarter, compared with $366.0 million at the end of Q4 2019, versus $346.7 million a year ago. This is solid growth and is exactly what we want to see.

Now you might be concerned that rising deposits and the issuing of loans indiscriminately could be a risk factor. We would agree. That said, the bank is also continuing to clean up its act and utilizes conservative lending practices. One key piece of data to be aware regarding asset quality is that Fauquier’s non-performing assets improved. Yes, it improved. Non-performing assets were just $5.9 million on March 31, 2020, compared with $6.5 million for the prior quarter and $7.8 million on March 31, 2019. But to protect itself, loan loss provisions were expanded.

Based on loan portfolio growth, net charge-off history, asset quality indicators, impaired loans and other qualitative factors, there was $350,000 in provision for loan losses for the first quarter compared with $91,000 and $50,000 in provisions for loan losses for the prior quarter and the first quarter of 2019, respectively. This resulted in the allowance for loan losses of $5.6 million or 0.99% of total loans to end Q1 2020 compared with $5.2 million or 0.95% of total loans for Q4 2019 and $5.3 million or 0.97% of total loans to end Q1 2019. This was impressive

Take home

It is tough to gauge performance here. As for the bottom line, we are targeting earnings per share in the range of $1.30-1.45 for the year, which means the bank is trading at less than 10X EPS. The bank is demonstrating reliable growth. As we emerge from the crisis and open the economy back up, we can expect the bank to expand the top and bottom line. We believe the conservative lending criteria as well as the traditional banking focus of the company is a strength. We like this underfollowed bank. We think it is a buy at $12-$13 with a near 4% dividend yield.

If you like this column and want to see more, click “follow” and if you want direct one-on-one guidance from our team join BAD BEAT Investing below

Let us help you navigate this awful market. Get a 50% off discount now

Like our thought process? Stop wasting time and join the community of 100’s of traders at BAD BEAT Investing at an annual 50% discount.

It is simple. We turn losers into winners for rapid-return gains

- You get access to a dedicated team, available all day during market hours.

- Rapid-return trade ideas each week, including shorts.

- Target entries, profit taking, and stops rooted in technical and fundamental analysis.

- Deep value situations identified through proprietary analysis.

- Stocks, options, trades, dividends, and one-on-one portfolio reviews.

{kind=link}

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment