Chip Somodevilla

OXY is a Buffett stock

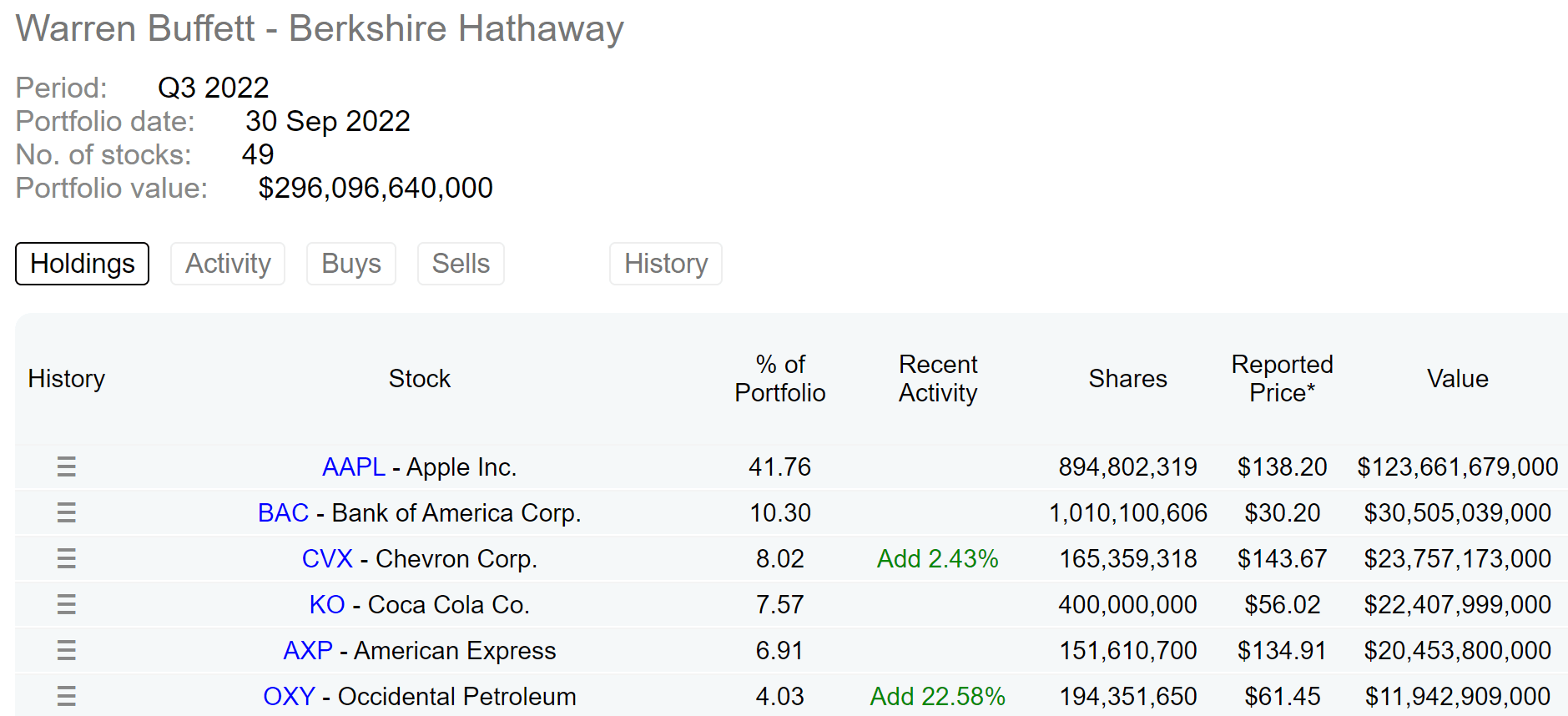

The thesis is really simple here. I will argue that Occidental Petroleum (NYSE:OXY) is not only a Warren Buffett stock under current conditions but also a Ben Graham stock. The first part of the argument is really simple. Too simple to be an argument at all. It is more of just laying out facts. It is public information that Buffett’s Berkshire Hathaway (BRK.B) has built a large OXY position in recent quarters. As you can see from the next chart, OXY is currently the 6th largest position in the BRK equity portfolio with a total market value of $11.9B. BRK now already owns around 20% of OXY shares plus nearly $10 billion worth of its preferred stock. Moreover, BRK recently received permission from federal energy regulatory to buy up to 50% of OXY common stock. As such, it is totally conceivable that BRK could acquire the whole OXY business eventually.

The remainder of this article will focus more on the second part of the argument. I will explain why Buffett’s mentor would have liked the stock himself too. I will detail why I see the stock meets all of Graham’s simple and timeless principles for picking value stocks.

Source: Dataroma.com

OXY is a Graham stock too

In the bible for value investors, The Intelligent Investor, Ben Graham developed a set of simple rules to value stocks. These simple rules have remained timeless since then and are detailed in my earlier article. A brief recap is provided below:

- Is the company large, prominent, and conservatively financed? The specific metrics to look for are stable financial strength, consistent capital structure, and a long record of continuous dividend payments.

- Especially the dividend record. Graham emphasized countless times the importance of dividend records – for good reasons. In his own words, he thinks “a record of continuous dividend payments for the last 20 years or more is an important plus factor in the company’s quality rating”.

- Has the company demonstrated an adequate level of Earnings Growth in the past? For defensive investors, growth is not the key and “adequate” is enough. In Graham’s mind, a minimum increase of at least one-third in per-share earnings in the past ten years is adequate enough.

- Finally, are the valuation multiples moderate? As a value investor to the core, he also recommended a series of methods for investors to gauge the price they should pay. And also, being fully aware of the uncertainties in his own method, he emphasized that you should always leave a safe margin of safety.

And next, you will see that OXY is a perfect fit for each and every one of these rules.

OXY: is it large, prominent, and conservatively financed?

It is simple to answer the 1st and the 2nd parts of the question. OXY is a global leader in the production of crude oil and natural gas and the associated chemicals (e.g., plastics & fertilizers). It also is a leader in the pipelines used to transport natural gases. It has net proved reserves of 1.77 billion barrels of oil and 5.85 billion cubic feet of natural gas.

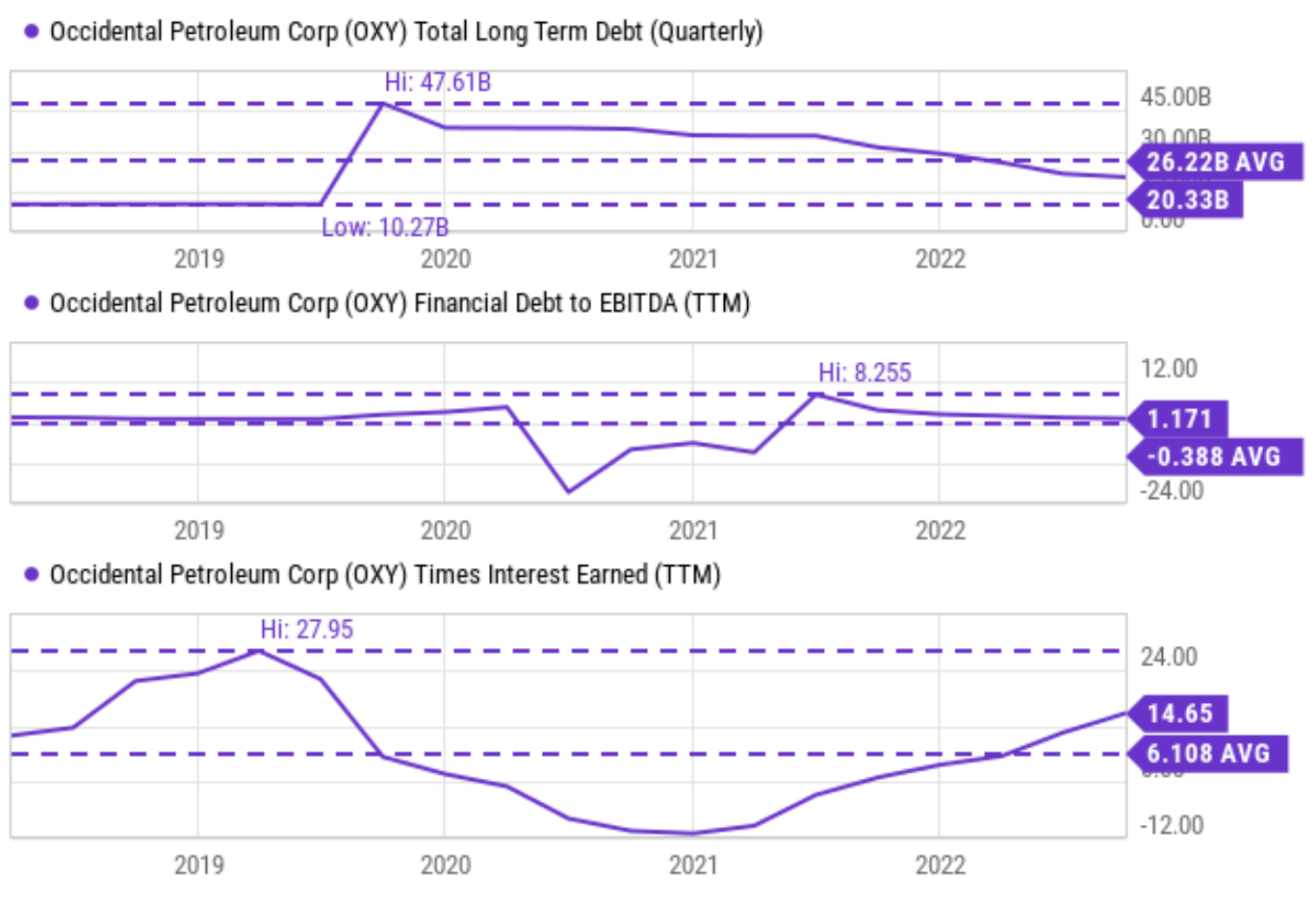

The 3rd part of the question would be a bit harder to answer a few years ago. But the answer is relatively clear cut under current conditions as you can see from the data shown below. OXY managed to improve its financial strength tremendously over the few years.

As you can see from the top panel, OXY was able to reduce its total debt by more than ½ since 2020, trimming it from $47B to the current $20B level. As a result, its current debt/EBITDA sits at a very conservative level of 1.17x only as seen from the middle panel. Thanks to the combination of debt reduction and improved earnings, OXY’s ability to service its debt is near a peak level in a decade. Its current interest coverage ratio is 14.6x as seen. It is not only more than twice higher than its 6.1x historical average. And it is also much higher than that of the overall economy (whose average interest coverage is also about 6~7x) despite the fact that energy companies, especially those with a midstream sector, typically leverage more than the overall economy.

Source: Seeking Alpha data.

OXY: does it have a strong dividend and growth record?

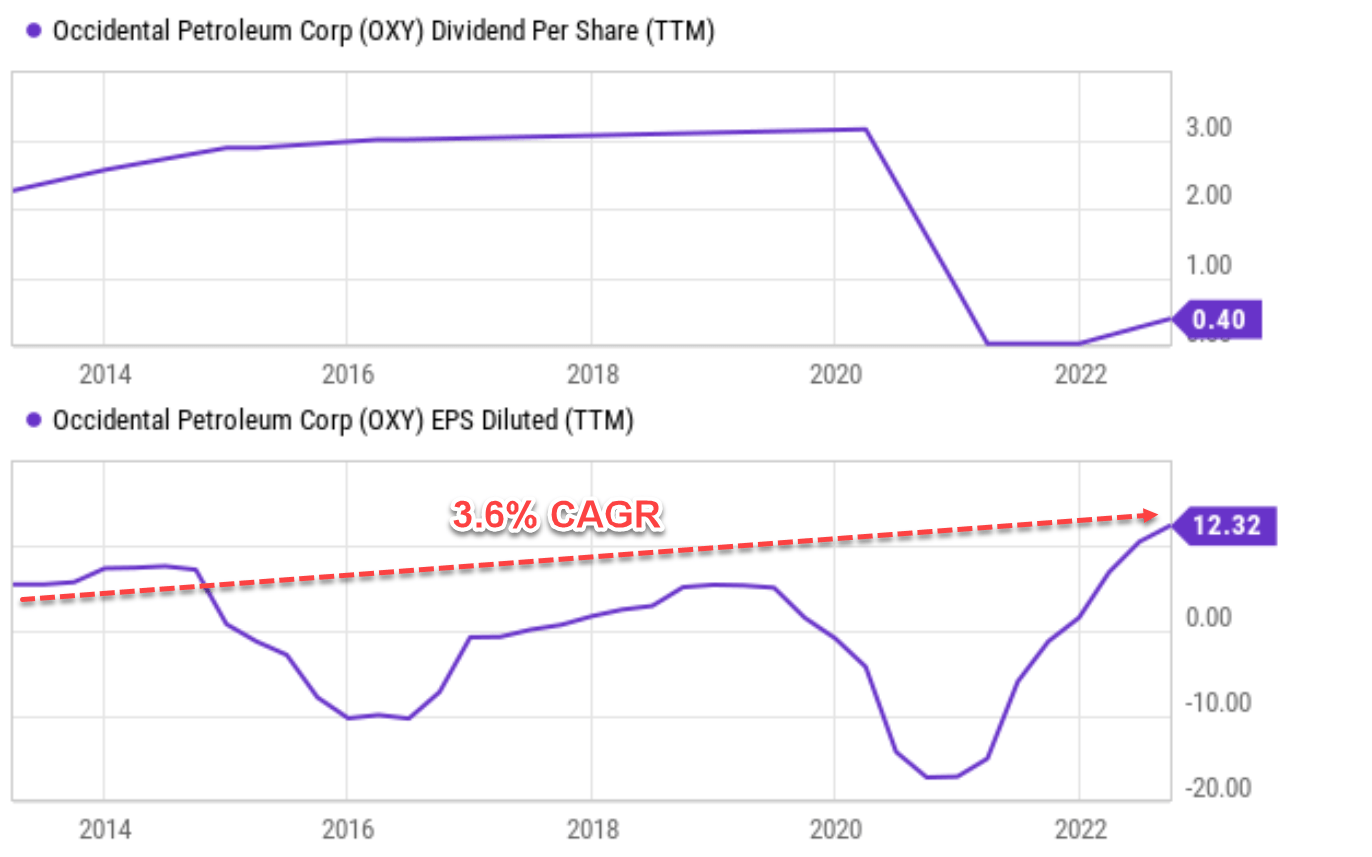

Let’s discuss the earnings growth question first as dividends are derived from earnings. As aforementioned, Graham’s guideline requires an EPS increase of 1/3 or more in 10 years. These numbers translate to about a 2.9% annual growth rate. OXY’s earnings growth is not consistent due to large fluctuations in commodity prices as seen in the chart below. However, when the fluctuations are averaged out, say over the past 10 years, roughly one whole business cycle, its EPS has grown at 3.6% CAGR, exceeding Graham’s requirement.

In terms of its dividend record, OXY has been paying out generous dividends in the long term, certainly meeting Graham’s requirement of 20 years of continuous dividend track record. However, investors need to bear in mind that its dividend payout fluctuates substantially together with its earnings as the following chart shows too. For example, in 2021, it had to reduce its quarterly payout from about $0.8 per share in 2020 to only 1 cent in 2021. Then it increased the quarterly dividend back to $0.13 per share in 2022.

Source: author based on Seeking Alpha data.

OXY: does it have a moderate valuation?

Finally, as also mentioned earlier,

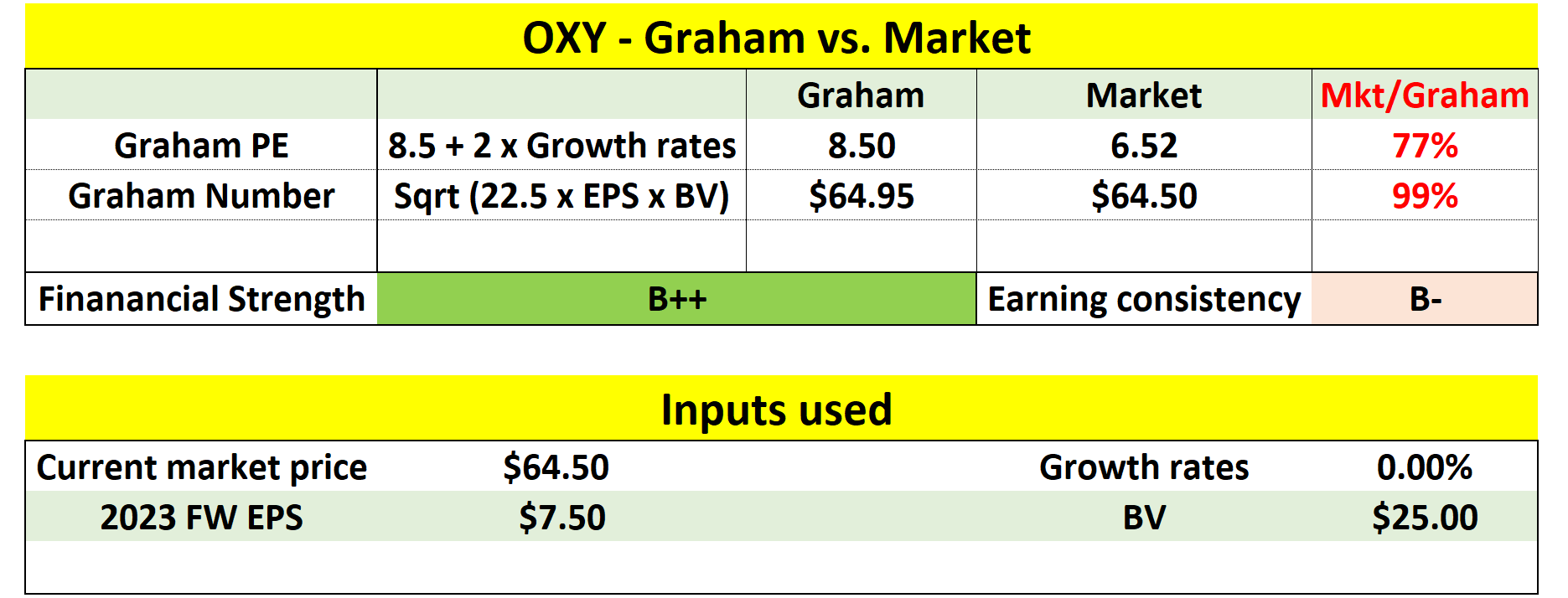

As a value investor to the core, Graham recommended a series of methods for investors to gauge the price they should pay. Here we will examine two of them (the other methods he recommended essentially paint the same picture). First, he recommended the PE for a defensive stock should be around 8.5 plus twice the expected annual growth rate, which I call the Graham PE. Hence, in his mind, a business that completely stagnates should be worth about 8.5x PE.

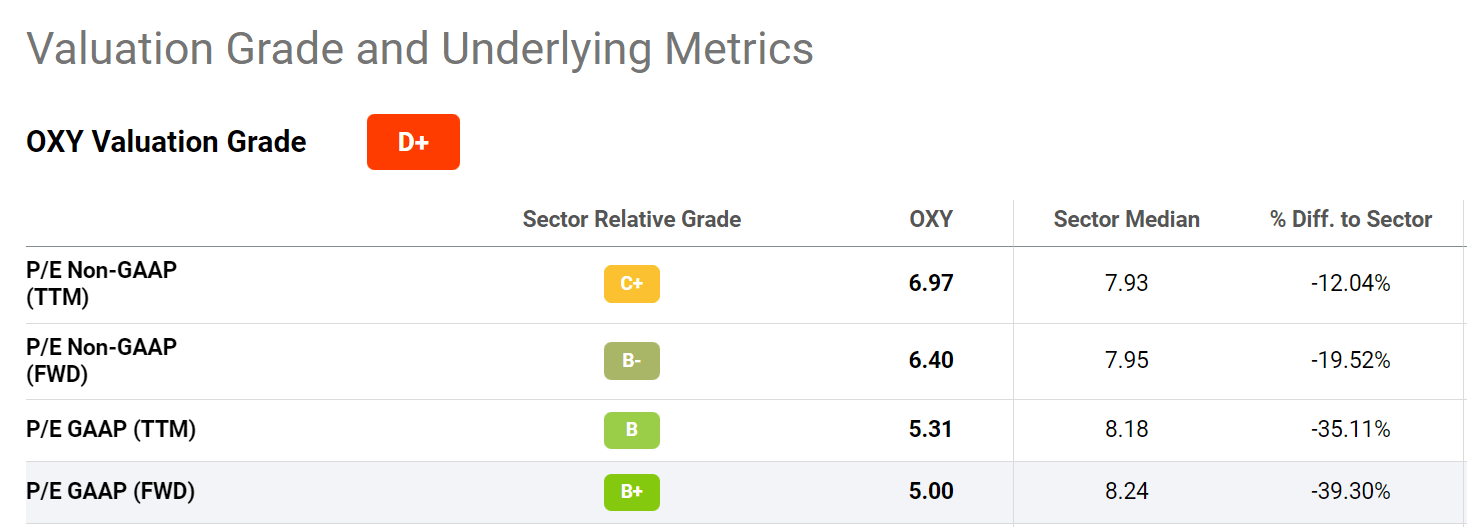

And in OXY’s case, I am projecting its EPS growth rates to be in the low-single-digit based on its return on capital employed (about 24%) and also reinvestment rate (about 10%). These analyses are detailed in my earlier article here. Assuming a 2.4% growth rate (24% ROCE * 10% reinvestment rate), the business should be priced around a P/E of 13x. Even assuming a 0% growth, the Graham P/E should be 8.5x. While the stock is currently trading at a P/E in the range of ~6x depending on which EPS metric you chose, a large discount off the Graham P/E.

Source: Seeking Alpha data.

Graham is certainly aware of the limitations of any valuation “rules”. Thus, he also developed other methods so he can cross-check and estimate the uncertainties. And here I’ll examine OXY’s valuation against an alternative metric, the so-called Graham Number:

In general, Graham cautions against paying a price of more than 15x times earnings or more than 1.5x times the book value (“BV”). However, a PE multiple above 15x could be justified if the P/BV ratio is lower than 1.5x. And vice versa. And as a result, the Graham number considers both the 15x PE limit and the 1.5x P/BV limit. More specifically, the Graham number is the square root of A) 22.5 (which equals 15 times 1.5), B) the EPS, and C) the book value.

My analyses of the Graham number for OXY are provided in the next table. All the financial information was either obtained from Seeking Alpha or Value Line as of this writing. As seen, OXY’s Graham number turned out to be $64.95 per share, remarkably close to its market price of $64.5.

Source: Author based on Seeking Alpha data

Risks and final thoughts

Investment in OXY does entail risks. As mentioned already, OXY is sensitive to commodity prices and its earnings and dividends can fluctuate substantially. To further compound the commodity price uncertainties, the current Russian/Ukraine situation can impact oil and natural gas prices tremendously depending on the duration and eventual outcome of the war. And finally, the market price of the stock most likely already includes what I call a Buffet premium given Buffett’s strong interest in the stock and the market’s interest in Buffett’s actions. These details are provided in our other articles. A possible way to minimize the impact of the Buffett premium, in our view, is to own OXY through BRK rather than directly owning OXY shares (if you do not mind owning other stuff that BRK holds).

To conclude, the thesis of this article is really simple. It is obvious that Buffett likes OXY very much. And my view is that his mentor, Ben Graham, would have liked the stock too. My results show that OXY is a perfect fit for each and every one of Graham’s timeless rules. In particular, the market valuation of the stock is at a large discount to the Graham P/E and close to the Graham number, signaling low valuation risks.

Be the first to comment