da-kuk

It’s been about 3 ½ months since I switched from being indifferent to being bullish on nVent Electric plc (NYSE:NVT), and in that time the shares have returned about 34% against a gain of 10.7% for the S&P 500. The company has just released financial results, and I want to review those, and compare them to the current valuation to see if it’s worth buying more, holding, or taking profits. As I start this analysis, I’ll admit that my bias is to preserve capital, and that I’m nervous about the state of the economy in general and stocks as an asset class in particular.

In each of my articles I offer a “thesis statement” paragraph for my readers. If you read my stuff regularly, you know that I’m absolutely obsessed with making your lives as pleasant as possible. One of the many ways I do this is with my thesis statement. These offer you the “gist” of my thinking up front so you can get in and then get out of the article before you’re exposed to too much of my tiresome bragging about a massive return like this one, for instance. You’re welcome. Although the company has generated great financial results recently, I think nVent Electric stock is now fairly valued. I don’t like the fact that new investors here are receiving a significantly lower cash flow than they would get from the risk free rate. For that reason, I’ll be taking my chips off the table at the earliest opportunity. I may very well lose further upside from current prices, but I would rather miss opportunity than risk losing capital. I’ve earned a nice return here, and I’m reminded of an old adage I heard years ago about investors: bulls make money, bears make money, pigs get slaughtered. This means that it’s foolhardy to try to suck every penny out of every trade. When it works out, take some profits and move on.

Financial Snapshot

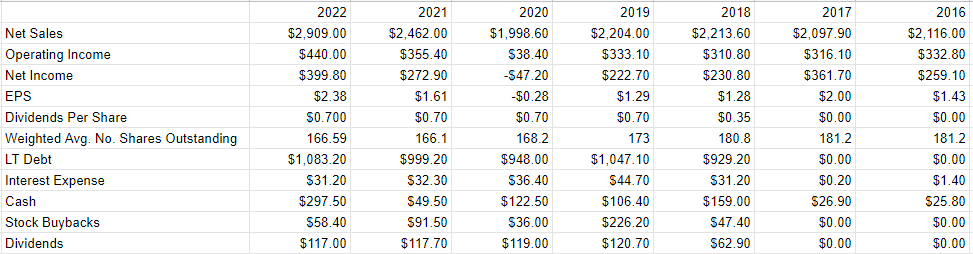

I think the latest financial results have been quite good here. The top and bottom lines in 2022 were up significantly when compared to 2021. Specifically, revenue was about 18% higher, and net income was up by a whopping 46.5%. When we compare the most recent period to the pre-pandemic era, a similar story emerges. Specifically, revenue and net income for 2022 was up by about 32%, and 79%, respectively. It seems to me that nVent is very much a “growth” company, as evidenced by the fact that net income has grown at a CAGR of about 6.4% over the past seven years.

Additionally, on the surface it looks as though the capital structure has deteriorated, but I think that view needs to be moderated somewhat. For example, long term debt has risen by $84 million over the past year, but cash on the balance sheet is up by $248 million. The upshot of this is that cash has gone from representing only about 5% of long term debt last year to about 27.5% of debt today. Add to that the fact that interest expenses have dropped by about $1.1 million, or 3.4%, and I think the balance sheet is actually a bit better now.

Although the dividend has remained frozen for a while now, I think it’s fair to say that it’s very well covered. For that reason, I’m very happy to buy more of this stock at the right price.

nVent Financials (nVent investor relations)

The Stock

As my regular readers know, I’ve talked myself out of some profitable trades with words like “at the right price.” Having made a nice return, I have previously sold some stocks too early before they continued to outperform. Additionally, I’ve avoided stocks that have gone on to perform very well. Some of my readers have criticized me for being excessively cautious, the idea being that if the stock price rises it’s a “good” investment, and missing out on that is a mistake. There are many responses to this relatively simplistic view, but in general I’d point out that I’m of the view that it’s better to miss out on some gains than lose capital. My regulars also know that I consider the “business” and the “stock” to be quite different things. Every business buys a number of inputs and turns them into a final product or service, like electrical connection and protection products worldwide, for instance. The stock, on the other hand, is an ownership stake in the business that gets traded around in a market that aggregates the crowd’s rapidly changing views about the future health of the business, future demand for electric products, and so on. The stock also moves around because it gets taken along for the ride when the crowd changes its views about “the market” in general. A reasonable sounding, if counterfactual, argument can be made to suggest that some portion of the bump in the value of nVent shares relates to the rise in the S&P 500 itself since I bought. It’s impossible to prove this point definitively, but it’s worth considering. In any case, the stock is affected by a host of variables that may be only peripherally related to the health of the business, and that can be frustrating.

This stock price volatility driven by all these factors is troublesome, but it’s a potential source of profit because these price movements have the potential to create a disconnect between market expectations and subsequent reality. I absolutely hate to remind you about my great performance here, but playing on this disconnect between expectation and reality is exactly how I generated a great market beating return on my nVent investment over the past 3 ½ months. The market was overly pessimistic, and I took advantage of that. I don’t want to be too repetitive, but in my view this is the only way to generate profits trading stocks: by determining the crowd’s expectations about a given company’s performance, spotting discrepancies between those assumptions and stock price, and placing a trade accordingly. I’ve also found it’s the case that investors do better/less badly when they buy shares that are relatively cheap, because cheap shares correlate with low expectations. Cheap shares are insulated from the buffeting that more expensive shares are hit by.

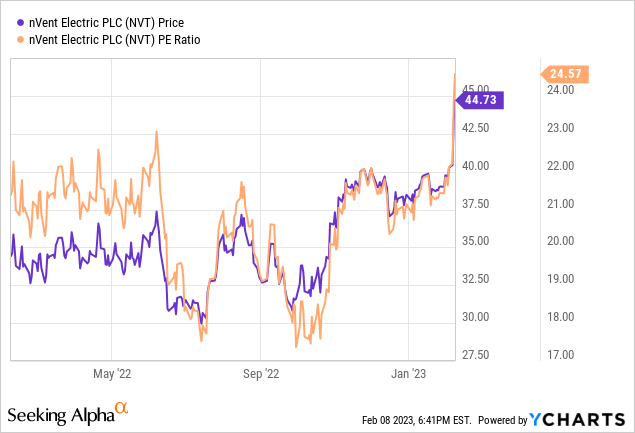

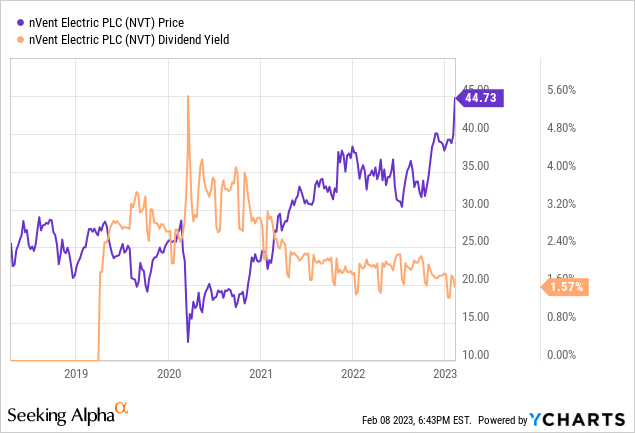

As my regulars know, I measure the relative cheapness of a stock in a few ways, ranging from the simple to the more complex. For example, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. I like to see a company trading at a discount to both the overall market, and to its own history. In case you don’t have your copy of “Doyle’s Almanac of 2022 Trades” in front of you, I turned very bullish on this stock when it was trading at a PE of about 19.4, and the dividend yield was about 2.11%. The shares are now about 26% higher, and the dividend yield is about 25% lower, per the following:

In my view, paying more and getting less is not great in my view. I also don’t like the fact that the current dividend yield is over 200 basis points lower than it is on the risk free 10 Year Treasury Note. One more thing my regulars know is that I want to try to understand what the crowd is currently “assuming” about the future of a given company, and in order to do this, I rely on the work of Professor Stephen Penman and his book “Accounting for Value.” In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit dense, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Anyway, applying this approach to nVent at the moment suggests the market is assuming that this company will grow profits at a rate of about 6.5% from here. In my view, that is a pretty optimistic forecast. Even though the company has managed to grow at this rate over the past seven years, I think growth inevitably slows. I’m of the view that on a long enough timeline, profits in aggregate can’t grow at a faster rate than the overall economy, so 6.5% is too rich for my blood. Given the above, I’m taking my profits at this point.

Be the first to comment