coward_lion/iStock via Getty Images

Summary

NIO Inc (NYSE:NIO) presented full-year earnings on Thursday the 24th after market close, which prompted a sell-off in post-market trading which extended into Friday. Since then the stock has recovered somewhat, and although investors were disappointed with guidance, institutions and investors are backing the stock, including Cathie Wood, who recently added NIO to her ARK Autonomous Technology & Robotics ETF fund (ARKQ)

The company beat revenue estimates but missed on GAAP EPS. The company estimates Q1 deliveries will be around 25-26K, with revenues expected to come in at $1,511-$1,567M. The average analyst consensus before that stood at $1.65M.

What was encouraging was the expansion in vehicle margin, and NIO also recently made the first deliveries of the much-awaited ET7. Before we get into how the recent results alter our valuation on NIO, let’s discuss some of the insights from the earnings call.-

Takeaway from the Earnings Call

In this section, I will review the most relevant points from the earnings call. I have divided this into three sections; Growth, Profitability and Challenges.

Growth

Despite the disappointing guidance, there are plenty of things to get excited about. Overall, the EV market is growing at a fast rate. The China Passenger Car Association estimated the battery electric vehicle penetration rate from 5.9% in January to 18.6% in December of last year. This rate was even higher in big cities like Shanghai.

To grow, NIO has to increase its production capacity, and this was discussed in depth in the earnings call. According to William Li, NIO has almost completed the construction of its F2 manufacturing facility in the NeoPark. With both factories up and running, production should come in at 240,000 units per year.

NIO will need this extra capacity to accommodate international demand and demand for the ET7. According to NIO, the ES8 has ranked second in sales in the category of 6 and 7 passenger vehicles. Li refused to give exact numbers for the ET7 but did state that pre-orders were much higher than the 5000 stated in a recent media report, so that is encouraging.

Lastly, NIO continues to expand its presence worldwide, with a confirmed 46 NIO houses and 341 NIO spaces in 155 cities all over the world.

All in all, while NIO’s CEO did acknowledge that European demand would be slow to pick up, NIO is laying the foundation for future growth, and its newest models will keep demand up in the near term.

Profitability

While NIO pursues growth, profitability is taking the backseat. In the last quarter, NIO accomplished a 20.9% vehicle margin, but this is expected to come down. The target for 2022 is 18-20%. Also, NIO has significant R&D and SG&A expenses, and it is still spending cash on expanding its infrastructure and service offering, which hurts profitability.

For now, the main objective is to have gross profit cover the SG&A costs. However, it was stated in the earnings call that break-even could be reached by 2024.

Profitability is also being challenged by supply shortages of certain materials and components. I will discuss this more in-depth in the next section.

Challenges

Of course, we can’t just focus on the positives, and we have to acknowledge that NIO faces some headwinds moving into 2022.

For the ET7 product ramp-up, because the ET7 is going to be manufactured in the first factory we called F1 and they’re going to share the production line with the current product ES8, ES6 and EC6, at the same time we will also introduce some new manufacturing technologies and techniques in the production of ET7. So that’s why, starting from last year, we started to adjust the production lines in the F1 to support the new product production.

Source: Earnings Call

This process already caused production delays last year, and it could cause problems moving forwards due to its complexity.

NIO will also have to deal with inflation in some of its inputs. Aluminium and copper are highlighted in the earnings call. This is one of the reasons the vehicle margin is projected to be lower. For the time being, NIO does not intend to raise its prices though.

Lastly, NIO is also exposed to the ongoing worldwide chip shortage. Each NIO car needs around 1000 chips, and according to William Li “around 10% of the chips may face supply shortages or challenges from time to time.” NIO has a strategic partnership with manufacturers like Qualcomm Incorporated (QCOM) and NVIDIA Corporation (NVDA), but getting chips will still prove challenging in 2022.

Valuation

Using the latest data, we have updated our forecast and target price for NIO, from around $58 per share to around $42 per share. This type of company’s valuation is very sensitive to changes, as we are talking about very long-term expectations of very high growth and the company is valued in terms of where it can be in many years.

Using a forecast of revenue, the number of shares, the price to sales ratio and an appropriate discount rate, we have produced a target price based on an average of where we expect the company to be in 5 and 10 years.

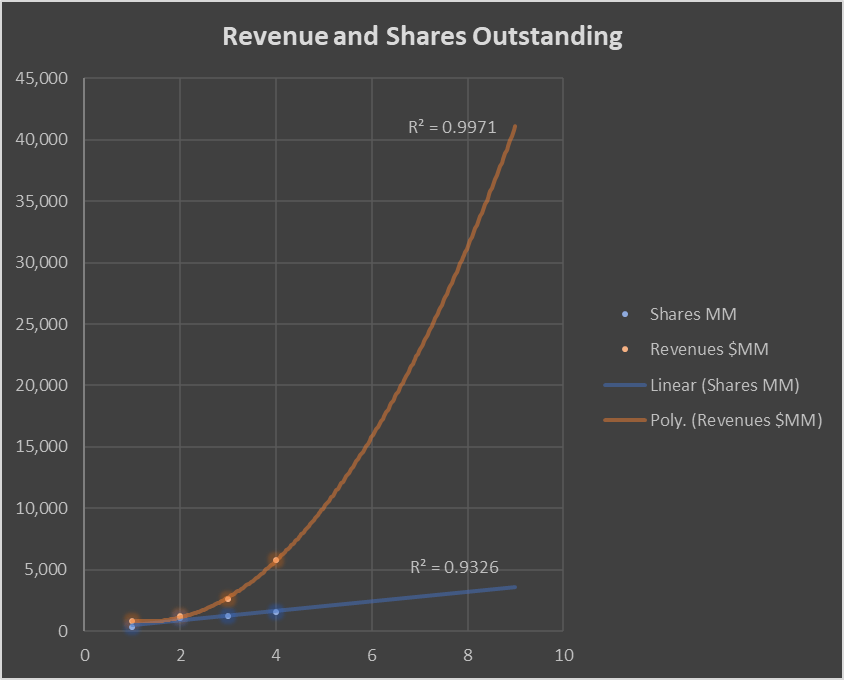

Our forecasted revenue per share is $11.59 in five years and $20.14 in ten years. This is based on the trends observed so far in total revenues and the number of shares outstanding. You can see a visual representation of our assumptions in the following chart, where values 1 to 4 on the horizontal axis represent years 2018 to 2021. The orange line is the polynomial trend that revenues follow, and the blue line is the linear trend that the number of shares outstanding follows. In each case, you can see the function and the measure of fit (out of 1)

NIO Revenues and Shares (Author’s work)

Source: Author’s work

Once you apply the functions, the specific forecasted figures are $41bn revenue for 3.5 million shares in 2026 and $110bn revenue for 5.5 million shares in 2031. This represents a revenue CAGR of 34% over the next 10 years, with a growth rate of 74% in 2022 falling progressively to 18% in 2031. To give you an idea of where we are compared to consensus estimates, our revenue forecast of $10.08bn in 2022 is 4% higher than estimates and our 2023% forecast of $15.8bn is 2% higher.

The next step is to decide the price to sales ratio we apply. We have applied a PS ratio of 6. This is almost the same as the current one, which is 6.07 if we take 2021 sales. We have taken into account how companies in the sector are valued depending on their growth rates.

Using the PS ratio and revenue per share forecast, we can try to predict the share price in 5 and 10 years. All we need to do after that is apply an appropriate discount rate so that we can decide how much it should be worth today. In this case, we are using a discount rate of 10.69%. The elements we consider when choosing a discount rate are the forecasted level of debt, forecasted growth, and the measure of fit, and we have a particular function that we have developed over time.

NIO’s declared net debt at the end of 2021 was a negative 90% of revenue, and this is set to increase by our forecasting method. This pushes the discount rate down, as the risk of bankruptcy is very low, and it eliminates the need for borrowing. On the other hand, the growth required to fulfil this valuation (34% CAGR) is very high, which increases the risk of underperforming and makes the required return higher.

The measure of fit (0.66) is an average of the R2 values of the trendlines we use to make the forecast. You can see the examples of revenue and number of shares in the previous chart, but this also includes items related to profitability and the balance sheet. We consider this an indicator of how reliable the forecast is, and we increase the discount rate proportionally when it is below average, which is around 0.70.

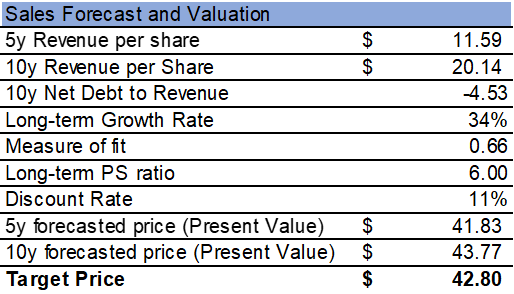

Taking all these elements into account, our price target comes up to $42.80. You can see a summary of the figures here:

NIO Price Forecast (Author’s work)

Source: Author’s work

This forecast is of course purely based on revenue growth. Valuing a young and fast-growing company like NIO has its limitations, and the valuation is more sensitive to small changes. As we have seen this earnings season, growth companies can be very volatile when growth expectations aren’t met, or when the macroeconomic environment changes.

In the case of NIO, we are confident in our calculations on revenue and share count, and we are especially encouraged after NIO released record Q1 deliveries. The current environment is also improving, with China signalling that they are willing to cooperate on regulation and the PBOC easing monetary policy.

The 5-year forecast shown above is, if anything, conservative, considering that NIO has historically traded at a PS of over 12.

Takeaway

After all, the price target of $42.80 represents a more cautious expectation of growth in the very long term and acknowledges the increased perception of challenges that I discussed above. However, this is still a 100% gain on the current price, so we still strongly believe in the upside for NIO and remain long despite the risks.

Be the first to comment