RHJ

NexGen Energy (NYSE:NXE) is a company that started off with the exploration and development of Uranium properties in Canada but currently focused on turning one of their discoveries into the largest low cost producing mine globally. They also have a full portfolio of discoveries in the Athabasca region of Saskatchewan, Canada. Mining and exploration companies are one of the worst industries to be invested in with only a handful of companies actually advancing from exploration stage to production stage (Visualizing the Life Cycle of a Mineral Discovery – Visual Capitalist)

With big discoveries already under its belt, in this thesis, I will try to present analysis on how this company could be a winner over any time frame.

A world that wants the cake and eat it too

It is unrealistic to expect that the growing energy needs of the world will be met only by conventional energy and/or renewable energy sources while sticking to emissions targets. Development of a country is closely tied to its fossil energy use and this is a concept apparently most find hard to grasp. As you try to move more people out of poverty to a higher standard of living, energy use increases substantially.

- This interactive map shows how the energy use per capita is tied to share in extreme poverty over the last 50 years

-

This interactive map shows how fossil fuel consumption has changed for the countries over the last 50 years (Notice how the most prominent countries that reduced their poverty levels show increased fossil fuel consumption over the years)

-

This interactive map shows the changing energy use per person over the last 50 years

As countries follow this trajectory, energy consumption will increase and if you throw emissions caveat in the mix, it is impossible for this balance (Increase standard of living while sticking to emissions targets) to occur while only counting on renewables (Not to mention the debate on how much environmental impact renewables actually have)

Enter Uranium

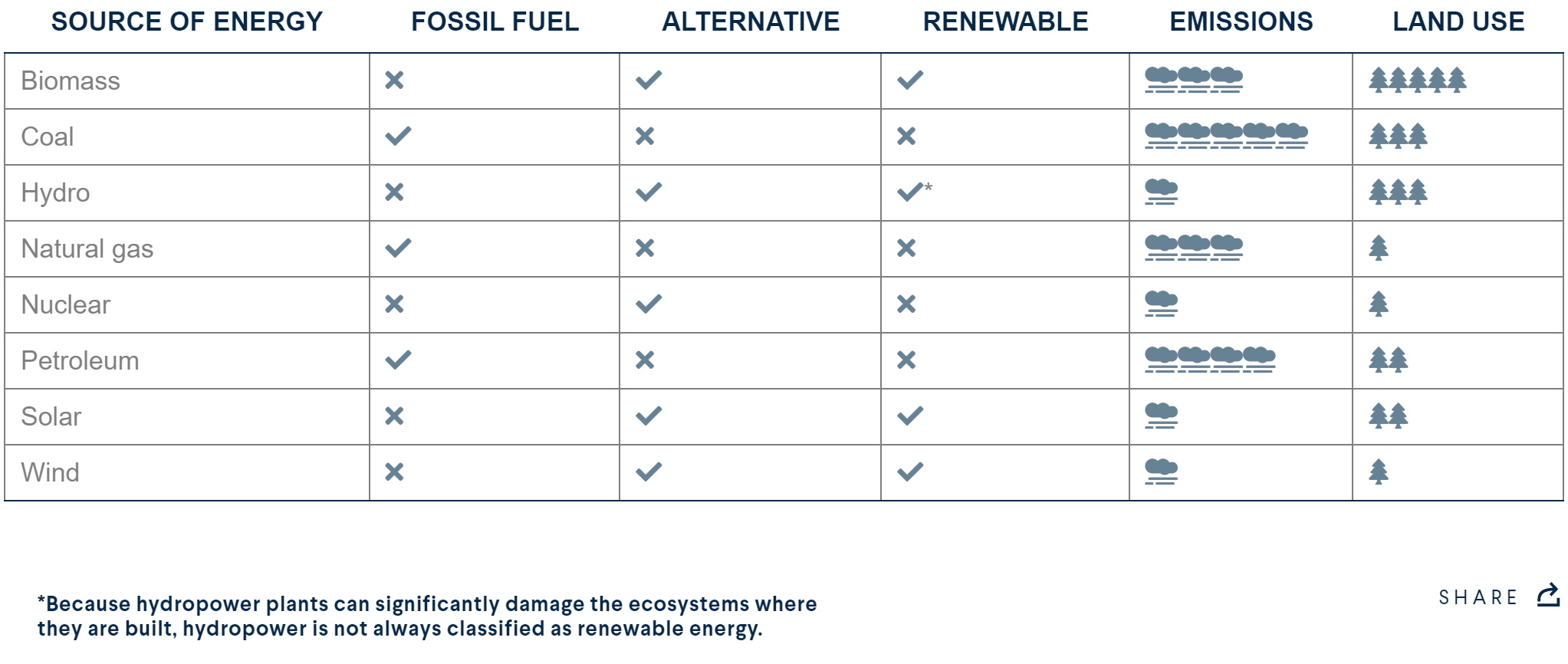

1) Nuclear industry is the only energy industry that can check several boxes – Reliable, high capacity and ability to add additional capacity, low emissions, large scale output and low land use (Sources of Energy: A Comparison)

Comparison of different Energy sources (World101)

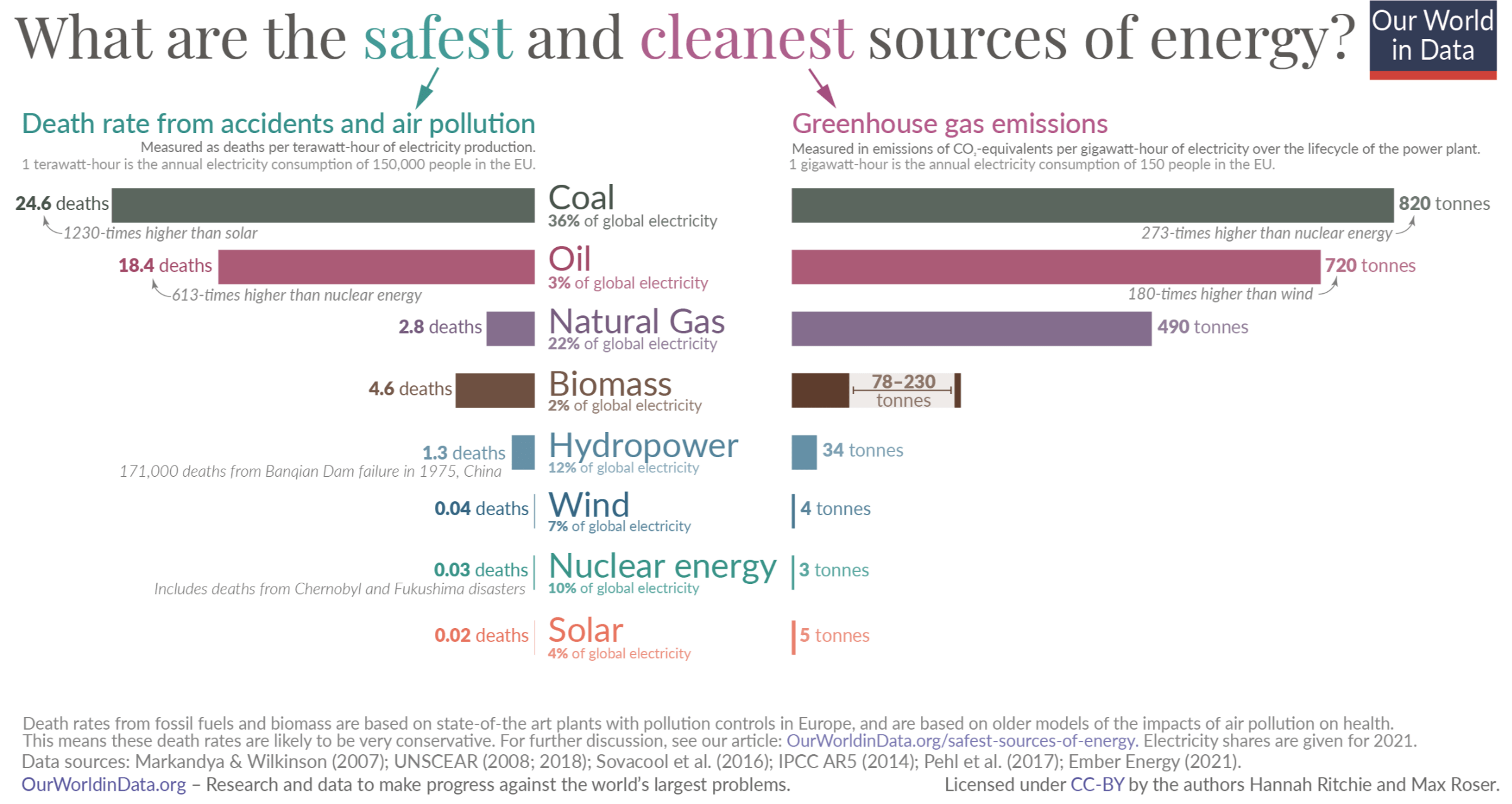

2) One of the safest and cleanest sources of energy

Safe and clean sources of energy (Our world in Data)

3) Has stable costs – Fuel costs for nuclear plants make up a small amount of generating costs, fluctuations in the market price of uranium have little effect on the cost of nuclear power

Demand & Supply

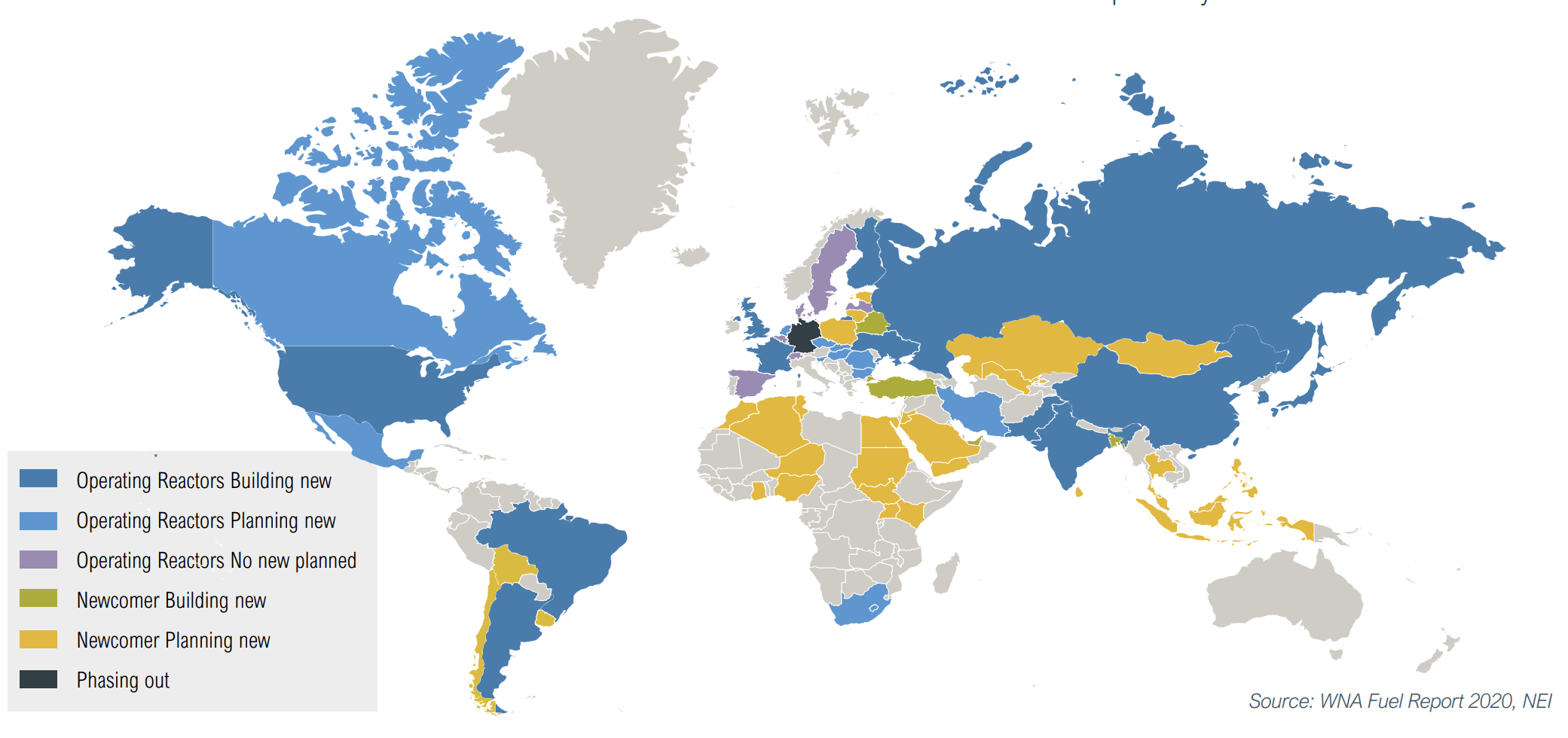

Key developed markets have announced plans to continue their fleet and emerging markets are going to be the drivers of new demand. According to the WNA, in October 2022 there were 59 reactors in construction, 100 reactors planned and 334 proposed. China is the fastest growing market for nuclear power planning to build more plants in the next 15 years than the rest of the world built over the last 40 years.

Reactor Planning (WNA Fuel Report)

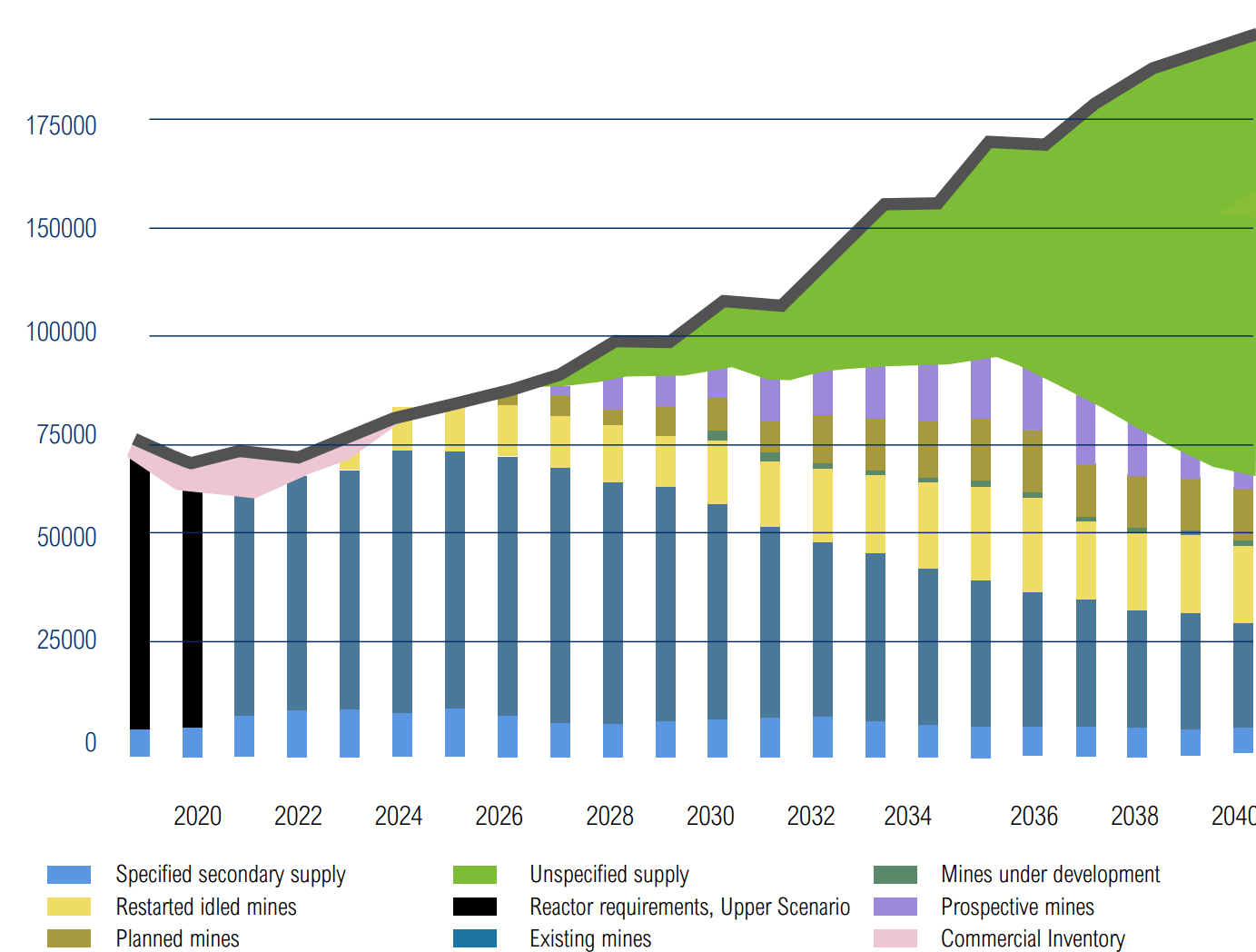

When it comes to Uranium supply, it has suffered in the last ten years due to several reasons –

- Prolonged bear market has resulted in significant under investment in the last 10 years with no incentive to explore or develop new mines

- Mines have been depleted and supply shortfall of about 40 million pounds was met with inventories from all over the globe

- Global average grade of Uranium is uneconomical to mine at prices we have seen over the last decade and for mining to be ‘economical‘ it requires >50% rise in prices from current levels

- UxC – Nuclear Industry’s leading market researcher estimates 100Mlbs supply deficit by 2030 without accounting for any demand from resurgence of interest from Japan, South Korea etc.

Enter NexGen

1) Supply deficit expected to be three times NexGen’s average volume by 2030

Demand Line V Supply (NexGen Investor Report)

2) Planned production from NexGen’s assets could represent a significant portion (15-20%) of global production. Rook I Project owned by the company is the largest development-stage uranium deposit in the world.

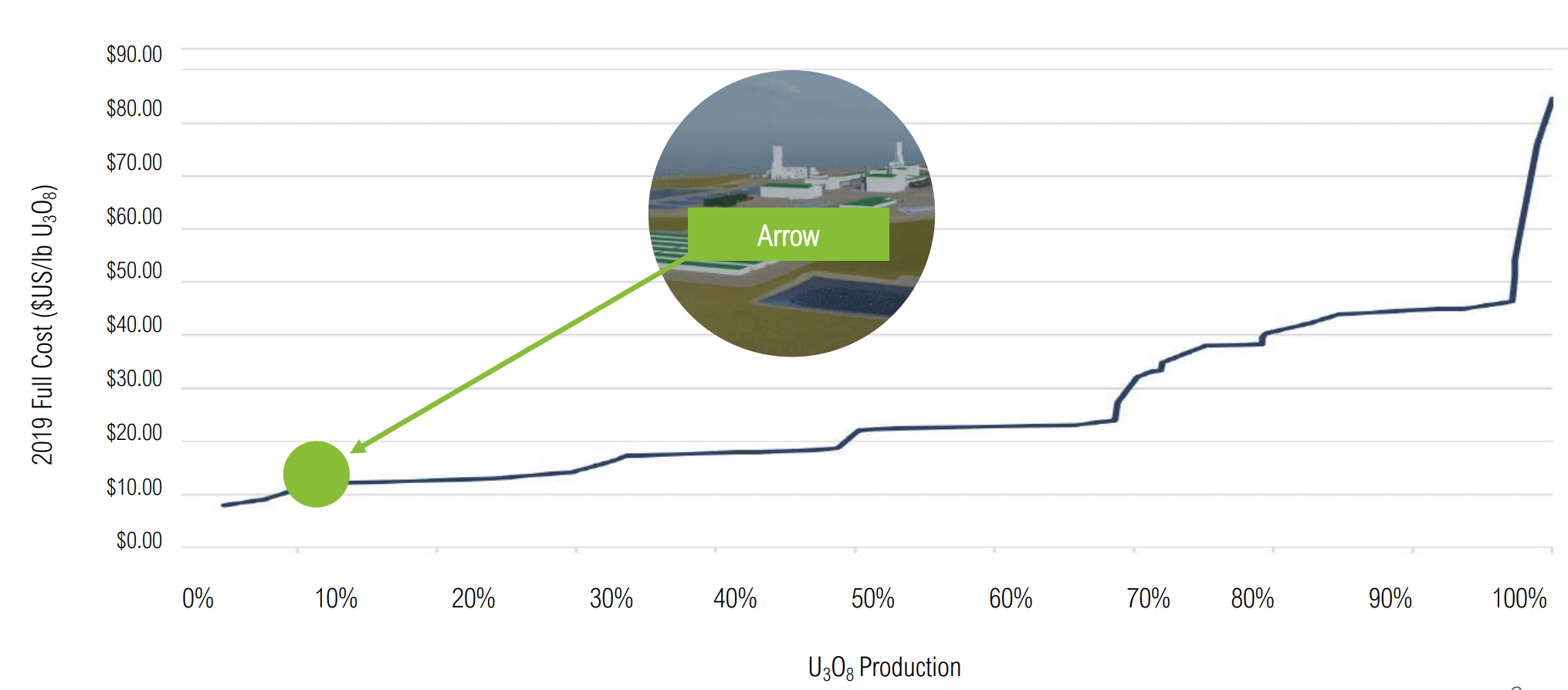

3) Owns top quality assets with one of the highest-grade deposits and extremely low productions costs

Uranium Production Costs (UxC)

3) Assets are expected to last multiple decades and amongst the world’s best mining jurisdictions (Saskatchewan, Canada)

4) Against an initial expenditure of $1.3B, it projects an average annual after-tax net cash flow of $1B for the first 5 years (Assuming a conservative US$50/lb. of shipped Uranium)

5) Average contracting price during last contracting cycle was US$75/lb. At this price it expects $2.5B average annual EBITDA during the first 5 years of production

For a pre-revenue company what does their balance sheet look like? Can they survive before they go into production?

From a quick glance following things are clear –

- They have enough cash or current assets to cover all their debt and liabilities

- Total liabilities of $70MM which includes $54M of long-term debt against a total equity of $325M which gives us a low Debt to Equity profile

- At its current burn rate they have more than sufficient cash to survive and fund their operations till they get into production

- Expenditure to bring their first mine into production would exceed $1B, at which point, they will have to raise outside capital. With their current roster of high profile investors, this does not seem to be a problem.

Now to the main event!

For a mining company still in early stages of its development, it may take several years for their prime property to become fully operational. So, let us examine three scenarios for an investor buying shares in this company.

Base Case

In this scenario we say that price of the Uranium stays at its current rate or even goes down and stays at a low rate of US$30 – $40/lb. for the next several years. This case would account for all industry risks being factored in (Ex: Another Fukushima type disaster that turns the tide against Uranium).

At a low production cost of less than US $20/lb., company could still be doing much better than operational mines from other companies. An investor buying now would have to hold this investment for a longer duration with the stock price slowly ticking higher over the years ramping into production and at some point see a big bump in valuation.

Moderately optimistic case

Increasing Supply constraints along with widening demand gap pushes the price of Uranium. Since the price of Uranium stocks are closely correlated to price of Uranium, we start seeing NXE tick higher much before production. Investors buying now could choose to get a good exit much earlier. There is also a possibility that bigger rivals find the valuation attractive enough to make an acquisition offer that would greatly benefit existing shareholders.

Highly Optimistic

This is an extension of the moderately optimistic case. Driven by supply and demand, price of the Uranium can get speculative which may provide a massive boost to underlying Uranium mining stocks. This wouldn’t be entirely new. Commodity stocks have undergone speculative frenzies before. Since NexGen has the largest development stage deposit in the world it may be one the biggest beneficiaries of a speculative environment.

Valuation

It is extremely hard to value pre-revenue companies (in case of NexGen, we won’t see revenue for next several years) without it coming across as “pie in the sky” valuation. Let us use the data provided by the company and see where we land. From company data of base case Uranium price at US $50/lb. and an after tax NPV of CAD 3.5B we can say it is currently trading at close to 1x NAV which looks fair against comps.

Forward EV/EBITDA

This one is trickier as we are trying to compute this for something way out in the future. From Seeking Alpha webpage we see that current EV is at $2.08B. We also know from NexGen’s investor presentations that the company requires another $1.3B to bring the first mine into production. Assuming worst case cost overruns of up to 100% and adding this as a debt to the current EV we would arrive at EV of $4.7B. At a base case Uranium price of US50$ /lb. NexGen estimates average annual EBITDA to be $1.6B during the first five years. This would give the EV to EBITDA multiple at 3 (For comparison CCJ’s present multiple is at 29) This makes the stock look extremely undervalued.

I do want to warn the reader to take this valuation with a grain of salt. A lot of things can change between now and production, and since the production is still a couple of years away, this method of valuation would not be entirely reliable by itself.

The most important takeaway point here is that even accounting for errors in this method of valuation the nearest comparable looks miles away. At its base case scenario this would still be a winner in the long term as more investors pour in looking at the progress of this company.

My current plan is to buy shares of this company, be patient for any of the three scenarios to play out and take an exit in batches for the next several years.

Be the first to comment